For many individuals, the idea of paying taxes is confined to an annual ritual, a once-a-year submission of documents and a potential refund or payment. However, for a significant portion of the workforce, particularly the self-employed, freelancers, small business owners, and those with substantial investment income, tax obligations extend beyond a single filing date. These individuals are often required to pay estimated taxes quarterly throughout the year, a system designed to ensure that the Internal Revenue Service (IRS) collects income tax as it is earned. Failing to understand and properly set up these quarterly tax payments can lead to unpleasant surprises, including penalties and interest charges.

Navigating the world of estimated taxes can seem daunting at first, but with a clear understanding of the requirements, calculation methods, and payment procedures, it becomes an integral and manageable part of one’s financial strategy. This comprehensive guide will walk you through everything you need to know to accurately calculate, set up, and make your quarterly tax payments, ensuring compliance and peace of mind.

Understanding Quarterly Taxes: Who Needs to Pay?

Before diving into the mechanics of setting up payments, it’s crucial to identify who is actually obligated to make them. The IRS operates on a pay-as-you-go tax system. This means that if you don’t have taxes automatically withheld from your income (like typical W-2 employees), you’re responsible for paying them yourself throughout the year.

The Self-Employed and Gig Economy Workers

The most common group required to make quarterly tax payments comprises individuals who work for themselves. This includes freelancers, independent contractors, consultants, sole proprietors, partners in a partnership, and anyone who earns income from a business they own. When you’re self-employed, no employer is withholding income tax, Social Security, or Medicare taxes from your paychecks. Consequently, you’re responsible for paying both the employer and employee portions of Social Security and Medicare taxes (known as self-employment tax), in addition to your income tax liability.

Investment Income and Other Unwithheld Earnings

Quarterly payments aren’t exclusive to the self-employed. If you have significant income from sources that don’t have tax withheld, you might also need to pay estimated taxes. This can include:

- Rental income: From properties you own.

- Dividends and interest: From investments.

- Alimony: Received from divorce settlements (for agreements executed before 2019).

- Gambling winnings: Substantial amounts not subject to immediate withholding.

- Retirement or pension income: If you opt out of withholding or have substantial other income.

Essentially, if you expect to owe at least $1,000 in tax for the year and your withholding and credits are less than the smaller of 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your prior year’s adjusted gross income was over $150,000), you’ll likely need to make estimated payments.

Avoiding Penalties: The Underpayment Trap

The primary reason for making quarterly tax payments is to avoid underpayment penalties from the IRS. If you don’t pay enough tax throughout the year through withholding or estimated payments, you could face penalties, even if you pay the balance due by the April deadline. These penalties are calculated on the amount of underpayment for the period that the tax was not paid or was underpaid. Being proactive with your quarterly payments ensures you stay compliant and avoid these unnecessary charges.

Calculating Your Estimated Tax Liability

The most challenging aspect of quarterly taxes for many is accurately estimating their income and subsequent tax liability. Unlike a salaried employee with a predictable income, freelancers and business owners often have fluctuating earnings. However, a structured approach can make this process manageable.

Reviewing Your Prior Year’s Tax Return (Form 1040-ES)

Your previous year’s tax return is often the best starting point. It provides a baseline for your income, deductions, and credits. The IRS Form 1040-ES, “Estimated Tax for Individuals,” includes a worksheet that guides you through the calculation process. It essentially asks you to project your current year’s adjusted gross income (AGI), deductions, and credits based on your prior year’s figures, adjusted for any expected changes.

Estimating Current Year Income and Deductions

This step requires a good degree of foresight. Project all sources of income you expect to receive during the year, including self-employment income, investment income, and any other income not subject to withholding. Simultaneously, estimate your deductions (standard or itemized) and any credits you anticipate qualifying for (e.g., child tax credit, education credits). If you have a business, accurately projecting your gross receipts and business expenses is critical for determining your net self-employment income.

Accounting for Major Life Changes

Life circumstances can significantly impact your tax liability. A new job, marriage or divorce, the birth of a child, a large inheritance, or a substantial capital gain can all alter your tax situation. When estimating your quarterly payments, consider how these changes will affect your income, deductions, and credits for the current year and adjust your estimates accordingly. For instance, if you anticipate selling a major asset, the capital gains will need to be factored into your projected income.

