The genesis of cryptocurrency is a journey that began long before Bitcoin’s public debut, rooted in decades of cryptographic research and an enduring desire for a decentralized form of digital money. While many equate the birth of crypto with Bitcoin in 2008-2009, its true origins lie in a series of conceptual breakthroughs and technological experiments that sought to create a secure, private, and censorship-resistant digital currency. Understanding this history is crucial for investors and financial professionals to grasp the underlying principles and long-term trajectory of this transformative asset class.

The Seeds of Digital Cash: Pre-Bitcoin Concepts

The idea of digital cash emerged in the 1980s, fueled by growing concerns over privacy in an increasingly digital world. Cryptographers and computer scientists envisioned electronic payment systems that could offer the anonymity of cash while operating securely online. However, these early attempts grappled with fundamental challenges that would only be fully resolved with the advent of Bitcoin.

Early Cryptographic Attempts and Digital Currencies

One of the earliest and most notable attempts was DigiCash, founded by cryptographer David Chaum in 1990. DigiCash aimed to provide anonymous electronic payments, protecting user privacy by employing cryptographic blind signatures. While technologically innovative, DigiCash ultimately failed to gain widespread adoption, partly due to its centralized nature and inability to scale globally. Users had to trust a single entity (DigiCash Inc.) with their funds, which ran counter to the evolving libertarian ethos that would later define much of the crypto movement.

Following DigiCash, various concepts like Hashcash (created by Adam Back in 1997) and B-Money (proposed by Wei Dai in 1998) laid critical groundwork. Hashcash was a proof-of-work system designed to combat email spam by requiring a small computational effort from the sender, a principle directly referenced in Satoshi Nakamoto’s Bitcoin whitepaper. B-Money, on the other hand, outlined a system of anonymous, distributed electronic cash, featuring concepts like proof-of-work to create currency and cryptographic commitments to ensure transaction integrity. Nick Szabo’s Bit Gold, proposed in 1998, went a step further, describing a protocol for a decentralized digital currency where participants would “mine” a series of proof-of-work functions, linking them cryptographically to create a chain of ownership. While Bit Gold was never implemented, its conceptual framework of a “chain of proofs” and a system to create scarce digital assets strongly foreshadowed Bitcoin.

The Fundamental Problem: Double-Spending and Centralization

Despite these innovative ideas, a major hurdle remained: the “double-spending problem.” In a digital environment, it’s easy to duplicate files. How could one ensure that a unit of digital currency was spent only once without relying on a trusted, central authority to verify every transaction? Centralized systems, like banks, solve this by maintaining a ledger and processing all transactions, preventing simultaneous identical payments. However, this centralization introduces points of failure, censorship, and control, which many sought to circumvent. The challenge was to create a digital cash system that was both decentralized (no single point of control) and immune to double-spending, maintaining the integrity and scarcity of its monetary units.

