Budgeting is often presented as a cornerstone of sound financial management, yet its practical application can sometimes feel daunting. One of the most common questions individuals grapple with is not whether to budget, but how often they should engage in this critical financial exercise. Is it a weekly chore, a monthly ritual, or an annual deep dive? The truth is, there’s no single, universally prescriptive answer, as the optimal budgeting frequency is deeply personal, evolving with individual circumstances, financial goals, and comfort levels. However, understanding the nuances of different approaches can help you forge a budgeting habit that is both effective and sustainable, transforming it from a dreaded task into an empowering tool for financial freedom.

The Foundational Importance of Consistent Budgeting

Before delving into the “how often,” it’s crucial to reinforce the “why.” A budget is far more than just a spreadsheet; it’s a strategic roadmap for your money, illuminating where your income goes and empowering you to make conscious decisions about spending, saving, and investing. Its power lies not just in its creation, but in its consistent application and review.

Beyond Just Tracking: The Purpose of a Budget

Many people view budgeting merely as a way to track past expenses. While expense tracking is an essential component, a truly effective budget is forward-looking. It sets limits, allocates funds to specific categories, and aligns your daily spending with your long-term financial aspirations. It helps you:

- Understand your cash flow: Knowing exactly how much comes in and goes out, and when.

- Identify overspending: Pinpointing areas where you might be unconsciously eroding your savings or incurring debt.

- Prioritize financial goals: Allocating funds to debt repayment, emergency savings, investments, or specific purchases like a home or a vacation.

- Reduce financial stress: Gaining a sense of control over your money alleviates anxiety and uncertainty.

- Make informed decisions: Whether it’s a major purchase or a spontaneous outing, a budget provides the context for responsible choices.

Without regular engagement, a budget quickly becomes stale and irrelevant. Life happens, expenses change, and priorities shift. Consistent budgeting ensures your financial plan remains a living document, reflective of your current reality and future ambitions.

Common Misconceptions About Budgeting

The resistance many feel towards budgeting often stems from pervasive misconceptions. Some believe it’s only for those struggling financially, or that it restricts freedom and joy. In reality:

- It’s not about deprivation: A well-crafted budget allows for discretionary spending and treats, ensuring you enjoy life while staying on track.

- It’s for everyone: From high-income earners to those just starting their financial journey, everyone benefits from understanding and managing their money.

- It’s not a one-time fix: Budgeting is an ongoing process, not a destination. Its effectiveness compounds over time with consistent attention.

- It doesn’t have to be complicated: Modern tools and simplified methods make budgeting accessible to all, regardless of financial literacy.

Overcoming these misconceptions is the first step towards embracing a consistent budgeting rhythm that genuinely serves your financial well-being.

Determining Your Ideal Budgeting Frequency

The “how often” of budgeting isn’t a fixed schedule but a dynamic cadence influenced by various factors. While the common wisdom points to monthly budgeting, it’s beneficial to consider a multi-tiered approach that incorporates different frequencies for different purposes.

The Monthly Standard: Why It Works for Many

For the vast majority of people, a monthly budget review forms the backbone of their financial management. This is largely because most incomes (salaries, rent payments) and recurring expenses (mortgage/rent, utilities, loan payments) are structured on a monthly cycle.

- Alignment with Pay Cycles: Most people are paid bi-weekly or monthly, making a monthly aggregation of income and expenses natural.

- Recurring Expenses: Monthly bills are easier to track and allocate funds for within a monthly framework.

- Strategic Overview: A month provides a good timeframe to assess spending patterns, adjust categories, and project future cash flow without getting bogged down in daily minutiae.

- Goal Tracking: Monthly check-ins allow you to see progress towards your savings and debt repayment goals.

A robust monthly budget involves reviewing the previous month’s actual spending against your planned budget, updating income projections for the upcoming month, allocating funds, and setting new mini-goals.

Weekly Check-ins: When and Why They’re Beneficial

While the monthly budget sets the overarching plan, weekly check-ins offer a more granular level of control, especially for those who are new to budgeting, managing variable income, or actively working on curbing impulse spending.

- Mid-Month Adjustments: Catching overspending early in a weekly review allows for mid-course corrections before the month is over.

- Transaction Reconciliation: Quickly reviewing transactions helps identify errors, fraud, or forgotten subscriptions.

- Mindful Spending: For those prone to impulse buys, a weekly check-in provides an opportunity to reflect on recent purchases and adjust behavior for the remainder of the week.

- Variable Income/Expenses: If your income fluctuates (e.g., freelancers, commission-based sales) or you have significant variable expenses, weekly tracking can prevent unpleasant surprises.

Think of weekly check-ins as the tactical execution of your monthly strategy, ensuring you stay on track day-to-day.

Quarterly Reviews: For Strategic Adjustments

Beyond the operational monthly and weekly rhythms, quarterly budget reviews offer a crucial opportunity to step back and assess your financial plan from a broader perspective.

