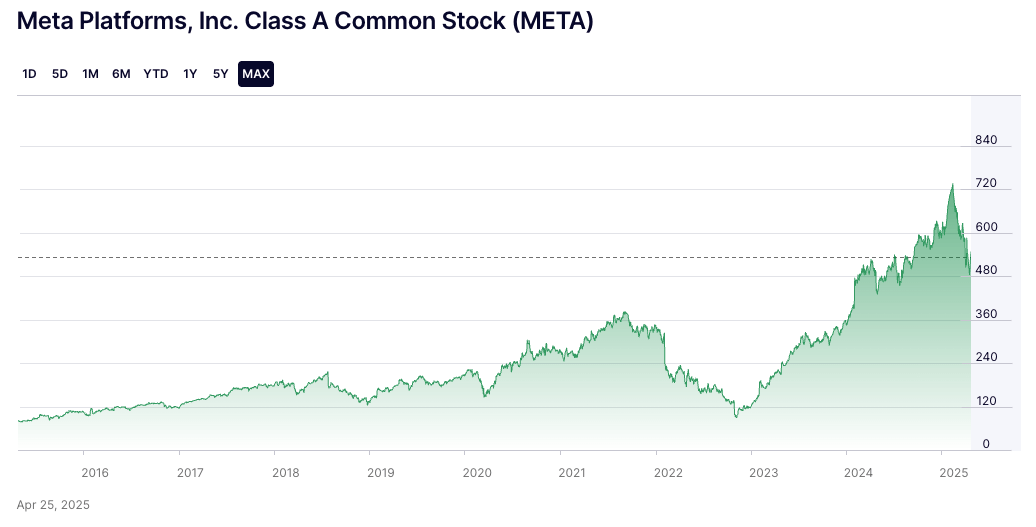

Meta Platforms, Inc. (META), once a darling of the growth stock market and a member of the elite FAANG group, has experienced significant volatility and substantial declines in its stock price over recent periods. While daily fluctuations are a norm in the stock market, a sustained downtrend or a dramatic drop on a particular day usually signals deeper concerns rooted in a confluence of macroeconomic headwinds, company-specific challenges, and shifting investor sentiment. Understanding why Meta’s stock has been under pressure requires a multi-faceted examination of its business finance, market positioning, and strategic bets.

Macroeconomic Headwinds and Investor Sentiment Shift

The broader economic environment plays a crucial role in the valuation and performance of all stocks, and Meta is no exception. A significant portion of Meta’s struggles can be attributed to a macro-level shift that has re-rated growth stocks across the board.

Rising Interest Rates and Inflationary Pressures

Central banks globally have embarked on aggressive interest rate hikes to combat persistent inflation. Higher interest rates make future earnings less valuable in present terms, impacting the discounted cash flow (DCF) models used to value growth companies like Meta, which are priced based on their long-term potential. Investors become more risk-averse, opting for safer assets or companies with more immediate profitability and stronger balance sheets. This environment puts pressure on companies that require significant capital expenditure or have long-term, uncertain bets, as their cost of capital increases, and the patience for future returns diminishes.

Recession Fears and Advertising Spend Contraction

The specter of a global recession looms large, leading to belt-tightening among consumers and, critically for Meta, advertisers. As businesses anticipate slower economic activity, they often cut discretionary spending, with marketing and advertising budgets frequently being among the first to be reduced. Since Meta’s core business relies almost entirely on advertising revenue across Facebook, Instagram, Messenger, and WhatsApp, any significant downturn in advertising spend directly impacts its top line. Brands become more selective, prioritizing proven channels over experimental or less efficient ones, which intensifies competition and squeezes Meta’s ad pricing.

Shifting Investor Appetites

For years, the market rewarded growth at any cost, often overlooking profitability in favor of user acquisition and revenue expansion. However, the current economic climate has triggered a pivot towards profitability, free cash flow, and strong fundamentals. Investors are now scrutinizing balance sheets and demanding evidence of efficient capital allocation. Meta’s substantial investments in its Reality Labs division, which is currently a significant money-loser, contrast sharply with this new investor preference, causing many to question the prudence of such large, speculative expenditures in the short to medium term.

Meta-Specific Operational and Strategic Challenges

Beyond macroeconomic factors, Meta faces several internal and industry-specific hurdles that have weighed heavily on its stock performance. These challenges touch upon its core advertising business and its ambitious, yet costly, pivot to the metaverse.

Core Business Pressures: Advertising Slowdown and Competition

Meta’s advertising engine, once an unassailable behemoth, is encountering unprecedented headwinds.

Apple’s App Tracking Transparency (ATT)

Apple’s privacy changes, particularly the App Tracking Transparency (ATT) framework introduced in iOS 14.5, severely hampered Meta’s ability to track users across apps and websites. This change reduced the effectiveness of personalized advertising, making it harder for advertisers to target specific demographics and measure campaign performance. Meta estimated this single change would cost it billions in revenue, forcing it to invest heavily in new ad measurement and targeting technologies, which have yet to fully compensate for the impact.