Bitcoin’s Genesis: A Revolutionary Answer

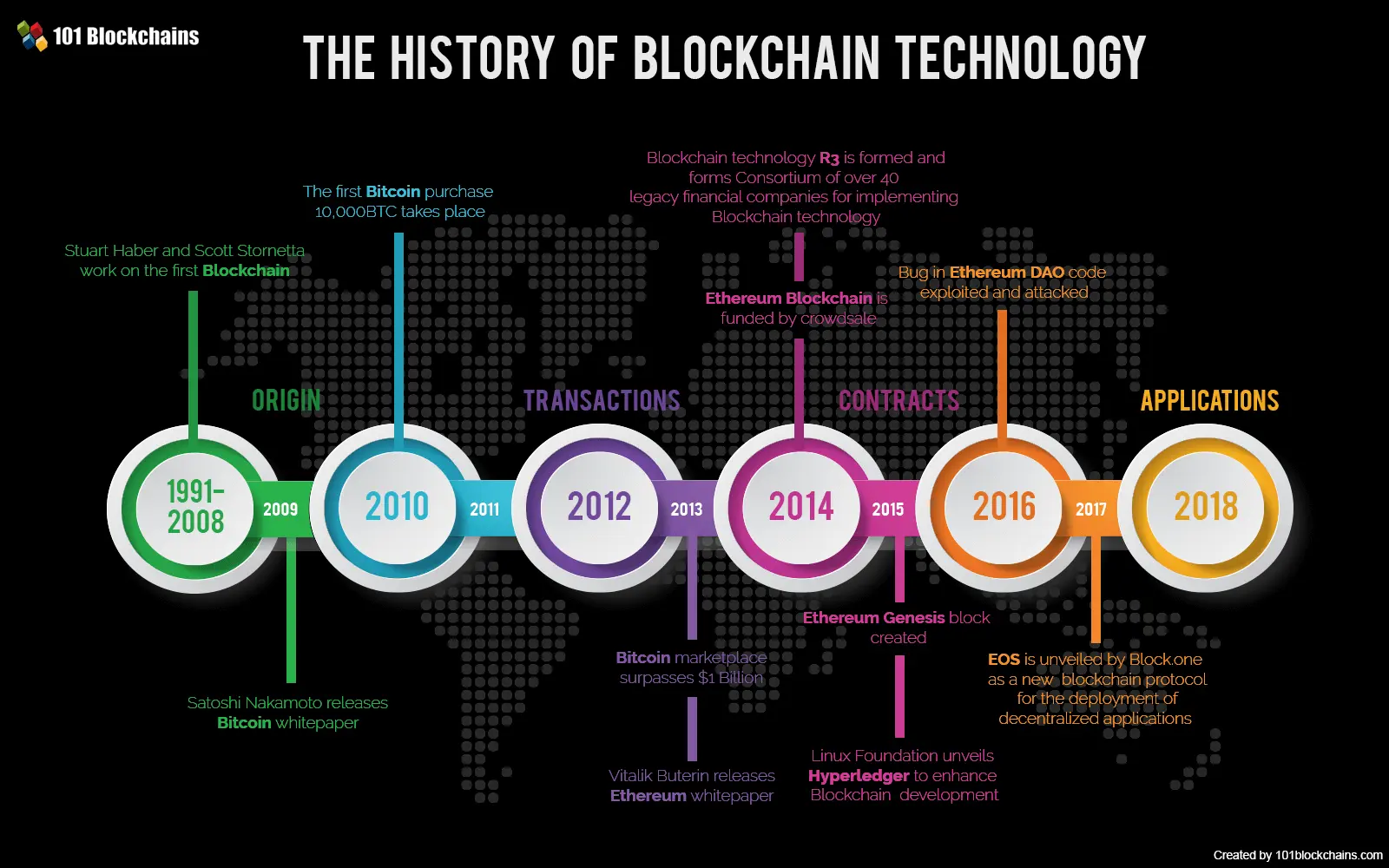

The solution to the double-spending problem in a decentralized network arrived in 2008 with the publication of a whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System,” authored by the pseudonymous Satoshi Nakamoto. This document outlined a groundbreaking new approach that combined existing cryptographic techniques with a novel system for maintaining a public, immutable ledger.

Satoshi Nakamoto’s Whitepaper: A New Financial Paradigm

On October 31, 2008, the Bitcoin whitepaper was released to a cryptography mailing list, presenting a radical vision for a completely decentralized digital currency. Nakamoto’s key innovation was the combination of a distributed ledger (the blockchain), proof-of-work for transaction validation (mining), and cryptographic signatures to secure ownership. This created a system where transactions were timestamped, bundled into blocks, and linked chronologically, forming an unbroken chain. Each block’s validity was secured by cryptographic proof, making it computationally infeasible to alter past transactions without redoing the entire chain. This elegant solution bypassed the need for a central authority, allowing participants to trust the network’s consensus mechanism rather than an intermediary.