- Seasonal Changes: Expenses often fluctuate seasonally (e.g., holiday spending, increased utility bills in winter/summer, back-to-school costs). Quarterly reviews allow you to anticipate and adjust for these.

- Mid-Year Goals: Assess progress towards larger, longer-term goals (e.g., saving for a down payment, a major vacation).

- Subscription Audits: A perfect time to review all recurring subscriptions and cancel those no longer needed.

- Minor Life Changes: Adjustments for minor changes in income, new recurring expenses, or shifts in priorities.

These reviews are less about individual transactions and more about the effectiveness of your overall budget framework and its alignment with your evolving life.

Annual Overhauls: Big Picture Financial Planning

Finally, an annual budget overhaul is essential. This is more than just a review; it’s a comprehensive re-evaluation of your entire financial landscape.

- Major Life Events: Reflect on significant changes from the past year (new job, marriage, birth of a child, home purchase) and project how potential future events might impact your finances.

- Long-Term Goals: Re-evaluate your retirement savings, investment strategy, and other long-term financial aspirations.

- Income & Expense Projections: Create a fresh projection for the upcoming year, taking into account raises, bonuses, new debts, or significant planned expenses.

- Insurance & Debt Review: A good time to review insurance policies for adequacy and shop for better rates, and to strategize debt repayment.

- Net Worth Calculation: A comprehensive annual review should include an update of your net worth statement.

This annual “reset” ensures your budget remains agile and continues to serve your most ambitious financial goals over the long haul.

Factors Influencing Your Budgeting Cadence

While the multi-tiered approach provides a solid framework, the ideal implementation is highly personalized. Several factors will dictate which frequencies you lean on most heavily.

Income Volatility and Expense Fluctuations

Individuals with stable, predictable incomes and fixed expenses might find a monthly review sufficient, complemented by lighter weekly checks. Conversely, those with variable income (freelancers, gig workers, commission-based roles) or highly fluctuating expenses (e.g., project-based spending, frequent travel) will benefit immensely from more frequent, perhaps even daily, check-ins to manage cash flow actively. The less predictable your financial landscape, the more often you’ll need to touch base with your budget.

Personal Financial Goals and Life Stages

Your financial goals play a significant role. If you are aggressively saving for a down payment, paying off high-interest debt, or trying to break a cycle of overspending, more frequent engagement will keep your goals top of mind and help you make quicker adjustments. Someone nearing retirement with robust savings might only need quarterly or annual strategic reviews.

- Early Career/High Debt: More frequent (weekly/bi-weekly)

- Mid-Career/Family Building: Monthly with quarterly deep dives

- Nearing Retirement/Wealth Preservation: Monthly/Quarterly with annual overhauls

Life stages also dictate needs. A college student managing limited funds will need a different approach than a working parent with diverse expenses or an empty-nester focused on legacy planning.

Your Relationship with Money and Financial Discipline

How you personally interact with money is a critical factor.

- Discipline Level: If you are naturally disciplined and track spending mentally or intuitively, less frequent formal budgeting might suffice. If you tend to lose track of spending or struggle with impulse control, more frequent checks (daily or weekly) can provide the necessary guardrails.

- Interest Level: Some people genuinely enjoy managing their money; others find it a chore. For the latter, finding the minimum effective frequency that prevents financial drift is key. For the former, more frequent engagement might be enjoyable and lead to greater insights.

- Stress & Anxiety: If thinking about money causes stress, it might be counter-intuitive, but regular, brief check-ins can actually reduce anxiety by providing clarity and control, rather than letting unknowns fester.

Ultimately, your budgeting frequency should be a tool that empowers you, not a source of stress. Find a rhythm that you can realistically maintain.

The Tools You Use: Digital vs. Manual

The chosen budgeting tools can significantly impact your ideal frequency.

- Manual Budgeting (Spreadsheets, Notebooks): These often require more time and effort to update, making less frequent (e.g., weekly or bi-weekly) comprehensive reviews more practical.

- Digital Budgeting Apps (Mint, YNAB, Personal Capital): Many apps automatically categorize transactions and provide real-time updates. This automation allows for daily or bi-daily glances at your financial picture with minimal effort, making more frequent “check-ins” less burdensome and highly effective. They can also send alerts for overspending, further integrating budgeting into your daily life.

Leveraging technology can transform budgeting from a dreaded task into a seamless, integrated part of your financial routine, making higher frequencies more feasible and beneficial.

Implementing and Maintaining an Effective Budget

Once you’ve determined your ideal frequency, the next step is consistent implementation. The best budget is the one you actually use.

Choosing the Right Budgeting Method

There isn’t one perfect method, but choosing one that resonates with you will boost adherence.

