Securing your financial future is one of the most critical endeavors you’ll undertake, and for many, an Individual Retirement Account (IRA) serves as a cornerstone of that plan. Whether you’re just starting your career, navigating mid-life financial shifts, or nearing retirement, understanding how to set up an IRA is an essential step towards building a robust savings strategy. An IRA is more than just a savings account; it’s a powerful, tax-advantaged investment vehicle designed to help you accumulate wealth specifically for your retirement years. It provides a level of flexibility and control often not found in employer-sponsored plans, making it an invaluable tool for nearly everyone.

This comprehensive guide will walk you through the process of establishing an IRA, from understanding the different types available to selecting the right financial institution and making informed investment choices. Our aim is to demystify the process, providing you with the knowledge and confidence to take control of your retirement savings journey. By the end, you’ll have a clear roadmap for setting up and maximizing your IRA, paving the way for a more secure and comfortable retirement.

Understanding the IRA Landscape: Types and Benefits

Before you can set up an IRA, it’s crucial to understand the various types available and the distinct advantages each offers. The choice often depends on your current income level, tax bracket, and long-term financial goals. Each IRA type comes with its own set of rules regarding contributions, tax deductions, and withdrawals, making it vital to select the one that best aligns with your personal circumstances.

Traditional IRA: The Tax-Deductible Powerhouse

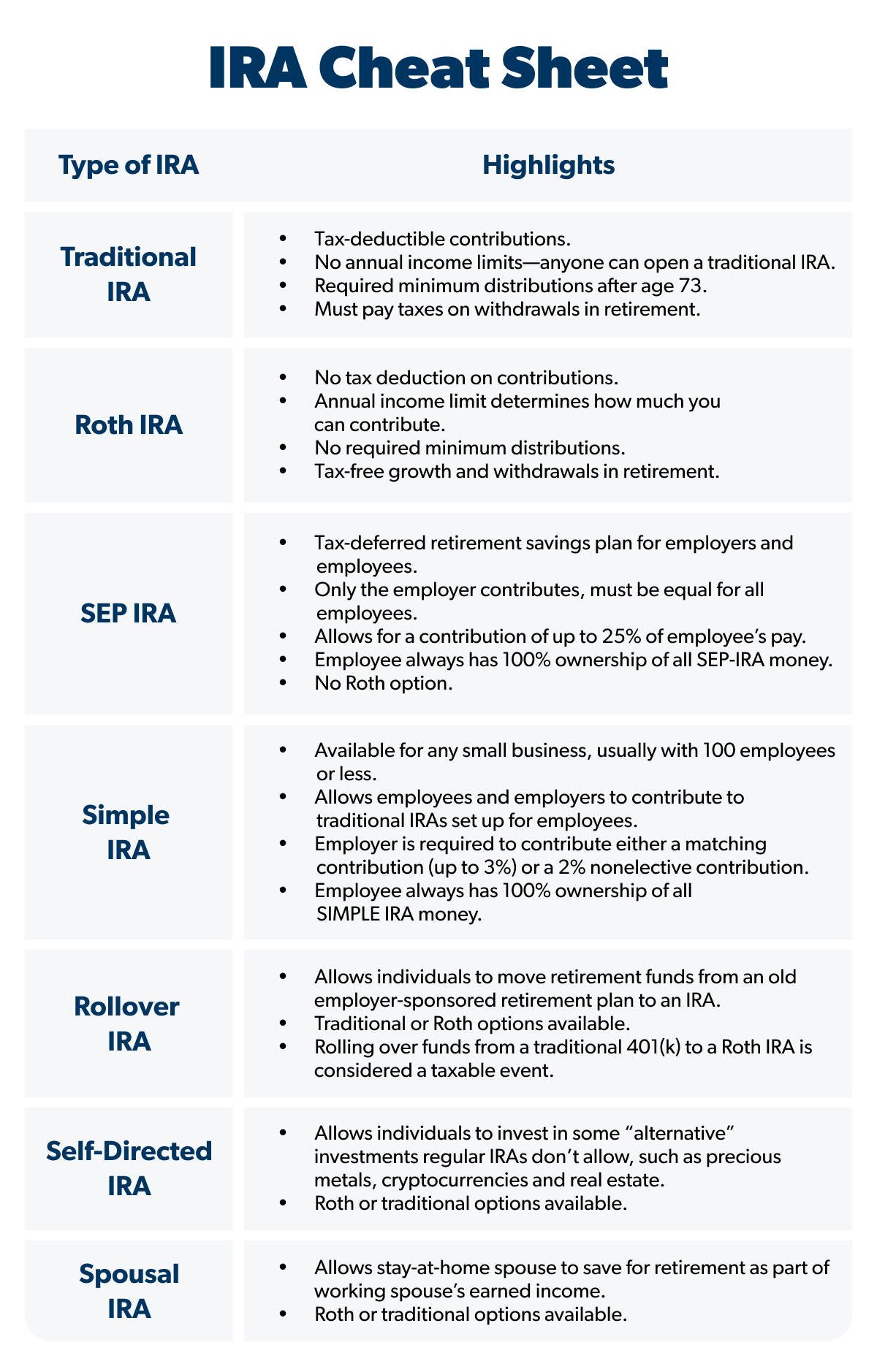

A Traditional IRA is perhaps the most widely recognized type, primarily favored for its immediate tax benefits. Contributions to a Traditional IRA are often tax-deductible in the year they are made, meaning they can lower your taxable income for that year. This makes it an attractive option for individuals looking to reduce their current tax burden. The money within the account then grows tax-deferred, meaning you don’t pay taxes on investment gains until you withdraw the funds in retirement.

There are annual contribution limits set by the IRS, which typically increase periodically. For instance, in 2024, the contribution limit for individuals under 50 is $7,000, with an additional catch-up contribution of $1,000 allowed for those aged 50 and over. While contributions might be tax-deductible, there can be income limitations if you or your spouse are covered by a retirement plan at work. Withdrawals in retirement, typically after age 59½, are taxed as ordinary income. You must also begin taking Required Minimum Distributions (RMDs) once you reach a certain age, currently 73, to prevent indefinite tax deferral.

