Understanding the costs associated with banking services is a cornerstone of sound personal finance. For many account holders, ordering physical checks remains a periodic necessity, and the question of “how much are checks at Chase?” is a common one. While the immediate answer can seem straightforward, a deeper dive reveals a nuanced landscape influenced by account types, ordering methods, and the evolving role of checks in modern financial management.

Understanding Check Costs at Major Banks

The practice of charging for checks is widespread across the banking industry, including major institutions like Chase. This isn’t merely a revenue-generating strategy but rather a reflection of the operational costs involved in producing secure, personalized financial instruments.

Why Banks Charge for Checks

Banks incur significant expenses in the process of providing checks. These include the cost of specialized paper, printing, security features (such as watermarks, microprinting, and chemical protection), quality control, and the logistics of order processing and delivery. Furthermore, maintaining the infrastructure for check processing—from clearing houses to fraud prevention systems—adds to the overhead. When you pay for a box of checks, you’re contributing to these operational costs and receiving a secure document that facilitates transactions while minimizing risk. Account tiers and relationship banking often play a role; customers with premium accounts or substantial balances may have these fees waived as a perk, reflecting the bank’s desire to retain valuable clients.

Standard Check Pricing Models

Check pricing typically follows a per-box model, where the cost varies based on the quantity, design complexity, and security features. A standard box usually contains 100-150 checks. Basic, no-frills designs are generally the least expensive, while custom designs featuring specific images, logos, or enhanced security measures will carry a higher price tag. Expedited shipping is almost always an additional charge, appealing to those in urgent need of new checks. It’s also common for banks to partner with third-party check printing companies, which manage the production and delivery, adding another layer to the pricing structure. The goal for consumers is often to balance cost with necessity and personal preference.

Chase Bank’s Approach to Check Orders

Chase, like other large financial institutions, has a structured approach to providing checks to its customers. The exact cost you pay can vary significantly based on several factors unique to your banking relationship and specific ordering choices.

Factors Influencing Chase Check Prices

The primary determinants of check costs at Chase include your specific checking account type, the design and style of the checks you choose, the quantity ordered, and your preferred delivery speed.

- Account Type: Certain Chase checking accounts, particularly premium tiers like Chase Private Client Checking℠ or Chase Sapphire Checking℠, often include complimentary standard checks as a benefit. Basic checking accounts, such as Chase Total Checking®, typically require customers to pay for checks. This is a common strategy to incentivize higher account balances or broader service utilization.

- Check Design: Basic checks, usually a standard blue or green security background, are the most affordable. If you opt for more personalized designs—perhaps with custom images, specific patterns, or advanced security features—the price will increase. Business checks, which often include company logos and specific formatting, also tend to be more expensive than personal checks.

- Quantity: Checks are usually sold in boxes, with common quantities being 100, 150, or 200 checks per box. While buying more checks at once might offer a slightly better per-check unit price, it’s crucial to consider how many you realistically need. Over-ordering can lead to wasted money if your banking habits shift or if your account details change before you use them all.

- Delivery Speed: Standard delivery is usually included in the base price, but if you need your checks quickly, expedited shipping options are available for an extra fee. This can add a significant percentage to the total cost.

Common Check Styles and Their Price Implications

Chase offers a range of check styles through its preferred vendor, Harland Clarke.

- Standard Personal Checks: These are the most common and typically the least expensive. They feature basic security measures and a simple design. For eligible accounts, these are often the “free” option.

- Custom/Designer Personal Checks: These allow for more personalization, including scenic images, specific themes, or character designs. While aesthetically pleasing, they come at a higher cost.

- Business Checks: Designed for businesses, these often include space for company information, logos, and can be structured for payroll or accounts payable. They are generally more robust and come with a higher price point due to their specialized nature and typically higher security requirements. The cost of business checks varies widely depending on the level of customization and security features required.

