The allure of the Powerball is undeniable. It represents a dream that transcends borders, a singular ticket that promises to liberate its owner from the constraints of debt, labor, and financial insecurity. Yet, for all its cultural significance, the lottery is fundamentally a mathematical exercise—a cold, hard equation that rarely tips in favor of the individual. To understand the Powerball is to understand the gravity of extreme probability.

The Mathematics of Impossible Odds

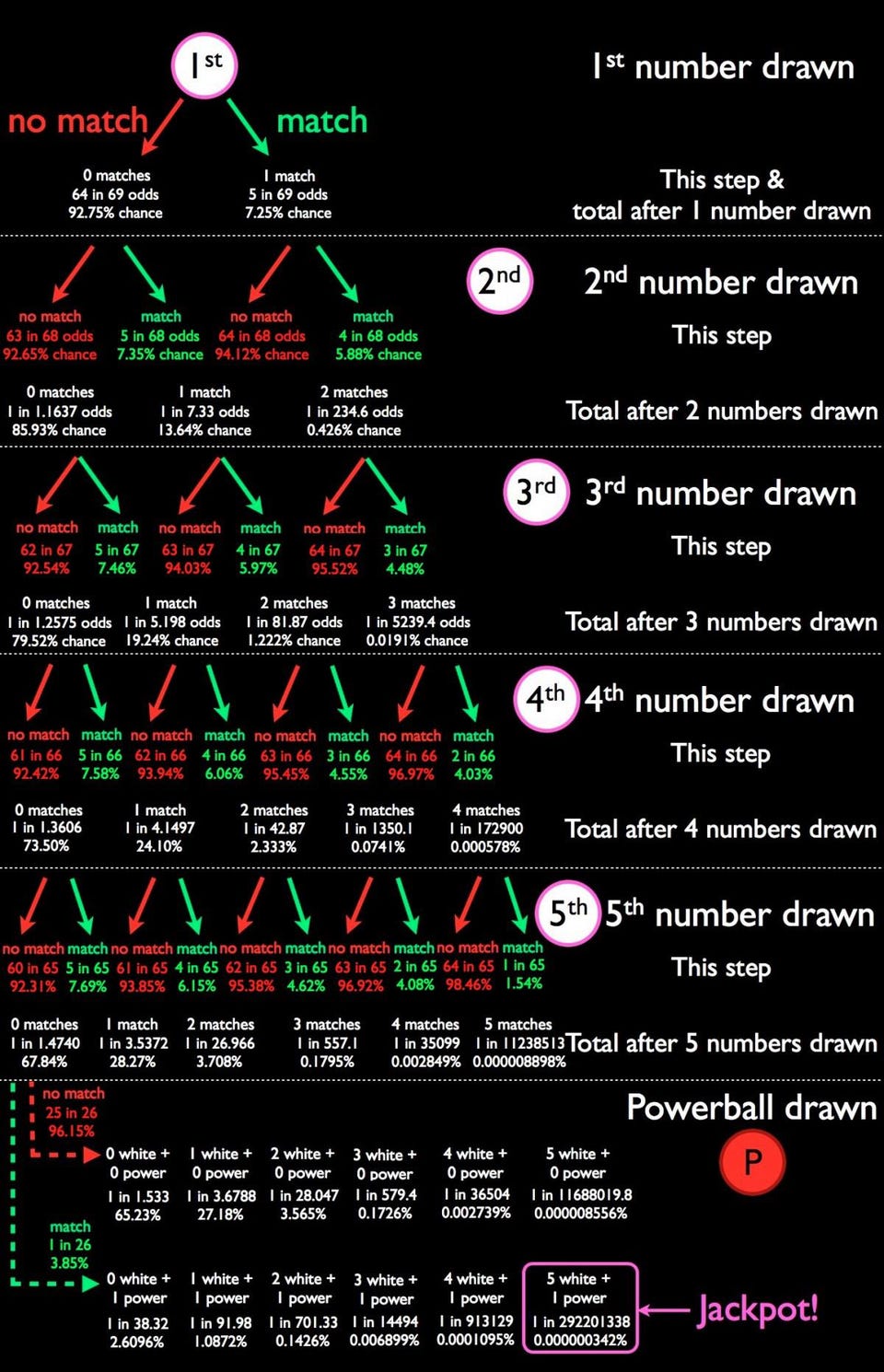

When you purchase a Powerball ticket, you are participating in a game designed with a singular, mathematical objective: to make winning as statistically improbable as possible while maintaining the illusion of accessibility. The current structure of the game requires players to select five numbers from a set of 69 white balls and one number from a set of 26 red Powerballs.

