In the intricate world of personal finance, managing your banking tools effectively is paramount to maintaining both financial security and peace of mind. Your debit card, a direct link to your checking account, is undoubtedly one of your most frequently used financial instruments. However, circumstances may arise where canceling it becomes a necessary, even urgent, action. Whether due to loss, theft, fraud concerns, or simply account management, understanding the proper procedure for canceling your Chase debit card is a fundamental aspect of responsible personal finance.

This guide will walk you through the nuances of debit card cancellation with Chase, ensuring you have the knowledge to act decisively and protect your financial well-being. We will delve into the various reasons for cancellation, detail the practical steps to take, discuss immediate follow-up actions, and explore the broader implications for your personal financial strategy.

Understanding When and Why to Cancel Your Debit Card

The decision to cancel your debit card is often prompted by specific events, each demanding a different level of urgency and consideration. Recognizing these triggers is the first step in protecting your finances.

Loss, Theft, or Suspicious Activity: Immediate Action for Security

This is arguably the most critical scenario requiring immediate action. If your debit card is lost or stolen, or if you notice unauthorized transactions or any suspicious activity on your account, canceling the card instantly is non-negotiable. A lost or stolen card in the wrong hands provides direct access to your checking account funds. Similarly, fraudulent transactions, even small ones, could be indicators of a larger security breach. Time is of the essence in these situations to mitigate potential financial damage and protect yourself from liability. While debit cards offer some fraud protection, acting quickly enhances your chances of recovery and limits your exposure.

Expired or Damaged Cards: Replacing Without Security Concerns

Sometimes, the need for a new card is less urgent. Debit cards have an expiration date, and as this date approaches, Chase will typically send you a new card automatically. However, if your card is damaged, unreadable, or simply not functioning correctly before its expiration, you’ll need to cancel the old one (or rather, disable it and order a replacement) to ensure uninterrupted access to your funds. In these cases, the primary goal isn’t security breach prevention but rather maintaining functionality. While the process might seem similar to a security-related cancellation, the urgency and immediate risk are significantly lower.

Closing Your Account: The Final Step for Account Termination

If you’ve made the decision to close your Chase checking account entirely, canceling the associated debit card is a natural and necessary final step. This ensures that no further transactions can occur on an account you intend to terminate, effectively severing all ties. It’s crucial to confirm all linked services and automatic payments are updated before fully closing the account and canceling the card to avoid any disruptions or unforeseen charges. This scenario is less about immediate threat and more about systematic financial management.

Shifting Banks or Financial Needs: Proactive Financial Management

Perhaps you’ve found a new banking institution that better suits your financial goals, or you’re consolidating accounts. In such instances, canceling your Chase debit card is part of a broader financial transition. It’s a proactive step to streamline your financial tools, reduce unnecessary accounts, and align your resources with your current financial strategy. This decision is driven by foresight and strategic planning rather than reactive damage control. It signifies an intentional choice to reorganize your personal finance ecosystem for greater efficiency or improved benefits.

Navigating the Cancellation Process with Chase

Chase, like most major financial institutions, offers several convenient channels for canceling your debit card. Knowing your options allows you to choose the method that best suits your situation and urgency.

Option 1: Contacting Chase Customer Service Directly

For immediate assistance, especially in cases of loss, theft, or suspected fraud, calling Chase’s customer service line is often the most direct and recommended approach. You’ll speak with a representative who can promptly disable your card and guide you through the next steps, including ordering a replacement and initiating a fraud investigation if necessary.

- Phone Number: Look for the customer service number on the back of your debit card, on your bank statements, or on Chase’s official website. Typically, it’s 1-800-935-9935 for general banking inquiries. For debit card issues, specific fraud lines might be available.

- Information Needed: Be prepared to provide your full name, account number, date of birth, and other identifying information to verify your identity. You’ll also need to explain the reason for cancellation.

- Key Advantage: Direct communication ensures immediate action and allows for questions and clarifications in real-time.

Option 2: Using the Chase Mobile App or Online Banking

For situations that are less urgent, such as a damaged card or a proactive replacement, Chase’s digital platforms offer a convenient self-service option.

- Chase Mobile App:

- Log in to your Chase Mobile app.

- Select the checking account associated with the debit card.

- Look for options like “Manage Card,” “Card Services,” or “Replace/Cancel Card.”

- Follow the prompts to report the card lost/stolen or to order a replacement for a damaged card.

- Chase Online Banking (via Website):

- Log in to your Chase online account at Chase.com.

- Navigate to your checking account summary.

- Find a section usually labeled “Customer Service,” “Account Services,” or “Manage Debit Card.”

- Select the option to report your card lost/stolen or to order a new one.

- Key Advantage: Available 24/7, offering flexibility and control from your own device without needing to speak to a representative. This is particularly useful for reporting a lost card outside of business hours.

Option 3: Visiting a Chase Branch

If you prefer in-person assistance, or if you’re dealing with a complex issue, visiting a local Chase branch can be beneficial.

