The journey to effective weight management often involves more than just diet and exercise; for many, it now includes medications like Wegovy. As a GLP-1 receptor agonist, Wegovy (semaglutide) has emerged as a significant advancement in treating chronic weight management, often leading to substantial weight loss when used in conjunction with lifestyle interventions. However, the efficacy of this groundbreaking medication comes with a considerable price tag, raising critical financial questions for prospective users. Understanding the true cost of Wegovy involves dissecting its retail price, the labyrinth of insurance coverage, and the potential for financial assistance programs. This article delves into the financial intricacies of accessing Wegovy, offering insights into budgeting, long-term planning, and making an informed financial decision about your health.

The Baseline Price Tag: Understanding Wegovy’s Uninsured Cost

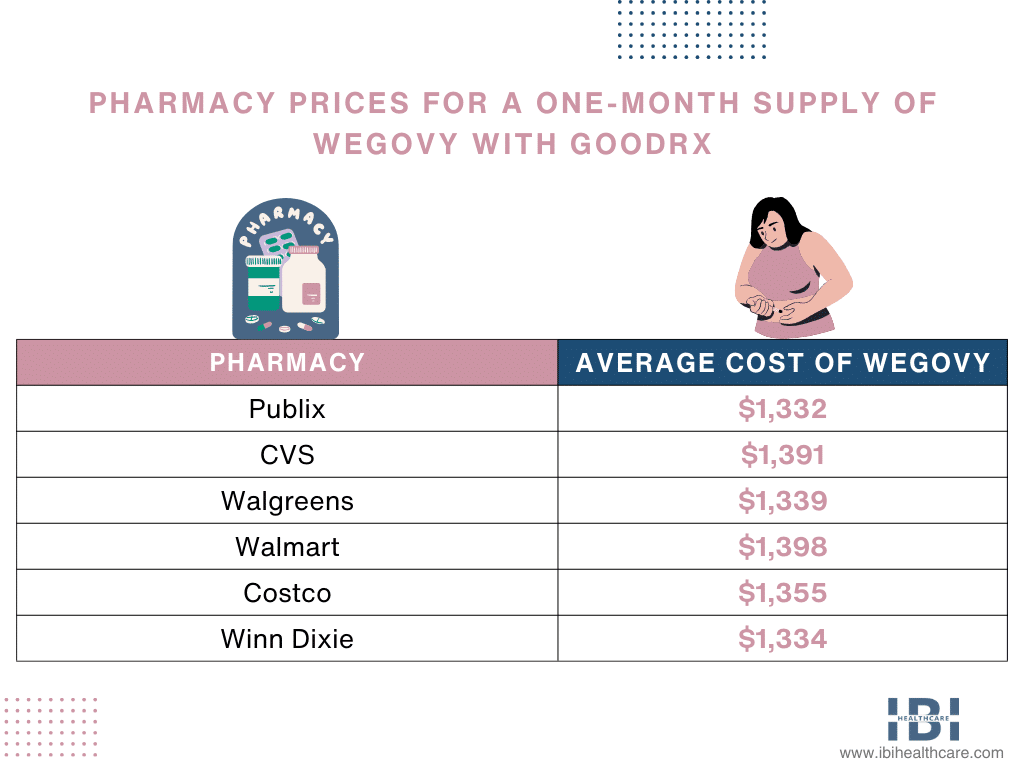

Before exploring insurance benefits and savings programs, it’s crucial to understand the foundational cost of Wegovy. For individuals without insurance coverage, or for those whose plans do not cover the medication, the retail cash price can be a significant barrier.

The Weekly and Monthly Out-of-Pocket Expense

Wegovy is administered via a once-weekly injection, making its cost calculation relatively straightforward on a monthly basis. The typical list price or cash price for a 28-day supply (four pre-filled pens, each containing one weekly dose) of Wegovy can range significantly, but it frequently hovers between $1,300 and $1,600 per month in the United States. This translates to an annual expenditure that could easily exceed $15,000 to $19,000 for continuous treatment without any form of financial aid. These figures represent the uninsured cost, often referred to as the “sticker price,” and serve as a starting point for financial planning.

Factors Influencing Retail Cash Prices

Several factors can influence the exact retail price you might encounter:

- Pharmacy Markups: Different pharmacies, both brick-and-mortar and online, may have varying markups and pricing strategies. Shopping around can sometimes yield slight differences, though the core manufacturer’s list price remains a dominant factor.

- Geographic Location: While less impactful for a widely distributed pharmaceutical like Wegovy, regional pricing variations can occasionally occur.

- Supply and Demand: High demand, coupled with any potential supply chain issues, can influence pricing, though manufacturers typically maintain a consistent list price for such medications.

- Dosage Strength: While Wegovy comes in escalating doses, the monthly cost for a 28-day supply generally remains consistent across different strengths once treatment is initiated and the maintenance dose is reached. The cost is for the kit of four pens, regardless of the mg content for a given month.

For many, this baseline cost is prohibitive, underscoring the necessity of exploring insurance coverage and financial assistance options.

