Understanding your monthly income is the bedrock of sound personal finance. It dictates your budgeting capacity, savings potential, and overall financial health. Yet, for many, the seemingly simple act of calculating this figure can be surprisingly complex, especially when juggling multiple income streams, varying pay cycles, and an array of deductions. This guide will demystify the process, offering a comprehensive framework to accurately determine what funds flow into your accounts each month.

Deconstructing Your Income: Gross vs. Net

Before diving into specific calculations, it’s crucial to distinguish between gross and net income. These two figures represent entirely different aspects of your earnings and are fundamental to accurate financial planning.

Gross Income: The Starting Point

Gross income is the total amount of money you earn before any deductions are taken out. This is the figure often quoted in job offers or contract agreements. For employees, it includes your base salary or hourly wages, along with any bonuses, commissions, tips, overtime pay, and taxable benefits. For the self-employed, it encompasses all revenue generated from your business activities before business expenses are subtracted.

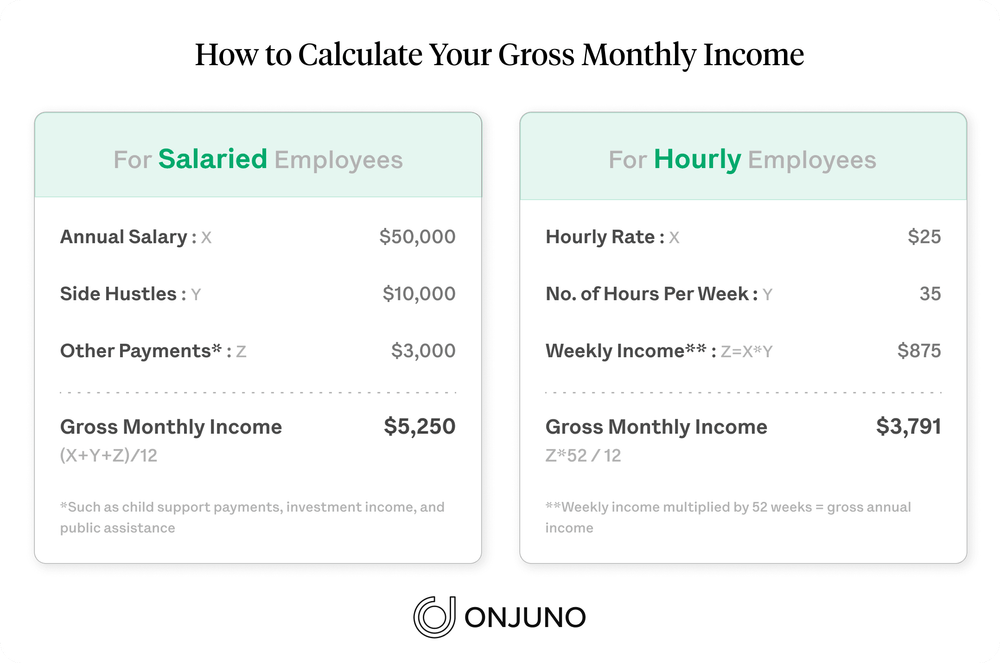

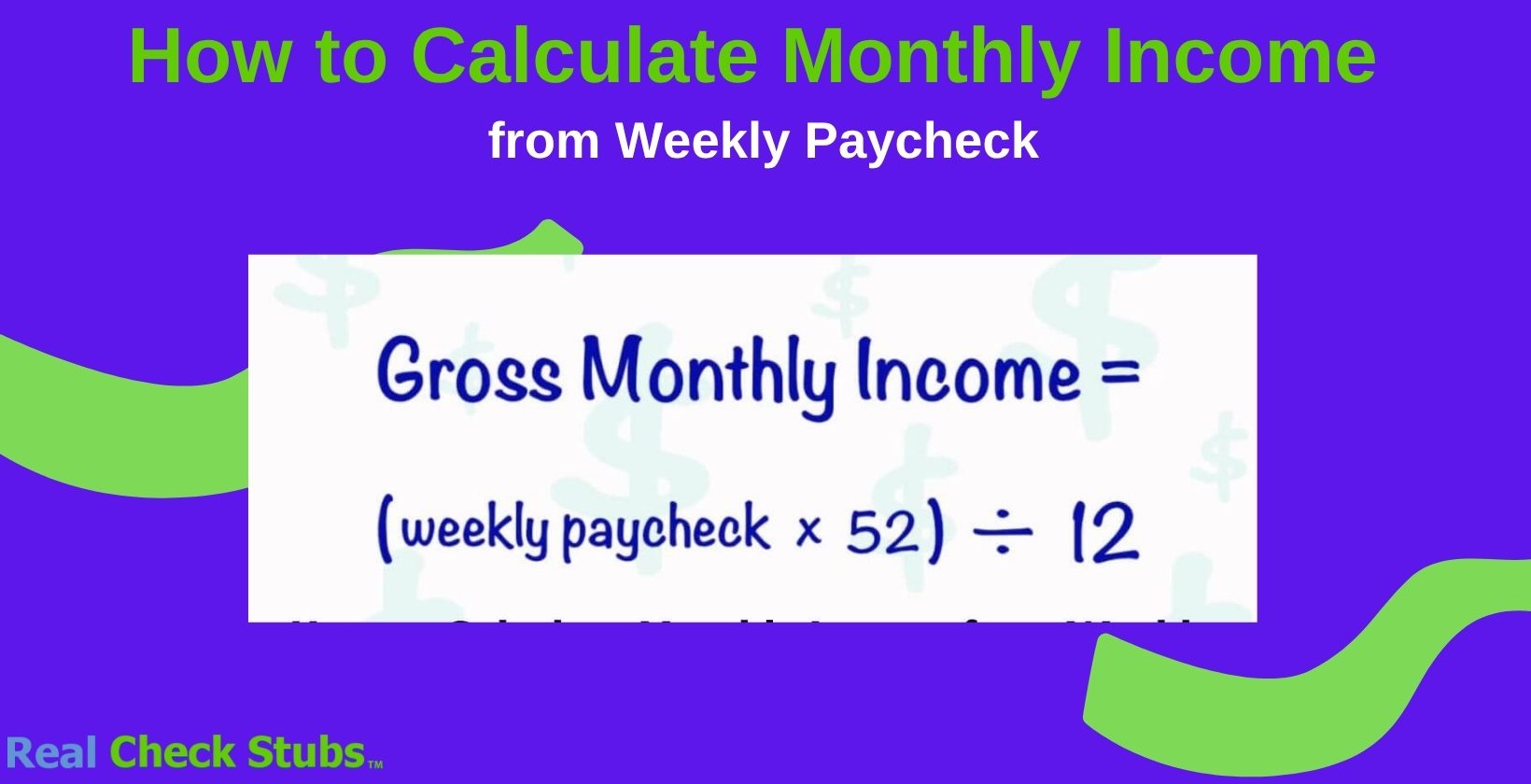

Calculating your gross monthly income is straightforward for salaried individuals: simply divide your annual salary by 12. For hourly workers, multiply your hourly rate by the number of hours worked in a month (accounting for any overtime). If your income varies, tracking your total gross earnings for a few months and then averaging them can provide a more realistic monthly figure.

Net Income: What You Actually Take Home

Net income, often referred to as “take-home pay,” is the amount of money you receive after all mandatory and voluntary deductions have been subtracted from your gross income. This is the figure that actually lands in your bank account and is the most important number for budgeting purposes.

Key Deductions and Their Impact

A variety of deductions can significantly reduce your gross income. Understanding these is vital for calculating your true take-home pay:

- Federal and State Income Taxes: These are withheld from your paycheck based on your W-4 (for employees) or estimated quarterly payments (for self-employed individuals). The amount depends on your income level, filing status, and dependents.

- Social Security and Medicare Taxes (FICA): These are mandatory payroll taxes that fund social security and Medicare programs. Employees typically pay half, with employers covering the other half, while self-employed individuals pay the full amount (self-employment tax).

