Securing a home loan is a pivotal step in the homeownership journey, representing a significant financial commitment. Navigating the complex landscape of lenders, loan types, and financial requirements can be daunting, but a strategic approach focused on personal financial readiness and thorough comparison can lead to the best possible terms. This guide breaks down the essential steps and considerations for finding a home loan that aligns with your financial goals.

Understanding Your Financial Readiness

Before even speaking to a lender, a thorough assessment of your financial health is paramount. Lenders evaluate several key financial metrics to determine your eligibility and the interest rate they can offer.

Assess Your Credit Score

Your credit score is a numerical representation of your creditworthiness, largely influencing the interest rate you’ll receive. Lenders typically look for FICO scores above 620 for conventional loans, with higher scores (740+) often qualifying for the most favorable rates. A strong credit history demonstrates your reliability in managing debt. Pull your credit reports from all three major bureaus (Experian, Equifax, TransUnion) annually via AnnualCreditReport.com to check for errors and understand your standing. Pay down existing debts, avoid opening new lines of credit, and make all payments on time to improve your score.

Evaluate Your Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including the prospective mortgage payment, credit card minimums, car loans, student loans, etc.) by your gross monthly income. Most lenders prefer a DTI ratio of 36% or less, though some programs may allow up to 43% or even 50% under certain circumstances. A lower DTI indicates less financial strain and a greater capacity to handle a mortgage.

Determine Your Down Payment

The down payment is the initial sum you pay towards the home’s purchase price. While a 20% down payment has traditionally been the benchmark for conventional loans to avoid Private Mortgage Insurance (PMI), many loan programs today allow for much lower down payments, some as little as 3% or even 0% for qualified borrowers (e.g., VA and USDA loans). The amount you can comfortably put down will affect your monthly mortgage payment, the total interest paid over the life of the loan, and potentially your interest rate. Carefully consider your savings and weigh the benefits of a larger down payment against keeping an emergency fund readily available.

Calculate Your Affordability

Beyond the down payment, understanding your monthly budget for housing costs is crucial. This includes not just the principal and interest (P&I) of the loan, but also property taxes, homeowner’s insurance, and potentially Private Mortgage Insurance (PMI) or homeowner’s association (HOA) fees. These combined costs are often referred to as PITI (Principal, Interest, Taxes, Insurance). Use online mortgage calculators to estimate these expenses, and compare them against your monthly income and overall budget to determine a comfortable and sustainable payment. Don’t forget to factor in potential closing costs, which can range from 2% to 5% of the loan amount.

Exploring Different Home Loan Types

The mortgage market offers a variety of loan products, each designed to meet different financial situations and borrower needs. Understanding these options is key to selecting the most suitable loan.

Conventional Loans

Conventional loans are not insured or guaranteed by a government agency. They adhere to lending guidelines set by Fannie Mae and Freddie Mac. These loans typically require good to excellent credit, and while a 20% down payment is ideal to avoid PMI, some conventional loans allow for as little as 3% down. They offer competitive interest rates for borrowers with strong financial profiles and often have more flexible terms once PMI is paid off or removed.

Government-Backed Loans

These loans are insured or guaranteed by federal agencies, making them accessible to a broader range of borrowers, particularly those who might not qualify for conventional loans.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are popular with first-time homebuyers and those with lower credit scores (as low as 580 with 3.5% down). They require an upfront mortgage insurance premium and annual premiums for the life of the loan or a significant portion of it.

