Navigating the complexities of federal income tax filing can often feel like a daunting annual ritual for many Americans. Far from being a mere bureaucratic chore, understanding how to properly file your federal taxes is a fundamental cornerstone of sound personal finance, impacting everything from your annual budget to long-term financial planning. This comprehensive guide aims to demystify the process, offering insights and practical steps to ensure you meet your obligations accurately, efficiently, and with confidence, potentially optimizing your financial outcome in the process.

Each year, millions of individuals and businesses contribute to the nation’s infrastructure and public services through their tax payments. While the Internal Revenue Service (IRS) continually strives to simplify the process, the onus remains on the taxpayer to understand their responsibilities, gather the necessary documentation, and choose the most suitable method for submitting their return. This article will break down the essential components of federal tax filing, transforming a potentially stressful task into a manageable and even empowering financial exercise.

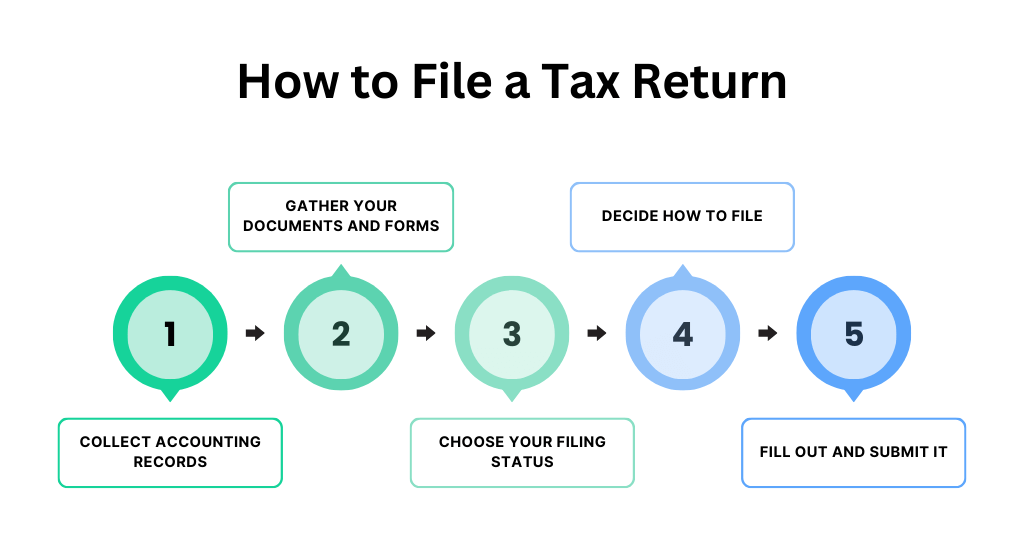

Understanding Your Tax Obligations

Before you can even begin to think about filling out forms, it’s crucial to grasp the fundamental aspects of your tax obligations. This foundational knowledge empowers you to approach the filing process strategically and avoid common pitfalls.

Who Needs to File?

Not everyone is required to file a federal income tax return. The obligation primarily depends on your gross income, filing status, and age. The IRS sets specific income thresholds annually. For instance, if you’re single and under 65, you might not need to file if your gross income is below a certain amount. However, even if you’re not required to file, you might still want to if you qualify for certain refundable tax credits (like the Earned Income Tax Credit or Additional Child Tax Credit) or if you had federal income tax withheld from your paychecks and are due a refund. It’s always wise to check the IRS guidelines for the specific tax year in question to determine your filing requirement. Additionally, individuals who are self-employed with net earnings above a certain threshold, or those who received certain types of income (e.g., from investments or rental properties), generally have a filing obligation regardless of overall gross income.

Key Tax Forms and Documents

The backbone of tax filing is the accurate collection and understanding of various financial documents. The most common include:

- Form W-2, Wage and Tax Statement: Received from your employer, this form reports your annual wages and the amount of federal, state, and local taxes withheld. If you have multiple employers, you’ll receive multiple W-2s.

- Form 1099 Series: These forms report various types of income not from an employer. Examples include:

- 1099-NEC (Nonemployee Compensation): For independent contractors or gig workers.

- 1099-INT (Interest Income): From banks and other financial institutions.

- 1099-DIV (Dividends and Distributions): From stocks and mutual funds.

- 1099-B (Proceeds From Broker and Barter Exchange Transactions): For sales of stocks, bonds, and other securities.

- 1099-R (Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.): For retirement income.

- 1099-MISC (Miscellaneous Information): For various other types of income not covered by other 1099s.

- Form 1098 Series: These forms report deductible expenses. Examples include:

- 1098 (Mortgage Interest Statement): Reports mortgage interest paid.

- 1098-E (Student Loan Interest Statement): Reports student loan interest paid.

- 1098-T (Tuition Statement): Reports tuition paid for higher education.

- Health Insurance Information: Depending on your health coverage, you might receive Form 1095-A, B, or C.

