For many retirees and those nearing retirement, Social Security represents a cornerstone of financial security. It’s a benefit earned over a lifetime of work, and there’s a common misconception that these benefits are entirely tax-free. However, for a significant number of beneficiaries, a portion of their Social Security income is indeed subject to federal income tax. Understanding how much of your Social Security is taxable is not just a matter of compliance; it’s a critical component of effective retirement planning.

This guide will demystify the federal taxation of Social Security benefits, introduce you to the concept of “provisional income,” and explain how a Social Security taxable benefits calculator can be an invaluable tool for anticipating your tax obligations. By the end, you’ll have a clear understanding of the rules and how to better plan for your financial future.

The Basics of Social Security Taxation

The taxation of Social Security benefits was introduced in 1983 and expanded in 1993, primarily affecting higher-income beneficiaries. The amount of your benefits that is subject to federal income tax depends on your total income, specifically what the IRS refers to as your “provisional income.”

Who Pays Taxes on Social Security?

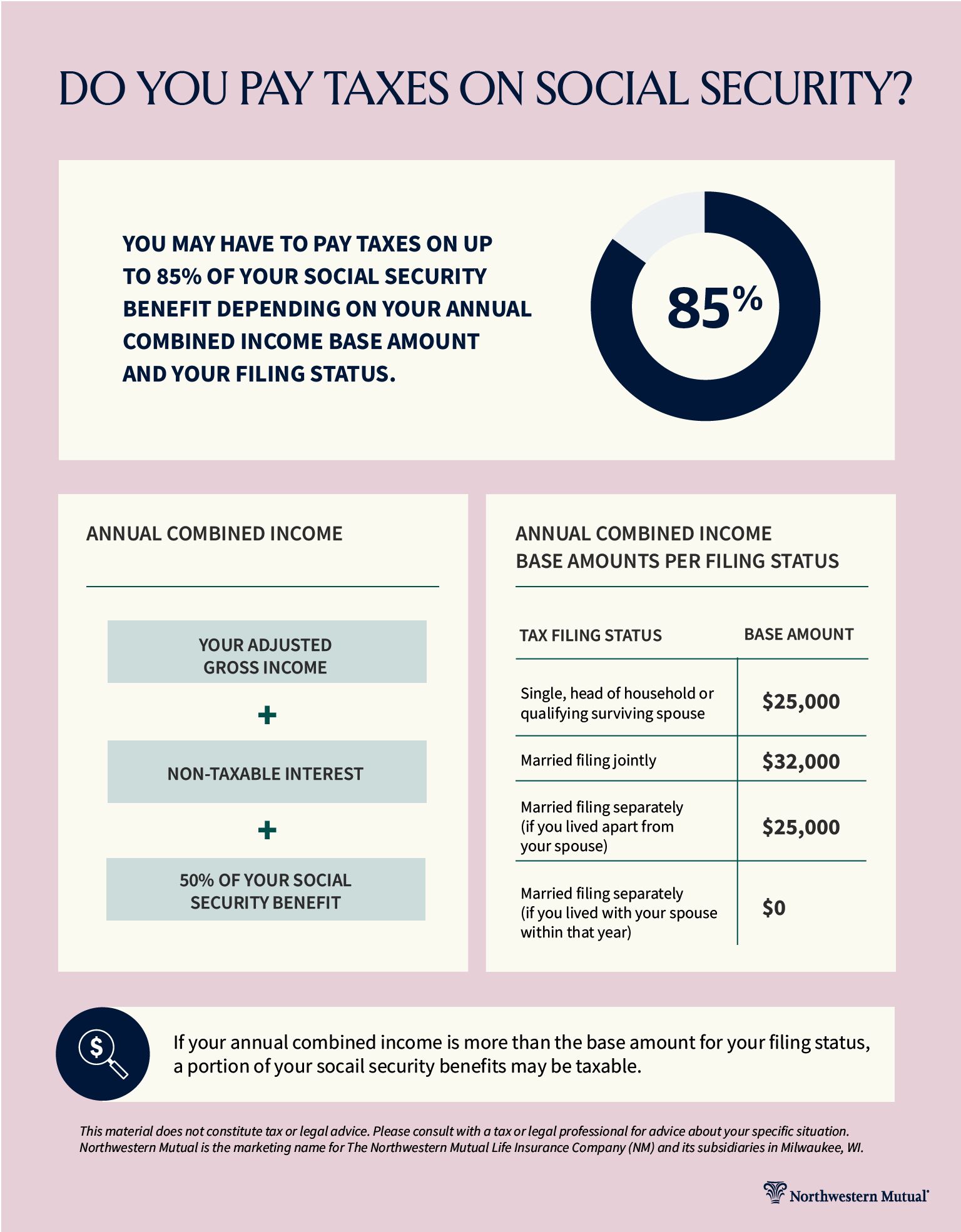

Whether you pay taxes on your Social Security benefits largely depends on your “provisional income.” This isn’t a term you’ll typically find on your tax return, but it’s crucial for this specific calculation. The IRS uses provisional income to determine if your income crosses certain thresholds that trigger the taxation of your benefits.

Your provisional income is calculated by adding three main components:

- Your Adjusted Gross Income (AGI): This is your gross income minus certain deductions, as shown on your tax return.

- Tax-exempt interest: This includes interest earned from sources like municipal bonds, which are generally not subject to federal income tax but are included for the purpose of this calculation.

- Half of your Social Security benefits: This refers to 50% of the total Social Security benefits you received during the tax year.

It’s important to note that tax-exempt interest is included because the original intent of the law was to ensure that people with substantial tax-free income still contributed to the funding of Social Security through taxation of their benefits.