- Process: Speak with a banker, who can help you cancel your card, order a replacement, and address any other account-related concerns.

- Information Needed: Bring a valid form of identification (e.g., driver’s license, passport) to verify your identity.

- Key Advantage: Provides personalized service and the ability to resolve multiple issues simultaneously, often suitable for closing an account or discussing broader financial strategies.

Essential Information You’ll Need

Regardless of the method you choose, having certain information readily available will expedite the process:

- Your Full Name and Address: As registered with Chase.

- Your Account Number: The checking account number linked to the debit card.

- Date of Birth: For identity verification.

- Social Security Number (SSN) or Taxpayer Identification Number (TIN): May be required for verification.

- The Reason for Cancellation: Be clear and concise about why you’re canceling the card (e.g., lost, stolen, damaged, closing account).

- Date of Last Known Use or Discovery of Loss/Theft: Crucial for fraud investigations.

Immediate Steps After Cancellation for Enhanced Security

Canceling your debit card is a critical first step, but your vigilance shouldn’t end there. Several follow-up actions are necessary to fully secure your finances and ensure a smooth transition.

Monitoring Your Account Activity: Vigilance Against Fraudulent Transactions

Even after cancellation, it’s imperative to meticulously monitor your checking account activity for several days, if not weeks. Fraudsters sometimes attempt to use card details before the cancellation fully propagates through all systems, or they might have gained access to your account in other ways. Regularly check your online banking statements for any unauthorized debits or pending transactions. Report any suspicious activity immediately to Chase. This continuous monitoring is a cornerstone of proactive personal financial security.

Updating Recurring Payments and Subscriptions: Avoiding Service Interruptions

Many services, from streaming subscriptions to utility bills, are linked to your debit card for automatic payments. Once your old card is canceled, these payments will fail.

- Create a List: Compile a comprehensive list of all recurring payments and subscriptions linked to your old debit card.

- Update Information: As soon as you receive your new card, log into each service provider’s portal and update your payment information with the new card details.

- Pro Tip: Consider using a credit card for recurring payments if possible, as credit cards generally offer stronger fraud protection and less direct access to your primary funds. This falls squarely within effective personal finance management.

Notifying Joint Account Holders (If Applicable): Ensuring Everyone is Informed

If your debit card is associated with a joint checking account, ensure all other account holders are immediately informed of the cancellation. This prevents confusion, failed transactions, and ensures everyone is aware of the change and any new card details. Transparent communication among joint account holders is vital for shared financial responsibility.

Securing Your Financial Information: Beyond the Card Itself

Canceling a debit card is a tactical move, but a broader strategic approach to financial security is also crucial.

- Review Your Computer/Mobile Device Security: If you suspect your card details were compromised online, ensure your devices are free of malware and updated with the latest security patches.

- Change Passwords: Consider changing passwords for your online banking and other sensitive financial accounts, especially if you suspect your credentials might have been compromised.

- Beware of Phishing: Be extra cautious of phishing attempts (emails, texts, calls) that might try to exploit your recent card cancellation by asking for personal information. Chase will never ask for your full SSN or online banking password via unsolicited email or text.

Receiving Your New Chase Debit Card and Activation

Once your old card is canceled and a replacement ordered, understanding the process for receiving and activating your new card is key to restoring full access to your funds.

Understanding Delivery Timelines

Chase typically mails new debit cards within 5-7 business days. If you’ve reported a card lost or stolen, you might have the option for expedited delivery, often for an additional fee, which can reduce delivery time to 2-3 business days. Be sure to confirm the delivery timeline with the Chase representative or via online banking when ordering.

Safe Receipt and Activation Best Practices

- Secure Mailbox: Ensure your mailbox is secure, especially if you live in an apartment building.

- Never Activate Until Received: Only activate your card once it is physically in your possession. Do not respond to requests to activate a card you haven’t received.

- Follow Activation Instructions: New cards come with activation instructions (usually a phone number or online portal). Follow these carefully. Often, you’ll need to verify your identity.

- Sign Immediately: Once activated, sign the back of your card immediately.

What to Do If Your New Card Doesn’t Arrive

If the expected delivery window passes and your new card hasn’t arrived, contact Chase customer service immediately. There might have been an issue with the mailing address, or the card could have been intercepted. Chase can then investigate and issue another replacement.

Broader Implications for Your Personal Finance

The act of canceling a debit card, while seemingly minor, touches upon broader themes within personal finance. It’s an opportunity to reinforce healthy financial habits and deepen your understanding of the tools at your disposal.

The Importance of Regular Financial Reviews: Proactive Risk Management

An incident requiring card cancellation should serve as a prompt for a comprehensive financial review. Regularly checking your credit reports, reviewing bank statements, and auditing your financial accounts are proactive measures that can identify vulnerabilities before they escalate into major problems. This regular oversight is a cornerstone of sound personal finance and risk management.

