Securing a mortgage is a significant financial milestone, and for many, it’s a journey shrouded in mystery. You’ve likely heard the common wisdom: lenders care about your credit score, income, and debt. While these are undeniably crucial, the modern mortgage application process is far more nuanced, influenced by the very trends shaping our digital world. From the underlying technology of underwriting to the branding of financial institutions and the intricate world of personal and business finance, mortgage lenders examine a comprehensive picture of your financial health and your ability to repay. This article will delve beyond the basics, exploring what mortgage lenders truly look at through the lens of technology, brand perception, and multifaceted financial considerations.

The Tech Behind the Trust: How Technology Underpins Mortgage Lending

The days of purely manual underwriting are largely behind us. Today, sophisticated technology plays a pivotal role in how mortgage lenders assess risk and streamline the application process. This isn’t just about faster approvals; it’s about more accurate assessments and a more transparent experience for borrowers.

AI and Automation: The New Underwriters

Artificial intelligence (AI) and automation are revolutionizing the mortgage industry. These tools are employed across various stages of the lending process:

- Automated Underwriting Systems (AUS): Lenders utilize sophisticated AUS platforms that analyze a vast array of borrower data in real-time. These systems go beyond simple credit score checks, incorporating algorithms that can identify complex patterns and predict repayment likelihood with a higher degree of accuracy. They can process application information, verify income and employment, and assess debt-to-income ratios much faster and more consistently than human underwriters alone.

- Data Analytics and Predictive Modeling: Lenders leverage big data analytics to understand market trends, identify potential risks, and even personalize loan offerings. Predictive models, powered by AI, can forecast borrower behavior, assess the risk of default based on historical data and economic indicators, and even flag potential fraudulent activity. This allows lenders to make more informed decisions and manage their portfolios more effectively.

- Digital Document Verification: Gone are the days of mountains of paper. Modern lenders rely on optical character recognition (OCR) and AI-powered tools to quickly and accurately extract information from uploaded documents such as pay stubs, bank statements, and tax returns. This not only speeds up the process but also reduces the potential for human error in data entry.

- Fraud Detection Software: In an increasingly digital landscape, fraud is a persistent concern. Lenders employ advanced software that uses AI and machine learning to detect anomalies, inconsistencies, and potential fraudulent patterns in applications and supporting documents. This protects both the lender and legitimate borrowers from financial harm.

- Blockchain Technology: While still emerging, blockchain technology holds promise for the mortgage industry. Its inherent security and transparency could be used for secure record-keeping of property titles, loan origination data, and transaction histories, potentially reducing fraud and streamlining the entire mortgage lifecycle.

The Borrower’s Digital Footprint: Beyond Credit Reports

While your credit report remains a cornerstone of your mortgage application, lenders are increasingly aware of your broader digital footprint. This doesn’t mean they’re actively digging through your social media (though some regulatory bodies might have stipulations about this), but rather how your online interactions and financial habits can be indirectly assessed.

- Digital Identity Verification: Lenders use sophisticated tools to verify your identity electronically, often comparing the information you provide with public records and other digital sources. This helps prevent identity theft and ensures that the applicant is who they claim to be.

- Online Financial Management Tools: Lenders may observe how you manage your finances online. While they won’t directly access your personal banking apps, the way you present your financial history through statements and the patterns of your spending and saving, as reflected in those statements, provide insights. Lenders are looking for evidence of financial responsibility and stability.

- App Usage and Digital Presence (Indirectly): Certain financial apps and platforms that you use to manage your money or investments, while private, contribute to the overall digital record of your financial life. For instance, consistently using budgeting apps and demonstrating responsible financial habits within those platforms (as evidenced by your bank statements) can indirectly contribute to a positive financial picture. Lenders are interested in your financial discipline, which is often reflected in how you engage with digital financial tools.

Brand Perception and Lender Trust: More Than Just a Name

The “Brand” aspect of a lender’s evaluation extends beyond just their company logo. It encompasses their reputation, their approach to customer service, their market position, and the trust they inspire in the financial ecosystem. For borrowers, understanding this can influence their choice of lender and how they are perceived throughout the application process.

The Lender’s Brand: Building Trust and Reputation

Lenders invest heavily in their brand for several reasons, all of which indirectly impact borrowers:

- Reputation and Stability: A strong brand is built on a foundation of trust and reliability. Lenders with a positive reputation and a history of sound financial practices are perceived as more stable and less risky. This can influence their ability to secure capital and offer competitive rates.

- Marketing and Customer Acquisition: Effective branding helps lenders attract a wider pool of applicants. Their marketing strategies, including online presence, content creation, and social media engagement, communicate their values, their product offerings, and their commitment to customer service.

