Budgeting isn’t merely about restricting your spending; it’s a fundamental pillar of personal finance, a powerful tool that empowers you to take control of your money, achieve your financial aspirations, and ultimately, build a more secure and prosperous future. For many, the idea of budgeting conjures images of complex spreadsheets and stringent cutbacks, but in reality, it’s a dynamic and adaptable process tailored to your unique circumstances and goals. This guide will demystify budgeting, offering practical strategies, insightful frameworks, and actionable steps to help you master the art of managing your money effectively.

Understanding the ‘Why’ Behind Budgeting

Before diving into the mechanics, it’s crucial to grasp the profound benefits that budgeting offers. Understanding the ‘why’ can provide the motivation needed to commit to this essential financial habit.

The Power of Financial Clarity

One of the most immediate benefits of budgeting is the unparalleled clarity it provides regarding your financial situation. Many people operate on autopilot, with money flowing in and out without a clear understanding of its destination. A budget forces you to confront your income and expenditures head-on, revealing exactly where your money goes each month. This transparency is the first step towards informed decision-making, allowing you to identify unnecessary spending, allocate funds more strategically, and eliminate the guesswork from your financial life. It’s like turning on the lights in a dark room – suddenly, you can see everything clearly.

Achieving Your Financial Goals

Whether your dream is to buy a house, save for retirement, pay off debt, fund a child’s education, or simply take a dream vacation, a budget is the roadmap that gets you there. Without a clear understanding of your cash flow, setting and achieving financial goals becomes a struggle. Budgeting allows you to earmark specific amounts for your objectives, transforming abstract desires into concrete targets. It helps you prioritize, ensuring that your spending aligns with your long-term vision, rather than being dictated by impulse or fleeting wants. Every dollar allocated towards a goal is a step closer to realizing it.

Reducing Stress and Building Security

Financial stress is a pervasive issue, often stemming from a feeling of being out of control. Budgeting instills a sense of mastery over your finances, significantly reducing anxiety related to bills, unexpected expenses, or simply wondering if you have enough. By creating a financial plan, you build a robust safety net. You’ll know you have funds set aside for emergencies, for future investments, and for enjoying life responsibly. This proactive approach to money management fosters a profound sense of security and peace of mind, freeing you to focus on other aspects of your life without the constant shadow of financial worry.

Essential Budgeting Methods and Frameworks

There isn’t a one-size-fits-all approach to budgeting. Different methods suit different personalities, incomes, and financial complexities. Exploring various frameworks can help you find the system that best resonates with you and your financial lifestyle.

