Securing a small business loan is often the most critical inflection point in an entrepreneur’s journey. Whether you are looking to expand your footprint, purchase essential equipment, or manage seasonal cash flow fluctuations, the infusion of external capital can be the difference between stagnant operations and exponential growth. However, the lending landscape has evolved into a complex ecosystem of traditional institutions, government-backed programs, and digital-first fintech platforms. Navigating this environment requires more than just a good idea; it demands financial literacy, meticulous preparation, and a strategic understanding of how lenders evaluate risk.

Understanding Your Financing Needs and Loan Options

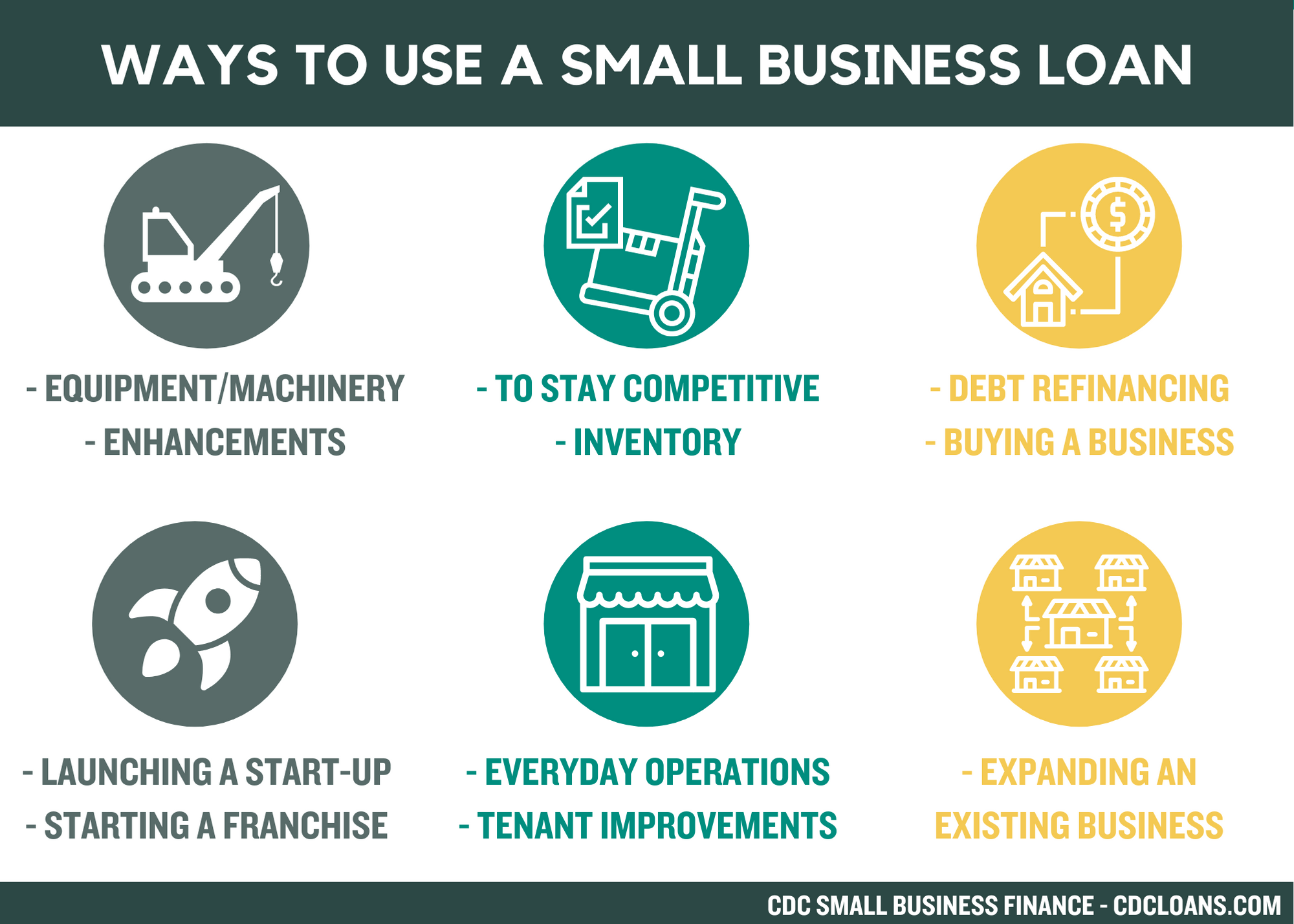

Before approaching a lender, you must have a crystalline understanding of why you need the money and how much you actually require. Over-borrowing can lead to an unmanageable debt service burden, while under-borrowing can leave you mid-project without the funds to complete your objectives.

