Securing a mortgage loan is one of the most significant financial decisions many individuals will make, often representing the largest debt they will incur. Navigating the complex landscape of lenders, interest rates, and loan products requires a strategic, informed approach. Effective shopping for a mortgage can save tens of thousands of dollars over the life of the loan, making it imperative to understand the process, your financial standing, and how to critically evaluate offers.

Laying the Groundwork: Understanding Your Needs and Eligibility

Before embarking on the search for a mortgage, it is crucial to establish a clear understanding of your personal financial situation and the various types of mortgage products available. This foundational knowledge empowers you to make informed decisions and approach lenders with confidence.

Demystifying Mortgage Types

Mortgages are not a one-size-fits-all product. Different loan structures cater to various financial circumstances and risk tolerances:

- Fixed-Rate Mortgages (FRMs): The interest rate remains constant for the entire life of the loan, providing predictable monthly payments. This stability is attractive for those who prefer consistent budgeting and are concerned about rising interest rates. Common terms are 15-year and 30-year fixed-rate mortgages. While a 15-year term typically comes with a lower interest rate, the monthly payments are higher, leading to faster equity buildup and less interest paid over the loan’s life.

- Adjustable-Rate Mortgages (ARMs): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a predetermined index, plus a margin. ARMs can offer lower initial interest rates, making them appealing to buyers who plan to sell or refinance before the fixed period ends, or those who anticipate their income increasing substantially. However, they carry the risk of higher payments if rates rise. Understanding the caps (limits on how much the rate can adjust) is vital.

- Government-Insured Loans:

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers or those with lower credit scores. They often require a lower down payment (as little as 3.5%) but come with mandatory mortgage insurance premiums (MIP) for the life of the loan or until specific conditions are met.

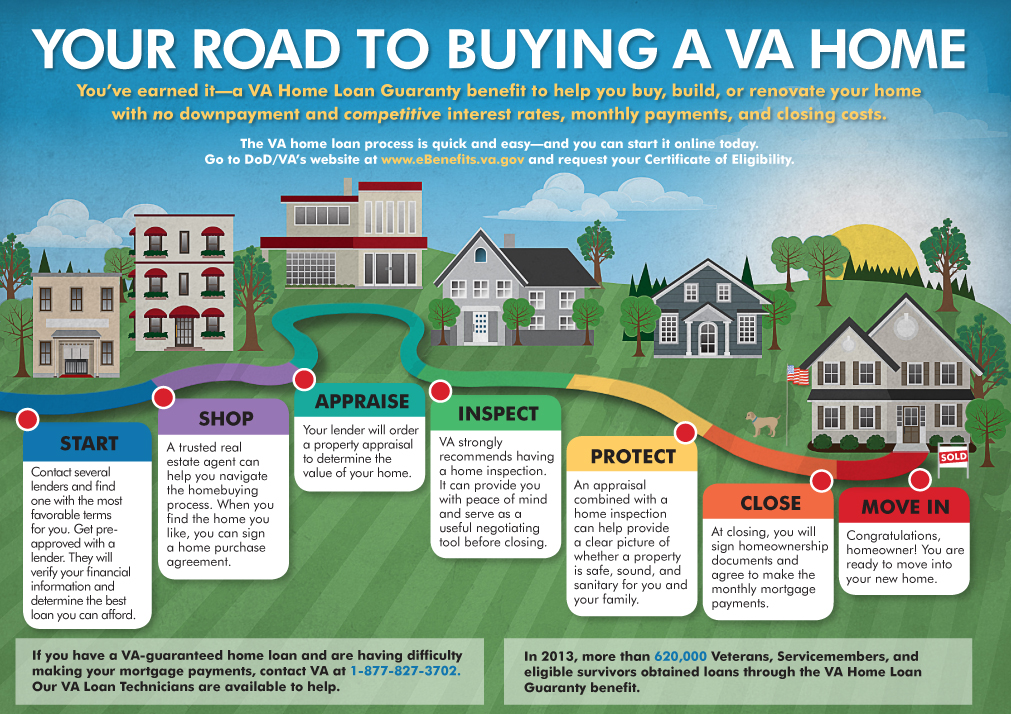

- VA Loans: Guaranteed by the Department of Veterans Affairs, these loans are available to eligible active-duty service members, veterans, and surviving spouses. They typically require no down payment and no private mortgage insurance (PMI), making them incredibly attractive for qualified borrowers. A funding fee usually applies.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are for low-to-moderate-income borrowers purchasing homes in eligible rural areas. They also often require no down payment and offer competitive interest rates.

