Managing your personal finances effectively often involves making strategic decisions about your banking relationships. Whether driven by a desire for better services, lower fees, relocation, or simply consolidating accounts, closing a bank account is a financial transaction that demands a structured and thoughtful approach. While the convenience of online banking might suggest an entirely digital closure process, the reality for institutions like Wells Fargo often involves a blend of online preparation and direct communication for security and compliance.

This guide provides a professional and insightful roadmap, detailing the crucial financial steps and considerations required to close your Wells Fargo account smoothly, minimizing potential pitfalls and ensuring your financial continuity remains uninterrupted. We’ll navigate the preparatory stages, illuminate the typical closure process, and empower you with the knowledge to manage this financial transition with confidence.

The Financial Implications of Account Closure

Closing a bank account is more than just stopping a service; it’s a significant financial decision that can impact your direct deposits, automatic payments, and overall financial ecosystem. Rushing this process without proper preparation can lead to missed payments, overdraft fees, or complications with your income streams.

Assessing Your Financial Readiness

Before you initiate any steps towards closing your Wells Fargo account, it’s paramount to assess your financial readiness and understand the ripple effects. The primary consideration is ensuring you have an alternative banking solution firmly in place. This means opening and activating a new account with another financial institution before you even consider closing your current one. Having a fully operational new account allows for seamless redirection of funds and transactions, preventing any financial limbo.

Consider the potential impact on your daily financial life. Are there any pending checks or transactions that have yet to clear? What about any recurring transfers you might have set up? A thorough review of your transaction history over the past few months will help identify all such linkages. Furthermore, be aware of any minimum balance requirements your Wells Fargo account might have. Closing an account below a certain threshold or with pending fees could result in unexpected charges, which must be resolved before a full closure can be processed. Understanding these financial interdependencies is the first critical step in ensuring a smooth transition.

Safeguarding Your Funds and Financial Records

A primary objective during account closure is to ensure all your funds are safely transferred and that you retain access to essential financial records. Once an account is closed, accessing past statements or transaction details can become significantly more complicated, or even impossible, depending on the bank’s policies. Therefore, before closing, meticulously transfer all remaining funds to your new account. This process often involves initiating an ACH transfer, a wire transfer, or, for smaller amounts, a direct withdrawal or requesting a cashier’s check for the remaining balance.

Equally important is the diligent collection of your financial history. Download and save all bank statements, tax documents (like 1099-INT forms), and transaction histories for at least the past five to seven years. These records are vital for tax purposes, proof of payment, loan applications, and general personal financial management. Banks generally provide online access to digital statements for a limited period, so proactive downloading is crucial. Neglecting this step could lead to significant administrative hurdles down the line, especially when dealing with audits or disputes. Remember, proper financial record-keeping is a cornerstone of sound personal finance.

Essential Preparatory Steps Before Initiating Closure

The key to a hassle-free account closure lies in thorough preparation. This involves meticulously updating all recurring financial activities linked to your Wells Fargo account and ensuring a clean slate before formally requesting closure.

Redirecting Direct Deposits and Automatic Payments

The single most critical preparatory step is redirecting all incoming direct deposits and outgoing automatic payments. This requires a comprehensive audit of your financial life. Start by identifying all sources of income that feed into your Wells Fargo account, such as your salary, government benefits (Social Security, unemployment), or pension payments. Contact your employer’s HR or payroll department, or the relevant government agency, to update your direct deposit information to your new bank account. This typically involves submitting a new direct deposit form, often found within your new bank’s online portal.

Next, compile a list of all automatic payments, bill pay setups, and recurring subscriptions linked to your Wells Fargo account. This includes utilities (electricity, gas, water), internet and phone bills, loan payments (mortgage, auto, student), insurance premiums, credit card payments, streaming services (Netflix, Spotify), gym memberships, and any other automated debits. For each, contact the service provider or log into their online portal to update your payment method to your new bank account or debit card. Create a checklist and meticulously tick off each item. Allow ample time for these changes to take effect, ideally running both accounts concurrently for a billing cycle or two to catch any forgotten links. This parallel operation provides a safety net against missed payments and associated late fees, ensuring your financial obligations continue without interruption.

