The Affordable Care Act (ACA) transformed the landscape of American healthcare by introducing the Premium Tax Credit (PTC)—a refundable tax credit designed to help eligible individuals and families cover the cost of premiums for health insurance purchased through the Health Insurance Marketplace. For many, this credit is the difference between having comprehensive medical coverage and being uninsured. However, the eligibility requirements are stringent, and many taxpayers find themselves unexpectedly disqualified due to specific financial or administrative criteria.

Navigating the intersection of health policy and tax law requires a clear understanding of the disqualifiers that can prevent you from receiving this subsidy. Whether you are an entrepreneur, a gig worker, or an employee at a small business, understanding these nuances is essential for effective financial planning.

The Fundamentals of the Premium Tax Credit (PTC)

Before diving into what disqualifies an individual, it is vital to understand what the Premium Tax Credit is and how it functions within the broader financial ecosystem. The PTC is unique because it can be taken in two ways: as Advance Premium Tax Credits (APTC) paid directly to your insurer to lower your monthly bills, or as a lump sum credit when you file your annual federal income tax return.

How the PTC Works

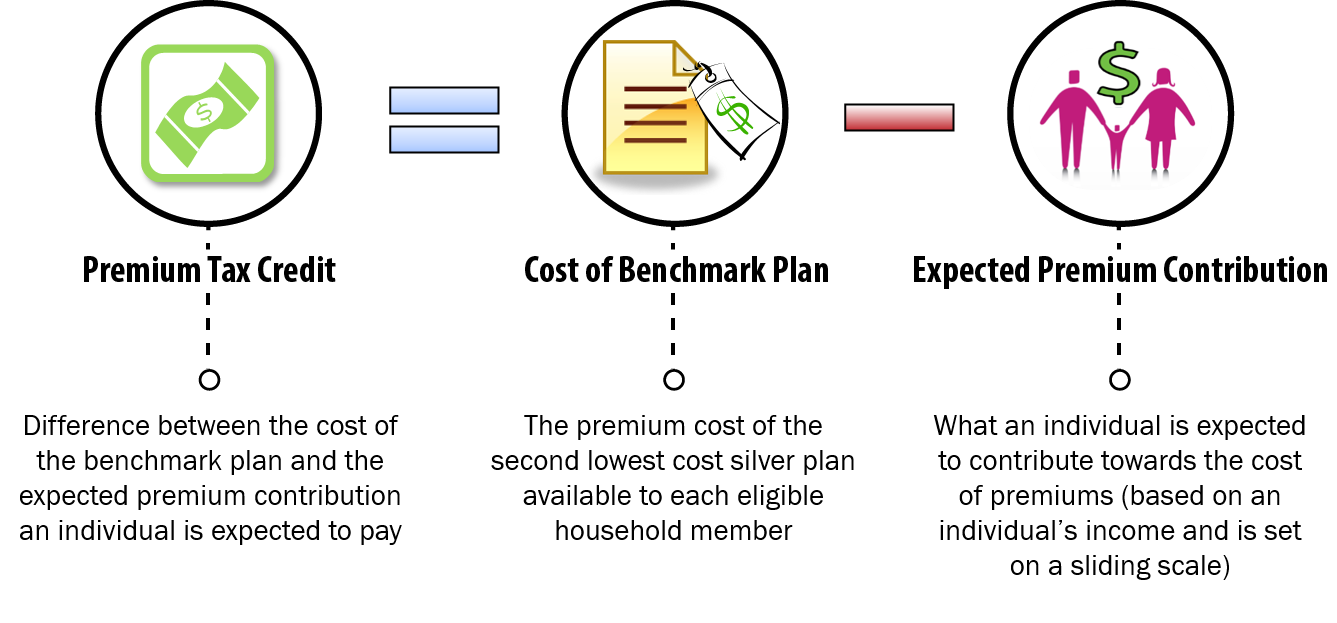

The credit is “refundable,” meaning that if the credit amount exceeds your tax liability, you can receive the excess as a refund. The amount of the credit is based on a sliding scale. Those with lower incomes receive a larger credit to cover a greater portion of their premiums, while those with higher incomes receive less. The calculation is based on the “Second Lowest Cost Silver Plan” (SLCSP) available in your area. This plan serves as the benchmark to determine how much assistance you need to make coverage “affordable” based on your household income.

The Role of the Health Insurance Marketplace

To be eligible for the PTC at all, you must purchase your health insurance through the official Health Insurance Marketplace (also known as the Exchange). If you purchase a plan directly from an insurance company (off-exchange), you are immediately disqualified from receiving the Premium Tax Credit, regardless of your income level. This is a common pitfall for individuals who seek out private brokers without ensuring the plan is Marketplace-certified.

Income Thresholds and the “Subsidy Cliff”

Income is the primary factor in determining PTC eligibility. Traditionally, the credit was reserved for those whose household income fell between 100% and 400% of the Federal Poverty Level (FPL). However, legislative changes have shifted these boundaries, creating new complexities for high and low earners alike.

Falling Below the Federal Poverty Level

In a seemingly counterintuitive rule, falling below 100% of the Federal Poverty Level can actually disqualify you from the Premium Tax Credit in states that have expanded Medicaid. If your income is low enough to qualify for Medicaid, the government expects you to utilize that program rather than the Marketplace. If you live in a state that has not expanded Medicaid and your income is below 100% FPL, you may find yourself in the “coverage gap”—too “rich” for Medicaid but too “poor” for the PTC. There are exceptions for certain immigrants who are not eligible for Medicaid, but for the general population, being eligible for Medicaid is a primary disqualifier for the PTC.