- Retirement Contributions: Deductions for 401(k), 403(b), or other employer-sponsored retirement plans reduce your taxable income, potentially lowering your current tax liability. These are crucial for long-term financial security.

- Health Insurance Premiums: If your employer offers health, dental, or vision insurance, your share of the premiums is often deducted from your paycheck, usually pre-tax.

- Life Insurance and Disability Insurance: Premiums for these types of coverage, if offered through your employer, may also be deducted.

- Other Voluntary Deductions: This can include contributions to Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), union dues, loan repayments (e.g., 401(k) loans), or charitable contributions made through payroll deduction.

To calculate your net monthly income, you must subtract the sum of all these deductions from your gross monthly income. This will give you the most accurate representation of the funds available for your living expenses, savings, and discretionary spending.

A Comprehensive Guide to Calculating Diverse Income Streams

The way you calculate your monthly income changes significantly depending on its source. A holistic view requires accounting for all funds you receive, no matter how irregular or unconventional.

Salaried Employment: Simple Yet Nuanced

For salaried employees, calculating gross monthly income is usually straightforward: divide your annual salary by 12. However, the net calculation requires careful attention to your pay stub. Access your latest pay stub to identify all deductions. If you are paid bi-weekly or semi-monthly, remember that some months will have three paychecks, impacting your overall monthly net income. For a consistent monthly figure, it’s often best to calculate your average monthly net pay by summing a year’s worth of net pay and dividing by 12.

Hourly Wages: Tracking Time for Accuracy

Hourly workers must meticulously track their hours. Multiply your hourly rate by the total regular hours worked in a month. Add any overtime pay (which is typically paid at 1.5 times your regular rate) and tips. As with salaried positions, consult your pay stubs to account for deductions and arrive at your net monthly income. Consistent logging of hours is critical, especially for roles with fluctuating schedules.

Freelance, Contract, and Gig Economy Earnings

This category often presents the most variability. Freelancers and contract workers might be paid per project, per hour, or on retainer. Gig economy participants (e.g., ride-share drivers, delivery services) have highly variable earnings.

To calculate monthly income here:

- Track all incoming payments: Keep detailed records of every invoice paid and every payment received.

- Estimate expenses: Freelancers and gig workers have significant business expenses (e.g., fuel, software subscriptions, home office deductions). While these are typically subtracted at tax time, understanding their impact on your actual take-home cash is vital for budgeting. For monthly income calculation, focus on gross receipts first, then understand that a percentage will be allocated for taxes and expenses.

- Account for self-employment tax: Unlike employees, you are responsible for both the employer and employee portions of FICA taxes. It’s prudent to set aside approximately 25-35% of your gross freelance income for taxes.

- Average highly variable income: If your income fluctuates wildly, average your earnings over 3-6 months to establish a more reliable monthly figure for budgeting. Some months you might earn more, others less, but an average provides stability for planning.

Business and Self-Employment Income

For small business owners, calculating monthly income involves a more complex formula: Total Revenue – Cost of Goods Sold – Operating Expenses = Gross Profit. From this gross profit, you’ll subtract owner draws or salaries. It’s crucial to distinguish between business revenue and your personal income. Often, business owners pay themselves a salary, which then falls under “salaried employment” for personal income calculation, or take owner’s draws. Always maintain clear separation between business and personal finances. For personal income purposes, focus on the consistent salary or the average of your owner’s draws after business expenses and taxes are accounted for.

Passive Income: Rental Properties, Investments, and Royalties

Passive income streams also contribute to your monthly income, though they often require their own set of calculations.

- Rental Income: Gross rent received minus property expenses (mortgage interest, property taxes, insurance, maintenance, vacancy reserves) equals your net rental income. Remember to budget for irregular large expenses like repairs.

- Investment Income: This includes dividends from stocks, interest from savings accounts or bonds, and distributions from mutual funds. Many of these are paid quarterly or annually, so you’ll need to annualize them and then divide by 12 to get a monthly average. Be aware that investment income can fluctuate based on market performance.