Transferring Remaining Funds and Zeroing Out the Account

Once all recurring transactions have been successfully redirected, the next step is to consolidate and transfer the remaining balance out of your Wells Fargo account. It’s advisable to leave a small buffer amount in the account initially (e.g., $50-$100) to cover any unforeseen pending transactions or minor fees that might emerge after you believe you’ve transferred everything. This buffer can prevent the account from going into overdraft and incurring fees, which must be settled before closure.

After a week or two, once you are confident all transactions have cleared and no new debits are expected, you can proceed to transfer the final remaining balance to your new bank account. The most common and cost-effective method for this is an ACH transfer, which can usually be initiated through your new bank’s online banking platform or sometimes from Wells Fargo’s platform itself. For larger sums or urgent transfers, a wire transfer is an option, though it typically incurs a fee. Alternatively, you can withdraw the remaining cash or request a cashier’s check for the balance from a Wells Fargo branch. The goal is to bring the account balance to zero. Be aware that if your account has a negative balance or any outstanding fees, these must be paid in full before Wells Fargo will process the closure request. A zero balance is a prerequisite for a clean closing.

Retrieving Necessary Financial Documents

Before the account is officially closed and access is potentially revoked, it is crucial to download and secure all necessary financial documents. These documents are vital for tax preparation, demonstrating proof of income or payments, and maintaining comprehensive personal financial records. Online banking platforms typically offer access to digital statements, transaction histories, and various tax forms (such as Form 1099-INT for interest earned) for a specific period.

Log into your Wells Fargo online account and navigate to the statements or document section. Download monthly statements for at least the past year, and ideally, up to seven years if available. Also, download any relevant tax documents. Save these files to a secure location on your computer, a cloud storage service, and ideally, a backup external drive. Some individuals prefer printing hard copies for their physical filing system. While Wells Fargo, like other banks, is required to retain certain records for regulatory purposes, accessing these post-closure can involve formal requests, potential fees, and significant delays. Proactive downloading ensures you have immediate and permanent access to your financial history, preventing future administrative headaches and supporting sound financial management practices.

