Social Security stands as a cornerstone of retirement planning for millions of Americans, providing a crucial financial safety net in later life. However, precisely answering “how much can you make a year on Social Security?” is far from a simple, one-size-fits-all figure. Your annual benefit payment is a highly individualized sum, sculpted by decades of your work history, earnings, and the strategic decisions you make as you approach retirement. This article will demystify the complex calculations and various factors that determine your yearly Social Security income, offering insights into how you can best estimate and potentially maximize this vital retirement resource. Understanding these intricacies is not just about numbers; it’s about securing a more predictable and comfortable financial future.

The Core Formula: How Social Security Benefits Are Calculated

The Social Security Administration (SSA) employs a progressive formula to determine your Primary Insurance Amount (PIA), which is the benefit you receive if you claim at your Full Retirement Age (FRA). This calculation is sophisticated, designed to be fair across different income levels, and primarily hinges on your lifetime earnings.

Average Indexed Monthly Earnings (AIME): Your Earning History Matters

The foundation of your Social Security benefit is your Average Indexed Monthly Earnings (AIME). The SSA doesn’t just look at your raw earnings; it adjusts, or “indexes,” your past earnings to account for changes in the average wage level in the economy over time. This indexing ensures that your earlier earnings are brought up to a more current value, reflecting their purchasing power today.

To calculate your AIME, the SSA takes your 35 highest-earning years, after indexing, and sums them up. If you have worked for fewer than 35 years, the remaining years will be counted as zeros, which can significantly lower your overall average. This highlights the importance of a long and consistent work history with steady or increasing income. The total indexed earnings from these 35 years are then divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings. For instance, a year with low earnings or unemployment can reduce your AIME if it falls within your top 35 years, or if you don’t have 35 years of substantial earnings to choose from.

Primary Insurance Amount (PIA): The Starting Point

Once your AIME is determined, the SSA applies a formula to convert it into your Primary Insurance Amount (PIA). The PIA is the monthly benefit you are entitled to if you begin receiving benefits at your Full Retirement Age (FRA). This formula is progressive, meaning it replaces a higher percentage of earnings for lower-income workers than for higher-income workers.

The PIA formula uses “bend points” – specific dollar amounts that divide your AIME into segments. For example, in 2024, the formula might look something like this (actual bend points vary annually):

- 90% of the first X dollars of AIME

- 32% of AIME between X and Y dollars

- 15% of AIME above Y dollars

These percentages are added together to arrive at your monthly PIA. It’s crucial to understand that your PIA is the foundational figure; all other adjustments, such as claiming early or late, are based on this amount. For a general annual estimate, simply multiply your PIA by 12.

