Understanding how to calculate loan payments is a fundamental skill for anyone engaging with personal or business finance. Whether you’re considering a mortgage, an auto loan, a personal loan, or a business loan, knowing the mechanics behind your monthly obligation empowers you to make informed decisions, budget effectively, and potentially save thousands over the life of the loan. This guide will demystify the process, from manual formulas to leveraging modern financial tools, ensuring you have a clear picture of your financial commitments.

Understanding the Fundamentals of Loan Payments

Before diving into calculations, it’s crucial to grasp the core elements that constitute a loan and, by extension, its payments. A loan is essentially a sum of money lent by one party to another, with the expectation that the principal amount will be repaid, usually with interest, over a specified period.

Key Components of a Loan

Every loan payment is primarily composed of two critical parts:

- Principal: This is the initial amount of money borrowed. As you make payments, a portion of each payment goes towards reducing this principal balance.

- Interest: This is the cost of borrowing the principal amount, expressed as a percentage of the outstanding balance. Interest is the lender’s profit for providing the capital.

Beyond these, other factors like loan term, compounding frequency, and fees can also influence the total cost and structure of your payments.

The Importance of Loan Payment Calculation

Accurately calculating loan payments is more than just a mathematical exercise; it’s a cornerstone of sound financial planning. It allows you to:

- Budget Effectively: Know precisely how much you need to set aside each month for debt obligations.

- Compare Loan Offers: Evaluate different lenders’ terms, interest rates, and fees to choose the most cost-effective option.

- Assess Affordability: Determine if a particular loan amount and its corresponding payments fit within your financial capacity without straining your budget.

- Plan for Early Repayment: Understand how additional payments can impact your loan term and total interest paid.

Factors Influencing Your Monthly Payment

Several variables work in tandem to determine the size of your regular loan payment:

- Principal Amount: The larger the amount borrowed, the higher your payments will generally be, assuming all other factors remain constant.

- Interest Rate: A higher interest rate means a larger portion of your payment goes towards interest, increasing the overall payment amount.

- Loan Term (Duration): This is the length of time over which you agree to repay the loan. A longer term typically results in lower monthly payments but often means paying more interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but less total interest.

- Compounding Frequency: Most loans compound interest monthly, meaning interest is calculated on the outstanding principal balance each month. This impacts how quickly the interest accrues.

Manual Calculation Methods: The Amortization Formula

While digital tools have simplified the process, understanding the underlying mathematical formula for loan amortization provides invaluable insight into how your payments are structured. This formula calculates the fixed monthly payment required to fully repay a loan over a set period.

Deconstructing the Loan Payment Formula

The standard formula for calculating a fixed monthly loan payment (M) is:

$M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]$

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (annual rate divided by 12)

- n = Total Number of Payments (loan term in years multiplied by 12)

Let’s break down each component:

- Principal (P): The initial loan amount.

- Monthly Interest Rate (i): If your annual interest rate is 6%, then

iwould be 0.06 / 12 = 0.005. It’s crucial to convert the annual rate to a monthly decimal. - (1 + i)^n: This represents the compounding effect of interest over the entire loan term.

nis the total number of payments. For a 5-year loan,nwould be 5 * 12 = 60.

Step-by-Step Manual Calculation Example

Let’s consider an example:

- Principal (P): $100,000

- Annual Interest Rate: 6%

- Loan Term: 30 years (360 months)

Step 1: Calculate Monthly Interest Rate (i)

i = 6% / 12 = 0.06 / 12 = 0.005

Step 2: Calculate Total Number of Payments (n)

n = 30 years * 12 months/year = 360

Step 3: Plug values into the formula

M = 100,000 [ 0.005(1 + 0.005)^360 ] / [ (1 + 0.005)^360 – 1 ]

First, calculate (1 + 0.005)^360 = (1.005)^360 ≈ 6.022575

Now, substitute this back:

M = 100,000 [ 0.005 * 6.022575 ] / [ 6.022575 – 1 ]

M = 100,000 [ 0.030112875 ] / [ 5.022575 ]

M = 3011.2875 / 5.022575

M ≈ $599.55

So, the estimated monthly payment for this loan would be approximately $599.55.