Calculating the Permutations

To find the probability of winning the jackpot, we must calculate the number of possible combinations. The math involves combinations ($nCr$), where $n$ is the total number of options and $r$ is the number of items being chosen.

First, the odds of correctly picking the five white balls are calculated as 69 choose 5, which results in 11,238,513 possible combinations. When you factor in the single red Powerball (1 in 26), the calculation becomes 11,238,513 multiplied by 26. This brings the total number of possible combinations to 292,201,338.

The Reality of 1 in 292.2 Million

Your odds of holding the winning ticket for the jackpot are approximately 1 in 292,201,338. To put this in perspective, you are significantly more likely to be struck by lightning, be born with extra fingers or toes, or become a professional athlete than you are to win the Powerball jackpot. This probability remains constant regardless of whether you choose your own numbers or use a “quick pick” generator, and it does not improve even if you purchase more tickets. Buying ten tickets simply moves your odds from 1 in 292,201,338 to 10 in 292,201,338—an improvement that is statistically negligible in the grand scheme of the game.

The Psychology of the Lottery and Financial Literacy

Why do millions of people continue to spend their hard-earned money on a game with such dismal odds? The answer lies in the intersection of behavioral economics and financial psychology. The lottery is not sold as a financial instrument; it is sold as a psychological comfort—a “hope tax” that allows individuals to visualize a different life for the cost of a few dollars.

The Availability Heuristic

Humans are notoriously bad at processing large numbers. We often rely on the “availability heuristic,” a mental shortcut where we weigh the probability of an event based on how easily we can recall similar instances. Because the media heavily covers jackpot winners—shining a spotlight on the one person who beat the odds while ignoring the 292 million who did not—our brains perceive the event as far more common than it actually is.

The Cost of Opportunity

From a personal finance perspective, the Powerball represents an extreme inefficiency. If an individual spends $10 per week on lottery tickets, they are committing $520 annually to a venture with a negative expected value. If that same $520 were invested annually in a low-cost index fund with an average historical return of 7%, after 30 years, that investment would grow to approximately $50,000.

When you treat the lottery as a “side hustle” or a “get-rich-quick” strategy, you are inadvertently sacrificing the slow, boring, but mathematically certain path of compound interest. Financial independence is rarely found in a drawing; it is built through the disciplined application of capital into assets that grow over time.

Risk Management and the “Lump Sum” Trap

Winning the lottery is widely regarded as one of the most volatile financial events an individual can experience. While the windfall seems like a permanent solution to all money problems, the reality is that the sudden acquisition of extreme wealth requires a level of financial literacy that most people have not had the opportunity to develop.