Roth IRA: Tax-Free Withdrawals in Retirement

The Roth IRA stands in contrast to the Traditional IRA, offering a different but equally compelling tax advantage: tax-free withdrawals in retirement. Contributions to a Roth IRA are made with after-tax dollars, meaning you don’t get an upfront tax deduction. However, once your money is in a Roth IRA, it grows tax-free, and qualified withdrawals in retirement are completely tax-free. This makes it an excellent choice for individuals who anticipate being in a higher tax bracket in retirement than they are today, or for younger investors who have many decades of tax-free growth ahead.

Like Traditional IRAs, Roth IRAs have annual contribution limits (e.g., $7,000 in 2024, with a $1,000 catch-up for those 50 and over). However, Roth IRAs have income limitations for direct contributions. If your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds, you may be unable to contribute directly to a Roth IRA. In such cases, a “backdoor Roth” strategy, involving contributing to a Traditional IRA and then converting it to a Roth, can be an option, though it requires careful consideration of tax implications. To qualify for tax-free withdrawals, the account must be open for at least five years, and you must be at least 59½ years old, or meet other specific criteria (e.g., disability, first-time home purchase up to $10,000).

SEP IRA and SIMPLE IRA: Options for the Self-Employed and Small Businesses

Beyond the Traditional and Roth IRAs, there are specialized options designed for self-employed individuals and small business owners. A Simplified Employee Pension (SEP) IRA allows employers (including self-employed individuals) to contribute to their employees’ (and their own) retirement accounts. These contributions are tax-deductible for the employer, and growth is tax-deferred for the employee. SEP IRAs boast much higher contribution limits than Traditional or Roth IRAs, making them powerful tools for high-income self-employed individuals.

The Savings Incentive Match Plan for Employees (SIMPLE) IRA is another option for small businesses (typically with 100 or fewer employees) that don’t offer another retirement plan. It allows both employee and employer contributions, with the employer typically required to make either a matching contribution or a non-elective contribution. SIMPLE IRAs have lower administrative costs and fewer compliance requirements than plans like 401(k)s, but also lower contribution limits than SEP IRAs.

