Navigating the world of taxes can often feel like deciphering a complex code. For many, the phrase “getting my tax return” conjures images of a much-anticipated refund, a welcome financial boost. However, the term “tax return” itself has a dual meaning, referring both to the official document you submit to the tax authorities and, colloquially, to the refund you might receive. Understanding this distinction is the first step toward confidently managing your annual tax obligations and maximizing any potential financial benefits.

This guide will demystify the entire process, from understanding your obligations to successfully filing your return, identifying opportunities to reduce your tax liability, and ultimately tracking and receiving any refund due to you. We’ll explore the various methods available for filing, crucial information you need to gather, and best practices for a smooth, stress-free tax season.

Demystifying “Your Tax Return”: Document, Obligation, and Refund

Before diving into the “how-to,” it’s essential to clarify what we mean by “tax return.” Often, people use the phrase “getting my tax return” when they’re actually referring to “getting my tax refund.” Let’s break down these critical concepts.

The Tax Return Document vs. The Tax Refund

A tax return is the official form (e.g., Form 1040 in the U.S.) that you file with a tax authority (like the IRS or your state’s revenue department) to report your income, deductions, and credits. It’s a comprehensive summary of your financial year, detailing how much tax you owe or how much you are owed back. This document is your declaration of your financial activities to the government.

A tax refund, on the other hand, is the money returned to you by the tax authority if you paid more in taxes than you actually owed throughout the year. This often happens when too much tax was withheld from your paychecks, or you qualify for various credits and deductions that reduce your overall tax liability below what you’ve already paid. Essentially, it’s an overpayment that the government is returning to you. So, when you ask “how do I get my tax return?”, you’re most likely asking “how do I file my tax return to get my tax refund?”

Why Filing On Time Matters

Filing your tax return by the due date (typically April 15th for most individuals in the U.S., though extensions are possible) is not just a suggestion; it’s a legal obligation for most income earners. Failing to file on time can result in penalties, interest charges, and even legal consequences, especially if you owe taxes. Even if you are due a refund, failing to file means you won’t receive that money until you submit your return. There is generally no penalty for filing late if you are owed a refund, but you typically have a three-year window from the original due date to claim it.

Who Needs to File?

Not everyone is required to file a tax return. Whether you need to file depends on factors like your gross income, filing status, age, and whether you are claimed as a dependent by someone else. For example, if your income falls below a certain threshold, you might not be required to file. However, even if not required, it’s often a good idea to file if you had taxes withheld from your pay or qualify for refundable tax credits (like the Earned Income Tax Credit), as this is the only way to get a refund you might be owed.

Navigating the Tax Filing Process: Your Options for Submission

Once you understand that “getting your tax return” primarily means filing the necessary documentation, the next step is to choose the method that best suits your needs and comfort level. You have several avenues, each with its own advantages.

DIY with Tax Software: Efficiency at Your Fingertips

For many individuals and families with relatively straightforward tax situations, using online tax preparation software is a popular and efficient choice. Platforms like TurboTax, H&R Block, TaxAct, and FreeTaxUSA guide you step-by-step through the filing process, asking questions about your income, deductions, and credits. They perform the calculations, check for errors, and often allow you to e-file (electronically file) your federal and state returns directly from the software. This method offers convenience, speed, and often cost-effectiveness, with many providers offering free versions for simple returns.

The Professional Touch: Enlisting an Accountant or Tax Preparer

If your tax situation is complex—perhaps you own a business, have investments, rental properties, or recently experienced significant life changes (marriage, divorce, new child)—hiring a professional tax preparer, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA), can be invaluable. These experts can provide personalized advice, identify obscure deductions, ensure compliance, and even represent you if audited. While more expensive, the peace of mind and potential for greater savings can often outweigh the cost, especially for those with intricate financial affairs.

Free Filing Options: Leveraging Government Resources

For taxpayers below certain income thresholds, several free filing options are available. The IRS offers its Free File program, which partners with commercial tax software providers to offer free online tax preparation and e-filing for eligible taxpayers. Additionally, the Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) programs offer free tax help to qualified individuals, including those with disabilities, limited English proficiency, or who are 60 years or older. These programs utilize IRS-certified volunteers to prepare basic tax returns.

