For many individuals, the ritual of tax season culminates in filing a single return and, perhaps, receiving a refund or paying a final balance. However, for a significant portion of the workforce, particularly those navigating the dynamic landscapes of self-employment, the gig economy, or diverse investment portfolios, the tax obligation isn’t a once-a-year event. Instead, it’s a recurring responsibility met through federal estimated tax payments. This mechanism ensures that taxpayers pay income tax as they earn or receive income throughout the year, rather than waiting until the annual tax filing deadline.

Understanding and correctly executing estimated tax payments is crucial not only for compliance with IRS regulations but also for effective personal and business financial planning. Failing to pay enough tax through withholding or estimated payments can lead to penalties, adding an unnecessary burden to your financial commitments. This comprehensive guide will demystify the process, providing insights into who needs to pay, how to calculate your obligations, the various methods available for payment, and essential strategies for seamless financial management.

Who Needs to Pay Federal Estimated Taxes?

The fundamental principle behind estimated tax payments is “pay-as-you-go.” The U.S. tax system requires taxpayers to pay most of their tax liability throughout the year, either through withholding from wages or through estimated tax payments. If you don’t have an employer withholding taxes on your behalf, or if the amount withheld is insufficient, you likely fall into the category of individuals needing to make estimated payments.

Self-Employed Individuals and Gig Economy Workers

This is perhaps the largest demographic requiring estimated tax payments. If you are a freelancer, independent contractor, small business owner, or participate in the gig economy (e.g., rideshare driver, delivery service, online seller), you are considered self-employed. As such, your income is not subject to employer withholding. This means you are responsible for paying not only your income tax but also self-employment taxes (Social Security and Medicare taxes) directly to the IRS. Generally, if you expect to owe at least $1,000 in tax for the year from your self-employment income, you should be making estimated payments.

Investors and High-Income Earners

Beyond earned income, various other income sources can trigger the need for estimated tax payments:

- Interest and Dividends: Substantial income from savings accounts, bonds, stocks, and mutual funds.

- Capital Gains: Profits from the sale of investments or property.

- Rental Income: Earnings from rental properties.

- Alimony: While subject to changes under the Tax Cuts and Jobs Act of 2017 for new divorces, older agreements may still require estimated payments on alimony received.

- Gambling Winnings: Significant winnings from lotteries, casinos, or other forms of gambling.

- Retirement Income (without sufficient withholding): If you’re receiving distributions from pensions, annuities, or IRAs and haven’t opted for adequate withholding, you might need to make estimated payments.

The critical threshold to remember is the $1,000 mark for individuals. If you expect to owe at least $1,000 in federal income tax for the year, you’ll generally need to make estimated payments. Corporations, too, are required to pay estimated tax if they expect to owe $500 or more.

Understanding the Underpayment Penalty Threshold

Even if you fall into one of the categories above, you might be exempt from estimated payments if you meet specific criteria that prevent an underpayment penalty. You typically avoid an underpayment penalty if you owe less than $1,000 in tax for the year, or if you paid at least 90% of the tax due for the current year, or 100% of the tax shown on your return for the prior year (110% if your adjusted gross income (AGI) in the prior year was more than $150,000). These are often referred to as “safe harbor” rules and can be a strategic way to manage your payments without incurring penalties.

Calculating Your Estimated Tax Liability

Accurately calculating your estimated tax is the cornerstone of effective tax management. It’s not just about guessing; it involves a methodical projection of your income, deductions, and credits for the entire tax year.

Using Form 1040-ES

The primary tool for calculating estimated taxes is Form 1040-ES, Estimated Tax for Individuals. This form includes a worksheet that guides you through the process of estimating your:

- Adjusted Gross Income (AGI): All your expected income sources, minus specific adjustments.

- Deductions: Whether you plan to take the standard deduction or itemize deductions.

- Taxable Income: AGI minus deductions.

- Tax: Calculated based on your taxable income using the appropriate tax rates.

- Credits: Any tax credits you expect to qualify for (e.g., child tax credit, education credits).

- Self-Employment Tax: If applicable, this is calculated separately and added to your income tax liability.

The worksheet then helps you determine your total estimated tax liability for the year, which is typically divided into four equal quarterly payments.

Factoring in Income, Deductions, and Credits

The accuracy of your estimated payments depends heavily on the accuracy of your projections.