Utilizing Tax Software and Professional Help

Many tax software programs offer estimated tax calculators as part of their suite of tools, which can simplify the process significantly. These tools can help you project your income and expenses and determine your estimated tax liability based on current tax laws. For complex situations, or if you feel overwhelmed, consulting a tax professional (like a CPA or enrolled agent) is highly recommended. They can help you accurately forecast your income and deductions, ensuring you make appropriate payments.

The 90% Rule and 100% (or 110%) Safe Harbor Rules

To avoid penalties, you generally need to pay at least 90% of your current year’s tax liability through withholding and estimated payments. Alternatively, you can satisfy a “safe harbor” rule by paying 100% of your prior year’s tax liability (or 110% if your prior year’s adjusted gross income was over $150,000). Whichever amount is smaller is your target for estimated payments. Understanding these rules is key to strategic tax planning and penalty avoidance.

Methods for Making Your Quarterly Payments

Once you’ve calculated your estimated tax liability, the next step is to actually make the payments. The IRS offers several convenient methods, ranging from electronic options to traditional mail.

IRS Direct Pay: The Easiest Option

IRS Direct Pay is a free, secure online service that allows you to pay your taxes directly from your checking or savings account. You can schedule payments up to 365 days in advance and receive immediate confirmation. This method is straightforward, requires no registration, and is highly recommended for its simplicity and efficiency.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is another robust electronic payment system, particularly useful for businesses or individuals who make frequent federal tax payments. It requires enrollment and provides a history of your payments. While it offers more features, Direct Pay is generally sufficient for individual estimated tax payments. Payments can be scheduled up to 365 days in advance.

Paying by Mail with Form 1040-ES Vouchers

For those who prefer a traditional approach, you can still pay your estimated taxes by mail using check or money order. If you use this method, it’s crucial to include a payment voucher from Form 1040-ES for each payment. The voucher ensures your payment is correctly credited to your account. Remember to write your name, address, Social Security number, and “20XX Form 1040-ES” on your check or money order.

Payment by Debit/Credit Card

You can also pay your estimated taxes using a debit or credit card through third-party payment processors. While convenient, this option typically involves a processing fee charged by the third-party provider, which can range from 1.87% to 2.25% for credit cards, plus a flat fee for debit cards. Consider this option only if the convenience outweighs the additional cost or if you are trying to meet minimum spend requirements for credit card rewards.

Adjusting W-4 Withholding (for Salaried Individuals with Side Income)

If you are primarily a W-2 employee with a side hustle or investment income that necessitates estimated payments, you might be able to avoid making separate quarterly payments by adjusting your W-4 withholding with your employer. By increasing your withholding, you can have more tax taken out of each paycheck, effectively covering your additional tax liability without the need for separate quarterly payments. Use the IRS Tax Withholding Estimator tool on IRS.gov to determine the appropriate adjustments.

Key Dates and Strategic Planning

Managing quarterly tax payments isn’t just about calculation; it’s also about timing and consistent financial discipline. Missing a deadline can result in penalties, while strategic planning can ease the burden.

