Securing a home loan is a significant financial milestone, representing a crucial step towards homeownership. While the prospect can seem daunting, understanding the key requirements and preparing your finances systematically can streamline the process. Lenders assess a range of factors to determine your eligibility and the terms of your loan, primarily focusing on your ability and willingness to repay the debt. This involves a deep dive into your credit history, income stability, existing debts, and available assets. Approaching this process with a clear understanding of what lenders look for will empower you to present the strongest possible application.

The Foundation: Financial Readiness

Before you even begin house hunting, establishing a solid financial foundation is paramount. Lenders want assurance that you are a reliable borrower, and this assurance comes from a comprehensive review of your financial health.

Credit Score: Your Financial Passport

Your credit score is arguably the most critical component lenders scrutinize. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Scores typically range from 300 to 850, with higher scores indicating lower risk. While the exact minimum score varies by loan program and lender, a score of 620-640 is generally considered a baseline for conventional loans, with higher scores (740+) opening doors to better interest rates and terms. To improve your score, focus on paying bills on time, keeping credit utilization low, and avoiding new credit inquiries in the months leading up to your application. Regularly check your credit report for inaccuracies, which can negatively impact your score.

Down Payment: The Initial Investment

The down payment is the upfront cash you contribute towards the home’s purchase price. It signals your commitment and reduces the amount you need to borrow, thereby lowering the lender’s risk. While a 20% down payment is often cited as ideal to avoid Private Mortgage Insurance (PMI) on conventional loans, many programs allow for much less, sometimes as low as 3-5% for conventional loans, or even 0% for VA and USDA loans. The size of your down payment directly influences your loan-to-value (LTV) ratio, monthly mortgage payments, and the total interest paid over the life of the loan. Saving diligently for a substantial down payment can significantly impact your financial future as a homeowner.

Debt-to-Income (DTI) Ratio: Managing Your Obligations

Your debt-to-income (DTI) ratio is a critical metric that compares your total monthly debt payments to your gross monthly income. Lenders typically look at two DTI ratios: the front-end ratio (housing expenses only) and the back-end ratio (all monthly debt payments, including housing). A common guideline for the back-end DTI is 36%, though some lenders may go up to 43-50% depending on the loan type and other qualifying factors. A lower DTI indicates that you have more disposable income available to manage your mortgage payments, making you a less risky borrower. To lower your DTI, consider paying down existing debts like credit cards, car loans, or student loans before applying for a home loan.

Stable Income and Employment History

Lenders require evidence of a stable and reliable income source to ensure you can consistently make your mortgage payments. This typically means having a consistent employment history for at least two years in the same line of work or industry. While traditional W-2 employment is straightforward, self-employed individuals or those with commission-based income will need to provide more extensive documentation, often including two years of tax returns and profit-and-loss statements. The key is demonstrating a consistent earning pattern that supports the proposed mortgage payments and other living expenses.

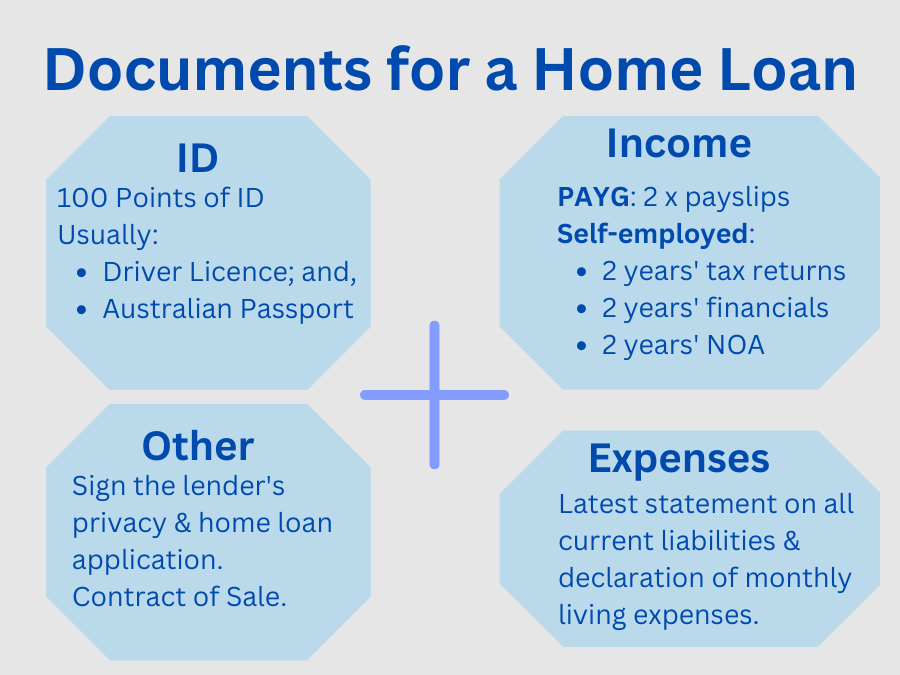

Essential Documentation and Information

Once your financial foundation is in order, gathering the necessary paperwork is the next crucial step. Being organized and having these documents readily available will significantly expedite the application process.