- Technological Innovation as Brand Differentiator: Lenders that embrace new technologies, like AI-powered loan origination platforms or user-friendly mobile apps, often position themselves as innovative and customer-centric. This can be a significant draw for tech-savvy borrowers.

- Case Studies and Track Record: A lender’s success stories, often presented as case studies on their websites or in marketing materials, highlight their ability to help diverse borrowers achieve homeownership. This builds confidence in their process and their understanding of individual needs.

- Corporate Identity and Values: A lender’s stated corporate identity and values can signal their approach to lending. Do they emphasize ethical practices? Do they support community initiatives? While not directly quantifiable for a borrower’s application, these aspects contribute to the overall perception of the institution.

The Borrower’s Personal Brand: Presenting a Credible Image

While you don’t need a formal “personal brand” to get a mortgage, the principles of branding apply to how you present yourself as a borrower. Lenders are assessing your credibility and your financial responsibility, and your presentation matters.

- Professionalism in Communication: Clear, concise, and professional communication throughout the application process is crucial. This includes how you interact with loan officers, how you respond to requests for information, and the overall tone of your correspondence.

- Consistency in Financial Storytelling: Your financial history should tell a consistent and believable story. Wild fluctuations in income, unexplained large deposits or withdrawals, or a sudden shift in spending habits can raise red flags. Lenders want to see a steady, responsible approach to managing money.

- Digital Presence and Professionalism (Indirectly): While lenders aren’t browsing your Instagram, a professional online presence can indirectly reinforce your credibility. For example, if you’re self-employed, a well-maintained professional LinkedIn profile or a business website can add to your perceived stability.

- Demonstrating Financial Literacy: By asking informed questions and showing an understanding of the mortgage process and your financial obligations, you project an image of financial literacy and preparedness, which lenders appreciate.