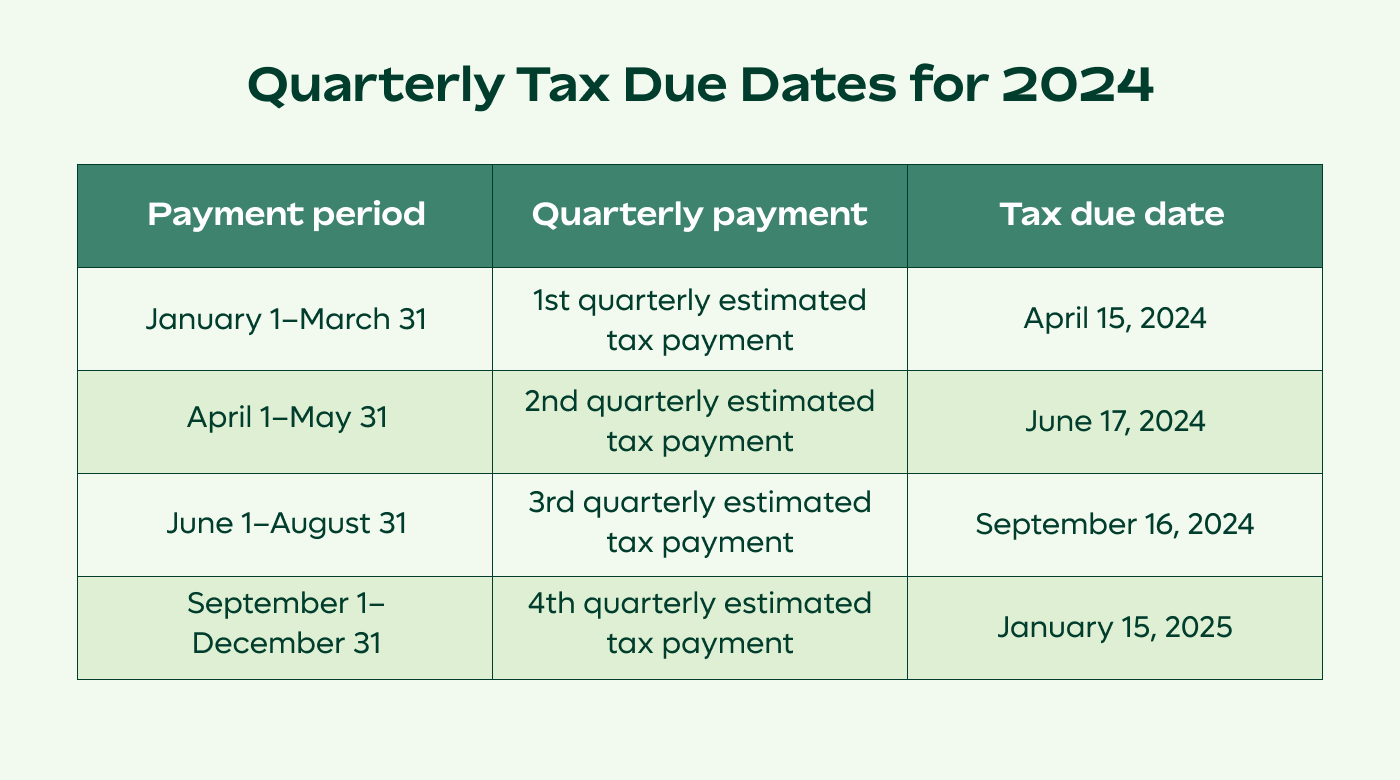

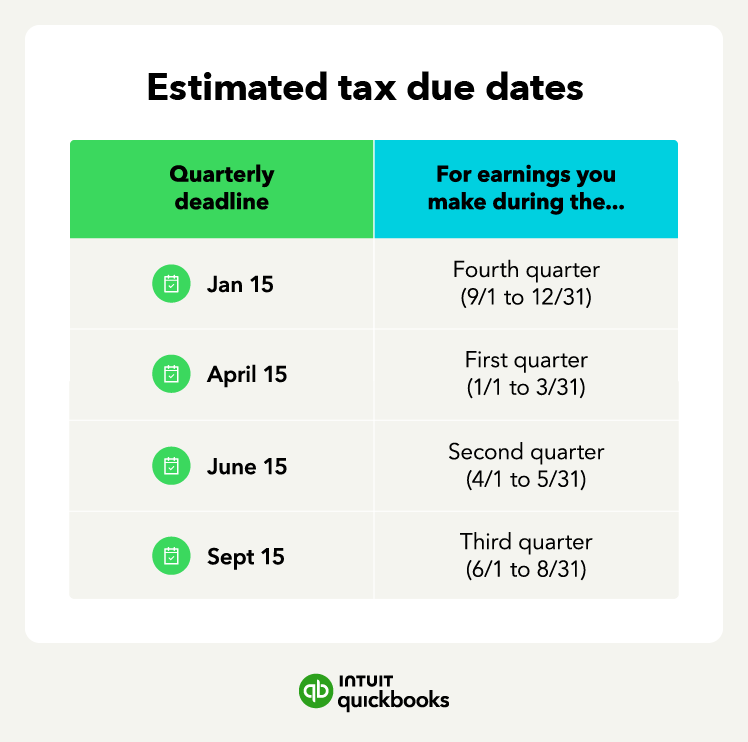

Understanding the Payment Due Dates

The tax year is divided into four payment periods, each with a specific due date. It’s important to mark these on your calendar:

- Period 1 (Jan 1 to March 31): Due April 15

- Period 2 (April 1 to May 31): Due June 15

- Period 3 (June 1 to Aug 31): Due September 15

- Period 4 (Sept 1 to Dec 31): Due January 15 of the following year

If any of these dates fall on a weekend or holiday, the deadline is shifted to the next business day. It’s important to note that even though the periods are uneven, the IRS generally expects you to pay roughly one-fourth of your estimated tax each period. However, if your income fluctuates significantly, you can use the annualized income method on Form 2210 to adjust payments to match when income is actually earned.

Proactive Budgeting and Saving for Taxes

One of the best practices for managing quarterly taxes is to set aside a portion of every payment or income stream specifically for taxes. Rather than scrambling to find funds just before each deadline, consistently allocating a percentage of your earnings to a dedicated “tax savings account” ensures that the money is always available when due. A common rule of thumb for self-employed individuals is to set aside 25-35% of their net income, but this can vary based on individual circumstances and tax brackets.

Regular Review and Adjustment of Estimates

Your initial estimate is just that – an estimate. Throughout the year, your income and expenses may change, rendering your initial projections inaccurate. It’s wise to review your income, deductions, and actual tax liability quarterly, or at least midway through the year. If you find your income is significantly higher or lower than expected, adjust your remaining payments accordingly. Overpaying ensures you avoid penalties, but tying up too much cash in overpayment might not be the most efficient use of your funds. Conversely, underpaying could lead to penalties.

What to Do If You Miss a Payment or Overpay

If you miss a payment deadline, make the payment as soon as possible. The penalty for underpayment is calculated from the due date of the installment until the date the payment is made. While a one-time slip-up might incur a small penalty, consistent underpayment or missed payments can add up. If you overpay your estimated taxes, the IRS will typically apply the excess amount to your next year’s tax liability or refund it to you when you file your annual return.

Advanced Strategies and Best Practices

Moving beyond the basics, some advanced strategies can further streamline your quarterly tax process and optimize your financial health.

Setting Up a Dedicated Tax Savings Account

As mentioned earlier, establishing a separate bank account exclusively for your tax savings is a game-changer. This physical separation prevents you from accidentally spending money earmarked for taxes and gives you a clear picture of your available funds. You can even set up automatic transfers from your primary checking account to this tax account each time you receive income.

Record-Keeping Essentials

Meticulous record-keeping is not just good practice; it’s essential for accuracy and audit readiness. Keep detailed records of all your income and expenses, especially for your business. Digital tools, spreadsheets, or accounting software can help automate and organize this process. Good records will make calculating your estimated tax liability easier and significantly simplify filing your annual tax return.

When to Consult a Tax Professional

While this guide provides a comprehensive overview, some situations warrant professional advice. If your income sources are complex, if you’ve experienced significant life changes, or if you’re unsure about specific deductions or credits, a qualified tax professional can provide tailored guidance. They can help you optimize your tax strategy, ensure compliance, and even represent you in the event of an IRS inquiry.

State Estimated Taxes

Remember that federal estimated taxes are only part of the equation. Most states that levy income tax also have their own estimated tax requirements, often with similar quarterly payment schedules. Be sure to research and comply with your state’s specific rules to avoid additional state-level penalties.

In conclusion, setting up quarterly tax payments is a vital aspect of financial management for anyone with income not subject to traditional withholding. By understanding who needs to pay, how to accurately calculate your liability, utilizing available payment methods, and adhering to key deadlines, you can effectively manage your tax obligations. Proactive planning, diligent record-keeping, and strategic saving will not only help you avoid penalties but also provide a greater sense of financial control and peace of mind throughout the year. Embrace the quarterly tax payment system as an opportunity to stay on top of your finances, rather than viewing it as a burden.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.