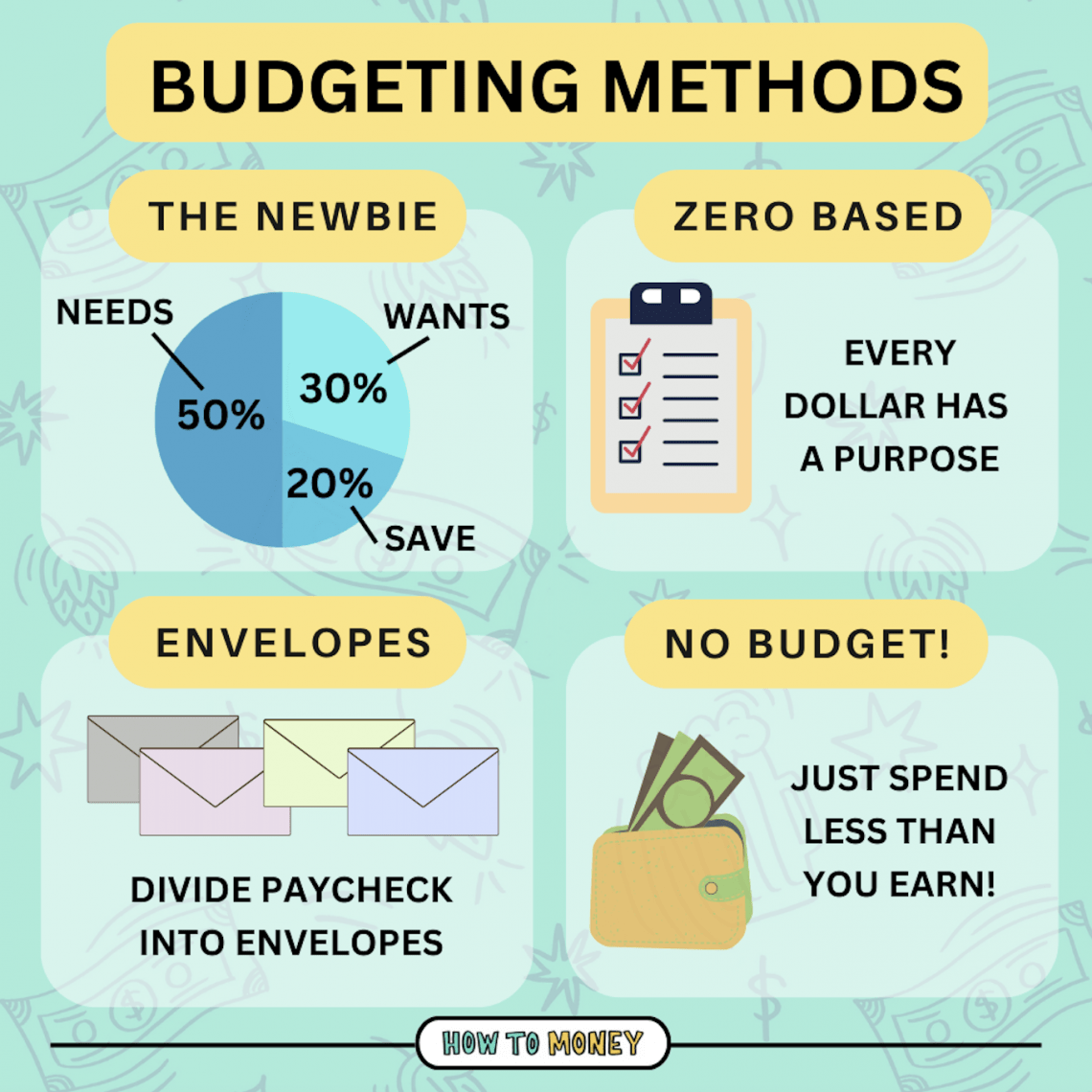

The 50/30/20 Rule: A Simple Approach

Popularized by Senator Elizabeth Warren, the 50/30/20 rule is an excellent starting point for those new to budgeting due to its simplicity. It suggests allocating your after-tax income into three broad categories:

- 50% for Needs: This includes essential expenses like housing (rent/mortgage), utilities, groceries, transportation, insurance, and minimum loan payments.

- 30% for Wants: This category covers discretionary spending that enhances your quality of life but isn’t strictly necessary for survival. Examples include dining out, entertainment, hobbies, vacations, and shopping for non-essentials.

- 20% for Savings & Debt Repayment: This portion is dedicated to building your financial future, including emergency funds, retirement contributions, investments, and accelerating debt repayment beyond the minimums.

This rule provides a flexible yet structured guideline, making it easy to implement without micromanaging every penny.

Zero-Based Budgeting: Every Dollar Has a Job

Zero-based budgeting (ZBB) is a meticulous method where every dollar of your income is assigned a purpose. The goal is that your income minus your expenses should equal zero. This doesn’t mean you spend all your money; rather, it means every dollar is accounted for – whether it’s allocated to bills, savings, debt, or discretionary spending. ZBB requires you to plan for every single expense, leaving no money unaccounted for. This method provides maximum control and ensures that your financial resources are intentionally directed. It’s particularly effective for those who want to be very precise with their spending and savings.