Personal Identification and Financial Statements

You will need to provide government-issued identification, such as a driver’s license or passport, to verify your identity. Additionally, lenders will request bank statements for all accounts (checking, savings, investments) typically for the past 60-90 days, to verify funds for the down payment and closing costs, and to ensure consistent cash flow. They will also look for any large, unexplained deposits that might signal unverified gifted funds or other liabilities.

Proof of Income and Employment

To substantiate your income and employment stability, lenders will require:

- Pay stubs: Typically for the most recent 30 days.

- W-2 forms: For the past two years.

- Tax returns: Complete federal tax returns, usually for the past two years, especially if you’re self-employed, receive commission, or have multiple income sources.

- Employment verification: Lenders will often contact your employer directly to confirm your current employment and salary.

Asset Verification

Beyond the down payment, lenders want to ensure you have sufficient reserves – additional funds available after closing to cover mortgage payments and other expenses in case of an unexpected financial setback. Documentation for all liquid assets, such as savings accounts, checking accounts, investment portfolios, and retirement accounts (like 401(k)s or IRAs), will be required. These statements verify your assets and contribute to a strong financial profile.

Debt Documentation

A comprehensive list of your current debts is essential. This includes statements for credit cards, auto loans, student loans, and any other outstanding liabilities. Lenders use this information to calculate your DTI ratio accurately and assess your overall financial obligations. It’s beneficial to know the balances, minimum monthly payments, and interest rates for all your debts before you apply.

Understanding Loan Types and Lenders

Navigating the various types of home loans and understanding the role of different lenders can be complex, but it’s vital for choosing the right financial product for your situation.

Conventional vs. Government-Backed Loans (FHA, VA, USDA)

- Conventional Loans: These are not insured or guaranteed by the government. They often require good credit scores and can be ideal for borrowers with solid financial histories and larger down payments (though low-down-payment options exist).

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers or those with lower credit scores. They typically require a lower minimum down payment (as low as 3.5%) but come with mandatory mortgage insurance premiums.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are for eligible service members, veterans, and surviving spouses. They offer significant benefits, including no down payment requirements and no private mortgage insurance, often with competitive interest rates.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income individuals purchasing homes in eligible rural areas. They also offer no down payment options.

Each loan type has specific eligibility criteria and advantages, so understanding which one best fits your financial profile is a critical step.

Fixed-Rate vs. Adjustable-Rate Mortgages

- Fixed-Rate Mortgages (FRMs): The interest rate remains constant for the entire loan term (e.g., 15 or 30 years). This provides predictable monthly payments, making budgeting easier and protecting against rising interest rates.

- Adjustable-Rate Mortgages (ARMs): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a market index. ARMs can offer lower initial interest rates but introduce the risk of fluctuating payments in the future.

Your financial stability and future plans should guide your choice between the predictability of a fixed rate and the potential initial savings of an adjustable rate.

The Role of Mortgage Brokers vs. Direct Lenders

- Direct Lenders (Banks, Credit Unions, Online Lenders): These institutions lend their own money directly to borrowers. They have their own specific loan products, underwriting guidelines, and often manage the entire loan process in-house.

- Mortgage Brokers: Act as intermediaries, working with multiple lenders to find the best loan products and rates for their clients. They can be particularly helpful for borrowers with unique financial situations or those who want to compare a wide range of options without applying to multiple institutions directly.

Understanding the difference can help you decide whether to shop around independently or leverage a broker’s expertise to find the optimal financing solution.