Limitations of Manual Calculation for Complex Scenarios

While manual calculation is excellent for understanding the mechanics, it can be tedious and prone to error, especially for large numbers, long terms, or when dealing with variations like bi-weekly payments, interest-only periods, or variable interest rates. For these reasons, financial professionals and individuals alike often turn to digital solutions.

Leveraging Digital Tools for Accuracy and Ease

In today’s digital age, a multitude of tools are available to calculate loan payments quickly and accurately. These resources eliminate human error and often provide additional insights that manual calculations cannot easily reveal.

Online Loan Calculators: Your Quick Solution

Online loan calculators are the simplest and most accessible tools for immediate loan payment estimates. A quick search for “loan calculator” will yield numerous free options from financial institutions, real estate websites, and personal finance blogs.

How to use them:

Typically, you input the principal amount, interest rate, and loan term, and the calculator instantly displays your estimated monthly payment. Many also offer amortization schedules, showing how much principal and interest you pay each month over the life of the loan. They are ideal for quick comparisons and initial budgeting.

Spreadsheet Software (Excel/Google Sheets) for Detailed Analysis

For more detailed analysis, custom scenarios, or integrating loan calculations into a larger financial model, spreadsheet software like Microsoft Excel or Google Sheets is indispensable. These programs feature powerful built-in financial functions.

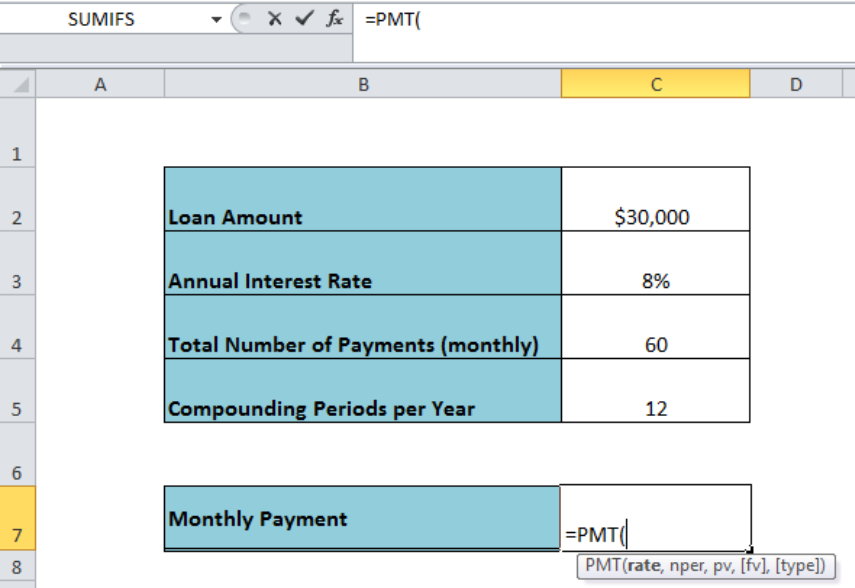

The PMT Function:

The PMT function is specifically designed to calculate the payment for a loan based on constant payments and a constant interest rate.

The syntax is: PMT(rate, nper, pv, [fv], [type])

- rate: The interest rate per period (monthly interest rate).

- nper: The total number of payments for the loan (total months).

- pv: The present value, or the total amount that a series of future payments is worth now; this is the principal amount.

- fv (optional): The future value, or a cash balance you want to attain after the last payment is made. If omitted, it’s assumed to be 0 (meaning the loan is fully paid off).

- type (optional): Indicates when payments are due (0 for end of period, 1 for beginning of period). If omitted, it’s assumed to be 0.

Example in Excel/Google Sheets:

For our previous example ($100,000 loan, 6% annual interest, 30 years):

- rate = 0.06/12 = 0.005

- nper = 30*12 = 360

- pv = -100000 (enter as a negative number because it’s an outflow)

The formula would be: =PMT(0.005, 360, -100000)

This would return $599.55, matching our manual calculation. Spreadsheets also allow you to easily create full amortization tables by varying inputs and tracking balances.

Financial Planning Apps and Software

Beyond generic spreadsheets, specialized financial planning apps and software (e.g., Quicken, Mint, dedicated loan management apps) often include robust loan calculators. These tools can integrate loan details directly into your overall financial picture, helping you track payments, monitor balances, and assess how loans fit into your broader budget and savings goals. They are particularly useful for managing multiple loans or complex financial portfolios.