The Provisional Income Thresholds

Once you’ve calculated your provisional income, you compare it against specific thresholds set by the IRS. These thresholds determine whether 0%, 50%, or 85% of your Social Security benefits will be subject to federal income tax. These thresholds vary based on your tax filing status:

-

For Single, Head of Household, or Qualifying Widow(er) filers:

- If your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable.

- If your provisional income is above $34,000, up to 85% of your benefits may be taxable.

- If your provisional income is below $25,000, none of your benefits are taxable.

-

For Married Filing Jointly filers:

- If your provisional income is between $32,000 and $44,000, up to 50% of your benefits may be taxable.

- If your provisional income is above $44,000, up to 85% of your benefits may be taxable.

- If your provisional income is below $32,000, none of your benefits are taxable.

-

For Married Filing Separately filers (who lived with their spouse at any time during the year):

- A different rule applies here. Generally, if you are married and file separately and lived with your spouse at any point during the year, up to 85% of your Social Security benefits are taxable, regardless of your provisional income level. This rule is designed to prevent couples from using separate filings to avoid Social Security taxation.

These thresholds are static and are not adjusted annually for inflation, which means more people may find their benefits becoming taxable over time as other income sources naturally increase.

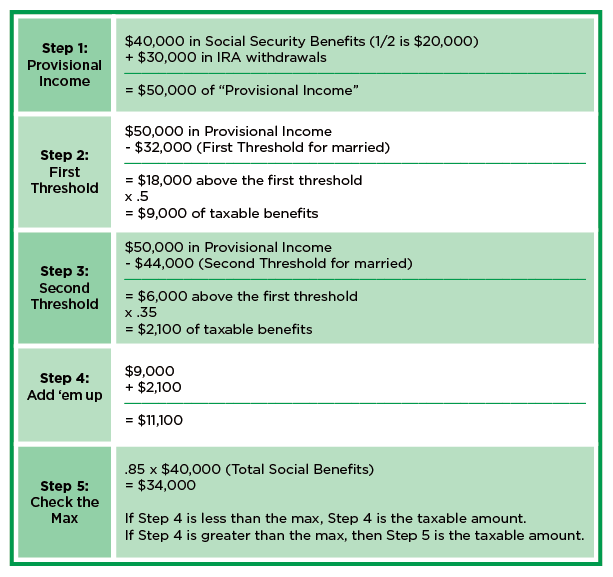

How Much is Taxed? The 50% and 85% Rules

The percentages—50% and 85%—do not mean that half or 85% of your entire Social Security benefit will necessarily be taxed. Instead, they define the maximum portion that could be included in your taxable income. The actual taxable amount is calculated using a more specific formula that involves your provisional income and the thresholds.

Here’s a simplified breakdown of the calculation:

-

Up to 50% Taxable: If your provisional income falls into the first threshold range (e.g., $25,000-$34,000 for single filers), the amount of your Social Security benefits included in your taxable income is the lesser of:

- 50% of your Social Security benefits, OR

- 50% of the amount by which your provisional income exceeds the lower threshold (e.g., $25,000).