Envelope System: Tangible Control for Cash Spenders

For those who prefer a more tactile approach or struggle with overspending on credit cards, the envelope system is a classic and highly effective method. After allocating funds to different spending categories (e.g., groceries, entertainment, dining out), you physically withdraw cash for each category and place it into separate envelopes. Once an envelope is empty, you stop spending in that category until the next budgeting period. This system provides a tangible limit, making you acutely aware of how much you have left to spend and preventing impulse purchases. While typically used with cash, a digital version can be simulated with budgeting apps that allow you to create virtual “envelopes” or categories.

Pay Yourself First: Prioritizing Savings

While not a complete budgeting system in itself, the “Pay Yourself First” principle is a powerful mindset that can be integrated into any budgeting method. It advocates for prioritizing savings and investments by automatically transferring a predetermined amount from your paycheck into a savings or investment account before you pay any bills or engage in discretionary spending. This ensures that your financial goals are consistently met, rather than relying on leftover funds at the end of the month, which often never materialize. It shifts savings from an afterthought to a priority, fostering consistent wealth accumulation.

Practical Steps to Create Your Budget

Once you’ve chosen a method, the next step is to put it into action. Creating a budget involves several practical, sequential steps that transform a conceptual framework into a working financial plan.

Track Your Income and Expenses

The foundational step for any budget is to understand your actual cash flow.

- Income: Accurately list all your sources of income, including your net take-home pay, freelance earnings, rental income, etc. Calculate your total monthly income.

- Expenses: This is where many people get tripped up. For at least one month, meticulously track every single expense. Use bank statements, credit card statements, receipts, or budgeting apps. Categorize these expenses as fixed (e.g., rent, loan payments, insurance premiums) or variable (e.g., groceries, entertainment, utilities, dining out). This tracking phase is critical for painting an honest picture of your spending habits and identifying areas for potential adjustment.

Categorize Your Spending

After tracking, group your expenses into meaningful categories. Common categories include housing, transportation, food (groceries vs. dining out), utilities, debt payments, insurance, personal care, entertainment, savings, and miscellaneous. The level of detail in categorization can vary; some prefer broad categories, while others like granular breakdowns. The key is to create categories that make sense to you and provide actionable insights into your spending patterns.

Set Realistic Spending Limits

Based on your income and tracked expenses, assign a specific spending limit to each category. This is where your chosen budgeting method (e.g., 50/30/20, zero-based) comes into play. Be realistic. If you cut too much too soon, you’re likely to get discouraged and abandon the budget. Start with minor adjustments and gradually tighten the reins as you become more comfortable. Ensure that your total allocated expenses, plus savings and debt repayment, do not exceed your total income. If they do, you’ll need to make tough decisions about reducing discretionary spending or finding ways to increase income.

Automate Savings and Bill Payments

Automation is your best friend in budgeting. Set up automatic transfers from your checking account to your savings or investment accounts immediately after payday (embracing the ‘Pay Yourself First’ principle). Similarly, automate bill payments for fixed expenses like rent, loan installments, and insurance. This ensures that essential payments are never missed, avoids late fees, and consistently builds your savings without requiring conscious effort each month.

Regularly Review and Adjust Your Budget

A budget is not a static document; it’s a living financial plan that needs regular attention. At least once a month, review your budget to see how your actual spending compares to your planned spending.

- Are you consistently overspending in certain categories? Why?

- Are there categories where you consistently have money left over?

- Have your income or fixed expenses changed?

- Are you on track to meet your financial goals?

Make adjustments as necessary. Life circumstances change, and your budget should evolve with them. Flexibility and adaptability are crucial for long-term budgeting success.

Leveraging Tools and Technology for Budgeting

In the digital age, a wealth of tools and technologies are available to simplify and enhance the budgeting process, making it more efficient and less daunting.