Exceeding the Upper Income Limits

Historically, once a household’s income exceeded 400% of the FPL, they hit the “subsidy cliff,” where all eligibility for the PTC vanished instantly. This meant a single dollar of additional income could cost a family thousands of dollars in lost tax credits. Under the American Rescue Plan and the subsequent Inflation Reduction Act, this “cliff” has been temporarily eliminated through 2025. Currently, eligibility is based on whether the cost of the benchmark plan exceeds 8.5% of your household income. However, if your income is high enough that the cost of insurance is deemed “affordable” (less than 8.5% of your income), you are disqualified from receiving the credit.

Access to Alternative Minimum Essential Coverage (MEC)

The Premium Tax Credit is intended to be a safety net for those who have no other options for affordable health coverage. Therefore, if you have access to other forms of “Minimum Essential Coverage” (MEC), you are generally disqualified from receiving the PTC.

Employer-Sponsored Coverage and the “Affordability” Test

The most common disqualifier for the PTC is the “offer” of insurance from an employer. If your employer offers a plan that is considered “affordable” and provides “minimum value,” you cannot claim the PTC, even if you choose not to enroll in the employer’s plan.

For 2024, an employer plan is considered affordable if the employee’s share of the premium for self-only coverage does not exceed roughly 8.39% of their household income. A major point of contention for years was the “Family Glitch,” where the affordability was based only on the individual’s cost, not the cost to cover the whole family. Recent IRS regulations have largely fixed this, allowing family members to qualify for the PTC if the cost of family coverage through an employer exceeds the affordability threshold, even if the individual coverage is affordable. However, if the employer’s offer meets the government’s definition of affordability, the entire household is disqualified from Marketplace subsidies.

Government-Sponsored Programs (Medicaid, Medicare, and VA)

If you are eligible for—or enrolled in—government-sponsored coverage, you are disqualified from the PTC. This includes:

- Medicare Part A: Once you are eligible for premium-free Medicare, you lose PTC eligibility.

- Medicaid and CHIP: If you are eligible for these programs, you cannot receive the credit.

- Veterans Coverage (VA): Most forms of VA healthcare count as MEC.

- TRICARE: Active duty and retired military coverage disqualifies you from the PTC.

It is important to note that simply being eligible for these programs is often enough to disqualify you, regardless of whether you actually sign up for them.

Filing Status and Household Requirements

The IRS has specific rules regarding how you file your taxes and who you claim as a dependent, both of which can serve as immediate disqualifiers for the Premium Tax Credit.

The “Married Filing Separately” Rule

One of the most rigid disqualifiers for the PTC is the requirement for married couples to file a joint return. If you are married but choose the “Married Filing Separately” status, you are generally ineligible for the Premium Tax Credit. This often catches separated couples off guard during tax season.

There are limited exceptions to this rule, specifically for victims of domestic abuse or spousal abandonment. In these cases, a taxpayer may be able to claim the PTC while filing separately if they meet specific criteria. Outside of these narrow exceptions, the “joint filing” requirement remains a significant barrier for many taxpayers.

Dependency Status and Tax Filings

To claim the PTC, you cannot be claimed as a dependent by another taxpayer. If a parent claims a college student as a dependent on their tax return, that student is disqualified from claiming the PTC on their own, even if they have their own Marketplace plan. Furthermore, the credit is calculated based on “household income,” which includes the income of the taxpayer, their spouse, and any dependents who are required to file a tax return. If your household composition changes—for example, if a child begins working and earns enough to be required to file—this can increase your household income and potentially disqualify you or reduce your credit amount.

Navigating Changes and Compliance

The Premium Tax Credit is a “forward-looking” benefit based on estimates, which introduces the risk of disqualification or “repayment” at the end of the year. Maintaining eligibility requires active management of your financial profile throughout the year.

Life Transitions and Reporting Changes

The Marketplace calculates your APTC based on your projected income for the coming year. If your income increases during the year—perhaps through a bonus, a new job, or a successful side hustle—you may no longer be eligible for the credit you are currently receiving. Failure to report these changes to the Marketplace in real-time can lead to a “disqualification after the fact.” When you file your taxes, the IRS will reconcile the credit you received with your actual year-end income. If you earned more than predicted, you may have to pay back some or all of the credit.

The Importance of Accurate Tax Reconciliation (Form 8962)

A procedural disqualifier exists for those who fail to “reconcile” their credits. If you received Advance Premium Tax Credits in a prior year but failed to file Form 8962 with your tax return to reconcile those payments, the Marketplace will disqualify you from receiving any future APTC. This “Failure to File and Reconcile” status is a common administrative reason why individuals lose their subsidies during the open enrollment period.

In conclusion, while the Premium Tax Credit is a vital financial tool for making healthcare accessible, it is not a universal guarantee. Disqualification can stem from income fluctuations, filing status, or the mere existence of an “affordable” offer from an employer. For those in the “Money” niche, understanding these variables is essential. Proper tax planning and a proactive approach to reporting life changes are the only ways to ensure that this valuable credit remains a benefit rather than a surprise liability at tax time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.