Beyond the Monthly Payment: Strategic Considerations

Calculating your monthly payment is just the first step. To truly master your debt, you need to look beyond that single number and understand its implications over the life of the loan.

The Impact of Interest Rates and Loan Terms

Even small differences in interest rates or loan terms can have a dramatic effect on your total cost of borrowing.

- Interest Rate: A loan with a 7% annual interest rate will cost significantly more than a 5% loan over the same term, even if the monthly payments appear similar at first glance.

- Loan Term: A 15-year mortgage will have higher monthly payments than a 30-year mortgage for the same principal, but you will pay substantially less in total interest over its life. Conversely, extending a personal loan from three years to five years will lower your monthly payment but increase the overall interest burden. Always balance affordability with the total cost.

Understanding Amortization Schedules

An amortization schedule is a table detailing each payment made over the life of a loan, showing how much of each payment goes towards interest and how much towards principal, as well as the remaining balance.

- Early Payments: In the early years of an amortizing loan (especially mortgages), a larger portion of your monthly payment goes towards interest, and a smaller portion reduces the principal.

- Later Payments: As the loan matures, the principal balance decreases, and therefore, a larger portion of each payment is applied to the principal.

Reviewing an amortization schedule highlights this critical dynamic and can motivate strategies for early principal reduction.

Strategies for Reducing Total Interest Paid

Knowing your payment structure opens doors to strategies for minimizing the total interest paid:

- Make Extra Payments: Even small additional payments applied directly to the principal can significantly shorten the loan term and save interest. For example, paying an extra $50 a month on a $100,000 30-year mortgage at 6% could shave years off the loan and save thousands in interest.

- Bi-weekly Payments: Paying half of your monthly payment every two weeks results in 26 half-payments per year, which equates to one extra full monthly payment annually. This simple strategy can drastically reduce the loan term.

- Refinancing: If interest rates drop significantly since you took out your loan, or if your credit score has improved, refinancing to a lower interest rate can reduce both your monthly payment and the total interest paid. Be mindful of closing costs associated with refinancing.

What If You Pay More? Prepayment Penalties and Benefits

Before making extra payments, always check your loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early, typically to compensate for the lost interest income. While less common with conventional mortgages and most consumer loans, they can exist with certain types of loans.

Assuming no penalties, paying more than your required monthly payment offers significant benefits:

- Reduced Total Interest: This is the primary advantage, as you’re paying down the principal faster, meaning less interest accrues over time.

- Shorter Loan Term: You’ll pay off your loan sooner, freeing up cash flow for other financial goals.

- Increased Equity (for secured loans): For mortgages, faster principal reduction builds home equity more quickly.

Practical Applications and Common Loan Types

The principles of loan payment calculation apply across various loan types, though specific nuances may exist.

Mortgage Loan Payment Calculation

Mortgages are typically large, long-term loans. The calculated monthly payment covers principal and interest. However, often, the lender will also collect amounts for property taxes and homeowner’s insurance (escrow), which are added to your P&I (Principal & Interest) payment to form your total monthly housing payment. When using calculators, remember to distinguish between P&I and the full escrowed payment.

Auto Loan Payment Calculation

Auto loans are generally shorter-term (3-7 years) and involve smaller principal amounts than mortgages. The calculation is straightforward, focusing on the vehicle’s price, interest rate, and loan term. Watch out for extended terms (e.g., 84 months), which can lower monthly payments but lead to significant depreciation and higher total interest.

Personal Loan Payment Calculation

Personal loans are unsecured (no collateral) or secured and used for various purposes like debt consolidation, home improvements, or unexpected expenses. The calculation follows the standard amortization formula. Pay close attention to origination fees, which can reduce the net amount you receive from the loan.

Student Loan Payment Considerations

Student loans, particularly federal ones, often have unique features like deferred payments, income-driven repayment plans, and grace periods. While the basic calculation applies, these features can significantly alter your actual payment structure and total interest paid. Always consult your loan servicer for the most accurate payment information on student loans.

Mastering loan payment calculation is a vital component of financial literacy. By understanding the underlying mechanics, leveraging digital tools for efficiency, and considering the strategic implications of interest rates and loan terms, you can confidently navigate your borrowing decisions. This knowledge empowers you to manage your debts wisely, optimize your financial resources, and ultimately achieve greater financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.