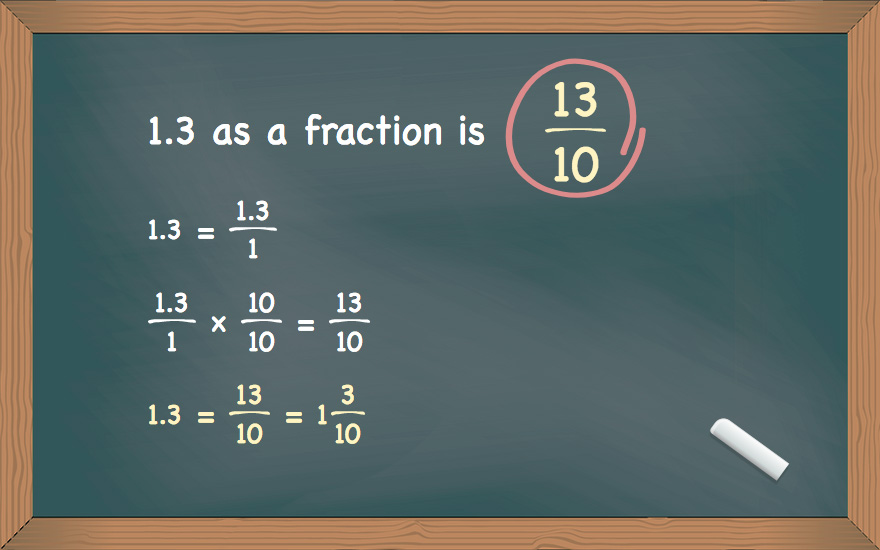

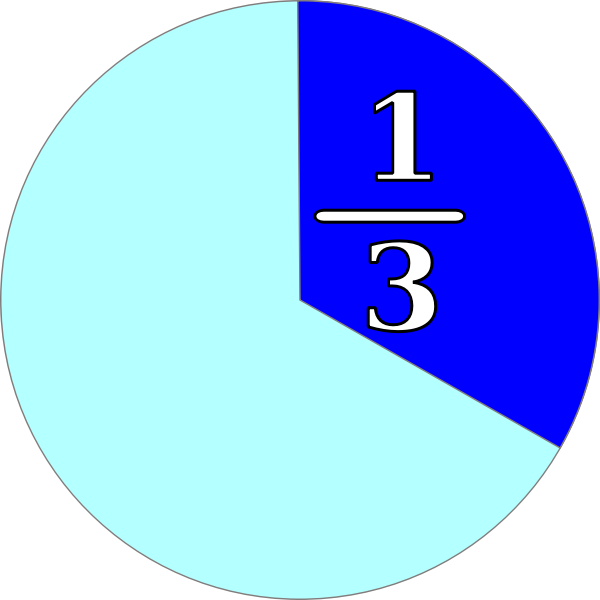

At its core, the question “what is 1/3 + 1/3 as a fraction?” is a fundamental exercise in arithmetic, a simple problem with a straightforward answer: 2/3. However, to confine our understanding to just this mathematical outcome would be to miss a profound and often overlooked truth. In the realm of money—be it personal finance, investing, or business—this seemingly basic calculation serves as a potent metaphor and a foundational concept. It underscores the critical importance of understanding proportions, divisions, and allocations, which are the bedrock of sound financial management.

Far from being a mere academic exercise, grasping how fractions work and applying that understanding to financial scenarios is an indispensable skill. It empowers individuals and businesses to make informed decisions, dissect complex financial data, and build robust strategies for growth and security. This article will delve into how this simple fractional sum illuminates the intricate world of finance, demonstrating its relevance from budgeting personal income to structuring investment portfolios and understanding business equity.

The Foundational Importance of Fractions in Financial Literacy

Before we can master complex financial instruments or sophisticated investment strategies, we must first be fluent in the language of numbers, and fractions are a crucial dialect within that language. The ability to conceptualize parts of a whole is not just for schoolchildren; it is a vital tool for anyone navigating the financial landscape.

Beyond Simple Arithmetic: Why Fractions Matter for Your Money

In finance, everything from your budget to your investment portfolio is a “whole” that is divided into various “parts.” A fraction provides the clearest, most intuitive way to represent these parts. When you consider your monthly income, it’s a whole, and every expense, saving, or investment is a fraction of that whole. If a third of your income goes to housing and another third to living expenses, then understanding that 1/3 + 1/3 equals 2/3 immediately tells you that two-thirds of your income is already allocated, leaving only one-third for other priorities or discretionary spending. This isn’t just about adding numbers; it’s about understanding the proportion of your resources being directed to different areas.