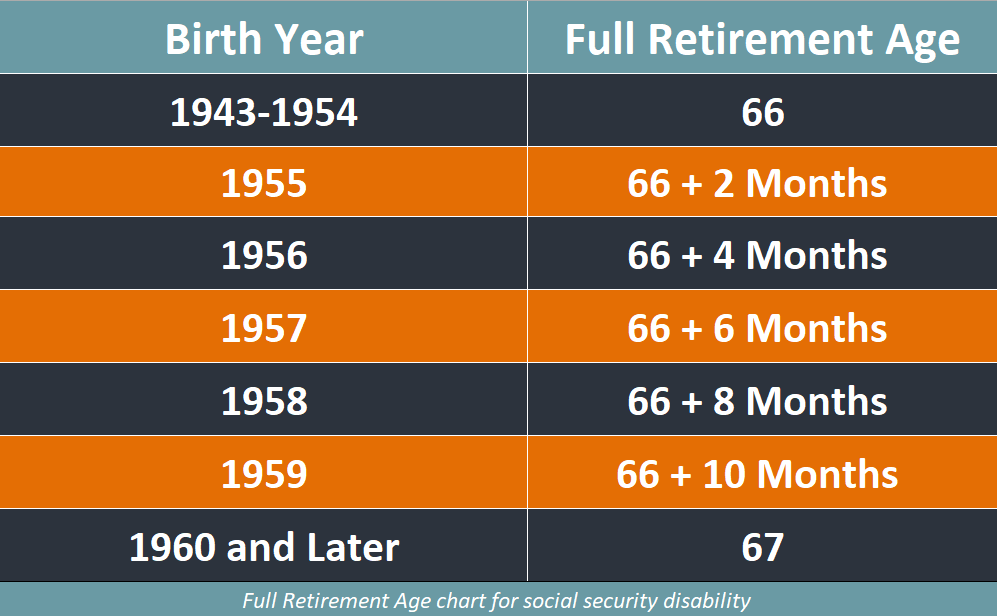

Understanding Your Full Retirement Age (FRA)

Your Full Retirement Age (FRA) is a critical determinant of your annual Social Security income. This is the age at which you are entitled to receive 100% of your PIA. FRA is not a fixed age for everyone; it depends on your birth year. For those born in 1937 or earlier, FRA was 65. For those born between 1943 and 1954, it’s 66. For subsequent birth years, FRA gradually increases, reaching 67 for anyone born in 1960 or later.

Claiming benefits before your FRA results in a permanent reduction of your monthly payment, while delaying benefits past your FRA can permanently increase them. Knowing your specific FRA is therefore essential for strategic retirement planning, as it directly impacts your annual benefit amount.

Key Factors Influencing Your Annual Social Security Income

While the core formula provides a baseline, several other critical factors can significantly alter the annual amount you actually receive from Social Security. These factors range from your continued work status to the timing of your application and even the annual economic landscape.

Your Earning History and the Earnings Limit

As established, a robust earning history is paramount. The higher your average indexed monthly earnings over your 35 top-earning years, the higher your PIA and, consequently, your annual Social Security benefit. Working consistently and aiming for higher wages, particularly earlier in your career, can have a compounding positive effect.

However, if you choose to claim Social Security benefits before your Full Retirement Age (FRA) and continue to work, you may be subject to the Social Security Earnings Limit. This limit allows you to earn a certain amount without penalty. If your earnings exceed this limit, the SSA will temporarily withhold a portion of your benefits. For instance, in 2024, if you are under FRA for the entire year, $1 in benefits is withheld for every $2 you earn above the annual limit (e.g., $22,320). In the year you reach FRA, the limit is higher (e.g., $59,520 in 2024), and $1 in benefits is withheld for every $3 you earn above the limit, up to the month you reach FRA. Once you reach your FRA, the earnings limit no longer applies, and you can earn any amount without your benefits being reduced. Any benefits withheld due to the earnings limit are not lost; they typically result in a recalculation of your benefits at FRA, potentially increasing your monthly payment in the future.

When You Choose to Claim Your Benefits

Perhaps the most significant decision impacting your annual Social Security income is when you decide to start receiving benefits.

- Early Claiming (Age 62): You can begin receiving benefits as early as age 62. However, claiming before your FRA results in a permanent reduction of your monthly benefit. The reduction can be substantial, as much as 25% to 30% depending on your FRA. This means a lower annual income for the rest of your life. For example, if your FRA is 67 and you claim at 62, your monthly benefit will be approximately 70% of your PIA.

- Full Retirement Age (FRA): As discussed, claiming at your FRA entitles you to 100% of your PIA. This is the baseline from which early or delayed claiming adjustments are made.

- Delayed Claiming (Up to Age 70): For every year you delay claiming benefits past your FRA, up to age 70, you earn Delayed Retirement Credits (DRCs). These credits permanently increase your monthly benefit by 8% per year (or 2/3 of 1% per month). This can lead to a significant increase in your annual income. For instance, if your FRA is 67 and you delay claiming until age 70, your monthly benefit will be 124% of your PIA – a substantial boost to your annual income for the remainder of your life.