Essential Documents to Gather

Regardless of your chosen filing method, preparation is key. Before you begin, gather all necessary documents:

- Proof of Identity: Social Security numbers (SSN) or Individual Taxpayer Identification Numbers (ITIN) for yourself, your spouse, and dependents.

- Income Statements: W-2s from employers, 1099 forms (1099-NEC for contract work, 1099-INT for interest, 1099-DIV for dividends, 1099-R for retirement distributions, etc.), K-1 forms for partnership income.

- Deduction and Credit Documentation: Statements for mortgage interest (Form 1098), student loan interest (Form 1098-E), tuition fees (Form 1098-T), charitable contributions, medical expenses, childcare expenses, and records of retirement contributions (IRA, 401(k)).

- Prior Year Information: A copy of your previous year’s tax return, as some information carries over.

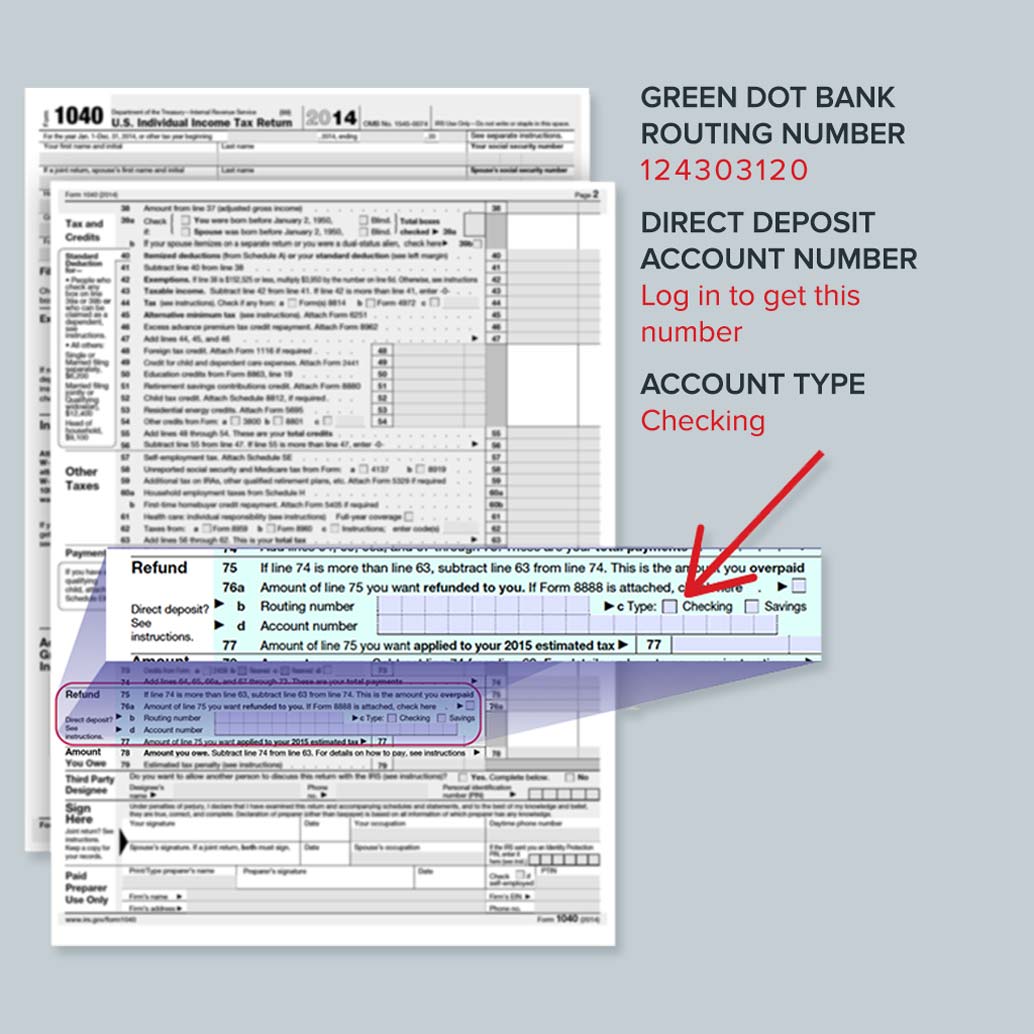

- Bank Account Information: For direct deposit of any refund.