- Income: Be realistic about your expected earnings. If your income fluctuates, you might need to re-evaluate your estimates throughout the year. Consider all sources, including self-employment, investments, and any other taxable income.

- Deductions: Account for any significant deductions you anticipate. This could include traditional IRA contributions, student loan interest, health savings account (HSA) contributions, or itemized deductions like mortgage interest and charitable contributions if they exceed the standard deduction.

- Credits: Don’t forget any tax credits that reduce your tax liability dollar-for-dollar. These are incredibly valuable and can significantly lower your estimated payments.

Annualized Income Method for Fluctuating Income

For individuals with income that varies significantly throughout the year (e.g., seasonal businesses, large bonuses, or significant capital gains at specific times), the standard equal quarterly payments might not be appropriate. The annualized income method allows you to pay estimated tax based on your income as you earn it. This means if you earn more in the first quarter, you’d pay more for that quarter. If your income is low in the second quarter, your payment for that quarter would be lower. This method can help avoid underpayment penalties that might arise if you spread out an unpredictable annual income evenly. Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts, includes a worksheet for calculating payments using this method.

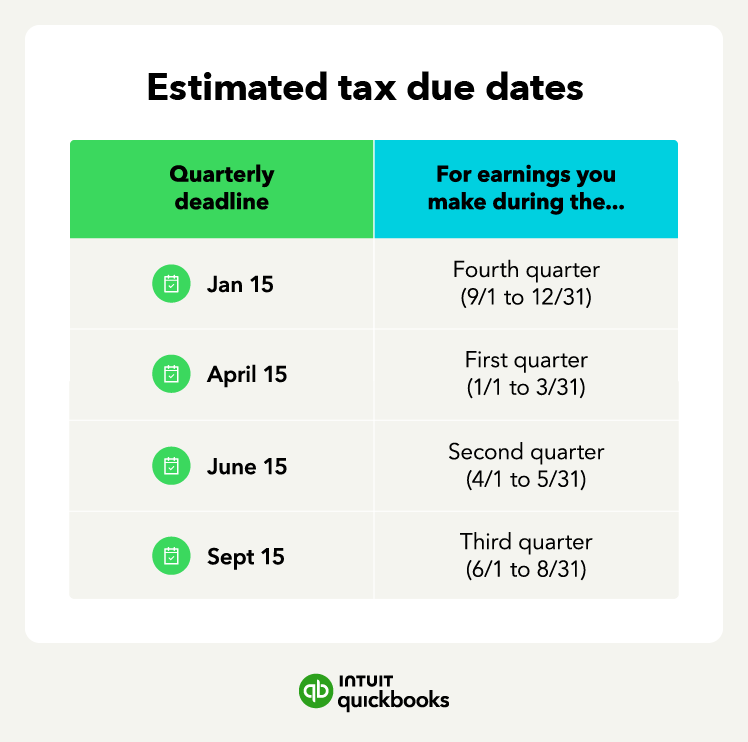

Quarterly Payment Schedule

The IRS sets specific deadlines for estimated tax payments, generally falling on the 15th of April, June, September, and January of the following year. If a due date falls on a weekend or holiday, the deadline shifts to the next business day. It’s crucial to adhere to these deadlines to avoid penalties.

- Payment 1 (January 1 to March 31 income): Due April 15

- Payment 2 (April 1 to May 31 income): Due June 15

- Payment 3 (June 1 to August 31 income): Due September 15

- Payment 4 (September 1 to December 31 income): Due January 15 of the next year

Methods for Making Your Payments

Once you’ve calculated your estimated tax, the next step is to make the payments. The IRS offers several convenient and secure options.

IRS Direct Pay

IRS Direct Pay is arguably the most straightforward and fastest way to pay your federal estimated taxes directly from your checking or savings account. It’s free, secure, and doesn’t require pre-registration. You simply visit the IRS website, select “Estimated Tax” as your payment reason, enter your bank account information, and schedule your payment. You’ll receive an immediate confirmation email once your payment is submitted.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is a robust, secure, and free online system designed for both individual and business taxpayers to make all types of federal tax payments. While it requires a one-time enrollment process (which can take a few days to receive your PIN by mail), it offers excellent flexibility. You can schedule payments up to 365 days in advance, review your payment history, and receive email confirmations. For business owners, EFTPS is particularly useful as it handles a wide array of business taxes, including employer payroll taxes.