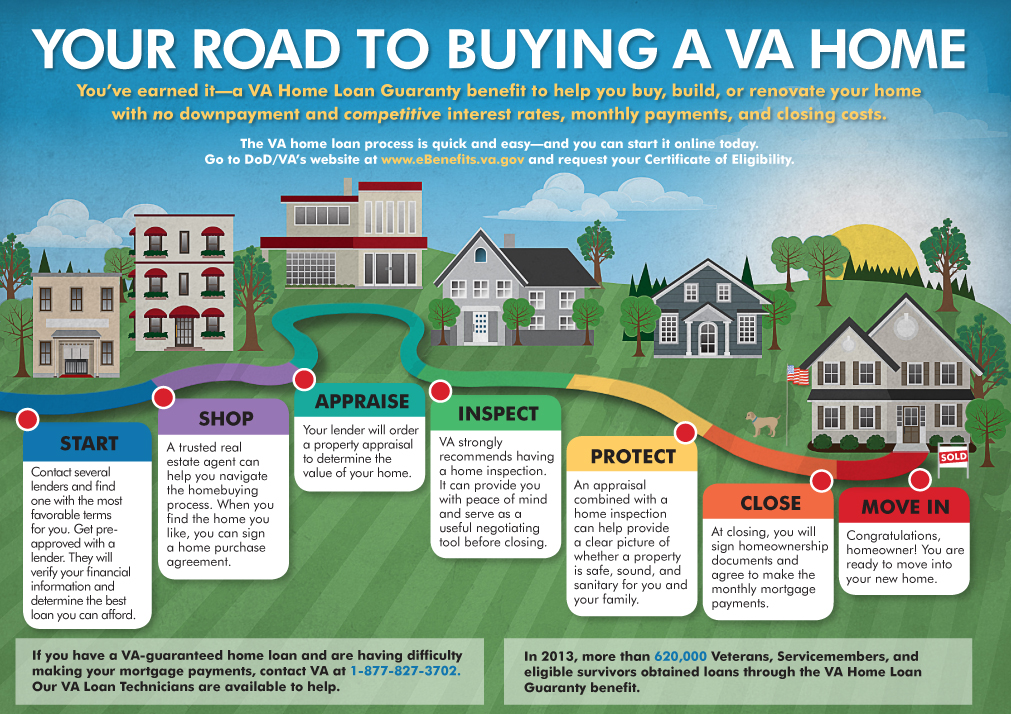

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are available to eligible service members, veterans, and surviving spouses. VA loans often feature no down payment requirements, no private mortgage insurance, and competitive interest rates, making them a powerful benefit for those who have served.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income individuals purchasing homes in designated rural areas. They also typically offer 0% down payment options and reduced mortgage insurance premiums.

Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages

- Fixed-Rate Mortgages: The interest rate remains constant for the entire life of the loan, providing predictable monthly payments. This stability is ideal for long-term homeowners who prefer financial certainty. Common terms are 15, 20, or 30 years.

- Adjustable-Rate Mortgages (ARMs): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a benchmark index, plus a margin. ARMs often start with lower interest rates than fixed-rate mortgages, making them attractive for borrowers who plan to sell or refinance before the fixed period ends, or who anticipate their income increasing substantially. However, there’s a risk of significantly higher payments if interest rates rise.

Jumbo Loans

Jumbo loans are conventional loans that exceed the conforming loan limits set by Fannie Mae and Freddie Mac. These are for high-value properties and typically require higher credit scores, larger down payments, and more substantial financial reserves due to their increased risk for lenders.

Navigating the Lender Landscape

Once you understand your financial position and the types of loans available, the next step is to explore potential lenders. The market offers diverse options, each with its own advantages.

Banks and Credit Unions

Traditional banks and credit unions are often the first stop for many borrowers.

- Banks: Large national banks offer a wide array of loan products and may provide incentives for existing customers. They have established processes and offer in-person service.

- Credit Unions: Member-owned financial cooperatives, credit unions often offer competitive rates and lower fees due to their non-profit structure. They are known for personalized service and may be more flexible with borrowers who have less-than-perfect credit but strong membership ties.

Online Lenders

The digital age has brought forth a wave of online lenders that streamline the application process. These lenders often boast competitive interest rates, lower overhead costs, and quick pre-approvals. Their convenience and efficiency can be appealing, but it’s crucial to ensure they offer sufficient customer support and transparency regarding fees.

Mortgage Brokers

A mortgage broker acts as an intermediary between you and various lenders. They don’t lend money themselves but work with multiple lenders to find you the best loan product and rates based on your financial profile. Brokers can save you time by shopping around on your behalf and can be particularly helpful for borrowers with unique financial situations, but they typically charge a fee, either directly or through the lender.

