In the complex landscape of personal and business finance, one question consistently stands out for individuals and entities alike: “How do you reduce your taxable income?” The answer isn’t a single silver bullet but rather a strategic combination of understanding tax laws, leveraging available deductions and credits, and making intelligent financial decisions throughout the year. Reducing your taxable income isn’t about avoiding taxes; it’s about optimizing your financial situation by legally minimizing the portion of your earnings subject to taxation. This proactive approach can lead to significant savings, freeing up capital for investment, debt reduction, or simply enhancing your overall financial well-being. This article will delve into actionable strategies to help you navigate the tax code and keep more of your hard-earned money.

Understanding Taxable Income and Why It Matters

Before diving into specific strategies, it’s crucial to grasp what taxable income is and why its reduction holds such financial power. A clear understanding forms the bedrock of effective tax planning.

What is Taxable Income?

At its most basic, taxable income is the portion of your gross income that the government can levy taxes on. It’s not the same as your gross income, which includes all earnings before any deductions. Instead, taxable income is typically derived after certain adjustments, deductions, and exemptions are applied. For individuals, this often starts with your Adjusted Gross Income (AGI), calculated by subtracting specific “above-the-line” deductions (like traditional IRA contributions, student loan interest, or self-employment tax) from your gross income. From your AGI, you then subtract either the standard deduction or your itemized deductions to arrive at your final taxable income figure. Businesses have a similar process, subtracting allowable business expenses from their revenue to determine taxable profit.

The Power of Tax Savings

The financial benefits of reducing your taxable income extend far beyond just paying less tax in the current year. Each dollar you save on taxes is a dollar that can be invested, compounded over time, and used to accelerate your financial goals. For instance, if you save $1,000 in taxes and invest it, that money has the potential to grow substantially over decades, contributing significantly to your retirement fund or other long-term savings. Furthermore, a lower taxable income can sometimes qualify you for various government benefits, tax credits, or lower premiums on things like healthcare, where eligibility is often tied to AGI. It’s a foundational step towards building enduring wealth and achieving financial freedom.

The Importance of Legal and Ethical Approaches

It’s paramount to emphasize that all strategies discussed herein are entirely legal and ethical. Tax planning is distinct from tax evasion. Tax evasion involves illegally misrepresenting your income or deductions to avoid paying taxes, which carries severe penalties. Tax planning, on the other hand, involves utilizing the tax code as intended by lawmakers to your advantage. It requires diligent record-keeping, an understanding of applicable laws, and often, the guidance of a qualified tax professional. The goal is to optimize, not to circumvent.

Leveraging Deductions to Shrink Your Tax Bill

Deductions are perhaps the most direct way to reduce your taxable income. They are expenses that you can subtract from your AGI, effectively lowering the amount of income subject to tax.

Standard vs. Itemized Deductions

Every taxpayer has a choice: take the standard deduction or itemize their deductions. The standard deduction is a fixed dollar amount, determined by your filing status, that you can subtract from your AGI. It simplifies tax filing for many. Itemized deductions, conversely, allow you to list and subtract specific expenses, such as mortgage interest, state and local taxes, or charitable contributions. You should choose whichever method results in a larger deduction, thereby providing a lower taxable income. For many, especially after recent tax reforms, the standard deduction is often more beneficial due to its increased amounts. However, certain life events or significant expenses can make itemizing more advantageous.

Common Itemized Deductions

If your eligible itemized expenses exceed the standard deduction, you can claim them. Some of the most common include:

- Mortgage Interest: Interest paid on a mortgage for a primary residence or a second home is typically deductible, up to certain limits.

- State and Local Taxes (SALT): You can deduct a combined total of up to $10,000 for state and local income, sales, and property taxes.

- Medical Expenses: If your unreimbursed medical expenses exceed 7.5% of your AGI, you can deduct the amount above that threshold. This can include doctor visits, prescription drugs, health insurance premiums (if not paid pre-tax), and long-term care services.

