In the intricate ecosystem of business finance, the term “return payment” frequently appears as a source of confusion for small business owners and consumers alike. While the concept may seem straightforward—essentially reversing a transaction—the reality involves a complex sequence of banking protocols, accounting adjustments, and risk management strategies. Understanding how these payments function is critical for maintaining healthy cash flow and avoiding unnecessary bank fees.

Defining the Return Payment Mechanism

At its most fundamental level, a return payment occurs when a transaction that was initiated—whether by check, electronic funds transfer (EFT), or Automated Clearing House (ACH) debit—is rejected by the receiving financial institution. Instead of the funds successfully moving from the payor to the payee, the transaction is “returned” to the originator.

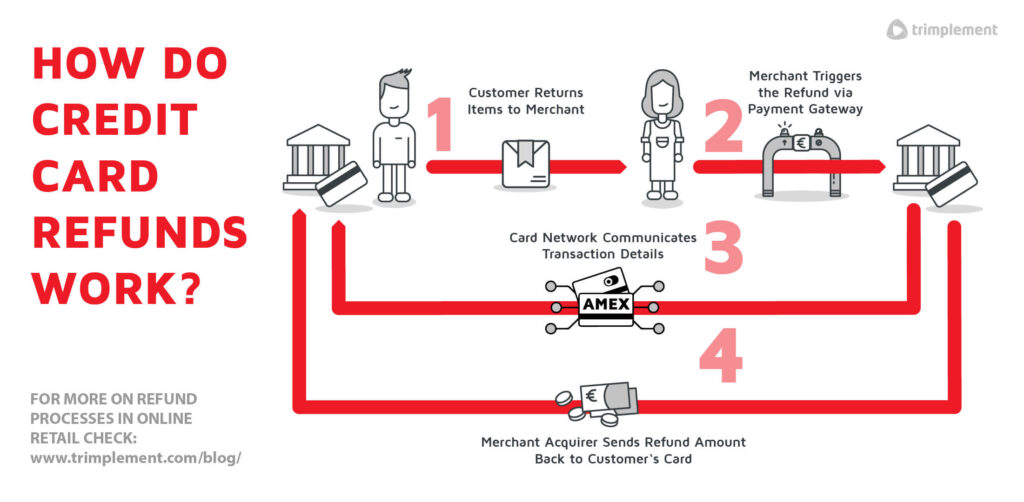

![]()

Why Transactions Fail

The reasons for a return payment are varied and are usually indicated by a specific “return code” issued by the clearinghouse. Common triggers include:

- Insufficient Funds (NSF): The most frequent cause, occurring when the account holder lacks the available balance to cover the transaction.

- Closed Accounts: The payor’s account has been deactivated or shut down before the transaction could clear.

- Authorization Issues: The account holder may have placed a “stop payment” order, or the transaction did not meet the predefined authorization parameters for that specific account.

- Incorrect Information: Clerical errors, such as a wrong routing number or account number, prevent the financial institution from identifying the destination or source.

The Lifecycle of a Return

When a payment is returned, the financial institution initiates a reversal. This is not instantaneous. The banking system operates in cycles, meaning a return might occur several days after the initial transaction attempt. During this window, the merchant or recipient may believe the payment is pending, only to be notified later that the transaction has bounced. This delay creates a “float” period that complicates financial planning for businesses relying on those funds.

The Financial Implications for Businesses

For businesses, return payments are more than just a nuisance; they are a direct hit to the bottom line. Every return triggers administrative overhead, banking fees, and potentially lost inventory or service value.

Cost of Processing and Recovery

Financial institutions almost universally charge a fee when a transaction is returned. These fees are often double-sided: the bank initiates a penalty for the failed transaction, and the receiving business may incur additional costs from their payment processor or merchant service provider. If a business operates on high-volume, low-margin transactions, a small cluster of return payments can quickly erode the profitability of a successful sales period.