- Jumbo Loans: For loan amounts exceeding conforming loan limits set by government-sponsored enterprises (Fannie Mae and Freddie Mac), jumbo loans are necessary. They often come with stricter underwriting requirements and may have slightly higher interest rates.

Assessing Your Financial Health

Lenders will scrutinize your financial profile to determine your eligibility and the terms they are willing to offer. A proactive assessment can help you identify areas for improvement. Key factors include:

- Credit Score: Your FICO score (or similar credit scoring model) is paramount. Lenders use it to gauge your creditworthiness and risk. Higher scores (typically 740+) unlock the most favorable interest rates. Review your credit reports from all three major bureaus (Equifax, Experian, Transunion) for accuracy and dispute any errors.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the prospective mortgage payment) to your gross monthly income. Most lenders prefer a DTI ratio of 36% to 43% or lower, though some programs may allow higher. A lower DTI indicates you can comfortably handle additional debt.

- Down Payment: The amount of money you contribute upfront significantly impacts your loan terms. A larger down payment reduces the loan amount, decreases your monthly payments, and can help you avoid private mortgage insurance (PMI) if you put down 20% or more on a conventional loan.

- Employment History and Income Stability: Lenders seek stable income. Expect to provide at least two years of employment history, tax returns, and pay stubs to demonstrate consistent earnings. Self-employed individuals may have more rigorous documentation requirements.

- Savings and Reserves: Having cash reserves beyond your down payment and closing costs demonstrates financial stability and your ability to weather unexpected expenses. LLenders often want to see reserves equivalent to a few months of mortgage payments.

Gathering Your Financial Arsenal: Documentation and Preparation

Once you understand the basics, the next step is to get your financial house in order. This involves proactive measures to strengthen your application and compiling all necessary documentation.

Boosting Your Credit Score

If your credit score isn’t in the excellent range, take steps to improve it before applying:

- Pay all bills on time, every time. Payment history is the most significant factor.

- Reduce outstanding debt, especially on credit cards, to lower your credit utilization ratio (amount of credit used vs. amount available).

- Avoid opening new credit accounts or making large purchases on credit before applying for a mortgage.

- Keep old accounts open, even if unused, as a longer credit history is beneficial.

Assembling Key Financial Documents

Be prepared to provide a comprehensive package of financial documents. Having these readily accessible streamlines the application process:

- Proof of Income: Pay stubs (most recent 30 days), W-2 forms (past two years), federal tax returns (past two years), and if self-employed, 1099s and profit and loss statements.

- Asset Information: Bank statements (past two to three months) for checking, savings, and investment accounts to verify your down payment and reserves.

- Debt Information: Statements for credit cards, auto loans, student loans, and any other outstanding debts.

- Identification: Driver’s license or other government-issued ID, and Social Security card.

- Residential History: Current and previous addresses for the past two years.

Calculating Your Affordability

Utilize online mortgage calculators to estimate potential monthly payments based on different loan amounts, interest rates, and terms. Factor in principal, interest, property taxes, homeowner’s insurance, and potential mortgage insurance (PITI + MI). It’s wise to consider not just what a lender will lend you, but what you can comfortably afford without straining your budget. Account for other homeownership costs like utilities, maintenance, and potential HOA fees.

Exploring the Mortgage Market: Where to Find Lenders

The mortgage market is diverse, offering various avenues to secure financing. Each type of lender has its advantages and disadvantages. It’s prudent to explore multiple options to compare rates, fees, and service.

Traditional Banks and Credit Unions

Large national banks (e.g., Chase, Wells Fargo, Bank of America) and local community banks often have established relationships with their customers and may offer competitive rates or loyalty programs. Credit unions, as non-profit financial institutions, are known for personalized service and potentially lower fees or better rates for their members. They can be a good starting point for comparison, especially if you already have an existing relationship.

Mortgage Brokers: Your Intermediary

A mortgage broker acts as an intermediary, working with multiple lenders to find a loan that fits your needs. They can save you time by shopping around on your behalf and may have access to a wider range of loan products, including niche offerings. Brokers earn a commission from either the borrower (directly or through an origination fee) or the lender, or both. Ensure transparency regarding their compensation structure. A good broker can be invaluable for complex financial situations or if you prefer a single point of contact.