Assessing Capital Requirements and ROI

Begin by conducting a rigorous internal audit of your financial needs. Are you seeking “working capital” to cover day-to-day operational costs, or “growth capital” for long-term investments? Professional financial management dictates that every dollar borrowed should have a projected Return on Investment (ROI). If you are borrowing at a 7% interest rate to fund an expansion that yields a 15% increase in net profit, the math supports the loan. You should prepare a detailed “Use of Funds” statement that accounts for every dollar, as lenders will scrutinize this to ensure the capital is being deployed into value-generating activities.

Navigating the Spectrum of Loan Products

The “Money” niche offers various vehicles for business finance, each suited to different stages of business maturity:

- Term Loans: The traditional format where you receive a lump sum and repay it with interest over a set period. Best for specific, one-time investments.

- Business Lines of Credit: A flexible option that allows you to draw funds as needed up to a certain limit. You only pay interest on what you use, making this ideal for managing inventory or payroll gaps.

- Equipment Financing: The equipment itself serves as collateral, often allowing for lower interest rates and easier qualification.

- Invoice Factoring: A specialized finance tool where you sell your accounts receivable at a discount to get immediate cash.

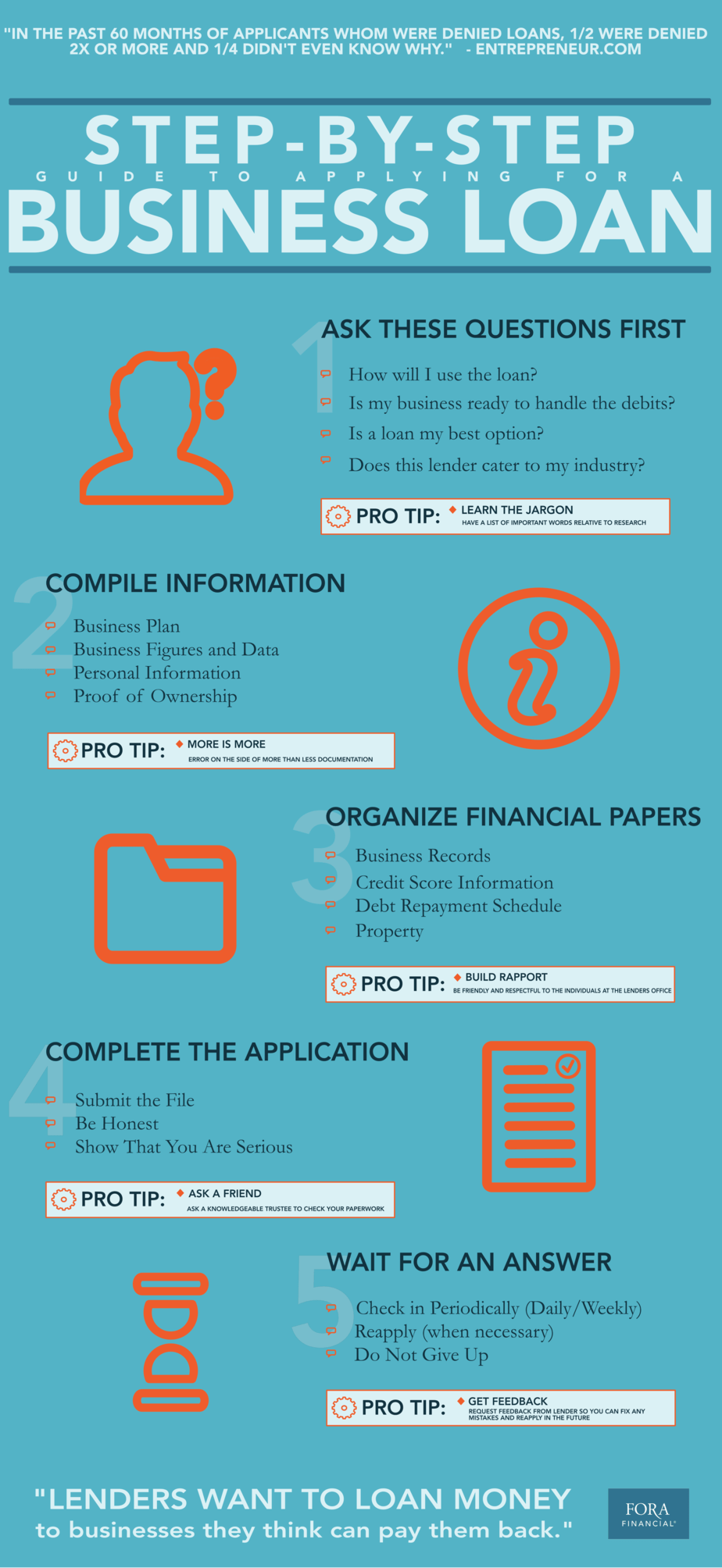

Preparing a Robust Loan Application Package

The difference between an approval and a rejection often lies in the documentation. Lenders look for “The Five C’s of Credit”: Character, Capacity, Capital, Collateral, and Conditions. To demonstrate these, you must compile a package that proves your business is a safe bet.

