In the complex landscape of personal finance and tax obligations, Form 1099 stands as a pivotal document for millions of Americans. It serves as an “information return,” meaning it’s used to report various types of income other than salaries, wages, and tips. For independent contractors, freelancers, investors, and even those who receive certain types of miscellaneous income, understanding where and how to obtain your Form 1099 is not just a matter of convenience—it’s a critical step in ensuring tax compliance and managing your financial health. This comprehensive guide delves into the nuances of Form 1099, pinpointing the primary sources for these essential documents and offering strategies for navigating common challenges.

Demystifying Form 1099: Its Purpose and Significance

Before delving into the practicalities of acquiring these forms, it’s essential to grasp what Form 1099 represents and why it holds such importance in the financial world. It’s more than just a piece of paper; it’s a key component of the IRS’s system for tracking non-employment income, ensuring fairness and accuracy in tax collection.

What Exactly is a Form 1099?

At its core, a Form 1099 is a series of tax forms issued by an individual or entity (the “payer”) to another individual or entity (the “payee”) to report specific types of payments made during the calendar year. Unlike a W-2 form, which reports wages and taxes withheld from an employee, 1099 forms report various forms of non-employment income. The IRS uses these forms to ensure that taxpayers accurately report all their income, thereby preventing tax evasion and promoting a more equitable tax system.

There are numerous variations of the Form 1099, each designed to report a specific type of income or transaction. While the most common might be for nonemployee compensation, others cover interest, dividends, stock sales, and even payments from third-party payment networks. Understanding the specific type of 1099 you need or receive is the first step toward accurate tax filing.

Who Needs a 1099? Understanding the Payer and Payee

The recipients of 1099 forms typically fall into several broad categories, reflecting the diverse nature of non-employment income.

- Independent Contractors and Freelancers: Perhaps the largest group, individuals who work for businesses as independent contractors rather than employees often receive a Form 1099-NEC (Nonemployee Compensation) if they earn $600 or more from a single payer in a calendar year. This includes gig workers, consultants, writers, designers, and many others operating in the burgeoning freelance economy.

- Investors: Those with investment income will receive various 1099s. Banks issue Form 1099-INT for interest earned, while brokerages send Form 1099-DIV for dividends and Form 1099-B for proceeds from stock or other security sales.

- Rental Property Owners: Landlords might receive a Form 1099-MISC if they are paid for rent by a business (e.g., if a business leases property from them).

- Recipients of Miscellaneous Income: This can include prize winnings, awards, legal settlements, and certain healthcare payments, often reported on Form 1099-MISC.

- Third-Party Payment Network Users: Individuals or businesses receiving payments through platforms like PayPal, Stripe, or even ride-sharing apps might receive a Form 1099-K if they meet certain transaction thresholds.

The “payer” is typically the business or financial institution making the payment. They are legally obligated to issue these forms to payees and also to submit a copy to the IRS, creating a paper trail that helps match reported income.

Why Is Accurate 1099 Reporting Crucial?

Accurate and timely handling of Form 1099s is not merely a bureaucratic exercise; it has significant implications for both the payer and the payee.

For the payee (the income recipient), these forms are indispensable for:

- Accurate Tax Filing: They provide the precise figures needed to report income on Schedule C (for self-employment), Schedule B (for interest/dividends), or other relevant tax forms, preventing errors that could lead to audits or penalties.

- Avoiding Penalties: The IRS matches the income reported on your tax return with the 1099s it receives. Discrepancies can trigger penalties for underreported income.

- Financial Planning: Understanding your total non-employment income helps in planning for estimated taxes throughout the year and assessing your overall financial health.

For the payer (the entity issuing the 1099), compliance is critical to:

- Deducting Business Expenses: Only by properly reporting payments to contractors on 1099s can businesses accurately deduct those expenses.

- Avoiding Penalties: Businesses face penalties for failing to issue 1099s, issuing them late, or providing incorrect information.

In essence, Form 1099 acts as a cornerstone of tax transparency, ensuring that all parties fulfill their financial obligations to the government.