-

Up to 85% Taxable: If your provisional income exceeds the second threshold (e.g., over $34,000 for single filers), the amount of your Social Security benefits included in your taxable income is the lesser of:

- 85% of your Social Security benefits, OR

- The sum of 85% of the amount by which your provisional income exceeds the higher threshold (e.g., $34,000 for single filers) plus the amount calculated for the 50% rule (which is always $4,500 for single filers, or $6,000 for married filing jointly, if the income fully exceeds the lower threshold).

This calculation can get complex quickly, which is precisely why a dedicated calculator can be so helpful.

Components of Your Provisional Income

To accurately use a Social Security taxable benefits calculator or perform a manual calculation, you need to precisely understand what constitutes your provisional income. It’s more than just your Social Security check.

Understanding Modified Adjusted Gross Income (MAGI)

While “provisional income” is the term the IRS uses for Social Security taxation, it’s often closely related to a “Modified Adjusted Gross Income” (MAGI) for other tax purposes. For Social Security taxation, your AGI (from line 11 of your Form 1040) is the starting point. To this, you add back any tax-exempt interest you received.

Common sources of income that contribute to your AGI and thus to your provisional income include:

- Wages and salaries: Income from any part-time work or consulting during retirement.

- Self-employment income: Profits from any business activities.

- Pensions and annuities: Regular payments from retirement plans or insurance contracts.

- Taxable interest and dividends: Earnings from savings accounts, CDs, stocks, and mutual funds.

- Capital gains: Profits from selling assets like stocks, bonds, or real estate.

- Traditional IRA and 401(k) distributions: Withdrawals from these pre-tax retirement accounts are fully taxable.

- Rental income: Income from properties you own and rent out.

- Other taxable income: Any other income that is generally subject to federal income tax.

It’s crucial to distinguish between taxable and non-taxable income sources. For example, qualified distributions from a Roth IRA or Roth 401(k) are generally tax-free and do not count towards your provisional income. This is a key advantage of Roth accounts for retirement planning, as it can help keep your provisional income below the Social Security taxation thresholds.

Incorporating Half of Your Social Security Benefits

As mentioned, only half of your total Social Security benefits received during the year is added to your AGI (plus tax-exempt interest) to arrive at your provisional income. This is not half of your monthly benefit, but half of the total annual amount shown on your Form SSA-1099, Social Security Benefit Statement. This form is mailed to you by the Social Security Administration each January and details the total benefits you received in the prior year.

For example, if you received $24,000 in Social Security benefits in a year, you would add $12,000 (half of $24,000) to your AGI and tax-exempt interest to calculate your provisional income.

The “Taxable Social Security Calculator” Explained

Given the complexity of provisional income, the various thresholds, and the 50%/85% rules, a dedicated calculator is an invaluable tool for both current retirees and those planning for retirement.

What a Calculator Does

A “how much of my Social Security is taxable calculator” automates the entire process for you. Instead of manually tallying income sources and applying intricate formulas, the calculator:

- Gathers your inputs: It prompts you for your filing status, total annual Social Security benefits, and other income (often by category like wages, pensions, interest, etc.).

- Calculates your provisional income: It accurately sums your AGI components, tax-exempt interest, and half of your Social Security benefits.

- Applies the thresholds: It compares your provisional income against the relevant IRS thresholds for your filing status.

- Determines the taxable portion: It then uses the 50% and 85% rules to compute the exact dollar amount of your Social Security benefits that will be subject to federal income tax.

- Provides an estimate: It gives you an immediate estimate, allowing you to understand your potential tax liability and adjust your financial plans accordingly.

Manual Calculation vs. Online Tools

While it’s possible to perform a manual calculation using IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits,” this method can be time-consuming and prone to error. The formulas are not intuitive, and missing a single detail can lead to an inaccurate result.

Online calculators, on the other hand, offer several advantages:

- Speed and Efficiency: Get an answer in minutes, not hours.

- Accuracy: Reduces the likelihood of human error in complex calculations.

- Scenario Planning: Many calculators allow you to input different income scenarios (e.g., if you take on a part-time job, or if your investments perform differently) to see how changes affect your taxable benefits. This is crucial for proactive planning.

- Accessibility: Widely available from reputable financial planning websites, government resources (like the IRS website itself sometimes provides links or instructions), and even some tax software providers.

When using an online calculator, always ensure it is from a reputable source to guarantee accuracy and up-to-date information. Look for calculators from established financial institutions, non-profits like AARP, or government-affiliated sites.