From a financial perspective, Bitcoin offered several unprecedented features: global accessibility, censorship resistance, pseudonymity, and a fixed supply cap (21 million coins), making it a truly scarce digital asset. This scarcity, combined with its decentralized nature, presented a stark contrast to fiat currencies managed by central banks, immediately attracting individuals disillusioned with traditional financial systems and the fallout from the 2008 global financial crisis.

The Genesis Block and the First Transactions

The Bitcoin network officially launched on January 3, 2009, when Satoshi Nakamoto mined the “genesis block” – the very first block in the Bitcoin blockchain. Embedded within this block was a message: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” This message served as both a timestamp and a subtle commentary on the very economic conditions that fueled the need for a decentralized alternative.

The first actual Bitcoin transaction occurred on January 12, 2009, when Satoshi Nakamoto sent 10 Bitcoins to Hal Finney, a renowned cryptographer and early supporter. These initial exchanges, though small in scale, marked the beginning of a new financial era, demonstrating the practical functionality of a peer-to-peer electronic cash system. For the first few years, Bitcoin remained largely a curiosity among cryptographers and tech enthusiasts, with its monetary value being negligible. The famous “Bitcoin Pizza Day” on May 22, 2010, when 10,000 Bitcoins were used to purchase two pizzas, stands as a testament to its nascent value at the time.

Why Bitcoin Succeeded Where Others Failed

Bitcoin succeeded primarily due to its ingenious solution to the double-spending problem through a decentralized consensus mechanism (Proof-of-Work) and its open-source, peer-to-peer architecture. Unlike previous attempts that relied on central entities or lacked a robust defense against digital duplication, Bitcoin’s network was designed to be self-sustaining and resilient. Its carefully designed economic incentives, where “miners” were rewarded with newly minted bitcoins and transaction fees, ensured the security and continued operation of the network. This combination of robust technology, economic incentive, and a compelling narrative for financial sovereignty allowed Bitcoin to gain a foothold and begin building the network effect necessary for its long-term viability as a financial asset.

The Evolution Beyond Bitcoin: Altcoins and Expanding Financial Horizons

While Bitcoin established the foundational principles of cryptocurrency, its success paved the way for a vast ecosystem of alternative cryptocurrencies, or “altcoins,” each introducing new features, functionalities, and financial applications. This proliferation marked the beginning of crypto’s diversification from a singular digital cash concept to a multifaceted financial asset class.

Litecoin and Peercoin: Early Innovations

Early altcoins often sought to improve upon specific aspects of Bitcoin. Litecoin, launched in 2011 by Charlie Lee, aimed to be the “silver to Bitcoin’s gold” by offering faster transaction times and a different hashing algorithm (Scrypt instead of SHA-256) which was initially more accessible for general users to mine. From an investment perspective, Litecoin presented itself as a more efficient, everyday transactional currency. Peercoin, introduced in 2012, was pioneering for its hybrid Proof-of-Work/Proof-of-Stake consensus mechanism. Proof-of-Stake, where validation power is based on the amount of currency held, offered a potential solution to the energy consumption concerns associated with Proof-of-Work, influencing many subsequent blockchain designs. These early projects demonstrated that the underlying blockchain technology could be adapted and improved upon for different financial use cases.

Ethereum’s Breakthrough: Programmable Money and Smart Contracts

The true expansion of crypto’s financial potential came with Ethereum, conceived by Vitalik Buterin and launched in 2015. Ethereum introduced the concept of a “world computer” — a decentralized platform capable of running “smart contracts.” Smart contracts are self-executing contracts with the terms of the agreement directly written into code. This innovation allowed developers to build decentralized applications (dApps) on top of the Ethereum blockchain, leading to an explosion of new financial possibilities.