The Primary Channels for Receiving Your 1099 Documents

Knowing where to look for your 1099s can save you considerable stress and time come tax season. While the core obligation lies with the payer, modern finance offers several avenues for recipients to access these vital documents.

Direct from the Payer: The Traditional Method

The most direct and traditional way to receive your Form 1099 is directly from the entity that paid you. By law, most payers must mail these forms by January 31st of the year following the tax year for which income is being reported.

- Physical Mail: Many smaller businesses or individuals still opt for sending 1099s via postal service. Ensure your mailing address with all clients and financial institutions is up-to-date.

- Direct Email (with Consent): Some payers might offer to send your 1099 electronically via email. This usually requires your explicit consent. Always ensure the email is from a legitimate source and that any attachments are secure before opening.

- Secure Online Portals: Increasingly, larger businesses and financial institutions provide dedicated secure portals where you can log in, view, and download your 1099 forms. These portals offer enhanced security and instant access once the forms are generated.

It is always prudent to keep an organized record of all entities from which you expect a 1099 to cross-reference against what you actually receive.

Digital Platforms and Financial Institutions: Your Online Hubs

The digital transformation of finance has created centralized hubs for accessing tax documents, significantly streamlining the process for many.

- Brokerage Accounts and Online Banks: If you have investment accounts (stocks, bonds, mutual funds) or high-yield savings accounts, your brokerage firm or bank will likely provide your 1099-B, 1099-DIV, and 1099-INT forms through your online account portal. Navigate to the “Tax Documents” or “Statements” section of your online account.

- Payment Processors: Companies like PayPal, Stripe, Square, and others that facilitate payments for goods and services often issue Form 1099-K if you meet specific transaction thresholds (e.g., over $20,000 in payments AND more than 200 transactions, though states may have lower thresholds). These are typically accessible through your merchant or business account dashboard on their respective websites.

- Gig Economy Platforms: If you drive for Uber or Lyft, deliver for DoorDash, or offer services through platforms like Upwork or Fiverr, these platforms usually provide your 1099-NEC (or 1099-K, depending on the platform and nature of the payments) directly through your driver or contractor portal.

These digital channels often offer the convenience of downloading printable PDFs or even integrating directly with tax software.

Your Employer’s/Client’s Online Dashboard

For independent contractors who work regularly with specific businesses, many companies provide dedicated contractor portals. These dashboards are designed to manage invoices, payments, and, critically, tax documents. Check your login area for sections labeled “Tax Information,” “Documents,” or “My Earnings.” This is especially common with larger organizations that manage a significant contractor workforce.

Leveraging Tax Software Integration

Modern tax preparation software, such as TurboTax, H&R Block, and TaxAct, has advanced capabilities to directly import tax data, including certain 1099 forms, from participating financial institutions and payroll providers. After linking your accounts within the software, it can automatically pull in the necessary information, reducing manual entry and potential errors. While this is incredibly convenient, it’s crucial to review the imported data against your own records to ensure accuracy. This method works best for institutions that have partnered with the specific tax software.

Navigating Common 1099 Types and What to Expect

The “1099” is not a singular form but a family of forms, each designed for a particular type of income. Understanding which ones you might receive is crucial for accurate tax reporting.

1099-NEC: The Freelancer’s Cornerstone

The Form 1099-NEC, or Nonemployee Compensation, was reintroduced by the IRS starting in the 2020 tax year. It specifically reports payments of $600 or more made to individuals not classified as employees, primarily independent contractors, freelancers, and self-employed individuals. This form replaced the use of Form 1099-MISC for reporting nonemployee compensation. If you’ve been paid for services as a contractor, this is the form you’ll most commonly receive. It summarizes your gross earnings from a specific payer, which you will then report on Schedule C (Form 1040) when filing your taxes.