Fractions help us visualize and compare these proportions. They allow us to intuitively grasp how significant one part is relative to another, or relative to the total. This proportional thinking is indispensable for financial planning, enabling individuals to assess their financial health, identify areas for improvement, and allocate resources strategically. Without this foundational understanding, financial decisions often become arbitrary, lacking the precision and insight that fractional analysis provides.

Demystifying Financial Language: Percentages and Decimals as Fractions

While financial statements and discussions often lean heavily on percentages and decimals, it’s crucial to remember that these are simply different representations of fractions. For instance, 1/3 is approximately 0.3333 or 33.33%. Understanding this direct conversion is powerful. When an investment offers a “1/3 share of profits,” or a budget rule suggests “spending no more than 1/3 of your income on housing,” these concepts are directly transferable to percentages or decimals, depending on the context.

Being able to fluidly move between fractions, decimals, and percentages ensures that you can interpret financial information regardless of how it’s presented. This versatility is key to comprehensive financial literacy. It means you won’t be flummoxed by a “33.33% expense ratio” in an investment fund, because you’ll instantly recognize it as roughly one-third of your returns being consumed by fees. Conversely, if you’re told you own “0.25 of the company,” you immediately understand that means a quarter, or 25%, of the ownership. This ability to convert and comprehend empowers individuals to engage critically with financial data, rather than being passively presented with numbers they don’t fully understand.

Applying Fractional Thinking to Personal Finance

The most immediate and impactful application of fractional understanding is within personal finance. Every budget, every savings goal, and every debt repayment plan benefits immensely from a proportional approach.

Budgeting and Expense Allocation: Dividing Your Financial Pie

Consider your monthly income as a pie. How do you slice it? This is where fractional thinking becomes tangible. Common budgeting strategies, such as the 50/30/20 rule (50% for needs, 30% for wants, 20% for savings and debt repayment), are essentially fractional allocations of your total income. Here, 50% is 1/2, 30% is 3/10, and 20% is 1/5. Understanding these as fractions reinforces the idea that each portion is a deliberate slice of your financial pie.

Let’s revisit our core problem: 1/3 + 1/3 = 2/3. Imagine you decide to allocate 1/3 of your income to rent and utilities, and another 1/3 to groceries and transportation. Immediately, you know that 2/3 of your income is committed to non-discretionary expenses. This leaves you with just 1/3 for everything else—savings, entertainment, debt repayment, and other wants. This simple addition highlights how quickly commitments can consume the majority of your resources, prompting you to consider if the remaining 1/3 is sufficient for your financial goals or if adjustments are needed. It forces a clear-eyed assessment of whether your spending aligns with your values and objectives.

Understanding Debt and Savings Proportions

Fractions are equally vital when assessing debt and savings. How much of your available funds are consumed by debt payments? If 1/3 of your discretionary income goes towards credit card interest, and another 1/3 towards a car loan, you’re looking at 2/3 of your flexibility being absorbed by past financial decisions. This insight can be a powerful motivator to tackle debt aggressively.

Conversely, for savings, fractional thinking helps you set and track goals. If you aim to save 1/10 of your income each month, you can easily calculate the absolute amount and track your progress. Over time, these small fractions accumulate, demonstrating the compounding power of consistent saving. The challenge then becomes how to increase that fraction—perhaps from 1/10 to 1/5—to accelerate your financial progress, moving from accumulating small parts to building a significant whole.

Fractions in Investment and Business Finance

Moving beyond personal finance, fractions are integral to understanding investment structures, portfolio diversification, and the equity dynamics within businesses.

Stock Ownership and Portfolio Diversification: Slicing the Investment Pie

In the investment world, owning “shares” of a company is literally owning fractions of that company. If a company has one million shares outstanding and you own 100,000 shares, you own 1/10 of the company. Understanding these proportions is crucial for grasping your stake and potential returns. The advent of fractional share investing, where you can buy a portion of a single share, makes this concept even more direct and accessible, allowing smaller investors to own slivers of high-priced stocks.