Direct Lenders

This category primarily includes banks, credit unions, and dedicated mortgage companies. The distinction is that you are applying directly to the institution that will fund and service your loan, or sell it to a servicer. This can sometimes lead to a more straightforward process than working through a broker.

The Application and Comparison Process

Finding the right loan involves more than just selecting a lender; it requires a diligent application and comparison process.

Get Pre-Approved, Not Just Pre-Qualified

While pre-qualification offers a basic estimate of what you might afford, pre-approval is a more rigorous process. A lender reviews your financial documents (credit report, income, assets) and commits to lending you a specific amount, subject to a property appraisal. Pre-approval makes your offer more attractive to sellers and helps you narrow down your home search to an affordable range.

Gather Necessary Documentation

Be prepared to provide a comprehensive financial picture. This typically includes:

- Two years of tax returns

- Two years of W-2 forms or 1099s if self-employed

- Recent pay stubs (typically 30 days)

- Bank statements (checking and savings, typically 60 days)

- Statements for retirement accounts, investment accounts, and other assets

- Identification (driver’s license, Social Security card)

- Proof of residency

Having these documents organized and ready can significantly speed up the application process.

Compare Loan Offers Diligently

Do not settle for the first loan offer. Apply with at least three to five different lenders to compare terms. While the interest rate is a critical factor, it’s not the only one.

- Annual Percentage Rate (APR): The APR reflects the total cost of the loan, including the interest rate and most closing costs and fees, expressed as an annual percentage. This provides a more accurate apples-to-apples comparison between different loan products.

- Closing Costs: These are fees paid at the close of the loan, covering services like appraisal, title insurance, origination fees, and attorney fees. They can add thousands to your upfront expenses.

- Points: Discount points are upfront fees paid to the lender in exchange for a lower interest rate. One point equals 1% of the loan amount. Evaluate whether paying points makes financial sense for your expected homeownership duration.

Understand the Loan Estimate

Once you apply for a mortgage, lenders are required to provide a Loan Estimate form within three business days. This standardized document clearly outlines the estimated interest rate, monthly payment, and total closing costs. Review it carefully, comparing line by line across different lenders to identify discrepancies and hidden fees.

Lock in Your Interest Rate

After getting pre-approved and comparing offers, you’ll want to “lock in” your interest rate. This guarantees your rate for a specific period (typically 30 to 60 days), protecting you from market fluctuations while your loan processes. Discuss the terms of the rate lock with your lender, including any fees associated with extending it if the closing takes longer than anticipated.

Avoiding Common Pitfalls and Optimizing Your Loan

Even after securing a loan, a few critical considerations can safeguard your financial health and optimize your mortgage.

Don’t Apply for New Credit Before Closing

A common mistake borrowers make is applying for new credit cards, car loans, or making large purchases on credit between pre-approval and closing. Any new credit inquiries or increased debt can significantly impact your credit score and DTI, potentially jeopardizing your loan approval or causing the lender to re-evaluate your terms. Maintain your financial status quo.

Ask About Escrow Accounts

Many lenders require or offer an escrow account for property taxes and homeowner’s insurance premiums. With an escrow account, a portion of these costs is added to your monthly mortgage payment, and the lender pays these bills on your behalf when they’re due. This simplifies budgeting and ensures these critical payments are made on time, preventing potential lapses in coverage or tax penalties.

Read the Fine Print

Before signing any documents, meticulously read all terms and conditions of your loan agreement. Understand every fee, clause, and contingency. If anything is unclear, ask your lender for clarification. This vigilance protects you from unexpected costs or unfavorable terms down the line.

Consider Refinancing Options Later

Your initial home loan isn’t necessarily a lifelong commitment. Market interest rates fluctuate, and your financial situation may change. Keep an eye on market trends, as refinancing your mortgage in the future could allow you to secure a lower interest rate, reduce your monthly payments, or even change your loan term, potentially saving you tens of thousands of dollars over the life of the loan.

Finding the right home loan is a meticulous process that demands financial diligence and informed decision-making. By understanding your readiness, exploring available options, comparing offers carefully, and avoiding common pitfalls, you can secure a mortgage that supports your financial well-being and opens the door to homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.