Key Benefits of an IRA

Regardless of the type you choose, IRAs offer several overarching benefits that make them indispensable for retirement planning:

- Tax Advantages: Whether it’s upfront tax deductions (Traditional), tax-deferred growth (Traditional), or tax-free withdrawals (Roth), IRAs provide significant tax benefits that allow your money to grow more efficiently than in a taxable brokerage account.

- Compounding Growth: The power of compound interest is amplified within an IRA, as your earnings generate further earnings, and the tax benefits ensure that more of your money stays invested and grows over time.

- Accessibility and Control: Unlike some employer-sponsored plans, you typically have full control over your investment choices within an IRA. You also have the flexibility to open an IRA even if you change jobs or are self-employed.

- Catch-Up Contributions: For those nearing retirement, the ability to make additional catch-up contributions after age 50 provides an invaluable opportunity to boost savings in later years.

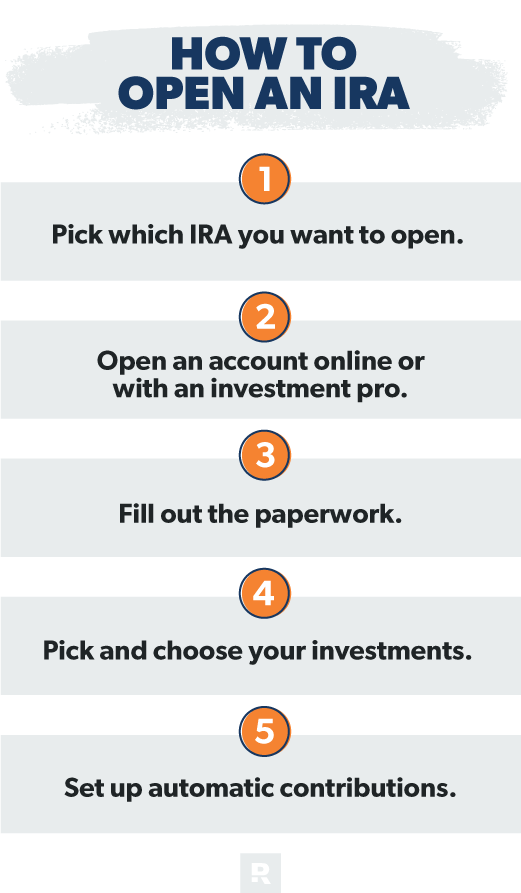

The Step-by-Step Guide to Opening Your IRA

Once you’ve grasped the different IRA types, the actual process of setting one up is straightforward. While it might seem daunting initially, breaking it down into manageable steps will clarify the path to securing your financial future.

Step 1: Choose Your IRA Type

This is arguably the most crucial initial decision. Consider the following:

- Your current income and expected future income: If you expect to be in a higher tax bracket in retirement, a Roth IRA might be more beneficial due to its tax-free withdrawals. If you’re in a high tax bracket now and expect to be in a lower one in retirement, a Traditional IRA with upfront deductions could be advantageous.

- Your employer-sponsored plan: Do you have access to a 401(k) or similar plan? If so, contributing enough to get the employer match is usually priority number one. After that, an IRA can complement your workplace plan.

- Your tax philosophy: Do you prefer paying taxes now (Roth) or deferring them until later (Traditional)?

- Income limitations: Be mindful of the income limits for direct Roth IRA contributions.

Step 2: Select a Financial Institution

After deciding on the type of IRA, the next step is to choose where you will open and hold your account. A wide array of financial institutions offer IRAs, each with its own strengths:

- Brokerage Firms: Companies like Vanguard, Fidelity, Charles Schwab, and E*TRADE are popular choices. They offer a vast selection of investment products (stocks, bonds, mutual funds, ETFs), research tools, and often competitive fees. They are ideal for those who want to be hands-on with their investments.