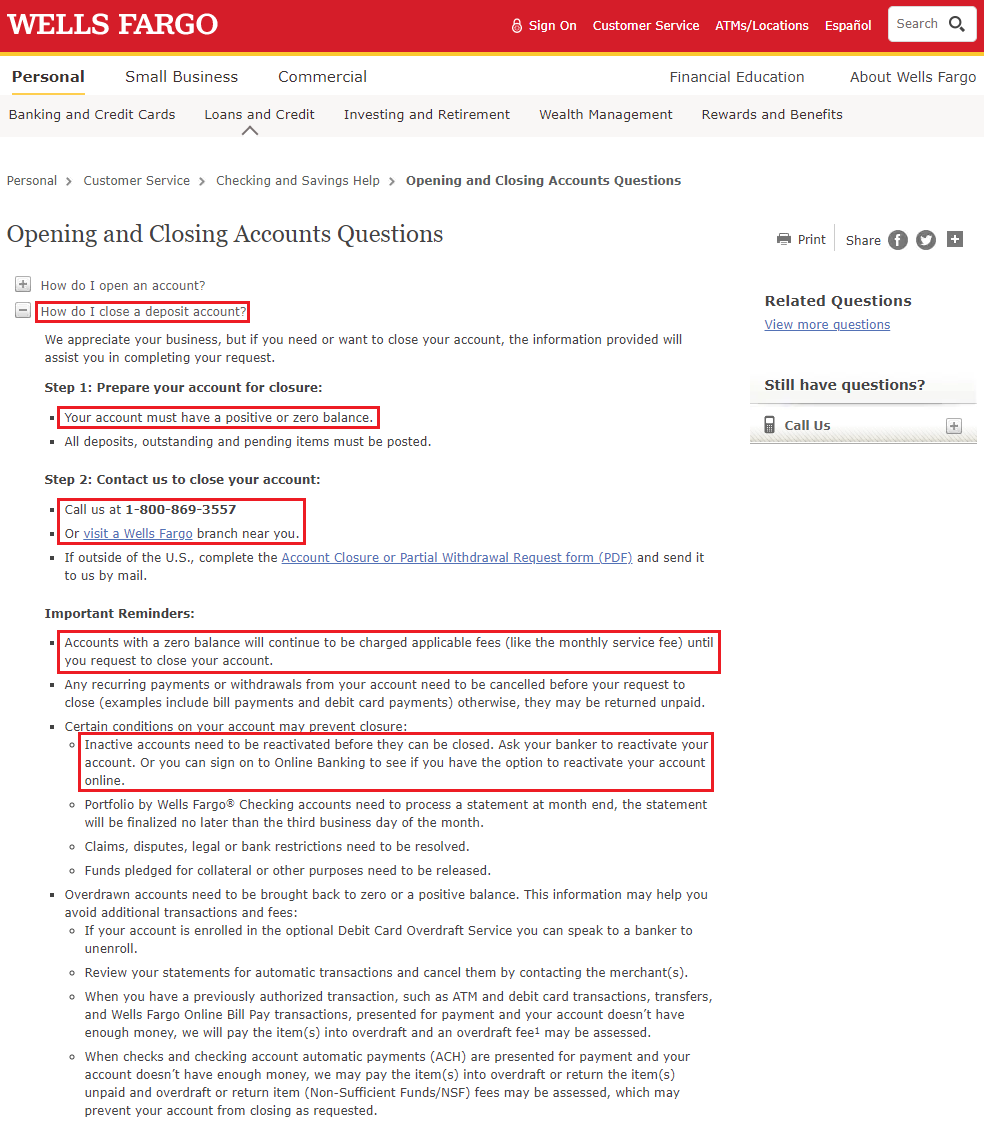

Navigating Wells Fargo’s Account Closure Process

While the convenience of modern banking suggests a purely “online” closure, financial institutions often implement specific protocols for account termination due to security and regulatory compliance. For Wells Fargo, initiating contact online is a viable first step, but the finalization typically requires direct communication.

Exploring Online and Alternative Closure Methods

It’s important to clarify that fully closing a Wells Fargo account with a single click entirely online is generally not an option for security and verification purposes. Most banks, including Wells Fargo, require a more robust verification process than a simple online form submission to protect against fraudulent account closures. However, you can use Wells Fargo’s online platform to prepare for closure and initiate the process.

You can often send a secure message through your Wells Fargo online banking portal expressing your intent to close the account and requesting instructions. This allows you to formally begin the communication while maintaining a digital record. Alternatively, you can search Wells Fargo’s website for specific instructions on account closure, which might outline the necessary forms or contact information.

The most common methods for formal closure typically involve:

- Phone Call: Calling Wells Fargo’s customer service number is often the quickest way to speak with a representative who can guide you through the process, verify your identity, and confirm your account balance.

- In-Person Visit: Visiting a Wells Fargo branch allows for face-to-face interaction, providing an opportunity to resolve any immediate issues, verify your identity with a valid ID, and obtain immediate confirmation of the closure request.

- Written Request: For those who prefer a paper trail or cannot visit a branch, sending a certified letter to Wells Fargo, including your account number and a clear request for closure, is another option. This method provides documented proof of your request.

While the preliminary steps of transferring funds and updating direct deposits are done online, the final act of closing usually requires a direct interaction to ensure proper verification and avoid errors.

What to Expect During the Closure Conversation/Process

When you contact Wells Fargo to close your account, be prepared for a structured conversation designed to ensure security and compliance. The representative will first meticulously verify your identity using several pieces of personal information to protect against fraud. This is a critical step and a standard banking practice.

Next, they will confirm that your account balance is zero and inquire about any pending transactions that might still clear. If there are any outstanding fees or a negative balance, you will be required to settle these before the closure can proceed. It’s not uncommon for banks to offer incentives or ask about your reasons for leaving, attempting to retain your business. While you are free to listen, remember your objective and stick to your decision if you’re certain.

Crucially, request written confirmation of the account closure. This could be an email, a letter mailed to your address, or a physical document if you’re closing in person. This confirmation serves as vital proof that the account has been officially terminated, which is essential for your records and for resolving any potential future discrepancies. Ensure the confirmation includes the date of closure and explicitly states that the account is closed and has a zero balance.