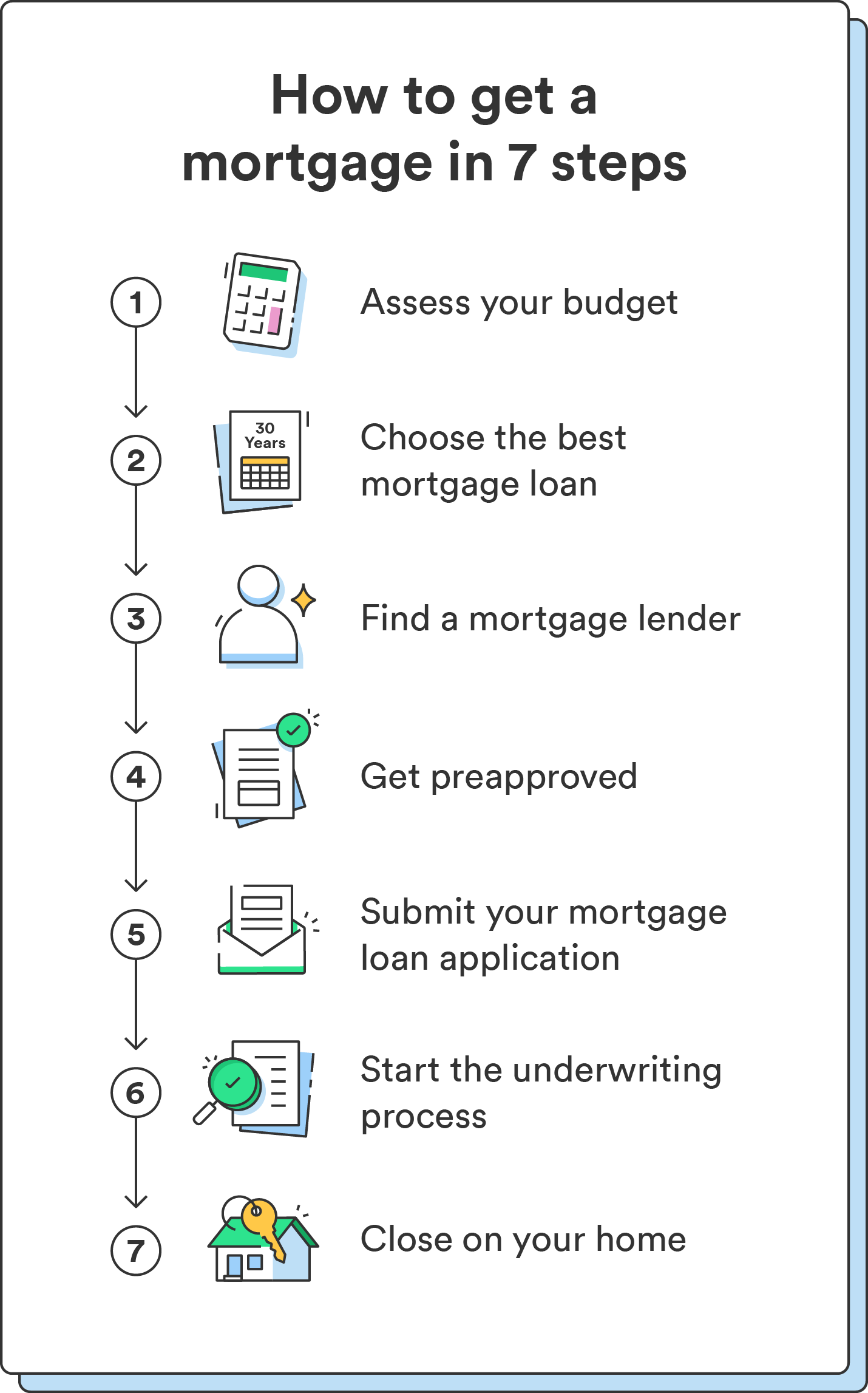

The Application and Approval Process

Once you’ve assembled your documents and understood your loan options, the final stages involve applying for the loan and navigating through underwriting to closing.

Getting Pre-Approved: A Critical First Step

Pre-approval is an official letter from a lender stating how much they are willing to lend you based on a preliminary review of your finances. This involves a hard credit pull and verification of your income and assets. A pre-approval letter demonstrates to sellers that you are a serious and qualified buyer, giving you a competitive edge in a hot housing market. It also helps you understand your budget, preventing you from looking at homes outside your affordable price range.

Loan Application Submission

After pre-approval, once you have an accepted offer on a home, you will formally submit your full loan application. This involves providing all the detailed documentation gathered earlier. The lender will review everything to ensure it aligns with your pre-approval assessment. Be prepared for follow-up questions and requests for additional information throughout this stage.

Underwriting and Appraisal

- Underwriting: This is the most intensive part of the loan approval process. The underwriter meticulously reviews all your financial documents, credit history, and the property details to assess the risk of lending to you. They ensure that your application meets both the lender’s and the specific loan program’s guidelines.

- Appraisal: The lender will order an independent appraisal of the property to determine its fair market value. This ensures that the loan amount is justified by the property’s worth and protects the lender in case of foreclosure. If the appraisal comes in lower than the purchase price, it can impact the loan amount or require renegotiation with the seller.

Closing the Loan: Final Steps and Costs

The closing is the final stage where all parties (buyer, seller, lenders, and attorneys/title company) meet to sign the necessary documents and transfer ownership. You will need to bring certified funds for the remaining down payment and closing costs. Closing costs are various fees associated with processing the loan and transferring the property, typically ranging from 2% to 5% of the loan amount. These can include origination fees, appraisal fees, title insurance, attorney fees, and recording fees. Be prepared for a significant amount of paperwork and ensure you understand every document before signing.

By systematically addressing each of these financial and documentation requirements, you can navigate the home loan process with confidence, ultimately achieving your goal of homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.