Navigating the landscape of modern digital banking requires understanding the nuances of how financial transactions materialize, particularly when moving away from traditional brick-and-mortar institutions. Chime, a leader in the fintech space, has revolutionized how millions manage their money. However, a common point of confusion for new users—or those receiving a payment from a Chime account—is the appearance and functionality of a “Chime check.”

Because Chime is a mobile-first banking platform, its approach to check writing differs from the standard paper checkbook you might receive at a local bank. Understanding these mechanics is essential for ensuring your payments are processed smoothly and that you can identify legitimate documentation when receiving funds.

Understanding Chime’s Digital-First Payment Architecture

Chime operates as a financial technology company rather than a traditional bank, utilizing partner banks to hold user deposits. Because it is optimized for digital efficiency, the platform does not issue physical, pre-printed checkbooks to every account holder by default. Instead, Chime utilizes a feature specifically designed for outgoing payments known as the “Checkbook” feature, which allows users to send digital checks that are then printed and mailed on their behalf.

How the Chime Check Feature Operates

When you initiate a payment through the Chime app using the check feature, you are essentially leveraging Chime’s back-end infrastructure to generate a negotiable instrument. You provide the recipient’s name, the amount, and the mailing address. Chime then drafts a physical check from their systems and mails it to the recipient via the United States Postal Service.

This means that a “Chime check” is rarely a document that you, the account holder, physically handle or print yourself. It is a service where the bank acts as the intermediary. From the recipient’s perspective, they receive a standard paper check in the mail, which looks almost identical to any personal check they might receive from a traditional bank account holder.