Post-Closure Verifications and Follow-Up

The process doesn’t end immediately after you’ve made the closure request. Diligent follow-up is a key component of sound financial management. Over the next few weeks, closely monitor your new bank account to ensure all previously redirected direct deposits and automatic payments are indeed flowing correctly. Any hiccups here could indicate a missed update or a delay in processing by a third party.

Additionally, keep an eye on your mail for the written confirmation of closure from Wells Fargo. If you don’t receive it within the promised timeframe, follow up with customer service. It’s also wise to occasionally check your online access to the Wells Fargo account (if it remains active for a short period after closure) to ensure it truly reflects a closed status, though typically access is revoked once fully closed.

If you had any debit cards or checks associated with the closed account, securely destroy them by shredding them. This prevents unauthorized use and protects your personal financial information. While the account is closed, the physical instruments can still pose a security risk. This final set of verifications ensures a complete and secure detachment from your old account and a smooth transition to your new banking arrangements.

Common Pitfalls and Best Practices for a Smooth Transition

Closing a bank account, while seemingly straightforward, can be fraught with minor complexities that, if overlooked, can lead to financial inconvenience or unexpected costs. Understanding these pitfalls and adopting best practices will ensure a seamless transition.

Avoiding Fees and Delays

One of the most common pitfalls when closing an account is incurring unexpected fees. These can stem from attempting to close an account with a negative balance, failing to meet minimum balance requirements before closure (triggering a fee), or having an overdraft occur from a lingering automatic payment that hasn’t been fully redirected. To avoid these:

- Ensure Zero Balance: Meticulously confirm all funds are transferred out and any outstanding fees or charges are paid. Leave a small buffer initially to catch unexpected debits.

- Update All Transactions Early: Begin redirecting direct deposits and automatic payments weeks, if not months, in advance of your target closure date. This provides a buffer for processing times and allows you to identify any forgotten links.

- Understand Bank Policies: Familiarize yourself with Wells Fargo’s specific account closure policies, including any potential fees for early closure (though rare for checking/savings), or requirements for a specific closure method.

Delays can also arise if identity verification is incomplete or if there’s a discrepancy in your account information. Double-check that your personal details are up-to-date with Wells Fargo before initiating the closure request.

Data Security and Privacy Considerations

When an account is closed, your personal financial data doesn’t simply vanish. Banks are legally obligated to retain certain records for several years for regulatory and audit purposes. However, it’s crucial to understand what happens to your data and to take proactive steps to protect your privacy.

- Review Privacy Policies: Read Wells Fargo’s privacy policy regarding closed accounts to understand how long they retain data and for what purposes. While you can’t entirely erase historical data, knowing the policy provides clarity.

- Delete Saved Login Info: Remove any saved login credentials for your Wells Fargo account from your web browsers, password managers, or banking apps on your devices. This minimizes any potential for unauthorized access, even to a closed account’s residual information.

- Securely Destroy Physical Items: As mentioned, shred all associated debit cards, ATM cards, and unused checks. These physical items contain sensitive account information that could be misused if they fall into the wrong hands.

- Monitor Credit Reports: After a few months, consider pulling your free annual credit report to ensure that the account is properly reported as closed (if it was a credit account or if associated with other credit products). This helps verify that your financial footprint is accurately updated.

By addressing these data security and privacy aspects, you safeguard yourself against potential future risks and maintain control over your personal financial information even after your banking relationship has concluded.

Conclusion

Closing a Wells Fargo account, while conceptually simple, requires a structured and deliberate approach within the realm of personal finance. While the initial thought of “how to close Wells Fargo account online” might evoke a fully digital, one-click solution, the reality is a nuanced process demanding meticulous preparation and direct communication for security and compliance.

By carefully assessing your financial readiness, safeguarding your funds and records, diligently redirecting all recurring transactions, and understanding the bank’s specific closure protocols, you can navigate this transition smoothly. The key lies in proactive planning, confirming every detail, and securing written proof of closure. This comprehensive, step-by-step financial management ensures not only that your old account is closed efficiently but also that your financial continuity remains robust, empowering you to maintain precise control over your personal finances. Taking these thoughtful steps transforms a potentially complex task into a clear, manageable process, aligning perfectly with sound personal financial practices.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.