Strategies for Maximizing Your Tax Refund (or Minimizing Your Liability)

Once you’ve decided how you’ll file, the focus shifts to ensuring you receive every dollar you’re entitled to. This involves understanding and leveraging the various deductions and credits available.

Understanding Deductions and Credits

- Deductions reduce your taxable income. For example, if you have an income of $50,000 and claim $5,000 in deductions, your taxable income becomes $45,000. This means you’ll pay tax on a lower amount of income. Deductions can be either standard (a fixed amount based on your filing status) or itemized (specific expenses like medical costs, state and local taxes, or mortgage interest). You choose whichever results in a larger reduction.

- Credits directly reduce the amount of tax you owe, dollar for dollar. A $1,000 tax credit reduces your tax bill by $1,000. Some credits are even “refundable,” meaning that if the credit amount is more than your tax liability, you get the difference back as a refund. Credits are generally more valuable than deductions.

Key Deductions to Look For

Common deductions include:

- Standard Deduction: A fixed amount that varies by filing status and age. Most taxpayers take the standard deduction.

- Itemized Deductions: If your eligible itemized expenses exceed the standard deduction, you can itemize. These include medical expenses (above a certain AGI threshold), state and local taxes (SALT cap applies), home mortgage interest, and charitable contributions.

- Above-the-Line Deductions: These reduce your gross income to arrive at your adjusted gross income (AGI) and can be taken even if you take the standard deduction. Examples include contributions to traditional IRAs, student loan interest, and health savings account (HSA) contributions.

Exploring Valuable Tax Credits

Credits can significantly boost your refund or reduce your tax owed:

- Child Tax Credit: For eligible parents, this non-refundable credit can be up to $2,000 per qualifying child. A portion of it may be refundable as the Additional Child Tax Credit.

- Earned Income Tax Credit (EITC): A refundable credit for low-to-moderate income working individuals and families, designed to provide a financial boost. The amount depends on income, filing status, and number of qualifying children.

- Education Credits: Credits like the American Opportunity Tax Credit and Lifetime Learning Credit help offset the cost of higher education.

- Child and Dependent Care Credit: Helps cover expenses for care of a qualifying child or dependent so you can work or look for work.

- Savers Credit (Retirement Savings Contributions Credit): A non-refundable credit for low- and moderate-income taxpayers who contribute to retirement accounts.

The Impact of Withholding: W-4 Adjustments

Your Form W-4, which you provide to your employer, dictates how much income tax is withheld from your paycheck. If too much is withheld, you’ll likely receive a larger refund. If too little is withheld, you might owe taxes or even face penalties. Reviewing and adjusting your W-4 annually, especially after major life changes, can help ensure your withholding matches your actual tax liability, minimizing the likelihood of a large tax bill or an unnecessarily large refund (which essentially means you gave the government an interest-free loan). The IRS Tax Withholding Estimator is a useful online tool for this purpose.

What Happens After You File? Tracking and Receiving Your Refund

Once you’ve diligently prepared and submitted your tax return, the next logical question is: “When will I get my money?” The processing of tax returns and the issuance of refunds follows a fairly predictable path, though patience is often required.

The Waiting Game: Processing Times Explained

The IRS typically processes most e-filed returns within 21 days. However, factors such as the time of year you file (early filers often see quicker refunds), the complexity of your return, whether you claim certain credits (like the EITC or Additional Child Tax Credit, which by law delay processing until mid-February), and any errors detected can extend this timeframe. Paper-filed returns take significantly longer, often 6-8 weeks or more. State refund processing times vary widely by state, from a few days to several weeks.