- Royalties: Income from books, music, patents, or other intellectual property can be highly variable. Average these over a period to get a monthly estimate.

Other Irregular Income Sources

Don’t overlook less frequent or one-off income sources. This could include tax refunds (though often best treated as a bonus rather than regular income), severance pay, alimony or child support payments, or one-time bonuses. While these shouldn’t be relied upon for regular monthly budgeting, they contribute to your overall financial picture and can be factored into specific savings goals or debt reduction efforts.

The Strategic Value of Knowing Your Monthly Income

Accurately calculating your monthly income isn’t merely an accounting exercise; it’s a foundational step towards achieving financial stability and realizing your monetary aspirations.

Budgeting and Expense Management

Your net monthly income is the absolute limit of what you can spend without going into debt. Knowing this figure precisely allows you to create a realistic budget, allocating funds for necessities (housing, food, utilities), discretionary spending (entertainment, dining out), and critical financial goals (savings, debt repayment). Without this anchor, budgeting becomes a guessing game, leading to potential overspending and financial stress. It enables you to identify areas where you might be spending too much and to make informed adjustments.

Debt Management and Repayment Strategies

When tackling debt, particularly high-interest consumer debt, your available monthly income dictates your capacity for accelerated repayment. A clear understanding of your take-home pay allows you to determine how much extra you can realistically put towards loans, which in turn shortens repayment timelines and saves on interest. It also helps you assess the affordability of new debt, such as a mortgage or car loan, ensuring your payments remain manageable within your financial framework.

Financial Goal Setting and Saving

Whether you’re saving for a down payment, retirement, a child’s education, or an emergency fund, your monthly income directly impacts how quickly you can achieve these goals. Knowing your income enables you to set ambitious yet attainable savings targets and to track your progress effectively. It empowers you to allocate specific percentages or fixed amounts of your income to various savings vehicles, transforming vague aspirations into concrete plans.

Planning for Taxes and Future Obligations

For self-employed individuals and those with significant investment income, accurately calculating monthly earnings is paramount for setting aside funds for estimated quarterly taxes. Underestimating income can lead to penalties and a significant tax bill come April. Furthermore, understanding your consistent income stream helps in planning for larger, irregular expenses like insurance premiums, property taxes, or annual subscriptions, ensuring these don’t derail your monthly budget.

Leveraging Financial Tools for Precision and Simplicity

While manual calculations are a good starting point, several tools can streamline the process of tracking and analyzing your monthly income, offering greater accuracy and insight.

Spreadsheets: The DIY Approach

Microsoft Excel, Google Sheets, or similar programs offer robust capabilities for income tracking. You can create custom templates to list all income sources, deductions, and calculate your net monthly take-home pay. Spreadsheets provide flexibility for modeling different scenarios, forecasting income, and integrating with budgeting templates. They require a bit more manual input but offer unparalleled customization and control.

Budgeting Apps and Software

Numerous personal finance apps and software solutions are designed to automate income tracking and budgeting. Platforms like Mint, YNAB (You Need A Budget), Personal Capital, or Simplifi can link directly to your bank accounts and investment platforms, automatically categorizing transactions and providing real-time insights into your income and spending. These tools often generate reports, graphs, and alerts, making it easier to visualize your financial flow and stay on track with your goals. Many offer features for setting financial goals, tracking investments, and managing debt.

Consulting a Financial Advisor

For complex financial situations, such as managing a diverse portfolio of investments, multiple businesses, or significant inheritance, engaging a financial advisor can be invaluable. A professional can help you consolidate your income data, factor in long-term financial planning, optimize tax strategies, and provide personalized advice tailored to your unique circumstances. While an investment, a good advisor can save you money and stress in the long run by ensuring all income streams are properly accounted for and integrated into a cohesive financial strategy.

Ultimately, mastering the calculation of your monthly income is an ongoing process that requires attention to detail and a commitment to financial transparency. By understanding your gross and net earnings, meticulously tracking all sources, and leveraging appropriate tools, you empower yourself to make informed financial decisions, build wealth, and achieve lasting financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.