Ethereum’s programmability laid the groundwork for entirely new financial paradigms, including:

- Decentralized Finance (DeFi): This movement leverages smart contracts to create traditional financial services like lending, borrowing, trading, and insurance, all without intermediaries like banks. DeFi protocols have established new forms of collateralized lending, automated market making, and yield farming, offering investors novel avenues for earning returns on their digital assets.

- Non-Fungible Tokens (NFTs): While often associated with digital art, NFTs are essentially unique digital assets recorded on a blockchain, representing ownership of specific items (digital or physical). They have opened up new markets for verifiable digital collectibles, intellectual property, and even real estate, creating entirely new financial instruments and investment opportunities.

- Decentralized Autonomous Organizations (DAOs): These are organizations governed by code and community consensus, enabling new forms of collective ownership and decision-making for various financial ventures and projects, from venture capital funds to art collectives.

The Diversification of Digital Assets: A New Asset Class

The success of Ethereum catalyzed a wave of innovation, leading to thousands of cryptocurrencies, each with unique value propositions. From stablecoins pegged to fiat currencies, designed to mitigate volatility, to privacy coins focused on enhanced anonymity, and platform tokens powering entire ecosystems, the digital asset landscape diversified rapidly. This diversification transformed cryptocurrency from a singular concept of digital cash into a broad, complex asset class, attracting diverse investors and institutional interest. Understanding the specific utility and economic models of these various assets became a new frontier in financial analysis.

Crypto’s Maturation: From Niche to Mainstream Financial Consideration

In just over a decade, cryptocurrency has evolved from an obscure internet phenomenon to a significant force in the global financial landscape. Its journey from a niche technological experiment to a recognized asset class has been marked by increasing regulatory attention, institutional adoption, and a deeper integration into the broader economy.

Regulatory Scrutiny and Financial Integration

As crypto markets grew, so did the interest and concern from governments and financial regulators worldwide. Early years saw little oversight, but the sheer scale of the crypto economy eventually necessitated a more structured approach. Regulatory frameworks are now being developed and implemented across jurisdictions to address issues such as consumer protection, anti-money laundering (AML), combating terrorist financing (CTF), and market integrity. Securities and exchange commissions, central banks, and financial authorities are all grappling with how to classify, supervise, and tax various digital assets. This ongoing regulatory development is crucial for integrating crypto into the traditional financial system, offering clarity and potentially reducing risks for investors and financial institutions.

Institutional Adoption and Investment Vehicles

Initially shunned by mainstream finance, cryptocurrencies, particularly Bitcoin, have increasingly found their way into institutional portfolios and traditional investment vehicles. Publicly traded companies like MicroStrategy and Tesla have added Bitcoin to their balance sheets. Major financial institutions, including investment banks and asset managers, now offer crypto-related services, custody solutions, and research. The launch of Bitcoin futures contracts by the Chicago Mercantile Exchange (CME) in 2017, followed by Bitcoin spot ETFs (Exchange Traded Funds) in the US in 2024, marked significant milestones. These developments provide institutional investors with regulated and familiar avenues to gain exposure to digital assets, signaling a growing acceptance of crypto as a legitimate part of a diversified investment portfolio. Furthermore, the emergence of institutional-grade platforms for trading and managing digital assets underscores their increasing financial maturity.

The Future of Crypto: A Continuous Financial Frontier

The story of crypto, beginning with early cryptographic musings and blossoming with Bitcoin, is far from over. It represents an ongoing evolution in financial technology, constantly pushing the boundaries of what money and value can be. As the underlying technology continues to advance, and as new financial applications emerge, crypto is set to play an even more prominent role in global finance. From central bank digital currencies (CBDCs) exploring state-backed digital money to ongoing innovations in DeFi, NFTs, and the metaverse economy, the financial implications of crypto are continually expanding. For investors, understanding its origins provides invaluable context for navigating its complex present and anticipating its potentially transformative future. The question “when did crypto start” is not just about a date, but about the genesis of a paradigm shift that continues to redefine financial possibilities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.