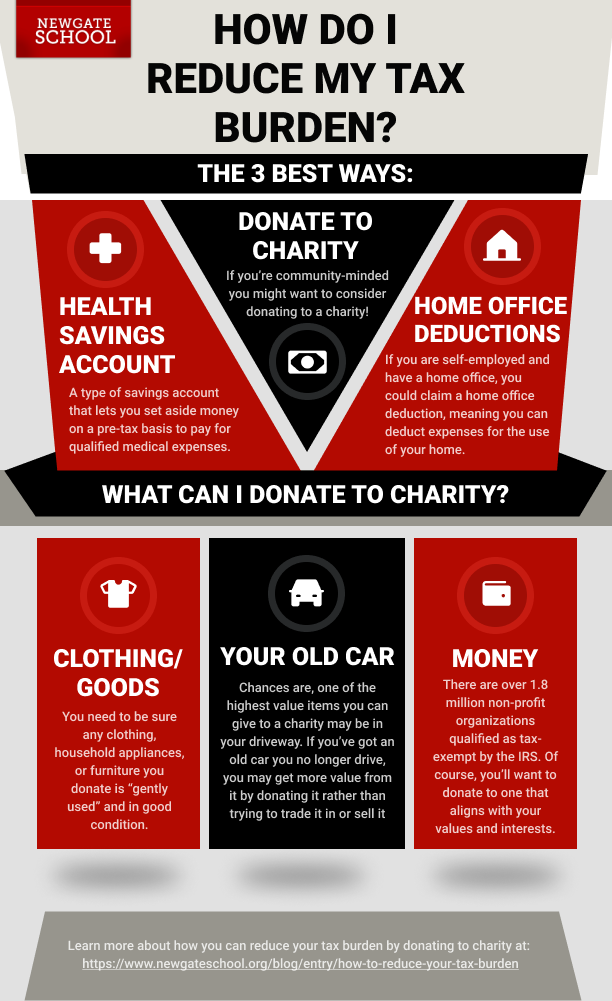

- Charitable Contributions: Donations made to qualified charitable organizations are deductible, up to certain percentages of your AGI. Both cash and non-cash contributions (like property or appreciated stock) can qualify.

Business Deductions for Self-Employed Individuals

For freelancers, contractors, and small business owners, a vast array of business deductions can significantly reduce taxable income. These “above-the-line” deductions often reduce your AGI directly. Key examples include:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for your business, you can deduct a percentage of your housing costs (rent, utilities, insurance) or use a simplified method.

- Business Expenses: Virtually all “ordinary and necessary” expenses related to running your business are deductible. This includes office supplies, software, marketing, travel for business, professional development, and legal fees.

- Health Insurance Premiums: If you’re self-employed and not eligible to participate in an employer-sponsored health plan, you can typically deduct the premiums you pay for health insurance.

- Self-Employment Tax Deduction: You can deduct one-half of your self-employment taxes (Social Security and Medicare) from your gross income.

Strategic Use of Tax-Advantaged Accounts

Beyond deductions, leveraging specific types of financial accounts designed with tax benefits in mind is a powerful strategy for reducing taxable income, particularly for long-term goals like retirement and healthcare.

Retirement Accounts

Contributions to certain retirement accounts are among the most effective ways to reduce your current taxable income.

- Traditional 401(k) and IRA: Contributions to these accounts are typically tax-deductible in the year they are made, meaning they reduce your AGI. Your money then grows tax-deferred until retirement, when withdrawals are taxed as ordinary income. Maximizing these contributions, especially employer-sponsored 401(k)s with matching contributions, is a dual benefit: saving for retirement and lowering your tax bill.

- SEP IRA and SOLO 401(k) for Self-Employed: These plans allow self-employed individuals to contribute a much larger percentage of their income than a traditional IRA, offering substantial tax deductions for business owners.

- Roth Accounts (401(k) and IRA): While Roth contributions are not tax-deductible in the present year, they offer tax-free growth and tax-free withdrawals in retirement. While they don’t reduce current taxable income, they are crucial for future tax planning, especially if you anticipate being in a higher tax bracket later in life. A blend of traditional and Roth accounts can be an optimal strategy.

Health Savings Accounts (HSAs)

HSAs are often hailed as having a “triple tax advantage” and are an invaluable tool for those with high-deductible health plans (HDHPs).

- Tax-Deductible Contributions: Contributions to an HSA are tax-deductible (or pre-tax if made through payroll deductions), reducing your taxable income.

- Tax-Free Growth: The money in your HSA grows tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

This makes HSAs not only a powerful way to save for healthcare costs but also a significant long-term investment vehicle, especially if you can afford to pay for current medical expenses out-of-pocket and let the HSA grow.

Education Savings Plans

Planning for education expenses can also offer tax benefits.

- 529 Plans: While contributions to 529 plans aren’t deductible at the federal level, many states offer a state income tax deduction or credit for contributions. Earnings within a 529 plan grow tax-free, and withdrawals are tax-free when used for qualified education expenses.