How to Track Your Federal Refund

The easiest and most efficient way to check the status of your federal refund is by using the IRS’s “Where’s My Refund?” tool. You’ll need your Social Security number or ITIN, your filing status, and the exact refund amount shown on your return. The tool updates daily, usually overnight, and provides three statuses:

- Return Received: The IRS has your return and is processing it.

- Refund Approved: The IRS has processed your return and confirmed your refund amount.

- Refund Sent: Your refund has been sent to your bank via direct deposit or as a paper check.

State Refunds: A Separate Journey

If you filed a state income tax return and are due a refund, you’ll need to check its status separately. Most state tax agencies have their own online “Where’s My Refund?” tools, similar to the federal one. You’ll typically need similar information: SSN, filing status, and refund amount. Access your state’s Department of Revenue or taxation website to find their specific tracking portal.

Direct Deposit vs. Paper Check: Choosing Your Payout Method

When you file your return, you’ll be asked to choose how you want to receive your refund.

- Direct Deposit: This is by far the fastest and most secure way to receive your refund. Providing your bank account and routing numbers allows the tax authority to electronically transfer the funds directly into your account, typically within days of approval.

- Paper Check: If you don’t opt for direct deposit, a paper check will be mailed to the address on your return. This method is slower and carries a higher risk of postal delays, loss, or theft. For a quicker and safer option, direct deposit is highly recommended.

Beyond the Basics: Common Questions and Proactive Planning

The tax journey doesn’t necessarily end when your refund hits your account. Understanding how to handle potential issues and planning for the future can prevent headaches and optimize your financial position.

What if I Made a Mistake? Amending Your Return

Don’t panic if you discover an error on a previously filed return. You can usually correct it by filing an amended return, typically using Form 1040-X, Amended U.S. Individual Income Tax Return. You generally have three years from the date you filed your original return (or two years from the date you paid the tax, whichever is later) to file an amended return to claim a refund. If you owe additional tax due to the error, it’s best to amend and pay as soon as possible to avoid further penalties and interest.

Dealing with an Audit: Preparedness is Key

The word “audit” can strike fear into the hearts of many, but audits are relatively rare. If the IRS selects your return for an audit, it typically means they need more information to verify items on your return. The best defense is a good offense:

- Keep Meticulous Records: Retain all supporting documentation (receipts, bank statements, W-2s, 1099s, etc.) for at least three years, or longer for certain assets.

- Be Honest and Accurate: Always report all income and claim only legitimate deductions and credits.

- Respond Promptly: If contacted for an audit, respond within the requested timeframe and provide only the information asked for. Consider seeking professional help from a tax preparer or CPA.

Proactive Tax Planning: A Year-Round Endeavor

Effective tax management isn’t just about filing once a year; it’s a continuous process. Throughout the year, consider:

- Reviewing Withholding: Adjust your W-4 if your income, deductions, or life circumstances change.

- Maximizing Tax-Advantaged Accounts: Contribute to 401(k)s, IRAs, HSAs, and 529 plans for their tax benefits.

- Tracking Expenses: Keep a digital or physical log of potential deductions and credits.

- Understanding Tax Law Changes: Stay informed about new tax laws or changes that might affect you.

- Consulting a Professional: A financial advisor or tax professional can help you develop a personalized tax strategy.

The Importance of Record Keeping

This cannot be overstated. Maintaining organized records of all financial transactions, income statements, deduction receipts, and previous tax returns is paramount. Not only does it make the current year’s filing easier, but it also serves as your evidence in case of discrepancies or an audit. Digital copies, stored securely, are often a convenient and reliable method.

In conclusion, “getting your tax return” is a multi-faceted process that culminates in filing an accurate document and, hopefully, receiving a well-deserved refund. By understanding the terminology, choosing the right filing method, strategically leveraging deductions and credits, and proactively managing your financial records, you can transform a potentially daunting annual task into a straightforward exercise in financial literacy and optimization.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.