Credit/Debit Card or Digital Wallet

You can also pay your estimated taxes using a credit card, debit card, or a digital wallet (like PayPal). This option is processed through third-party payment processors who charge a small fee for their service. While there’s a fee, some taxpayers prefer this method for the convenience, potential to earn credit card rewards, or for managing cash flow. The IRS provides a list of approved payment processors on its website.

Mail (Check or Money Order)

For those who prefer traditional methods, you can still mail in your estimated tax payments. This involves filling out a payment voucher (Form 1040-ES, Payment Voucher) and mailing it along with a check or money order payable to the “U.S. Treasury.” It’s essential to use the correct mailing address for your state, which can be found in the Form 1040-ES instructions. Always mail early to ensure it’s postmarked by the due date.

Penalties and Pitfalls to Avoid

Navigating estimated taxes effectively means understanding not only how to pay but also the consequences of not paying correctly.

Understanding Underpayment Penalties

The IRS may charge a penalty if you don’t pay enough tax through withholding and estimated payments. The penalty applies if your total tax payments (withholding plus estimated payments) are less than 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your AGI was over $150,000). The penalty is calculated based on the underpayment amount for each payment period and the current interest rate, which can change quarterly. It’s not a flat fee but rather an annualized interest charge.

Common Mistakes to Sidestep

- Underestimating Income: The most frequent mistake is simply under-projecting annual income, leading to insufficient payments.

- Ignoring Self-Employment Tax: Many self-employed individuals forget to include their self-employment tax (Social Security and Medicare) in their estimated tax calculations. This can be a significant portion of your liability.

- Missing Deadlines: Each quarterly payment has a strict deadline. Missing them can trigger penalties even if your total annual payment is sufficient.

- Not Adjusting Throughout the Year: Your financial situation isn’t static. If you have a significant increase or decrease in income, or a major life event, you need to revisit and adjust your estimated payments.

- Relying on Old Habits: If your income sources or employment status changes, your tax obligations change too. Don’t assume what worked last year will work this year.

Seeking Professional Guidance

For complex financial situations, fluctuating incomes, or simply for peace of mind, consulting with a tax professional (like a CPA or Enrolled Agent) is highly recommended. They can help you accurately project your income, identify applicable deductions and credits, navigate the annualized income method, and ensure you comply with all IRS regulations, potentially saving you from costly penalties.

Strategies for Managing Estimated Tax Payments

Proactive management of estimated tax payments can integrate seamlessly with your overall financial planning, reducing stress and optimizing your financial health.

Budgeting for Tax Payments

Treat your estimated tax payments like any other recurring expense. Create a separate savings account for your tax money or simply earmark a portion of each incoming payment for taxes. This “tax fund” ensures the money is available when payment deadlines roll around, preventing last-minute scrambles or dipping into funds needed for other purposes. Aim to set aside 25-35% of your gross self-employment income, or adjust based on your specific tax bracket and deductions.

Adjusting Withholding (If Applicable)

If you have a W-2 job in addition to self-employment or investment income, you might be able to avoid estimated tax payments by simply adjusting the withholding from your employee wages. You can increase the amount withheld from your paycheck by submitting a new Form W-4 to your employer. This can be a simpler alternative to making quarterly payments for some individuals, as the employer sends the money to the IRS on your behalf.

Tax Planning Throughout the Year

Effective tax planning is an ongoing process, not an annual event. Regularly review your income and expenses, especially if they deviate significantly from your initial projections. This proactive approach allows you to adjust your estimated payments as needed, preventing large underpayments or overpayments. Consider setting quarterly reminders to re-evaluate your tax situation and make any necessary adjustments to your payments.

Leveraging Tax Software and Tools

Modern tax software can be an invaluable asset for managing estimated taxes. Many programs offer tools to help you calculate your estimated tax liability based on your projected income and expenses. Some even integrate with online banking to streamline payments. Additionally, various financial planning apps and spreadsheets can help you track your income and deductions, making the quarterly calculation process more manageable.

Making federal estimated tax payments is a critical responsibility for many taxpayers, requiring diligence and foresight. By understanding who needs to pay, accurately calculating your obligations, utilizing convenient payment methods, and adopting proactive management strategies, you can meet your tax responsibilities confidently and avoid unnecessary penalties, allowing you to focus on growing your income and achieving your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.