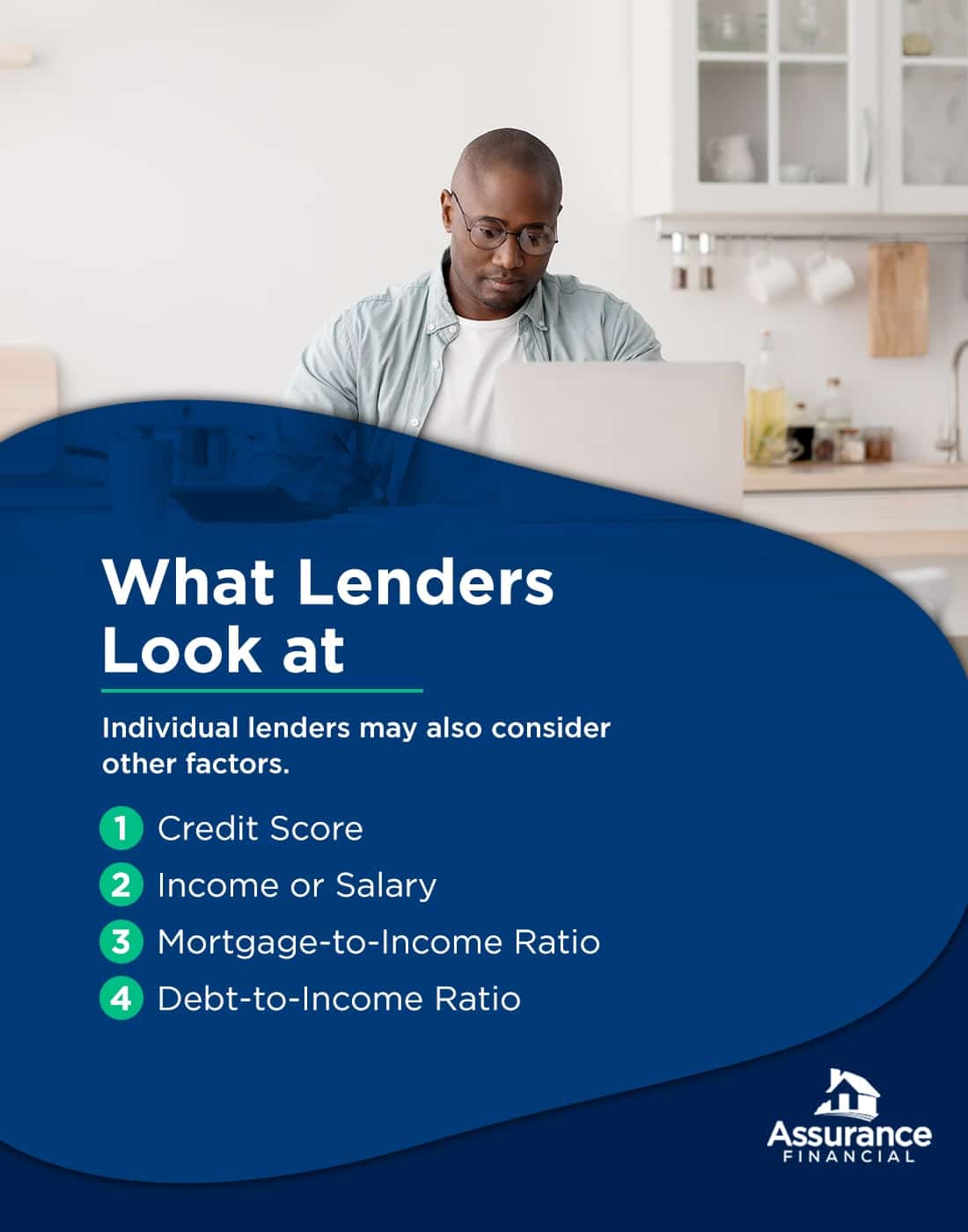

The Pillars of Financial Assessment: Money Matters Most

At its core, mortgage lending is about money. Lenders need to be confident that you have the financial capacity to repay the loan over its entire term. This involves a deep dive into your income, assets, debts, and overall financial stability.

Income Verification: Proving Your Earning Power

Lenders need to verify that your income is stable, consistent, and sufficient to cover your mortgage payments. The specifics vary depending on your employment situation.

- W-2 Employees: For those employed by a company, lenders will typically request recent pay stubs, W-2 forms from the past two years, and potentially employment verification calls to your employer. They look for consistency in your salary and any overtime or bonuses. Significant changes or gaps in employment can be a cause for concern.

- Self-Employed and Business Owners: This category requires more thorough documentation. Lenders will scrutinize tax returns (usually for the past two years), profit and loss statements, balance sheets, and bank statements. They want to see a consistent and profitable business. They will also look for a clear understanding of your business’s financial health and your personal draw from the business.

- Other Income Sources: If you rely on other income streams such as rental properties, investments, or alimony, you’ll need to provide documentation to support these. This could include lease agreements, investment statements, or court orders.

Debt-to-Income Ratio (DTI): Your Financial Balancing Act

Your Debt-to-Income ratio is a critical metric that lenders use to assess your ability to manage monthly payments. It compares your total monthly debt obligations (including the proposed mortgage payment) to your gross monthly income.

- Front-End DTI (Housing Ratio): This ratio focuses solely on your housing costs (principal, interest, taxes, and insurance) and compares it to your gross monthly income.

- Back-End DTI (Total Debt Ratio): This is the more commonly cited DTI. It includes all your monthly debt obligations – credit cards, car loans, student loans, personal loans, and the proposed mortgage payment – as a percentage of your gross monthly income. Lenders have specific DTI thresholds they are comfortable with, and exceeding these can make it difficult to qualify for a loan.

Assets and Reserves: Your Financial Cushion

Beyond your income, lenders want to see that you have sufficient assets to cover your down payment, closing costs, and, importantly, reserves for unexpected expenses.

- Down Payment: This is the portion of the home’s purchase price that you pay upfront. Lenders typically have minimum down payment requirements, though these can vary based on loan programs. The source of your down payment is also scrutinized; gifted funds need proper documentation.

- Closing Costs: These are the various fees associated with finalizing a mortgage, including appraisal fees, title insurance, lender fees, and more.

- Reserves: Lenders want to ensure you have funds set aside to cover your mortgage payments for a period of time (typically 2-6 months) in case of job loss, illness, or other unforeseen circumstances. These reserves can be held in savings accounts, checking accounts, investment accounts, or retirement funds (with certain limitations).

Credit Score and History: The Foundation of Trust

While we’ve touched on technology, your credit score and history remain a cornerstone of mortgage lending.

- Credit Score: This three-digit number, generated by credit bureaus, is a summary of your creditworthiness. A higher score generally indicates lower risk and can lead to better interest rates.

- Credit History: Lenders review your entire credit report, looking at payment history, credit utilization, length of credit history, credit mix, and new credit. Late payments, defaults, bankruptcies, or significant collections can negatively impact your application. They want to see a consistent track record of responsible credit management.

- Credit Inquiries: While not a dealbreaker, a large number of recent credit inquiries can sometimes signal to lenders that you are actively seeking a lot of credit, which might be perceived as a higher risk.

In conclusion, what mortgage lenders look at is a multi-faceted evaluation that blends traditional financial metrics with the influence of modern technology and the subtle power of brand perception. By understanding these elements – from the AI algorithms that assess your risk to the way you present your financial story, and of course, your verifiable income and assets – you can approach the mortgage application process with greater confidence and a clearer understanding of what it takes to secure your dream home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.