The decision of when to claim often involves weighing factors like immediate financial need, expected longevity, other retirement income sources, and spousal benefits.

Cost-of-Living Adjustments (COLAs)

To help maintain the purchasing power of Social Security benefits against inflation, the SSA implements annual Cost-of-Living Adjustments (COLAs). Each year, typically in October, the SSA announces whether a COLA will be applied for the following calendar year. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If the CPI-W increases, your annual Social Security benefit will also increase by the determined percentage.

While COLAs are a vital mechanism for preserving your benefit’s value over time, they are not guaranteed every year. In periods of low or no inflation, there may be no COLA, or a very minimal one. However, historically, COLAs have been a consistent feature, providing regular, albeit sometimes modest, boosts to annual Social Security income.

Taxation of Social Security Benefits

It’s important to remember that a portion of your Social Security benefits may be subject to federal income tax, and in some states, state income tax as well. Whether your benefits are taxable depends on your “provisional income,” which is calculated as your adjusted gross income (AGI) plus any tax-exempt interest income, plus one-half of your Social Security benefits.

- Federal Taxation:

- If your provisional income is between $25,000 and $34,000 for an individual ($32,000 to $44,000 for a married couple filing jointly), up to 50% of your benefits may be taxable.

- If your provisional income exceeds $34,000 for an individual ($44,000 for a married couple filing jointly), up to 85% of your benefits may be taxable.

- If your provisional income is below these thresholds, your Social Security benefits are not federally taxed.

- State Taxation: While most states do not tax Social Security benefits, a handful do. It’s important to check the tax laws in your state of residence to understand the full tax implications for your annual Social Security income.

Understanding potential taxation is crucial for accurately forecasting your net annual Social Security income.

Maximizing Your Social Security Benefits: Strategic Considerations

Given the profound impact of various factors, a thoughtful strategy can significantly enhance your annual Social Security income. Maximization isn’t about finding loopholes; it’s about making informed decisions aligned with your financial goals and life circumstances.

Working Longer and Earning More

One of the most direct ways to boost your annual Social Security income is to continue working, especially if you haven’t yet accumulated 35 years of substantial earnings. Each additional year you work, particularly at a higher salary, can replace a lower-earning year (or a zero-earning year) in your 35-year average. This directly increases your Average Indexed Monthly Earnings (AIME) and, consequently, your Primary Insurance Amount (PIA). Even if you have 35 years of earnings, replacing a relatively low-earning year with a higher one can still improve your overall average. Therefore, strategic career planning and considering working an extra few years can have a lasting positive effect on your lifetime benefits.

Strategic Claiming Decisions

The timing of your benefit claim is arguably the most impactful decision. While claiming early at age 62 provides immediate income, it comes with a significant and permanent reduction in your monthly (and thus annual) benefit. Conversely, delaying your claim up to age 70 can result in a substantially higher annual income due to Delayed Retirement Credits.

The “optimal” claiming age is highly personal and depends on several factors:

- Longevity: If you expect to live a long life, delaying benefits often yields a higher total lifetime benefit, despite fewer years of receiving payments.

- Health: Poor health might suggest claiming earlier to receive benefits for as long as possible.

- Other Income Sources: If you have ample savings, pensions, or other retirement income, you might have the flexibility to delay claiming and maximize your Social Security.

- Spousal and Survivor Benefits: These can complicate the decision, especially for married couples where one spouse might have significantly higher earnings.

A thorough analysis, sometimes involving a “breakeven point” calculation (the age at which the cumulative total from delaying benefits surpasses the cumulative total from claiming early), is often advisable.

Understanding Spousal and Survivor Benefits

Social Security is not just for individual workers; it also provides benefits for spouses, ex-spouses, and survivors, which can significantly increase a household’s annual Social Security income.