The Tax and Payout Structure

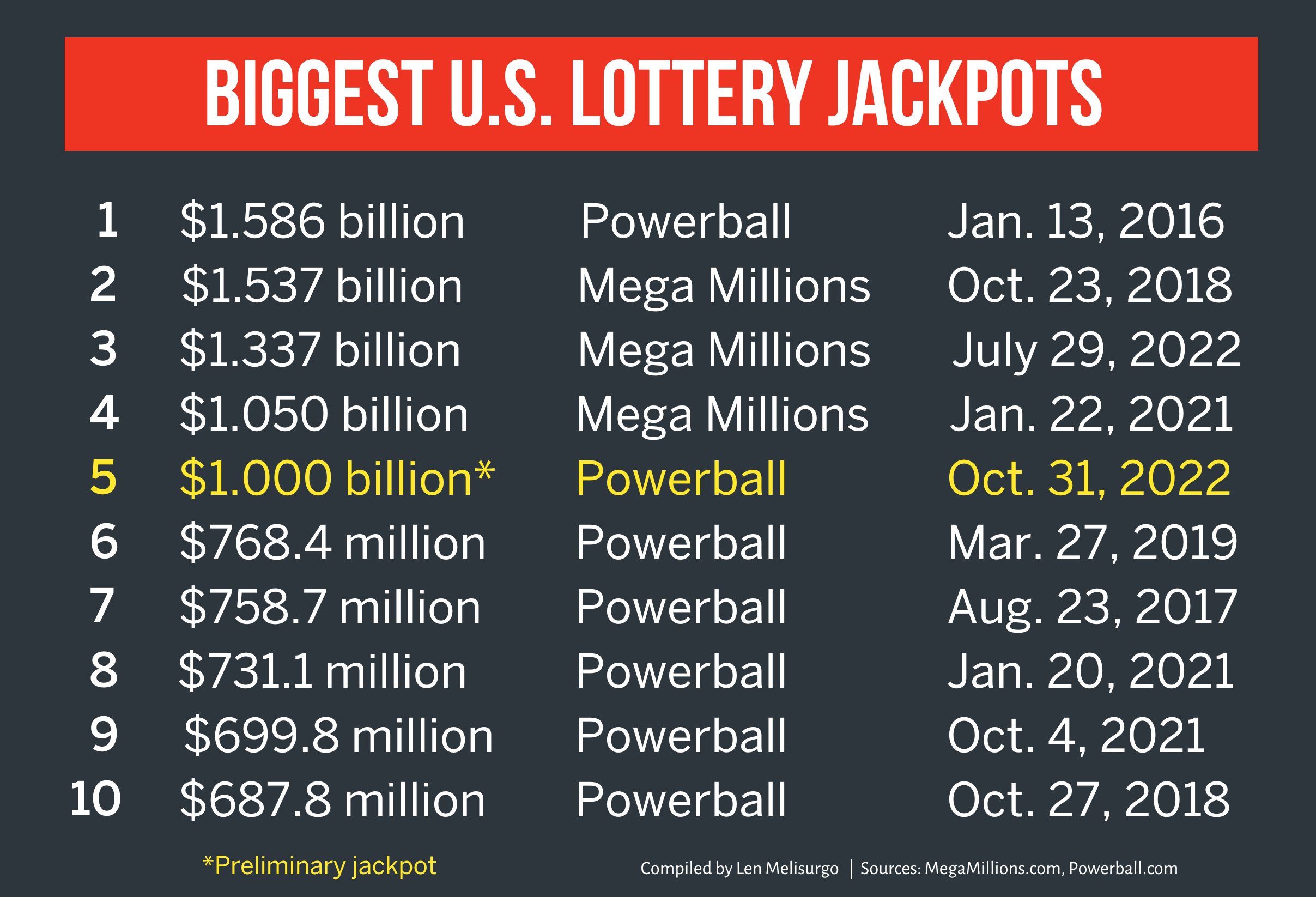

When you see a advertised jackpot of $500 million, that number is misleading. The Powerball offers two options: the annuity (paid over 30 years) or the cash lump sum. The cash lump sum is significantly lower because it represents the actual money currently available in the prize pool. Once you select the lump sum, you must then factor in federal taxes—which can take up to 37%—and state taxes, which vary by jurisdiction. By the time the government takes its share, you may be looking at less than 50% of the advertised “jackpot” figure.

Wealth Preservation vs. Wealth Creation

The transition from having limited assets to managing a nine-figure portfolio is a massive liability. Many lottery winners experience “sudden wealth syndrome,” characterized by social isolation, intense pressure from family and friends for loans or gifts, and poor investment choices made under the influence of newfound status.

Sustainable wealth is about management, not just acquisition. The infrastructure required to maintain a massive fortune—tax attorneys, fiduciary financial planners, and estate planners—is often absent for the average lottery winner. This is why a staggering percentage of lottery winners end up in worse financial condition just a few years after their win than they were before.

Rethinking the Value of a Ticket

If we strip away the fantasy, the Powerball is essentially a regressive tax on those who can least afford it. Statistically, lower-income households spend a higher percentage of their income on lottery tickets compared to wealthier individuals. This indicates that the game thrives on the desperation or the lack of viable investment avenues for those in lower socioeconomic brackets.

The Alternative: Investing in Yourself

If you are looking for a way to change your financial trajectory, the best “ticket” you can buy is one that offers a positive expected return. This might involve:

- Education and Skills Training: Investing in certifications or degrees that increase your earning potential in the marketplace.

- Starting a Micro-Business: Using that $10 a week to fund the initial costs of a side hustle, such as a subscription to a design tool, domain hosting, or raw materials for a craft.

- Automated Savings: Redirecting the “lottery budget” into a high-yield savings account or a brokerage account. Even small, consistent contributions to a Roth IRA or 401(k) exploit the power of compounding, which is the only “get-rich-quick” scheme that has been proven to work over a long enough timeline.

Final Thoughts on Probability

The odds of winning the Powerball are designed to be astronomical because the business model of the lottery relies on the accumulation of millions of small losses to fund one massive, media-friendly win. Understanding these odds is an essential exercise in financial maturity. When you realize that the game is not designed for you to win, you are empowered to stop participating in it and start focusing your financial energy on systems where the probability of success is entirely within your control. The jackpot of life is not found in a series of numbered balls, but in the deliberate management of your own economic potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.