Intensified Competition from TikTok

TikTok has emerged as a formidable competitor, particularly for younger audiences and short-form video content. This has led to a significant shift in user attention and, consequently, advertising dollars. Meta’s response, through Instagram Reels, has shown promise but requires substantial investment and effort to compete effectively, potentially cannibalizing attention from its higher-monetizing traditional feeds. The battle for user engagement directly translates to a battle for ad revenue, putting pressure on Meta’s market share and growth prospects.

Decelerating Ad Market Growth

Even without specific competitive pressures, the overall digital advertising market has seen a slowdown in growth, exacerbated by the macroeconomic climate. Advertisers are more cautious, demanding higher ROI, and spreading their budgets across a wider array of platforms, diminishing Meta’s historical dominance.

The Metaverse Bet: Reality Labs Investment

Meta’s aggressive pivot towards building the metaverse, spearheaded by its Reality Labs (RL) division, is perhaps the most significant and controversial factor influencing its stock.

Massive Capital Expenditures and Operating Losses

Reality Labs has been a significant drain on Meta’s profitability. The company has consistently reported billions in operating losses for this division each quarter. These investments include research and development for virtual and augmented reality hardware (like the Quest headsets) and software platforms. While the long-term vision may be transformative, the immediate financial impact is a substantial reduction in overall company profitability and free cash flow.

Long-Term, Uncertain Returns

Investors typically prefer clear pathways to profitability. The metaverse, by Meta’s own admission, is a multi-year, multi-decade bet with highly uncertain returns. The technological hurdles are immense, user adoption is nascent, and the commercial viability of a fully realized metaverse is still speculative. This extended timeline and high risk aversion among current investors means that the market is struggling to assign a reasonable valuation to these future, ethereal returns, leading to a discount on the stock today. The sheer scale of investment without a clear short-to-medium term payback has been a major point of contention for analysts and shareholders.

Earnings Reports and Guidance Misses

Specific financial results and forward-looking guidance have often served as catalysts for sharp declines in Meta’s stock. When the company reports earnings that miss analyst expectations or issues conservative guidance, it signals that the underlying operational challenges are having a more severe impact than anticipated.

Declining Revenue Growth and Profitability

Meta has, in some quarters, reported its first-ever year-over-year revenue declines, a stark contrast to its historical hyper-growth trajectory. Coupled with escalating costs from Reality Labs and other operational expenses, this has led to significant drops in net income and earnings per share (EPS). For a company previously valued for its consistent, robust growth, any sign of contraction or deceleration is met with severe market punishment.

Increased Capital Expenditures

The company’s commitment to building the metaverse also necessitates massive capital expenditures (CapEx) for data centers, servers, and other infrastructure. While necessary for future growth, these investments reduce free cash flow and increase perceived risk, especially when the returns on these investments are not yet clear or realized. Analysts scrutinize these figures closely, often reacting negatively to rising CapEx that isn’t immediately tied to demonstrable revenue growth.

Valuation and Market Expectations Re-calibration

Meta’s stock has undergone a significant re-rating, moving from a premium valuation typically associated with high-growth tech companies to one that reflects its mature core business and speculative future bets.

Shrinking Price-to-Earnings (P/E) Multiples

Historically, Meta commanded a high P/E ratio, reflecting its strong growth prospects. As growth has slowed and profitability has been impacted by metaverse investments, its P/E multiple has compressed significantly. This compression is a re-evaluation by the market, indicating that investors are no longer willing to pay a premium for Meta’s earnings given the current challenges and uncertainties.

Discount for Uncertainty

The market applies a “discount for uncertainty” to companies with significant unproven ventures. The sheer scale of Meta’s metaverse ambition, combined with its current unprofitability, creates a large pool of uncertainty. Investors often prefer to wait until there is more clarity on the path to profitability or a proven track record of adoption before fully valuing these endeavors. This discount explains why even if the core advertising business remains highly profitable, the combined entity’s valuation struggles under the weight of Reality Labs.

The Road Ahead: Path to Recovery or Continued Volatility?

The trajectory of Meta’s stock depends on several factors, including the global economic outlook, the company’s ability to navigate its core business challenges, and the eventual realization of its metaverse vision.

Potential Catalysts for Recovery

A rebound could be triggered by several developments. An improvement in the macroeconomic environment, leading to a resurgence in advertising spending, would immediately boost Meta’s top line. Successful product innovations in its core apps that drive user engagement and monetization, particularly with Reels, could also provide a lift. Furthermore, any indication that Reality Labs is becoming more capital-efficient, showing signs of broader consumer adoption for its VR/AR products, or outlining a clearer path to profitability for the metaverse could alleviate investor concerns. Strategic cost-cutting measures beyond Reality Labs would also be welcomed by the market.

Continued Scrutiny and Long-Term Outlook

However, Meta will continue to face intense scrutiny regarding its capital allocation, particularly for Reality Labs. Regulatory pressures around data privacy, antitrust, and content moderation also remain an ongoing risk that could impact its operations and financial performance. For long-term investors, the question revolves around whether the metaverse bet will ultimately pay off and whether Meta can sustain its core advertising business in an increasingly competitive and privacy-conscious world. The path for Meta’s stock is likely to remain volatile as the market weighs the formidable challenges against the potentially transformative, but distant, rewards of its strategic pivot.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.