Accounting and Reconciliation Challenges

From an accounting perspective, a return payment requires careful documentation to maintain accurate financial records. When a payment is returned, the business must reverse the initial entry in its ledger. If the business has already shipped goods based on the assumption that a payment was “pending,” the return payment creates an accounts receivable issue. Managing this requires a robust reconciliation process where the finance team tracks these reversals against bank statements, ensuring that the ledger reflects actual liquidity rather than anticipated income.

Impact on Credit and Trust

Frequent return payments can have long-term consequences for a business’s reputation within the banking sector. Financial institutions monitor the “return rate” of a merchant account. If a company exhibits a high return rate, banks may flag the account as high-risk. This can lead to increased processing fees, a hold on funds, or in extreme cases, the termination of the merchant account. Maintaining a low return rate is therefore a essential component of corporate financial health.

Mitigating Risk and Preventing Return Payments

Proactive management is the most effective strategy for dealing with return payments. By implementing rigorous verification protocols and utilizing modern financial tools, businesses can significantly reduce the likelihood of encountering failed transactions.

Verification and Pre-Note Systems

One of the most effective ways to prevent errors is the use of “pre-note” systems for recurring payments. A pre-note is a zero-dollar transaction sent through the ACH network to verify that the routing and account information is valid and active. While this adds a small delay to the initial setup of a recurring billing cycle, it effectively eliminates the risk of returns caused by clerical errors.

Real-Time Balance Verification

For high-value transactions, businesses can integrate API-driven solutions that check the availability of funds in real-time. By connecting directly with the payor’s financial institution, a business can confirm that the balance is sufficient before finalizing the transaction. This minimizes the risk of NSF returns, which are the most common and difficult to manage.

Clear Communication with Clients

Often, returns are not the result of malice, but of simple oversight. Implementing a communication strategy can drastically reduce return rates. For example, sending automated payment reminders 48 hours before an ACH debit is processed allows the payor to ensure their account is funded. Similarly, providing a transparent portal where customers can update their banking details prevents the “incorrect account info” errors that plague subscription-based business models.

The Role of Automated Clearing House (ACH) Regulations

In the United States, the National Automated Clearing House Association (Nacha) governs the rules surrounding electronic payments, including return payments. Understanding these regulations is vital for any business that relies on automated payments.

Understanding NACHA Return Codes

Nacha mandates that every return payment must be accompanied by a specific return code. These codes—ranging from R01 (Insufficient Funds) to R31 (Permissible Return Entry)—serve as the standard language between banks. By analyzing these codes, financial teams can categorize their returns:

- Human Error: Issues related to typos or outdated information.

- Liquidity Issues: Issues related to the customer’s actual bank balance.

- Security Issues: Potential fraud signals that require an immediate investigation.

By tracking these codes over time, businesses can identify patterns. For instance, if a specific region or payment method consistently shows a high rate of R01 codes, the business might need to adjust their billing date to align better with when customers typically receive their salaries.

Compliance and Due Diligence

Compliance is not merely about avoiding fees; it is about protecting the financial infrastructure. Businesses must adhere to strict data security standards, such as PCI-DSS for credit cards and Nacha’s operating rules for ACH. Failure to comply can result in heavy fines and a total loss of the ability to process electronic payments. A strong internal policy for handling returned payments—one that treats every reversal as a data point for improvement—is the hallmark of a financially mature organization.

Conclusion: Turning Returns into Insights

A return payment is an inevitable part of doing business in a digital economy, but it does not have to be a recurring drain on resources. By treating return payments as a measurable business metric rather than just an administrative hurdle, companies can optimize their revenue cycles. Through improved verification methods, better communication with customers, and a deep understanding of banking regulations, businesses can minimize the friction of returned funds. Ultimately, the goal is to shift from reactive handling of failed payments to a proactive, streamlined financial strategy that ensures cash flow stability and protects the integrity of the business’s financial operations. Consistent vigilance in this area ensures that the digital flow of money remains efficient, secure, and beneficial to all parties involved.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.