- Robo-Advisors: Services like Betterment and Wealthfront use algorithms to build and manage diversified portfolios based on your risk tolerance and financial goals. They are excellent for new investors or those who prefer a low-cost, hands-off approach.

- Banks and Credit Unions: While they offer IRAs, their investment options are often limited, typically to Certificates of Deposit (CDs) or savings accounts, which may not provide sufficient growth for long-term retirement savings. They are generally less suitable for a diversified IRA portfolio.

When selecting an institution, consider:

- Fees: Look for low expense ratios on investment funds and minimal (or no) account maintenance fees or trading commissions.

- Investment Options: Ensure they offer the types of investments you’re interested in (e.g., a wide range of ETFs, low-cost index funds).

- Customer Service and Research Tools: Good support and robust tools can be invaluable, especially for newer investors.

- Minimums: Some institutions have minimum initial deposit requirements.

Step 3: Complete the Application Process

Once you’ve chosen your institution, opening the IRA is usually a straightforward process. Most institutions allow you to complete the application entirely online in about 15-30 minutes. You will typically need to provide:

- Personal Information: Your full name, address, date of birth.

- Social Security Number (SSN): Required for tax reporting purposes.

- Employer Information: Sometimes requested but not always mandatory for an IRA.

- Bank Account Information: To link your bank account for funding the IRA.

- Beneficiary Designation: Crucially, you’ll be asked to name beneficiaries who will inherit your IRA funds upon your passing. This bypasses probate and ensures your assets go to your chosen individuals.

Take your time to accurately fill out all sections and review them before submitting.

Step 4: Fund Your IRA Account

After your application is approved, the final step is to fund your IRA. You can do this by:

- Electronic Funds Transfer (EFT): Linking your bank account allows you to transfer funds directly. This is the most common method.

- Check: Mailing a check to the institution.

- Rollover: If you’re moving funds from an old 401(k) or another retirement account, you can initiate a direct rollover.

- Recurring Contributions: Many institutions allow you to set up automatic, recurring contributions, which is an excellent way to maintain consistency and leverage dollar-cost averaging.

Remember to stay within the annual contribution limits to avoid penalties. The deadline for contributing to an IRA for a given tax year is typically the tax filing deadline for that year (e.g., April 15th of the following year).

Navigating Investment Choices Within Your IRA

Setting up the IRA is only half the battle; the other half is wisely investing the funds within it. An IRA is a wrapper; what you put inside matters most for your long-term growth. The goal is to build a diversified portfolio that aligns with your risk tolerance and time horizon.

Diversification is Key

Diversification is the cornerstone of sound investing. It means spreading your investments across different asset classes, industries, and geographies to reduce risk. The principle is simple: don’t put all your eggs in one basket. If one investment performs poorly, others may still do well, smoothing out your overall returns.

- Asset Allocation: This refers to how you divide your portfolio among different asset classes like stocks, bonds, and cash. Your age, financial goals, and comfort with risk will largely determine your ideal asset allocation. Younger investors with a longer time horizon can typically afford to take on more risk with a higher allocation to stocks, while those closer to retirement might shift towards a more conservative portfolio with a higher allocation to bonds.

- Risk Tolerance Assessment: Honestly evaluate how much market volatility you can psychologically endure. This will guide your investment choices.

Common Investment Vehicles

Within your IRA, you’ll typically have access to a wide range of investment options:

- Stocks: Represent ownership in a company. They offer potential for high growth but also higher risk. You can buy individual stocks or invest in stock funds.

- Bonds: Essentially loans to governments or corporations, paying regular interest. They are generally less volatile than stocks and provide income, acting as a ballast in a portfolio.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other investments. They offer instant diversification.

- Index Funds: A type of mutual fund or ETF that aims to replicate the performance of a specific market index (e.g., S&P 500). They are typically low-cost and passively managed.

- Actively Managed Funds: Fund managers actively buy and sell investments to try and outperform an index. They often come with higher fees.

- Exchange-Traded Funds (ETFs): Similar to mutual funds, but they trade like individual stocks on an exchange throughout the day. They often have lower expense ratios than actively managed mutual funds and offer great flexibility.