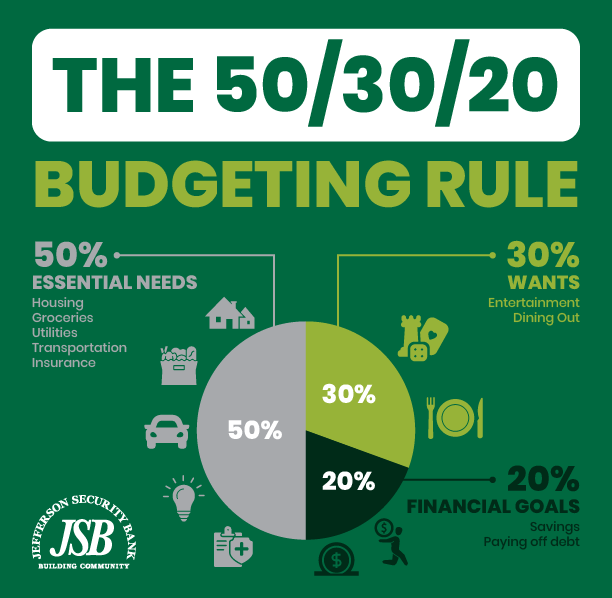

- 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt repayment. Simple and effective for general guidance.

- Zero-Based Budgeting: Every dollar is assigned a job, ensuring no money is left unaccounted for. Ideal for those who want tight control.

- Envelope System: A cash-based system where money for different categories is physically separated into envelopes. Great for visual learners and those prone to overspending on certain categories.

- Paycheck to Paycheck Budgeting: Focusing on what you have until the next paycheck. Useful for variable income or those building a buffer.

Match the method to your personality and financial situation for maximum impact.

Automating Your Financial Management

Automation is your best friend in maintaining budgeting consistency.

- Automatic Transfers: Set up automatic transfers from your checking account to savings, investment, and debt repayment accounts immediately after you get paid. This “pays yourself first” approach ensures your financial goals are prioritized.

- Bill Pay: Schedule recurring bills to be paid automatically, reducing the risk of late fees and simplifying monthly reconciliation.

- Budgeting Apps: Utilize apps that link to your bank accounts, categorize transactions, and provide real-time updates. These tools significantly reduce the manual effort required for daily or weekly monitoring.

Automation ensures that even when life gets hectic, your financial plan continues to progress.

The Art of Adjustment: When to Pivot Your Budget

No budget is static. Life is dynamic, and your budget must be too.

- Regular Reviews: Use your weekly, monthly, and quarterly reviews to identify discrepancies between planned and actual spending.

- Embrace Flexibility: Don’t be afraid to adjust categories. If you consistently overspend on dining out, either cut back or reallocate funds from a less critical category. If a category is consistently underspent, perhaps those funds can be redirected to savings or debt.

- Respond to Life Changes: A new job, a raise, a new baby, an unexpected expense – all these warrant a fresh look at your budget. Proactive adjustment prevents financial derailment.

- Don’t Strive for Perfection: The goal isn’t a perfectly adhered-to budget every single period, but rather consistent engagement and improvement. Learn from your budget, don’t let it become a source of guilt.

The ability to pivot and adapt is a hallmark of effective, long-term financial management.

The Long-Term Benefits of Consistent Budgeting

Regardless of your chosen frequency, the sustained habit of budgeting yields profound and lasting benefits that extend far beyond simply having more money.

Achieving Financial Milestones

Consistent budgeting provides the clarity and control needed to systematically work towards and achieve your financial milestones. Whether it’s building an emergency fund, paying off student loans, saving for a down payment on a home, funding a child’s education, or securing a comfortable retirement, each budgeted dollar is a step closer to these significant accomplishments. Without a budget, these goals often remain distant dreams; with it, they become actionable plans.

Reducing Financial Stress

One of the most immediate and impactful benefits of regular budgeting is a significant reduction in financial stress. Uncertainty about money is a leading cause of anxiety. A budget removes that uncertainty, replacing it with a clear picture of your financial situation. Knowing where your money comes from, where it goes, and what it’s doing for you creates a powerful sense of control and peace of mind. You’re no longer reacting to financial surprises but proactively managing your resources.

Building Lasting Wealth

Ultimately, consistent budgeting is a powerful engine for building lasting wealth. It fosters habits of saving, wise spending, and strategic investing. It helps you avoid debt, maximize your income’s potential, and make conscious choices that align with your long-term prosperity. Over time, these consistent small actions accumulate, leading to significant financial growth and security. A budget isn’t just about managing today’s money; it’s about shaping tomorrow’s financial future.

In conclusion, the question of “how often should you create a budget” is best answered by recognizing the need for a layered approach. A comprehensive annual overhaul, strategic quarterly reviews, detailed monthly planning, and tactical weekly or even daily check-ins each serve a unique purpose. Your ideal rhythm will depend on your personal circumstances, financial goals, and comfort level with managing money. By finding a consistent, sustainable frequency and leveraging appropriate tools, you can transform budgeting from a periodic chore into an indispensable habit that empowers you to take control of your financial destiny and build the life you envision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.