Furthermore, diversification—a cornerstone of intelligent investing—is entirely based on fractional allocation. An investor might decide to put 1/3 of their portfolio into large-cap stocks, 1/3 into bonds, and 1/3 into real estate or alternative investments. This strategy aims to mitigate risk by not putting all “eggs in one basket.” The exact proportions, or fractions, assigned to each asset class are critical decisions based on risk tolerance, investment goals, and time horizon. The 1/3 + 1/3 = 2/3 calculation here might represent the combined allocation to two major asset classes, helping an investor quickly see how much of their capital is tied up in specific market segments. It ensures a balanced approach and prevents over-concentration in any single area.

Business Equity and Profit Sharing

For entrepreneurs and business owners, fractions define ownership, control, and profit distribution. When starting a company with partners, each partner’s stake is often expressed as a fraction—1/2, 1/3, 1/4, and so on. These fractions determine voting power, rights to assets, and, crucially, shares of the profits (or losses).

Consider a scenario where three partners start a business. Partner A invests significantly more cash but contributes less time, receiving 1/2 of the equity. Partner B and C contribute equally in time and skill, each receiving 1/4 of the equity. Here, 1/2 + 1/4 + 1/4 = 1, representing the whole business. If profits are distributed based on equity, then Partner A gets twice as much as Partner B or C. Understanding these fractional divisions is paramount for fair and legally sound business relationships, avoiding future disputes over control or financial returns. Similarly, profit-sharing schemes with employees often involve allocating a certain fraction of the company’s profits to a bonus pool, which is then further fractioned among eligible staff.

From Simple Sums to Complex Financial Decisions: The Power of Proportional Reasoning

The journey from understanding 1/3 + 1/3 = 2/3 to making astute financial decisions is built on the power of proportional reasoning. It teaches us not just to count, but to understand scale and relativity.

The Cumulative Impact: How Small Fractions Add Up (or Detract)

One of the most profound lessons from fractional math in finance is the concept of cumulative impact. Just as 1/3 + 1/3 accumulates to 2/3, consistently saving a small fraction of your income each month, or consistently paying a small fraction of fees on your investments, will have a significant cumulative effect over time. A seemingly small 1/100 (1%) fee on an investment portfolio might appear negligible, but compounded over decades, it can erode a substantial fraction of your potential returns. Conversely, consistently investing 1/10 of your income can lead to substantial wealth accumulation.

This highlights the importance of consistency and long-term perspective. Financial success often isn’t about grand gestures but about the diligent management of small, consistent fractions that add up (positively or negatively) over time. Understanding this teaches patience and reinforces the value of habitual financial discipline.

Avoiding Fractional Fallacies: Critical Thinking in Financial Analysis

Finally, fractional understanding arms us with critical thinking skills to avoid common financial fallacies. Sometimes, numbers can be presented in a way that obscures the true proportion. For example, a company might boast a “50% increase in market share,” but if their original market share was only 1/100 (1%), then a 50% increase only brings them to 1.5/100 (1.5%)—still a tiny fraction of the overall market. Without understanding the base (the denominator of the fraction), the percentage increase can be misleading.

Being able to translate percentages back into fractions helps to contextualize information. It allows you to ask: “50% of what?” or “What fraction of the total does this really represent?” This critical lens is invaluable for evaluating investment pitches, marketing claims, and even government economic reports, ensuring that you’re not swayed by impressive-sounding numbers that represent an insignificant fraction of the bigger picture.

Conclusion: Building a Strong Financial Foundation, One Fraction at a Time

The answer to “what is 1/3 + 1/3 as a fraction?” is 2/3. But its implications, particularly in the domain of money, extend far beyond basic arithmetic. This simple sum serves as a potent reminder that financial literacy begins with foundational mathematical concepts. From crafting a sustainable personal budget and strategically allocating savings, to diversifying investment portfolios and understanding business equity, the ability to think in terms of fractions—parts of a whole—is indispensable.

It empowers individuals and businesses to measure, compare, and allocate resources with precision and insight. It demystifies financial jargon, encourages critical thinking, and reveals the cumulative impact of financial decisions over time. By embracing the power of proportional reasoning, we can transform abstract financial concepts into tangible, manageable components, paving the way for more informed decisions and a stronger, more secure financial future. So, the next time you encounter a seemingly simple fraction, remember its profound potential to unlock greater financial understanding and empowerment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.