- Target-Date Funds: A single fund that automatically adjusts its asset allocation (becoming more conservative) as you approach a specific target retirement date. These are excellent for hands-off investors who want a “set it and forget it” approach to diversification and rebalancing.

- Real Estate Investment Trusts (REITs): Companies that own, operate, or finance income-producing real estate. They allow you to invest in real estate without directly owning property.

Rebalancing Your Portfolio

Over time, your initial asset allocation can drift as certain investments perform better than others. Rebalancing is the process of adjusting your portfolio back to your desired asset allocation. This typically involves selling investments that have grown significantly and buying more of those that have lagged. Regular rebalancing (e.g., once a year or when allocations drift significantly) helps maintain your desired risk level and ensures you’re not overexposed to any single asset class.

Maximizing Your IRA for Long-Term Growth

Opening and funding your IRA is a fantastic start, but to truly maximize its potential, you need to adopt a disciplined, long-term approach. Strategic management and consistent attention, even if minimal, can significantly enhance your retirement savings.

Consistency is Crucial: Automate Your Contributions

One of the most powerful strategies for IRA growth is consistent contributions. Automating your contributions—setting up regular, recurring transfers from your bank account to your IRA—removes the temptation to skip contributions and ensures you’re consistently investing. This strategy also harnesses the power of “dollar-cost averaging,” where you invest a fixed amount regularly, regardless of market fluctuations. When prices are high, your fixed dollar amount buys fewer shares; when prices are low, it buys more shares. Over time, this can lead to a lower average cost per share and reduce the impact of market volatility.

Understand and Avoid Common Pitfalls

While IRAs offer significant benefits, there are pitfalls to avoid:

- Early Withdrawal Penalties: Withdrawing funds from your IRA before age 59½ typically incurs a 10% early withdrawal penalty, in addition to income taxes on Traditional IRA withdrawals. There are a few exceptions (e.g., for certain medical expenses, first-time home purchases up to $10,000), but generally, it’s best to keep your IRA funds reserved for retirement.

- Required Minimum Distributions (RMDs): For Traditional IRAs, you must begin taking RMDs once you reach age 73 (as of 2023 legislation). Failing to do so can result in substantial penalties (up to 25% of the amount you should have withdrawn). Roth IRAs generally do not have RMDs for the original owner.

- Over-Contributing: Exceeding the annual contribution limits can lead to a 6% excise tax on the excess amount each year it remains in the account. Most financial institutions will alert you if you’re nearing the limit.

- Ignoring Fees: High investment fees, even seemingly small percentages, can significantly erode your returns over decades. Prioritize low-cost index funds and ETFs.

Review and Adjust Annually

Your financial life is not static, and neither should be your retirement plan. Make it a habit to review your IRA and overall financial strategy at least once a year. This annual check-up should include:

- Contribution Limits: Ensure you’re aware of and contributing up to the maximum allowable amount.

- Investment Performance: How are your investments doing? Are they still aligned with your risk tolerance?

- Life Changes: Has your income changed? Have you gotten married, had children, or changed jobs? These events might necessitate adjustments to your IRA strategy or beneficiary designations.

- Market Conditions: While you shouldn’t react to every market swing, a general awareness of the economic landscape can inform your long-term strategy.

- Tax Law Changes: Retirement and tax laws can change, so staying informed (or consulting a professional) is important.

Consider Professional Guidance

For many, navigating the complexities of investing and retirement planning can be overwhelming. Don’t hesitate to consider seeking advice from a qualified financial advisor. A fee-only financial planner can provide personalized guidance, help you choose the right IRA, develop a suitable investment strategy, optimize your tax situation, and ensure your retirement plan stays on track through life’s changes. Their expertise can be particularly valuable for those with complex financial situations or those who simply prefer professional oversight.

In conclusion, setting up an IRA is a powerful step towards achieving financial independence in retirement. By understanding the different types, choosing the right institution, making informed investment choices, and committing to a consistent, long-term approach, you can harness the full potential of this invaluable retirement vehicle. Start today, stay disciplined, and watch your future self thank you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.