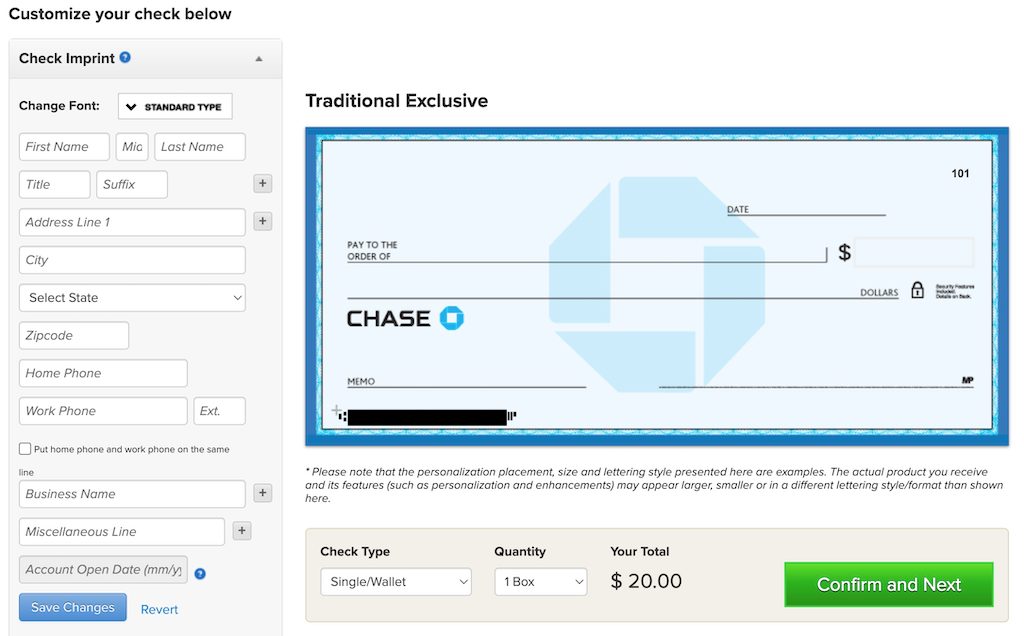

How to Order Checks from Chase

Chase provides multiple convenient ways to order checks, each with its own workflow:

- Online Banking: This is often the easiest and most preferred method. Log into your Chase Online account, navigate to the “Customer Service” or “Account Services” section, and look for an option to “Order Checks” or “Supplies.” You’ll be able to view available designs, prices, and track your order. The online portal typically displays the most up-to-date pricing based on your account type.

- Through a Branch: You can visit any Chase branch and request to order checks. A banking representative can assist you with the process, show you design options, and confirm pricing. This method can be helpful if you have specific questions or prefer in-person assistance.

- By Phone: Contact Chase customer service directly. A representative can guide you through the ordering process over the phone, confirm details, and provide pricing information. This is a good option if you cannot access online banking or a branch.

- Reorder Slips: Many checkbooks include a reorder slip near the end. You can fill this out and mail it, although this is generally the slowest method.

Regardless of the method, it’s always wise to confirm the total cost, including any shipping fees, before finalizing your order.

Strategies to Minimize or Avoid Check Fees

While checks remain essential for certain transactions, understanding how to reduce or avoid associated costs is a key aspect of managing your personal finances efficiently.

Leveraging Premium or Relationship Accounts

One of the most effective ways to avoid check fees at Chase is to qualify for one of their premium checking accounts. As mentioned, accounts like Chase Private Client Checking or Chase Sapphire Checking often come with perks such as complimentary standard checks. These accounts typically require higher average daily balances or significant assets under management with Chase. If you meet the criteria for such an account, the cost savings on checks (along with other potential fee waivers on services like wire transfers or ATM fees) can be a significant benefit. Regularly reviewing your account benefits and comparing them to your banking needs can help you ensure you’re getting the most value.

Utilizing Digital Payment Alternatives

In today’s digital age, the need for physical checks has significantly diminished for many routine transactions. Leveraging digital alternatives can not only save you money on check orders but also offer greater convenience, speed, and often enhanced security.

- Online Bill Pay: Chase offers a robust online bill pay service through its banking portal and mobile app. You can set up one-time or recurring payments to virtually any payee, from utilities and credit cards to individuals. Chase typically handles the electronic payment, or if the payee doesn’t accept electronic payments, the bank will mail a physical check on your behalf—often at no charge to you.