Key Inputs for the Calculator

To get an accurate estimate from any Social Security taxable benefits calculator, you’ll need to have the following information readily available:

- Your Tax Filing Status: Single, Married Filing Jointly, Head of Household, Qualifying Widow(er), or Married Filing Separately.

- Total Annual Social Security Benefits: This is the figure reported on Box 5 of your Form SSA-1099.

- Your Other Annual Income: This includes all taxable income sources that contribute to your AGI (wages, pensions, taxable interest, dividends, capital gains, traditional IRA/401(k) distributions, etc.) and any tax-exempt interest.

Providing accurate inputs is paramount; even small discrepancies can lead to incorrect results.

Strategies to Potentially Reduce Social Security Taxation

Understanding the calculation is the first step; the next is exploring strategies to potentially minimize the amount of your Social Security benefits subject to taxation. This often involves managing your provisional income.

Managing Your Provisional Income

Since the taxation of Social Security benefits is directly linked to your provisional income, strategies often revolve around controlling this figure:

- Roth Conversions: Consider converting traditional IRA or 401(k) assets to a Roth IRA during years when your income is lower (e.g., before you start taking Social Security or during early retirement). While you’ll pay taxes on the converted amount, future qualified Roth distributions will be tax-free and won’t count towards provisional income, potentially keeping your taxable Social Security lower in later years.

- Strategic Retirement Account Withdrawals: If you have multiple retirement accounts (e.g., traditional IRA, Roth IRA, taxable brokerage accounts), strategically choose which accounts to draw from. Prioritizing tax-free Roth distributions or drawing from non-qualified taxable accounts (after exhausting your basis) can help keep your AGI, and thus provisional income, lower.

- Tax-Advantaged Investments: Investing in municipal bonds can generate interest income that is tax-exempt at the federal level (and sometimes state and local levels). While this interest is added back to calculate provisional income for Social Security purposes, it may still offer overall tax advantages compared to fully taxable investments, depending on your tax bracket.

- Delaying Social Security: While not directly reducing taxability once benefits begin, delaying Social Security can be a strategy for overall tax planning. By waiting, you accrue delayed retirement credits, leading to higher monthly benefits. This might mean fewer years of benefits being subject to taxation, or it could be part of a broader strategy where other income sources are managed to keep provisional income lower in earlier retirement years.

The Role of Tax Planning

Effective tax planning is crucial, especially in retirement when income sources often diversify.

- Consult a Professional: A qualified financial advisor or tax professional can help you navigate the complexities of Social Security taxation, integrate it into your broader retirement income strategy, and identify personalized opportunities for tax optimization. They can project your income and expenses over time, helping you make informed decisions.

- Understand State Taxation: Beyond federal taxes, some states also tax Social Security benefits. It’s essential to understand the rules in your state of residence, as this can add another layer to your tax planning. As of my last update, a number of states tax Social Security benefits, though many offer exemptions or deductions based on income.

Beyond the Calculator: Planning for Your Financial Future

A Social Security taxable benefits calculator is a powerful diagnostic tool, but it’s just one piece of a larger financial puzzle.

The Impact on Overall Retirement Income

Understanding the taxable portion of your Social Security benefits allows you to accurately budget for your net retirement income. If a significant portion is taxable, it means less money in your pocket than the gross benefit amount might suggest. This realization can inform your spending habits, investment strategies, and overall financial outlook for retirement. It underscores the importance of not just how much income you receive, but how much income you keep after taxes.

Comprehensive Financial Planning

Integrating your Social Security benefits, including their tax implications, into a comprehensive financial plan is vital. This plan should consider:

- All Income Sources: Social Security, pensions, traditional IRA/401(k) withdrawals, Roth IRA distributions, investment income, and any part-time work.

- Expenses: Regular living costs, healthcare expenses, travel, and discretionary spending.

- Asset Allocation: How your investments are structured to provide income while managing risk.

- Estate Planning: How your assets will be distributed.

By taking a holistic view, you can proactively make decisions that optimize your tax situation, ensure sufficient income throughout retirement, and achieve your long-term financial goals.

In conclusion, the question of “how much of my Social Security is taxable” is far from simple, yet critically important. While the rules can seem intricate, tools like the Social Security taxable benefits calculator provide clarity and empowerment. By understanding your provisional income, familiarizing yourself with the thresholds, and leveraging smart tax planning strategies, you can minimize surprises and ensure that your Social Security benefits contribute maximally to the retirement lifestyle you envision. Don’t leave your retirement taxes to chance; use the available resources to plan wisely and confidently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.