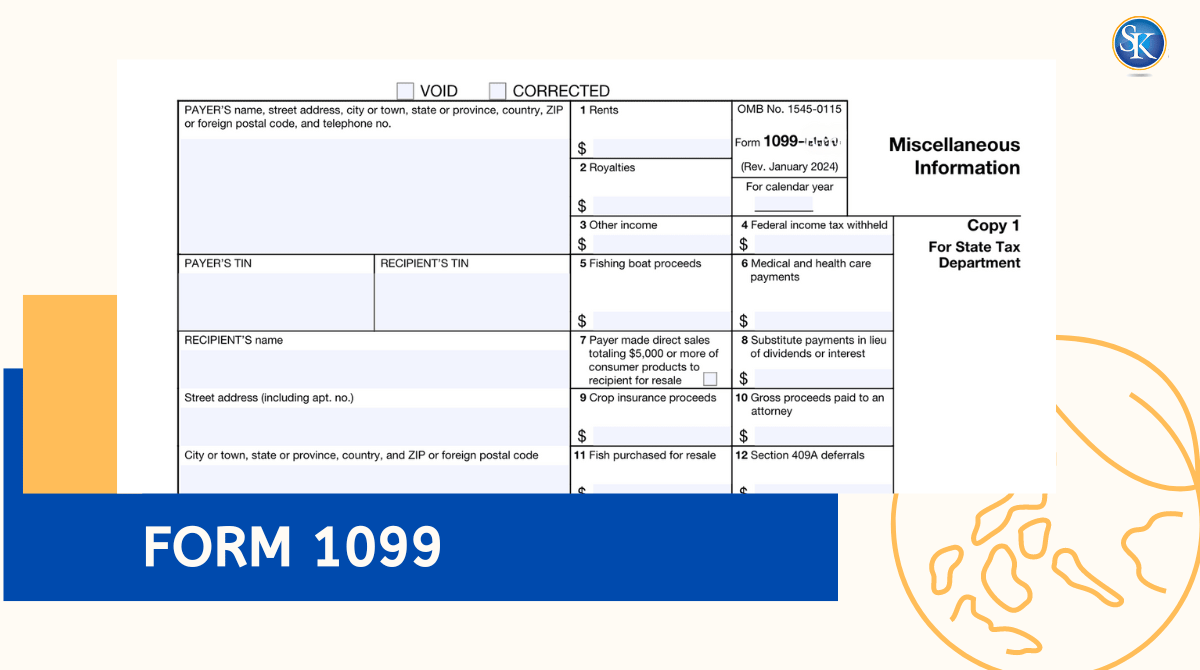

1099-MISC: Beyond Nonemployee Compensation

While previously used for nonemployee compensation, the Form 1099-MISC (Miscellaneous Information) now primarily reports other types of miscellaneous income totaling $600 or more. This can include:

- Rents (e.g., if you’re a landlord and a business pays you rent)

- Prizes and awards

- Other income payments

- Medical and health care payments

- Payments to attorneys (in certain circumstances)

It’s important to distinguish between 1099-NEC and 1099-MISC to ensure proper income classification on your tax return.

Investment Income: 1099-INT, 1099-DIV, 1099-B

For investors, a trio of 1099 forms reports various aspects of investment income:

- 1099-INT (Interest Income): Issued by banks, credit unions, and other financial institutions, this form reports interest of $10 or more paid to you during the year.

- 1099-DIV (Dividends and Distributions): Brokerage firms and mutual fund companies issue this form to report dividends and other distributions of $10 or more from stocks and mutual funds.

- 1099-B (Proceeds From Broker and Barter Exchange Transactions): This is a critical form for anyone who sells stocks, bonds, mutual funds, or other securities. It reports the proceeds from sales, along with details like acquisition date and cost basis (if available), which are essential for calculating capital gains or losses.

Other Key 1099 Forms

Several other 1099 forms address specific financial scenarios:

- 1099-K (Payment Card and Third Party Network Transactions): If you process payments through credit cards or third-party payment networks (like PayPal, Square, or various gig-economy apps) and meet specific thresholds ($20,000 in gross payments and 200 transactions federally, with some states having lower thresholds), you will receive a 1099-K. This reports the total gross amount of reportable payment transactions.