Evaluating Credit Scores and Financial Health

In the world of business finance, your personal credit history is often just as important as your business credit, especially for Small and Medium Enterprises (SMEs). Lenders typically look for a personal FICO score of 680 or higher for traditional loans. Simultaneously, you should check your business credit reports from bureaus like Dun & Bradstreet or Experian Business. Beyond credit, lenders will evaluate your Debt Service Coverage Ratio (DSCR), which measures your business’s ability to use its operating income to repay all its debt obligations. A DSCR of 1.25 or higher is generally considered healthy.

Essential Financial Statements and Documentation

Expect to provide at least two to three years of both personal and business tax returns. Furthermore, you will need to produce “The Big Three” financial statements:

- Profit and Loss (P&L) Statement: Shows your revenue and expenses over a specific period.

- Balance Sheet: A snapshot of your assets, liabilities, and equity.

- Cash Flow Statement: Demonstrates how cash moves in and out of the business, proving you have the liquidity to make monthly payments.

The Importance of a Solid Business Plan

While financial statements show where you have been, a business plan shows where you are going. A professional business plan for a loan application should include an executive summary, a detailed market analysis, an explanation of the management team’s expertise, and—most importantly—financial projections for the next three to five years. These projections must be realistic and backed by historical data or industry benchmarks. If your plan claims you will triple your revenue in twelve months without a clear explanation of how, lenders will view it as a high-risk red flag.

Identifying the Right Lender for Your Niche

Not all lenders are created equal. The source of your capital will dictate your interest rates, your repayment terms, and the speed at which you receive funds.

Traditional Banks vs. Credit Unions

Traditional commercial banks (like Chase, BofA, or regional banks) offer the lowest interest rates and the most favorable terms. However, they also have the strictest qualification criteria. They prefer businesses with strong collateral, several years of profitability, and a high credit score. Credit unions, being member-owned, can sometimes offer more flexible terms or personalized service, but they often have smaller lending limits than major national banks.

The Role of SBA-Backed Loans

The U.S. Small Business Administration (SBA) does not lend money directly to entrepreneurs. Instead, it guarantees a portion of the loan made by participating lenders. This reduces the risk for the bank, allowing them to provide loans to businesses that might not otherwise qualify.

- SBA 7(a) Loans: The most popular program, used for working capital, debt refinancing, and equipment.

- SBA 504 Loans: Specifically designed for major fixed assets like real estate or long-term machinery.

While SBA loans have excellent rates, the application process is notoriously rigorous and can take several months to finalize.

Fintech and Online Lenders

If speed is your primary concern, online lenders and fintech platforms have revolutionized business finance. These lenders use proprietary algorithms to evaluate risk, often providing approval within 24 to 48 hours. The trade-off for this convenience is usually a higher Annual Percentage Rate (APR) and shorter repayment terms. This is a viable option for businesses that need capital immediately to seize a time-sensitive opportunity but have the cash flow to handle higher monthly payments.

Navigating the Approval and Underwriting Process

Once you submit your application, you enter the underwriting phase. This is where the lender’s team of analysts digs deep into your data to verify everything you have claimed.

Understanding Underwriting and Due Diligence

Underwriting is the process of risk assessment. The lender will verify your bank statements, check for outstanding liens or legal judgments against your business, and potentially appraise any collateral you have offered. During this stage, responsiveness is key. Lenders will often ask for “addendums” or clarifications on specific transactions. Providing this information quickly demonstrates professional management and helps move the process toward “final approval.”

Analyzing the Term Sheet

If the underwriter clears the file, you will receive a term sheet. This is a non-binding document outlining the proposed loan amount, interest rate, fees (such as origination or processing fees), and the repayment schedule. It is vital to look beyond the “sticker price” of the interest rate. Calculate the total cost of capital, including all fees, to understand the true impact on your bottom line. Look specifically for “prepayment penalties”—some lenders charge you a fee if you pay the loan off early, which can be a significant disadvantage if your business sees a sudden windfall.

Closing and Strategic Fund Management

The final step is the closing, where you sign the formal loan agreement and the funds are disbursed—usually via wire transfer. However, the work does not end there. From a financial strategy perspective, the management of these funds is critical. Segregating loan proceeds into a separate account can help you track spending against your original “Use of Funds” statement. Maintaining a flawless repayment history will not only protect your credit score but will also make it significantly easier to secure larger amounts of capital at lower rates in the future.

In conclusion, getting a small business loan is a multifaceted financial maneuver that requires a blend of strategic planning and meticulous record-keeping. By understanding the specific needs of your business, preparing a bulletproof application, and choosing the lender that aligns with your growth stage, you turn debt into a powerful tool for wealth creation. Capital is the fuel for the business engine; securing it effectively is the hallmark of a sophisticated entrepreneur.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.