Decoding Insurance Coverage: A Complex Equation

The vast majority of individuals seeking Wegovy will rely on health insurance to mitigate its high cost. However, securing coverage is rarely a straightforward process and involves navigating a complex landscape of formularies, prior authorizations, and out-of-pocket responsibilities.

Private Insurance: Navigating Formularies and Prior Authorization

Private health insurance plans vary widely in their coverage of weight loss medications. While some employers and insurers are beginning to recognize obesity as a chronic disease requiring medical treatment, many plans still classify weight loss drugs as “lifestyle” medications, often excluding them from coverage or imposing stringent criteria.

- Formulary Inclusion: The first hurdle is checking if Wegovy is listed on your insurance plan’s formulary (its list of covered drugs). If it’s not, you may need to pursue an appeal or request an exception, which can be a lengthy and often unsuccessful process.

- Prior Authorization (PA): Even if on the formulary, Wegovy almost invariably requires prior authorization. This means your prescribing physician must submit documentation to your insurance company demonstrating medical necessity. This often includes proving that you meet specific diagnostic criteria for obesity (e.g., a certain BMI), have tried and failed other weight loss interventions, and have obesity-related comorbidities.

- Step Therapy: Some plans may also require “step therapy,” meaning you must try and fail less expensive or alternative medications before Wegovy will be covered.

Medicare, Medicaid, and Government Plans: Evolving Policies

Historically, Medicare has explicitly excluded coverage for weight loss medications under Part D. However, there’s growing advocacy and legislative pressure to change this policy, recognizing obesity’s status as a disease. As of early 2024, Medicare Part D still generally does not cover Wegovy, although some exceptions for related conditions (like cardiovascular risk reduction if an FDA indication is approved) could potentially arise in the future.

Medicaid coverage varies significantly by state. Some state Medicaid programs may cover weight loss medications, while others do not. Eligibility for these programs also depends on income and other factors. Similarly, other government-sponsored plans (like TRICARE for military personnel) have their own specific formularies and criteria. It’s imperative to consult your specific plan’s details.

The Role of Deductibles, Co-pays, and Co-insurance

Even with insurance coverage, you’re unlikely to pay nothing. Your out-of-pocket costs will be determined by your plan’s structure:

- Deductible: This is the amount you must pay out of pocket before your insurance company starts to cover costs. Given Wegovy’s price, many individuals will pay the full cash price for several months until their deductible is met.

- Co-pay: A fixed amount you pay for a prescription after your deductible is met. For specialty medications like Wegovy, co-pays can still be substantial, often ranging from $50 to several hundred dollars per month.

- Co-insurance: A percentage of the drug’s cost you pay after your deductible is met. For example, if your co-insurance is 20% and Wegovy costs $1,300 per month, you would pay $260.

- Out-of-Pocket Maximum: Most plans have an annual out-of-pocket maximum, which is the most you’ll have to pay for covered services in a plan year. Once this is met, your insurance typically covers 100% of additional covered costs for the remainder of the year.

Understanding these components is vital for accurately projecting your personal financial burden.

Alleviating the Burden: Manufacturer Programs and Patient Assistance

Recognizing the high cost and the challenges of insurance coverage, the manufacturer of Wegovy, Novo Nordisk, offers programs designed to make the medication more accessible and affordable for eligible patients.

Novo Nordisk’s Savings Card: Reducing Your Co-pay

The most common form of assistance is the Novo Nordisk Savings Card. This program is typically available for commercially insured patients (those with private insurance) who meet certain eligibility requirements.

- How it Works: The savings card can help reduce your monthly out-of-pocket cost by covering a portion of your co-pay or co-insurance. For example, it might bring your monthly cost down to as little as $25 for a 28-day supply, up to an annual maximum benefit.

- Eligibility: To qualify, you generally must have commercial insurance that covers Wegovy, be a resident of the U.S., and not be enrolled in any government healthcare program (like Medicare, Medicaid, or TRICARE).

- Activation and Usage: You can usually apply for and activate the card online. Once approved, you present the card to your pharmacy along with your insurance information. It’s crucial to understand the annual maximum benefit; once that limit is reached, you will be responsible for the full co-pay amount for the remainder of the year.

Exploring Patient Assistance Programs (PAPs)

For individuals who are uninsured, underinsured, or facing significant financial hardship, Novo Nordisk also offers a robust Patient Assistance Program (PAP).

- Purpose: These programs are designed to provide free or low-cost medication to eligible patients who cannot afford their prescriptions.

- Eligibility: PAPs typically have strict income guidelines, often requiring applicants’ household income to be below a certain percentage of the Federal Poverty Level. Uninsured status or lack of adequate insurance coverage is also a primary criterion.

- Application Process: The application usually requires detailed financial documentation, proof of income, and a prescription from your healthcare provider. The process can be time-consuming, but for those who qualify, it can be a lifeline for accessing essential medication.

Investigating both the savings card and the PAP, depending on your insurance status and financial situation, is a crucial step in managing the cost of Wegovy.