- Zelle®: For person-to-person payments, Zelle, integrated directly into the Chase Mobile® app, allows you to send and receive money directly between bank accounts, typically within minutes, using just an email address or U.S. mobile number. This is a free service for Chase customers and eliminates the need for checks for gifting, splitting bills, or paying contractors.

- ACH Transfers: Automated Clearing House (ACH) transfers are electronic funds transfers that are commonly used for direct deposits (like paychecks) and direct debits (like mortgage payments). These are cost-effective and secure ways to move money between accounts or pay bills electronically, bypassing physical checks entirely.

- Mobile Banking Features: Many tasks traditionally requiring checks, such as paying friends or even depositing a check you’ve received, can now be done via the Chase Mobile app. Mobile check deposit, for instance, allows you to snap a photo of a received check and deposit it without visiting an ATM or branch.

By embracing these digital tools, you can dramatically reduce your reliance on physical checks and, consequently, the costs associated with ordering them.

Exploring Third-Party Check Providers (with caution)

For those who do not qualify for free checks through their Chase account and find Chase’s pricing too high, there are numerous third-party check printing companies that often offer checks at a lower cost. Websites like Checks Unlimited, Deluxe, or VistaPrint frequently advertise competitive pricing.

- Cost Savings: These providers can often undercut bank pricing because they specialize solely in check printing and benefit from economies of scale.

- Cautionary Notes: While third-party providers can save money, it’s crucial to exercise caution. Ensure the provider is reputable, uses secure printing methods, and offers checks that meet banking industry standards for security and compatibility. Verify that their checks will be accepted by Chase’s processing systems. Always double-check your account and routing numbers before finalizing an order. Also, be mindful of privacy and data security when providing sensitive banking information to a third party. While a valid cost-saving strategy, it requires due diligence.

The Evolving Role of Checks in Modern Finance

While digital payments dominate the financial landscape, physical checks have not entirely disappeared. Understanding when they are still necessary and how to integrate their use into a broader financial strategy is important for comprehensive personal finance management.

When Checks Are Still Necessary

Despite the proliferation of digital payment methods, there are specific situations where a physical check remains the preferred or even the only option:

- Rent Payments: Many landlords, particularly smaller or individual landlords, still prefer or require rent payments via physical check.

- Specific Bill Payments: Certain niche service providers, older businesses, or government agencies might not have robust electronic payment systems and may request checks.

- Gifts: Presenting a financial gift in the form of a check is still a common and socially accepted practice, often tucked into a card.

- Business Transactions: Some businesses still rely on checks for vendor payments, payroll for small operations, or in situations where an electronic audit trail is less convenient than a paper one.

- Security Deposits: Landlords or service providers often prefer checks for security deposits, as they provide a clear paper trail and can be easier to manage than cash or some digital transfers for this specific purpose.

In these scenarios, having a supply of checks, even if rarely used, can be a practical necessity.

The Shift Towards Digital Transactions

The ongoing shift from physical checks to digital transactions is driven by several compelling advantages:

- Efficiency: Digital payments are often instantaneous or process much faster than checks, which can take several business days to clear.

- Security: While checks have security features, they are susceptible to fraud (e.g., check washing). Digital transactions, especially those with multi-factor authentication and encryption, can offer robust security protocols.

- Convenience: Payments can be initiated from anywhere with an internet connection, eliminating the need for stamps, envelopes, or trips to the bank.

- Record Keeping: Digital transactions automatically create an electronic record, simplifying budgeting, expense tracking, and tax preparation.

This shift signifies a broader trend in personal finance towards streamlined, real-time money management.

Financial Planning Beyond Physical Checks

Effective financial planning in the modern era means recognizing that checks are just one tool in a vast financial toolkit. Budgeting for check costs, understanding your bank’s fee structure, and proactively adopting digital alternatives are all crucial. Regularly review your bank statements for any unexpected fees, including those related to checks or other services. Engage with Chase’s online banking and mobile app to explore all available payment and money management features. By being informed and strategic about how you pay, you can optimize your financial flow, minimize unnecessary expenses, and maintain better control over your money. Understanding the cost of checks at Chase is not just about a single fee; it’s about making informed choices that contribute to your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.