Spreadsheet Templates: DIY Control

For those who enjoy a hands-on approach and spreadsheet literacy, a simple spreadsheet (Excel, Google Sheets) can be a powerful budgeting tool. Numerous free templates are available online, or you can create your own from scratch. Spreadsheets offer complete customization, allowing you to tailor categories, formulas, and visual representations to your exact needs. They require manual input or data export from bank accounts, which can be time-consuming but offers a deep level of engagement with your finances.

Budgeting Apps and Software: Modern Convenience

A vast array of budgeting apps and software has revolutionized personal finance. Tools like Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard automatically link to your bank accounts, credit cards, and investment accounts, pulling in transactions and categorizing them for you. They offer real-time insights into your spending, track your net worth, provide financial goal-setting features, and send alerts for unusual activity or upcoming bills. While some are free and ad-supported, others charge a subscription fee, often justified by their robust features, security, and ad-free experience. These tools significantly reduce the manual effort of tracking and provide comprehensive dashboards for a holistic financial overview.

Online Banking Features: Streamlining Your Finances

Don’t overlook the budgeting capabilities built into your existing online banking platform. Many banks now offer features like spending categorization, graphical breakdowns of your expenditures, financial goal trackers, and alerts for balances or transactions. These integrated tools can be a convenient starting point, especially if you prefer to keep your financial data within your primary banking ecosystem. Additionally, online banking facilitates easy setup of automatic transfers and bill payments, which are cornerstone elements of an effective budget.

Overcoming Common Budgeting Challenges

Budgeting, like any new habit, can present its share of hurdles. Anticipating and addressing these common challenges can significantly improve your chances of long-term success.

Dealing with Irregular Income

For freelancers, commission-based workers, or those with seasonal employment, irregular income can make traditional budgeting feel impossible. The key is to base your budget on your lowest expected monthly income. Treat any income above this baseline as a bonus, using it for extra debt payments, increasing emergency savings, or investing. Creating a “buffer” savings account specifically for lean months can also provide stability. Another strategy is to track income over a longer period (e.g., quarterly or annually) to get a more accurate average.

Handling Unexpected Expenses

Life is unpredictable, and unexpected expenses (car repairs, medical bills, home repairs) can derail even the best-laid budgets. The best defense is a strong offense: an emergency fund. Aim to build up 3-6 months’ worth of living expenses in an easily accessible, high-yield savings account. This fund acts as a financial shock absorber, preventing you from going into debt or disrupting your primary budget when surprises arise. When you use your emergency fund, make replenishing it your top priority.

Staying Motivated and Disciplined

Budgeting requires ongoing discipline, and it’s easy to lose motivation, especially when you feel deprived. To combat this:

- Be Realistic: Don’t cut out all your “wants” immediately. Allow for some discretionary spending to prevent burnout.

- Celebrate Small Wins: Acknowledge your progress. Did you stick to your grocery budget? Did you meet your savings goal for the month? Reward yourself (responsibly, within your budget!).

- Focus on Goals: Regularly revisit your financial goals. Remind yourself why you’re budgeting to reignite your motivation.

- Find a Budget Buddy: Sharing your goals and progress with a trusted friend or partner can provide accountability and encouragement.

Involving Your Household in the Process

If you share finances with a partner or live with family, budgeting is a team sport. Trying to budget alone while others are unaware or unsupportive can lead to friction and failure. Open and honest communication is vital. Hold regular family budget meetings to discuss income, expenses, goals, and any financial challenges. Ensure everyone understands the budget’s purpose and how their individual spending impacts the collective financial health. When everyone is on the same page and working towards common goals, budgeting becomes a shared journey toward financial well-being.

In conclusion, budgeting is a dynamic and empowering process that puts you firmly in the driver’s seat of your financial life. It’s not about deprivation, but about intentionality and alignment between your money and your life goals. By understanding the ‘why,’ choosing the right method, taking practical steps, leveraging modern tools, and overcoming challenges with resilience, you can transform your relationship with money, gain unparalleled clarity, reduce stress, and pave a clear path to financial freedom and lasting security. Start today, and watch your financial future unfold by design, not by default.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.