Strategic Financial Planning for Long-Term Treatment

Wegovy is often a long-term treatment, meaning financial considerations extend beyond a single prescription fill. Effective financial planning is essential to sustain therapy and ensure its health benefits are fully realized.

Leveraging HSAs and FSAs for Medical Expenses

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are powerful tax-advantaged tools that can significantly reduce the net cost of Wegovy.

- HSAs: Available to those with high-deductible health plans, contributions to an HSA are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are tax-free. This triple-tax advantage makes HSAs ideal for saving and paying for medications like Wegovy, especially if you anticipate hitting your deductible.

- FSAs: Offered through employers, FSAs allow you to set aside pre-tax money from your paycheck for qualified medical expenses. While FSAs typically have a “use-it-or-lose-it” rule (funds generally expire at year-end), they can still provide substantial tax savings for known upcoming medical costs like Wegovy.

Using these accounts can effectively lower your overall healthcare spending by reducing your taxable income.

Budgeting for Ongoing Medication Costs

Even with insurance and savings programs, budgeting for Wegovy requires careful planning:

- Annual Cost Projection: Calculate your estimated annual out-of-pocket costs, considering your deductible, co-pays/co-insurance, and the annual maximums of any savings cards.

- Monthly Allocation: Integrate this projected cost into your monthly budget. If your deductible means higher payments early in the year, plan for those larger initial expenditures.

- Emergency Fund: Maintain an emergency fund that can cover unexpected healthcare costs or potential gaps in coverage.

- Review Regularly: Re-evaluate your financial situation and insurance coverage annually during open enrollment periods to ensure you’re in the most cost-effective plan for your needs.

Weighing the Cost-Benefit: Health Investments vs. Financial Outlay

The financial decision to take Wegovy is not just about the monetary cost but also about the potential health benefits and the long-term investment in your well-being. Significant weight loss can reduce the risk and severity of numerous obesity-related comorbidities, such as type 2 diabetes, heart disease, sleep apnea, and certain cancers.

While the direct cost of Wegovy is high, consider the potential future savings:

- Reduced Medical Expenses: Lowering your risk for chronic diseases can mean fewer doctor visits, fewer other medications, and potentially avoiding costly procedures or hospitalizations down the line.

- Improved Quality of Life: The intangible benefits of improved health, mobility, energy levels, and mental well-being are immeasurable, but contribute significantly to your overall quality of life.

This holistic perspective helps frame the cost of Wegovy not just as an expense, but as a strategic investment in long-term health.

Beyond Wegovy: The Holistic Financial View of Weight Management

Understanding Wegovy’s cost is part of a larger financial picture concerning weight management. It’s beneficial to compare its financial implications with other interventions and consider the broader economic impact of obesity.

Comparing Costs: Wegovy vs. Other Interventions

When evaluating the financial commitment to Wegovy, it can be helpful to consider the costs of alternative weight management strategies:

- Bariatric Surgery: While often covered by insurance, bariatric surgery involves significant upfront costs, including surgeon fees, hospital stays, anesthesia, and post-operative care, which can easily range from $15,000 to over $30,000 without insurance.

- Other Medications: Other weight loss medications (e.g., phentermine-topiramate, naltrexone-bupropion) may have lower monthly costs, but also different efficacy profiles and side effects.

- Structured Diet Programs & Personal Training: Commercial weight loss programs, specialized meal plans, and personal trainers can accrue significant monthly or annual costs, ranging from hundreds to thousands of dollars, without the same level of clinical efficacy demonstrated by GLP-1 agonists.

A comprehensive financial comparison helps contextualize Wegovy’s price point within the landscape of effective weight loss solutions.

The Economic Impact of Obesity: Indirect Savings

Obesity itself carries a substantial economic burden, both individually and societally. Individuals with obesity often incur higher direct medical costs (doctor visits, prescriptions, hospitalizations) and indirect costs (lost productivity, disability).

By effectively managing weight, Wegovy users might realize:

- Fewer Co-morbidities: Reduced incidence or severity of chronic diseases linked to obesity.

- Lower Medication Load: Potentially needing fewer medications for conditions like hypertension or diabetes.

- Increased Productivity: Improved health can lead to better work performance and fewer sick days.

These indirect savings, though harder to quantify precisely, represent a significant financial benefit that can offset a portion of Wegovy’s cost over time.

Making an Informed Financial Decision

Ultimately, the decision to pursue Wegovy treatment is deeply personal and multifaceted, with financial considerations playing a pivotal role. It requires:

- Thorough Research: Understand the medication, its efficacy, and its side effects.

- Detailed Financial Assessment: Accurately calculate your potential out-of-pocket costs, considering all insurance variables, savings programs, and tax advantages.

- Consultation with Professionals: Discuss the financial implications with your healthcare provider, a financial advisor if needed, and directly with your insurance provider.

- Long-Term Perspective: Consider the ongoing nature of treatment and its implications for your budget and overall financial health.

While the cost of Wegovy is undoubtedly high, understanding the full scope of financial planning, insurance navigation, and available assistance can empower individuals to make an informed, sustainable decision about investing in their health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.