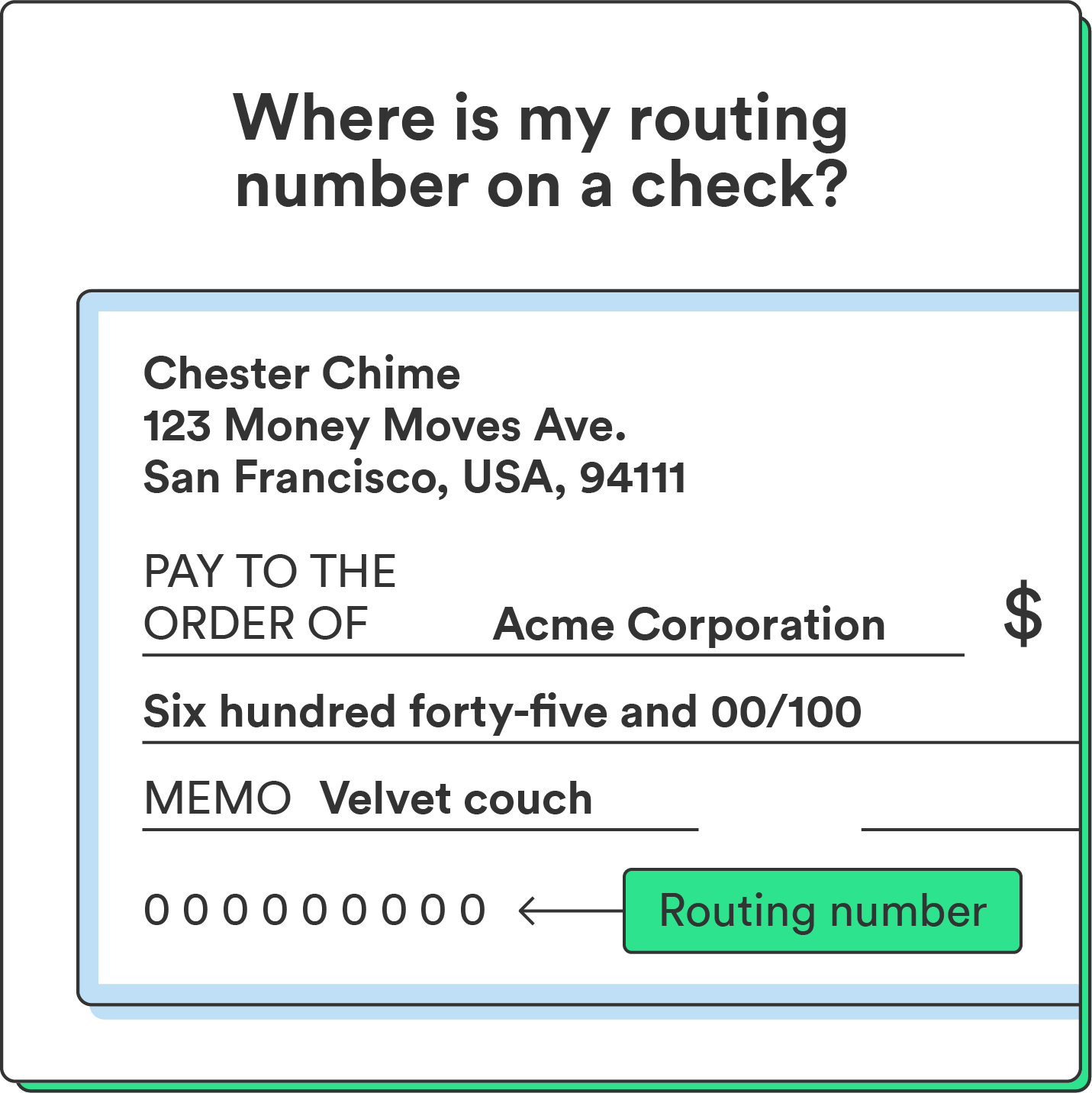

Identifying the Components of a Chime Check

If you receive a check generated by Chime, it will typically contain the standard elements required for banking processing:

- The Drawer’s Information: The name and address of the Chime account holder who initiated the payment.

- The Paying Bank: Since Chime partners with institutions like The Bancorp Bank or Stride Bank, N.A., the check will list the name and routing information of the specific partner bank holding the funds.

- MICR Encoding: Along the bottom of the check, you will find the standard Magnetic Ink Character Recognition (MICR) line, containing the bank’s routing number and the specific account number associated with the check transaction.

- Signature Line: Instead of a wet ink signature from the individual, these generated checks often feature a digital reproduction of the account holder’s name or a statement indicating that the signature is on file.

The Physical Appearance of a Chime Check

If you are a recipient, you might be surprised to see a check that looks professional, clean, and sometimes slightly different in cardstock weight than a premium bank check. Because these checks are printed on demand by a third-party service provider integrated with Chime, they adhere to standard banking regulations to ensure they are negotiable at any financial institution.