- Coverdell Education Savings Accounts (ESAs): Similar to 529 plans, contributions are not federally deductible, but earnings and withdrawals are tax-free when used for qualified education expenses. ESAs offer more investment flexibility but have lower contribution limits and income restrictions.

Exploring Tax Credits and Other Income-Reducing Strategies

Beyond deductions and tax-advantaged accounts, tax credits and more advanced financial strategies can further reduce your tax liability and, in some cases, effectively lower your taxable income by direct reduction of tax owed.

Understanding Tax Credits

Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of tax you owe, dollar for dollar. A $1,000 credit reduces your tax bill by $1,000. Some credits are refundable, meaning you can get money back even if it exceeds your tax liability, while others are non-refundable.

Common Credits

Many credits are designed to help specific demographics or encourage certain behaviors:

- Child Tax Credit: A significant credit for families with qualifying children, offering up to $2,000 per child, with up to $1,600 being refundable for 2023.

- Earned Income Tax Credit (EITC): A refundable credit for low-to-moderate-income working individuals and families, particularly those with children. Its value depends on income, filing status, and number of children.

- Education Credits:

- American Opportunity Tax Credit (AOTC): A partially refundable credit for undergraduate students during their first four years of higher education.

- Lifetime Learning Credit (LLC): A non-refundable credit for tuition and related expenses for undergraduate, graduate, and professional degree courses, or courses taken to acquire job skills.

- Dependent Care Credit: For expenses incurred caring for a child under 13 or an incapacitated dependent while you work or look for work.

Income Shifting and Tax Loss Harvesting

More advanced strategies can also play a role:

- Income Shifting: This involves moving income to a family member in a lower tax bracket. A classic example is employing your child in your small business and paying them a reasonable wage. The income is taxed at their lower rate, and they can even contribute to a Roth IRA, making it a powerful long-term wealth-building strategy.

- Tax Loss Harvesting: This involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. If you have capital losses exceeding capital gains, you can deduct up to $3,000 of those losses against your ordinary income in a given year, carrying forward any remaining losses to future years. This strategy doesn’t reduce your taxable income directly but reduces your net capital gains, which are part of your taxable income, and can offset other income.

Maximizing Benefits of Tax-Efficient Investments

Beyond traditional savings, certain investment vehicles are inherently more tax-efficient:

- Municipal Bonds: Interest earned on municipal bonds issued by state and local governments is typically exempt from federal income tax and, in some cases, state and local taxes as well, making them attractive for high-income earners.

- Long-Term Capital Gains: Investments held for more than one year are subject to long-term capital gains tax rates, which are often lower than ordinary income tax rates. Strategically holding investments for the long term can reduce your overall tax burden compared to frequent trading.

The Role of Planning and Professional Guidance

Successfully reducing your taxable income isn’t a one-time event; it’s an ongoing process that benefits immensely from forethought and, for many, expert advice.

Proactive Tax Planning Throughout the Year

Waiting until tax season to consider these strategies is often too late. Effective tax planning is a year-round endeavor. Regularly reviewing your financial situation, understanding upcoming life changes (marriage, children, new job, starting a business), and adjusting your contributions to tax-advantaged accounts can make a substantial difference. Consider scheduling an annual “tax check-up” to assess your deductions, credits, and contribution limits.

When to Seek Professional Advice

While this article provides a comprehensive overview, the nuances of tax law can be complex and are highly individualized. A qualified tax professional – such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA) – can offer personalized advice tailored to your specific financial situation. They can help you identify overlooked deductions, optimize your investment strategies for tax efficiency, navigate complex business tax situations, and ensure you remain compliant with all tax regulations. Their fees can often be offset by the tax savings they help you achieve.

Keeping Meticulous Records

Regardless of whether you use a professional or do your taxes yourself, meticulous record-keeping is non-negotiable. Keep organized records of all income, expenses, charitable donations, medical bills, investment statements, and any other documents relevant to your financial activities. Digital copies, cloud storage, and dedicated expense tracking apps can simplify this process and ensure you have all necessary documentation in case of an audit.

Conclusion

Reducing your taxable income is a foundational pillar of sound financial management. By strategically leveraging deductions, maximizing contributions to tax-advantaged accounts, understanding and claiming applicable tax credits, and exploring more sophisticated income-reducing strategies, you can legally and ethically minimize your tax liability. This isn’t just about saving money in the short term; it’s about empowering your long-term financial goals, from building a robust retirement fund to funding education or achieving financial independence. Remember, effective tax planning is an ongoing commitment that thrives on proactive engagement and, when appropriate, professional guidance. Embrace these strategies, and take control of your financial future by keeping more of what you earn.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.