- Records for Deductions and Credits: Keep meticulous records for charitable donations, medical expenses, business expenses for self-employed individuals, childcare costs, and other potential deductions or credits. These often don’t come on official IRS forms but are crucial for substantiating your claims.

Important Deadlines

The most well-known federal tax deadline is April 15th for most individual taxpayers, though this date can shift slightly if it falls on a weekend or holiday. This is the deadline to file your return and pay any taxes you owe for the previous calendar year. If you can’t file on time, you can request an automatic six-month extension by filing Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. It’s vital to remember that an extension to file is not an extension to pay. If you expect to owe taxes, you should estimate and pay them by the original April deadline to avoid penalties and interest. Self-employed individuals and those with significant income not subject to withholding may also have quarterly estimated tax payment deadlines throughout the year (April 15, June 15, September 15, and January 15 of the following year). Missing these can also result in penalties.

Choosing Your Filing Method

Once you understand your obligations and have gathered your documents, the next step is to decide how you will prepare and submit your tax return. Several options are available, each with its own advantages and suitable for different financial situations and comfort levels.

DIY Tax Software

For many taxpayers, especially those with straightforward financial situations, do-it-yourself tax software has become the go-to choice. These financial tools guide you step-by-step through the filing process, asking questions about your income, deductions, and credits, then automatically filling out the correct forms. Popular options like TurboTax, H&R Block Tax Software, and TaxAct offer both online and desktop versions, catering to various operating systems and preferences.

The benefits of DIY software include cost-effectiveness (often cheaper than a professional), convenience (file from anywhere, anytime), and a sense of control over your financial data. Most software packages include accuracy guarantees and audit support features. However, it requires a certain level of comfort with technology and the ability to accurately interpret your financial documents. While the software simplifies complex calculations, the responsibility for inputting correct information ultimately rests with you. Choosing the right software often depends on the complexity of your tax situation; basic versions might be free or low-cost for simple returns, while those with investments, self-employment income, or rental properties will likely need a more advanced, and pricier, version.

Hiring a Tax Professional

For those with complex financial situations, such as business owners, individuals with significant investment portfolios, those who’ve experienced major life changes (marriage, divorce, new home), or simply those who prefer peace of mind, hiring a tax professional can be an invaluable investment. Certified Public Accountants (CPAs), Enrolled Agents (EAs), and other professional tax preparers offer expertise in tax law, can identify overlooked deductions and credits, and represent you in the event of an audit.

A good tax professional can offer strategic financial planning advice beyond just filing your current year’s taxes, helping you minimize future tax liabilities. They can navigate intricate tax codes, ensure compliance, and often save you more money than their fees cost. When selecting a professional, look for credentials, experience with situations similar to yours, and transparent fee structures. Always ensure they are authorized to e-file and have an IRS Preparer Tax Identification Number (PTIN).

Free Tax Filing Options

The IRS is committed to making tax filing accessible. Several free options are available for eligible taxpayers:

- IRS Free File: This program allows taxpayers with adjusted gross income (AGI) below a certain threshold (which changes annually) to use guided tax preparation software from leading tax software companies at no cost. For those with higher AGIs, Free File Fillable Forms provides electronic versions of IRS paper forms, suitable for those comfortable doing their own calculations.

- Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE): These IRS-sponsored programs offer free tax preparation and e-filing services to qualified individuals. VITA serves people who generally make $64,000 or less, persons with disabilities, and limited English-speaking taxpayers. TCE specializes in tax issues unique to seniors, generally 60 years or older. Both programs use IRS-certified volunteers. These are excellent resources for personalized, free assistance, particularly for those who prefer human guidance over software.

Gathering Your Financial Information

Regardless of your chosen filing method, meticulous preparation of your financial documents is paramount. This stage requires patience and organization but is crucial for accurate and optimized tax filing.

Income Records

Start by compiling all documents detailing your income. This includes:

- W-2s from all employers.

- All 1099 forms (NEC, INT, DIV, B, R, MISC) covering any non-employment income, investment income, retirement distributions, etc.

- Records of cash income not reported on a 1099, tips, or income from side hustles that didn’t generate official forms.

- Statements from social security benefits (Form SSA-1099).

- Documentation for rental income or royalty income.

- Any other documentation of income, whether taxable or not (e.g., tax-exempt interest).

Deduction and Credit Documentation

This is where proactive record-keeping truly pays off. Gather all records that support potential deductions or credits:

- Mortgage interest statements (Form 1098) and real estate tax payments.

- Student loan interest statements (Form 1098-E) and tuition statements (Form 1098-T).

- Records of charitable contributions (cash receipts, donation letters for non-cash items).

- Medical expense records (if itemizing and they exceed a certain percentage of your AGI).

- Childcare expenses (including provider’s name, address, and EIN/SSN).

- IRA or retirement account contributions.

- Receipts for business expenses if you’re self-employed.

- Records for energy-efficient home improvements or other specific tax credits you might qualify for.