Online Lenders: Speed and Convenience

Companies like Rocket Mortgage (Quicken Loans), Better.com, and Ally Bank operate primarily online, often offering streamlined application processes, competitive rates due to lower overhead, and digital tools for managing your loan. They can be very efficient for tech-savvy borrowers who are comfortable with less face-to-face interaction. However, ensure you still receive personalized attention and clear communication regarding the specifics of your loan.

Government-Backed Loans: FHA, VA, USDA

If you qualify for an FHA, VA, or USDA loan, these government-backed options can be highly advantageous due to lower down payment requirements, more flexible credit criteria, or the absence of PMI. Not all lenders offer all types of government-backed loans, so specify your interest if you believe you qualify. Researching lenders specializing in these programs can yield better results.

Deciphering Offers: Beyond the Interest Rate

When comparing loan offers, looking solely at the interest rate is a common mistake. The true cost of a mortgage involves many factors. A thorough comparison requires attention to all components of the loan.

The True Cost: Understanding APR

The Annual Percentage Rate (APR) is a more comprehensive measure of the cost of borrowing than the interest rate alone. It reflects the interest rate plus certain fees and charges that you pay to get the loan, expressed as a yearly rate. While not perfect (it doesn’t include all closing costs), APR provides a better basis for comparing different loan offers. A lower APR generally indicates a cheaper loan over its lifetime.

Navigating Closing Costs and Fees

Closing costs are the expenses incurred in the loan process, typically ranging from 2% to 5% of the loan amount. These can include:

- Lender Fees: Origination fees (a percentage of the loan amount for processing), underwriting fees, application fees.

- Third-Party Fees: Appraisal fees, credit report fees, title insurance fees, escrow fees, attorney fees, recording fees.

- Prepaid Items: Property taxes and homeowner’s insurance premiums that are paid in advance.

Ask each lender for a detailed Loan Estimate (LE). This standardized form allows for easy comparison of interest rates, monthly payments, and closing costs across different lenders. Pay close attention to the “Cash to Close” section and any credits you might receive. Understand what fees are negotiable (e.g., origination fees) versus those that are not (e.g., appraisal fees).

Lock-In Periods and Rate Fluctuations

A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan is being processed. This protects you if market rates rise during this time. Understand the length of the lock and any fees associated with extending it. If rates are volatile, a longer lock might be worth a slightly higher fee or rate. Conversely, if rates are falling, you might prefer a shorter lock or even a “float-down” option, if available, which allows you to secure a lower rate if they drop before closing.

Understanding Escrow and Property Taxes

Many mortgages require an escrow account for property taxes and homeowner’s insurance. This means a portion of your monthly payment goes into this account, and the lender pays these bills on your behalf when they are due. While convenient, it adds to your monthly payment, and the amount can adjust annually based on changes in taxes or insurance premiums. Understand how these are calculated and managed.

Making Your Choice and Moving Forward

After comparing multiple offers and understanding all the associated costs, it’s time to make a decision and proceed with the application.

The Pre-Approval Advantage

Obtaining a mortgage pre-approval is highly recommended before seriously house hunting. A pre-approval letter from a lender states the maximum loan amount you qualify for, based on a review of your financial information and a hard credit pull. This demonstrates to sellers that you are a serious and qualified buyer, giving you a competitive edge in a hot market. It also clarifies your budget, preventing you from looking at homes outside your financial reach. Note that pre-qualification is a less rigorous estimate and not as strong as pre-approval.

Finalizing Your Decision

Review the Loan Estimates from at least three different lenders side-by-side. Compare the APRs, total closing costs, and monthly payments. Consider not only the numbers but also the lender’s responsiveness, reputation, and the clarity of their communication. A lender that provides clear answers and excellent customer service throughout the process can be invaluable. Don’t be afraid to leverage one offer to negotiate better terms with another lender.

What to Expect at Closing

The closing is the final step where you sign all the necessary documents and the loan is funded. Before closing, you will receive a Closing Disclosure (CD) at least three business days prior to the closing date. This document provides the final terms of your loan and a breakdown of all closing costs. Compare it carefully against your last Loan Estimate to ensure there are no unexpected changes. Be prepared for a significant amount of paperwork and don’t hesitate to ask questions if anything is unclear. Bring your government-issued ID and the required funds for your down payment and closing costs, typically in the form of a cashier’s check or wire transfer.

Shopping for a mortgage loan is a detailed process that demands diligence and a critical eye for financial particulars. By understanding the different loan types, preparing your finances, exploring various lenders, and meticulously comparing offers, you can secure the most favorable terms, ultimately leading to significant savings over the life of your home loan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.