- Spousal Benefits: If you are married, you may be eligible to receive a spousal benefit equal to up to 50% of your spouse’s PIA, provided your own benefit based on your work record is less than this amount. This can be a vital component of retirement income for couples, especially if one spouse had a much lower earning history.

- Divorced Spouse Benefits: You may be able to claim benefits on an ex-spouse’s record if the marriage lasted at least 10 years, you are currently unmarried, and both you and your ex-spouse are at least 62.

- Survivor Benefits: After the death of a spouse or ex-spouse, eligible family members (widows, widowers, and sometimes children) can receive survivor benefits. A widow(er) can receive up to 100% of the deceased worker’s benefit.

Understanding these auxiliary benefits is critical for couples and individuals alike, as they can represent a substantial addition to the annual Social Security income for a household. Strategic claiming decisions for spousal and survivor benefits are complex and often require careful planning.

Practical Steps to Estimate Your Social Security Income

While the calculations can seem daunting, the Social Security Administration provides excellent resources to help you accurately estimate your potential annual income. Taking proactive steps to review these estimates is a fundamental part of responsible retirement planning.

Using Your Social Security Statement

The most direct and personalized way to estimate your Social Security benefits is through your Social Security Statement. This statement provides a detailed summary of your earnings history and personalized estimates of your future benefits at different claiming ages (e.g., age 62, Full Retirement Age, and age 70).

You can easily access your statement by creating a free, secure online “my Social Security” account on the SSA website (www.ssa.gov). Once logged in, you can view your earnings record, check for inaccuracies, and get updated benefit estimates based on your actual earnings. The statement typically projects your benefits based on your current earnings continuing until retirement, offering a realistic snapshot of your potential annual income.

Social Security Administration’s Online Tools

Beyond the personal statement, the SSA website offers a suite of online tools and calculators that can help you explore various scenarios:

- Retirement Estimator: This tool allows you to plug in different earnings and retirement dates to see how changes might affect your benefit amounts. It’s excellent for “what if” scenarios, such as how working an extra year or delaying your claim might impact your annual income.

- Benefit Calculators: Other calculators can help you estimate spousal, divorced spouse, or survivor benefits, providing a comprehensive view of potential household income.

- Life Expectancy Calculator: While not directly a benefit calculator, understanding your projected life expectancy can inform your claiming strategy.

These tools are invaluable for personal financial planning and can help you visualize the long-term impact of your decisions on your annual Social Security income.

Consulting a Financial Advisor

For complex situations, such as coordinating Social Security benefits with other retirement accounts (401(k)s, IRAs), managing taxation of benefits, or making intricate decisions about spousal and survivor benefits, consulting a qualified financial advisor is highly recommended. A financial advisor specializing in retirement planning can offer personalized guidance, help you run detailed projections, and develop a comprehensive strategy that integrates Social Security into your overall financial plan. They can assist in understanding the nuances of your specific situation and optimizing your claiming strategy to maximize your annual Social Security income and ensure it aligns with your broader financial goals.

Conclusion

Determining “how much you can make a year on Social Security” involves understanding a multi-faceted system driven by your earning history, Full Retirement Age, and crucially, your claiming decisions. Your Average Indexed Monthly Earnings (AIME) forms the bedrock, leading to your Primary Insurance Amount (PIA), which can then be adjusted significantly by choosing to claim early, at full retirement age, or delaying until age 70. Factors like annual Cost-of-Living Adjustments (COLAs) and potential taxation further refine your net annual income.

By strategically maximizing your earnings history, making informed choices about when to claim, and understanding the potential for spousal or survivor benefits, you can significantly influence your annual Social Security income. Utilizing the SSA’s online resources, such as your personal Social Security Statement and various estimators, is vital for accurate forecasting. For intricate situations, professional financial advice can be invaluable. Social Security is a fundamental pillar of retirement security; proactively engaging with its rules and your personal situation is key to ensuring it provides the most robust financial support possible throughout your retirement years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.