- 1099-R (Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.): This form reports distributions from retirement accounts, pensions, and annuities. It’s crucial for determining the taxable portion of your retirement income.

- 1099-G (Certain Government Payments): This reports taxable grants, agricultural payments, unemployment compensation, and state or local income tax refunds.

Each of these forms plays a unique role in your overall tax picture, and understanding their purpose is key to accurate filing.

Addressing Missing 1099s and Proactive Tax Planning

Despite best efforts, you might encounter situations where a 1099 is missing, incorrect, or delayed. Knowing how to react and, more importantly, how to plan proactively can prevent undue stress during tax season.

Understanding 1099 Deadlines: When to Expect Them

Most 1099 forms (including 1099-NEC, 1099-MISC, 1099-INT, 1099-DIV, and 1099-B) are required to be sent to recipients by January 31st of the year following the tax year for which income is being reported. For example, for income earned in 2023, you should receive your forms by January 31, 2024. Some forms, like certain 1099-B statements with complex transactions, might have a later deadline, typically February 15th. It’s wise to mark these dates on your calendar.

What to Do If a 1099 Is Missing or Incorrect

If January 31st (or February 15th for some forms) passes and you haven’t received an expected 1099, don’t panic, but do take action:

- Check All Possible Locations: Re-check your physical mail (including spam folders if you opted for electronic delivery) and all online portals for financial institutions and platforms you use.

- Contact the Payer Directly: This is the first and most effective step. Reach out to the client, business, or financial institution you expect the 1099 from. Confirm your mailing address or email, and inquire about the status of the form. Request that they resend it. Document all communication, including dates and names.

- Wait a Reasonable Time: Allow a week or two after contacting the payer for the form to arrive.

- Contact the IRS: If you still haven’t received the form by the end of February, you can contact the IRS directly for assistance. The IRS can reach out to the payer on your behalf. You’ll need the payer’s name, address, phone number, and employer identification number (EIN), if known.

If you receive a 1099 with incorrect information (e.g., wrong amount or name), contact the payer immediately to request a corrected form.

Reporting Income Without a 1099: Your Obligation

Crucially, even if you do not receive a Form 1099 for income you earned, you are still legally obligated to report that income to the IRS. The absence of a 1099 does not absolve you of your tax responsibilities.

- Maintain Detailed Records: This is where meticulous record-keeping throughout the year becomes invaluable. Keep invoices, bank statements, and payment confirmations to accurately track all income received.

- Use Substitute Statements: You can use your own records to report the income. For example, if you know you received $1,200 from a client, but never got a 1099-NEC, you would still report that $1,200 on Schedule C. The IRS generally expects individuals to report all income regardless of whether a 1099 was issued.

Failing to report income simply because you didn’t receive a 1099 can lead to penalties and interest.

Best Practices for Year-Round Financial Organization

Proactive financial management is the best defense against tax season headaches.

- Dedicated Accounts: Use separate bank accounts for business income and expenses if you’re a freelancer or independent contractor. This makes tracking revenue much simpler.

- Digital Record Keeping: Implement a system for saving invoices, receipts, and payment confirmations digitally. Cloud storage or accounting software can automate much of this.

- Track Expected 1099s: Maintain a running list of all clients, platforms, and financial institutions from which you expect a 1099. Include their contact information and EINs if available.

- Estimated Taxes: If you anticipate significant non-employment income, remember to pay estimated quarterly taxes to avoid underpayment penalties.

- Consult a Professional: If your financial situation is complex, or you have questions about specific 1099s, consider consulting a tax professional. Their expertise can ensure compliance and potentially identify deductions you might overlook.

In conclusion, Form 1099 is a foundational document in the realm of non-employment income reporting. While the process of obtaining and understanding these forms might seem daunting, knowing where to look, what to expect, and how to proactively manage your financial records will empower you to navigate tax season with confidence and ensure full compliance with IRS regulations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.