Design and Formatting

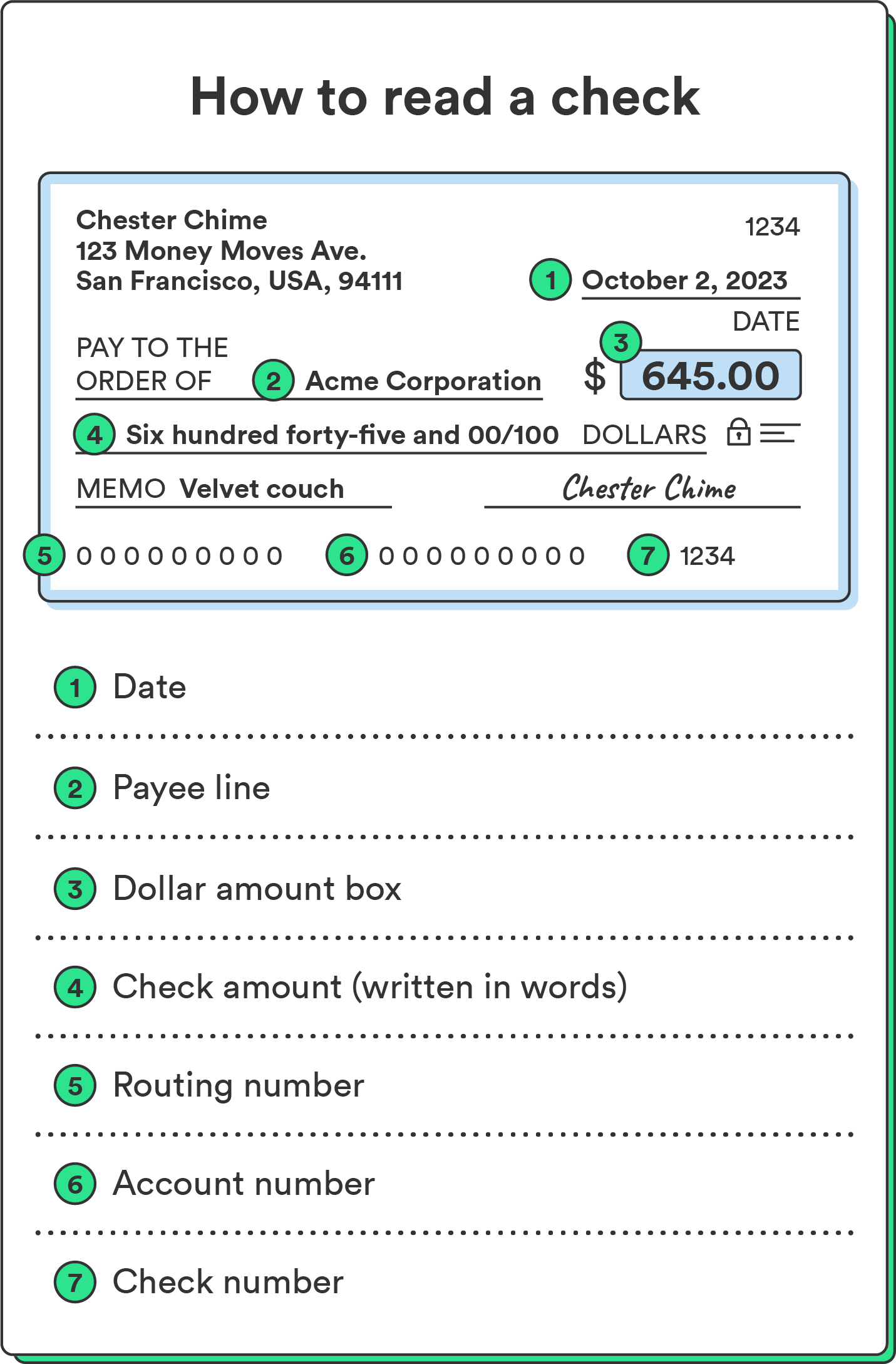

The layout of a Chime-generated check is utilitarian by design. You will typically see:

- Standard Banking Layout: The date field, payee line, numeric and written amount lines are all placed in the conventional positions dictated by the Federal Reserve and banking standards.

- Professional Printing: Because these are laser-printed rather than written by hand, they are highly legible. This often reduces the likelihood of processing errors at the bank, as there is no ambiguity regarding the dollar amount or the recipient’s name.

- Security Features: To prevent fraud, these checks include standard security measures such as watermarks or specialized background patterns designed to deter photocopying and tampering.

Is it a “Certified” or “Cashier’s” Check?

A common misconception is that a check sent via Chime is equivalent to a cashier’s check. This is not strictly true. A Chime-generated check is a personal check. While it is backed by the funds in your Chime account, it is not a bank-guaranteed instrument in the same way a cashier’s check is. Recipients should treat it with the same caution they would any personal check, ensuring the funds are cleared by their own bank before considering the transaction finalized.

Managing Checks Within the Chime App

For Chime users, the process of sending a check is entirely integrated into the mobile app interface. This digital-to-physical bridge is what makes the experience seamless, but it also creates a unique workflow that differs from traditional checkbook management.

Initiating a Payment

To send a check, you navigate to the “Move Money” or “Transfers” section of the Chime app. By selecting the “Check” option, you are prompted to input the recipient’s details. Once submitted, Chime takes over. The funds are deducted from your Chime Spending Account, and the physical check is put into production.

Tracking and History

Because this is a digital service, you have a distinct advantage over traditional checkbooks: an automatic digital trail. You do not need to maintain a physical check register. Your Chime app keeps a history of every check sent, including the status of the mailing. You can see when the check was requested, when it was mailed, and the status of the transaction. This transparency is a significant upgrade over the “pen-and-paper” method of tracking personal checks.

Considerations for Delivery Times

Unlike an Instant Transfer or an ACH payment, a Chime check is subject to the speed of the postal service. Recipients should be informed that the check is on the way, as it may take several business days to arrive at the destination. Users should always factor in this lead time when planning payments for rent, services, or other time-sensitive obligations.

Security Best Practices for Digital Checks

Whether you are the one sending a Chime check or the one receiving it, security remains the top priority. Financial transactions involving paper checks are still susceptible to fraud, though the digitizing of the issuance process mitigates many traditional risks.

For the Sender: Verification is Key

Before hitting “Submit,” double-check the recipient’s address. Since the check is being mailed directly, an incorrect address could result in the check being intercepted or lost. Furthermore, ensure that the recipient is someone you trust, as you would with any check-based payment. Once the check is mailed, it is difficult to “cancel” or “stop payment” on it without incurring potential fees or dealing with complex bank processes.

For the Recipient: Authenticity and Deposit

If you receive a check that claims to be from a Chime account, you can verify it like any other check. If you have concerns, look at the bank name printed on the check—this is the partner bank that actually processes the payment. If you are ever unsure about the legitimacy of a check, the best practice is to contact your own bank’s teller or mobile support team. They can provide guidance on how to deposit it and how to verify if the check has cleared.

Protecting Your Chime Credentials

The security of your Chime checks starts with the security of your app. Always use two-factor authentication (2FA) and never share your login credentials. If you lose access to your account or suspect unauthorized activity, disable your account immediately through the Chime app to prevent any outgoing fraudulent check requests.

Conclusion

A Chime check is a bridge between the convenience of a modern mobile banking app and the necessary tradition of paper-based financial systems. For the user, it is a streamlined, digital process that removes the headache of physical checkbooks. For the recipient, it is a recognizable, negotiable instrument that functions just like a check from a traditional bank.

By understanding that a Chime check is an automatically generated document—printed and mailed by the bank on behalf of the user—you can navigate these transactions with confidence. Whether you are using the app to manage your monthly expenses or receiving a payment from a friend or client who uses Chime, the process is designed for clarity, security, and efficiency in the digital age. Keeping these details in mind ensures that you can utilize this feature to its full potential while maintaining the integrity of your personal financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.