Understanding Debit Card vs. Credit Card Protections: Key Differences

It’s crucial to understand that debit card fraud protections, while significant, often differ from those offered by credit cards. With a debit card, fraudsters gain direct access to your bank account, potentially draining funds immediately. While federal law (Regulation E) limits your liability if you report fraud promptly, the temporary loss of funds can be disruptive. Credit cards, on the other hand, provide a layer of separation between your funds and the fraudulent transaction, as you’re spending the bank’s money, not your own. This distinction is vital for understanding your risk exposure and informs smart spending habits.

Leveraging Chase’s Security Features: Utilizing Available Tools

Chase offers various security features designed to protect your account. Familiarize yourself with and utilize tools like:

- Account Alerts: Set up alerts for large transactions, international usage, or online purchases to be notified immediately of activity.

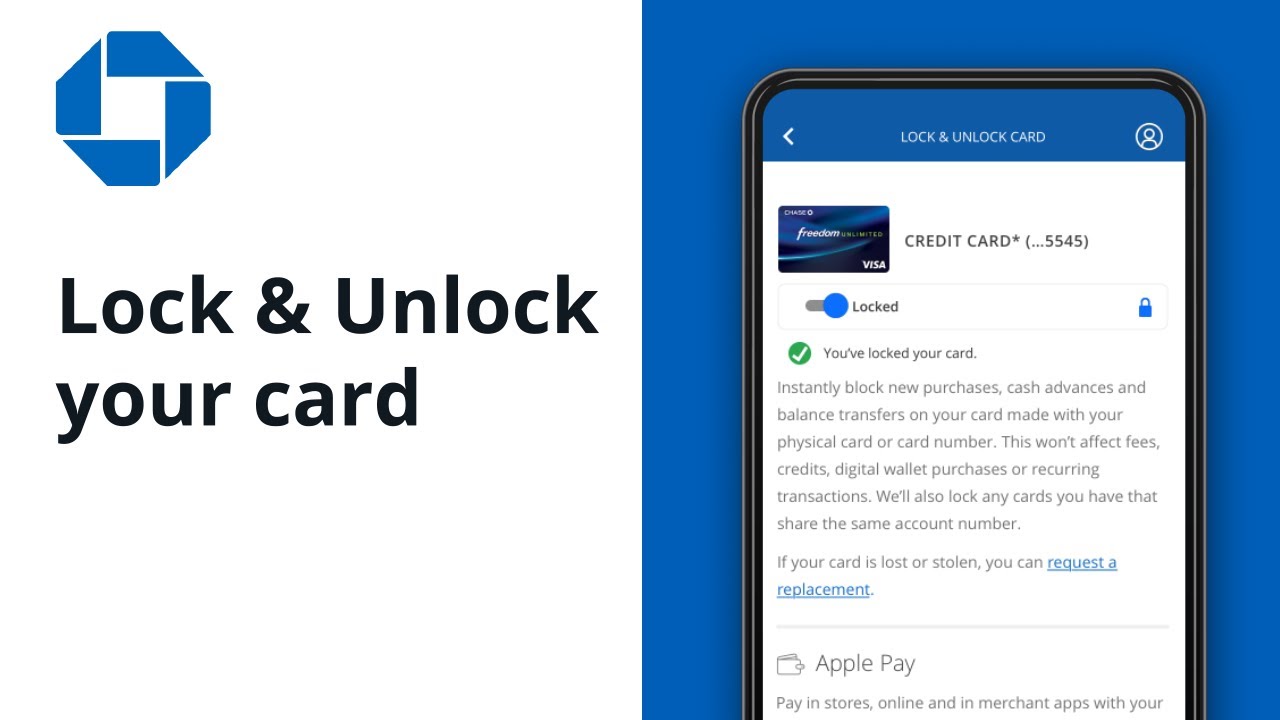

- Card Lock/Unlock Feature: The Chase mobile app often allows you to temporarily “lock” your debit card if you misplace it, and “unlock” it when found, without needing a full cancellation and replacement. This is an excellent interim security measure.

- Zero Liability Protection: Understand Chase’s zero liability policy, which generally protects you from unauthorized transactions as long as you report them promptly.

Building a Resilient Financial Security Strategy: Long-Term Planning

Ultimately, knowing how to cancel your Chase debit card is part of a larger strategy for building resilient financial security. This strategy includes:

- Diversifying Funds: Not keeping all your funds in a single, easily accessible checking account.

- Strong Passwords and Multi-Factor Authentication: Implementing robust digital security practices across all financial platforms.

- Identity Theft Protection: Considering services that monitor your identity and alert you to potential breaches.

- Financial Literacy: Continuously educating yourself on best practices for managing your money, protecting your assets, and navigating the evolving landscape of financial tools and threats.

In conclusion, managing your Chase debit card, including knowing when and how to cancel it, is a fundamental skill in personal finance. By understanding the processes, taking immediate action when necessary, and implementing broader security measures, you empower yourself to protect your assets and maintain control over your financial destiny. This proactive approach ensures that your journey towards financial well-being remains secure and uninterrupted.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.