Investment and Savings Statements

Don’t overlook information related to your investments and savings, as these can significantly impact your tax return:

- Brokerage statements detailing gains and losses from stock sales, dividends, and interest.

- Bank statements for interest earned on savings accounts.

- Mutual fund statements showing distributions.

- Information on any cryptocurrency transactions, as these are typically treated as property for tax purposes.

The Filing Process: Step-by-Step

With all your financial ducks in a row, you can now proceed to the actual process of preparing and submitting your return.

Inputting Your Data

Whether you’re using software or working with a professional, this step involves systematically entering all your gathered financial information into the appropriate fields. If using software, follow the prompts carefully. It’s crucial to ensure every figure from your W-2s, 1099s, and other documents is entered precisely as it appears. Common pitfalls include transposing numbers, missing a form, or miscategorizing income or expenses. Take your time and double-check each entry.

Reviewing for Accuracy and Optimization

Before hitting “submit,” conduct a thorough review of your entire return. Most tax software includes a review function that checks for errors or missing information. Pay close attention to:

- Personal information: Correct name, SSN, date of birth, and filing status.

- Dependent information: Correct names, SSNs, and relationship.

- Income totals: Do they match your W-2s and 1099s?

- Deductions and credits: Have you claimed all applicable ones? Have you chosen between the standard deduction and itemizing if it’s more beneficial?

- Bank account information: If you’re receiving a refund or paying via direct debit, ensure your routing and account numbers are correct.

- State tax return: If you’re filing a state return, ensure consistency with your federal return.

This review phase is also an opportunity for optimization. Are there any overlooked opportunities for tax savings? For instance, did you contribute to an IRA and forget to claim the deduction? Did you incur significant medical expenses that might push you over the itemizing threshold?

Submitting Your Return

The vast majority of taxpayers now e-file their federal tax returns, which is generally faster, more secure, and reduces the chance of errors compared to mailing a paper return. If you’re using tax software or a professional, e-filing is typically integrated into their service. After submission, you’ll usually receive an email confirmation that the IRS has accepted your return.

If you choose to mail a paper return, ensure you use the correct IRS mailing address for your state (found on the IRS website). Send it via certified mail with a return receipt for proof of mailing and delivery. Always sign and date your return and include all necessary forms and schedules.

Paying or Receiving Your Refund

If you owe taxes, you have several options for payment:

- Direct Pay: Through the IRS website, you can pay directly from your checking or savings account.

- Electronic Federal Tax Payment System (EFTPS): A free service for individuals and businesses.

- Debit Card, Credit Card, or Digital Wallet: Through third-party processors (fees may apply).

- Electronic Funds Withdrawal: Available if you e-file and authorize the IRS to withdraw payment from your bank account.

- Check or Money Order: Mailed with Form 1040-V, Payment Voucher.

If you’re due a refund, electing direct deposit into your bank account is the quickest way to receive it. You can track the status of your refund using the “Where’s My Refund?” tool on the IRS website.

Post-Filing Best Practices

Your tax duties don’t end the moment you hit “submit” or drop your envelope in the mail. A few crucial steps after filing can safeguard your financial well-being.

Record Keeping for Future Reference

After filing, it’s essential to keep copies of your tax return and all supporting documentation for at least three years. The IRS generally has three years to audit your return from the date you filed it (or the due date, whichever is later). For more complex situations, like underreporting income, this period can extend to six years. Store these documents securely, preferably both digitally and physically. These records are invaluable if you’re audited, need to amend a return, or apply for loans in the future.

What to Do if You Made a Mistake

Discovering an error after you’ve filed your return isn’t the end of the world. You can typically correct it by filing an amended return using Form 1040-X, Amended U.S. Individual Income Tax Return. File an amended return as soon as you discover the error, especially if it results in additional tax owed. If the error leads to a larger refund, you generally have three years from the date you filed your original return or two years from the date you paid the tax, whichever is later, to file an amended return to claim the refund.

Planning for Next Year’s Taxes

Tax filing shouldn’t just be an annual sprint; it should be part of a continuous financial strategy. After filing, take some time to review your tax outcome. Did you owe a lot, indicating you might need to adjust your withholdings (Form W-4) or make estimated payments? Did you receive a huge refund, suggesting you had too much withheld and could have had more money throughout the year?

Consider proactive strategies for the coming year:

- Maximize tax-advantaged accounts: Contribute to 401(k)s, IRAs, and HSAs to reduce taxable income.

- Keep better records: Implement a system for tracking income and expenses throughout the year.

- Understand tax law changes: Stay informed about new tax laws or provisions that might affect your financial situation.

- Consult a financial planner: Work with a professional to integrate tax planning into your broader financial goals, optimizing your investments and financial decisions to minimize your tax burden legally.

By understanding your obligations, choosing the right tools, meticulously gathering information, and embracing post-filing best practices, you can transform the often-dreaded task of federal tax filing into a powerful annual review of your financial health, ensuring compliance and fostering long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.