Percentages are a fundamental mathematical concept with pervasive applications in our financial lives. From understanding sales discounts and interest rates on loans to analyzing investment returns and budgeting effectively, a solid grasp of percentage calculation is indispensable for informed financial decision-making. Far from being a mere academic exercise, calculating percentages empowers individuals and businesses to quantify change, compare proportions, and assess financial performance with precision. This guide will demystify the process, grounding each step in practical financial scenarios.

The Foundational Math: Understanding the Basics

At its core, a percentage represents a part of a whole expressed as a fraction of 100. The term “percent” literally means “per hundred.” This universal language allows for easy comparison of ratios, even when the original whole amounts differ significantly.

The Core Formula: Part / Whole * 100

The most fundamental formula for calculating a percentage is straightforward:

Percentage = (Part / Whole) × 100

- Part: This is the specific amount or quantity you want to express as a percentage of the whole.

- Whole: This is the total amount, the original value, or the base figure against which the part is being compared.

- 100: Multiplying by 100 converts the resulting decimal or fraction into a percentage format.

Example 1: Calculating a Budget Allocation

Suppose your monthly income (whole) is $4,000, and you spend $800 on groceries (part). To find what percentage of your income goes to groceries:

Percentage = ($800 / $4,000) × 100 = 0.20 × 100 = 20%

This tells you 20% of your income is allocated to groceries, a crucial insight for budgeting.

Converting Decimals and Fractions

Percentages, decimals, and fractions are different ways of expressing the same proportional relationship. Understanding how to convert between them is vital for financial literacy.

- Decimal to Percentage: Multiply the decimal by 100.

- Example: An interest rate of 0.05 as a decimal is 0.05 × 100 = 5%.

- Percentage to Decimal: Divide the percentage by 100.

- Example: A 15% tax rate is 15 / 100 = 0.15 as a decimal, which is often used in calculations.

- Fraction to Percentage: First, convert the fraction to a decimal by dividing the numerator by the denominator, then multiply by 100.

- Example: If an investment returned 1/4 of its initial value, this is (1 ÷ 4) × 100 = 0.25 × 100 = 25%.

Mastering these conversions ensures flexibility when working with various financial data formats.

Percentages in Personal Finance: Everyday Applications

Percentages are woven into the fabric of daily personal finance, influencing everything from your shopping choices to your long-term financial planning.

Sales Discounts and Markups

Shopping savvy often hinges on understanding percentage discounts.

Example 2: Discount Calculation

A new appliance originally costs $500 and is on sale for 20% off.

Discount Amount = 20% of $500 = 0.20 × $500 = $100

Sale Price = Original Price – Discount Amount = $500 – $100 = $400

Conversely, markups determine retail prices. If a store buys an item for $100 and applies a 50% markup:

Markup Amount = 50% of $100 = 0.50 × $100 = $50

Selling Price = Cost + Markup Amount = $100 + $50 = $150

Calculating Tips and Service Charges

Tipping is a common social practice, often calculated as a percentage of the bill.

Example 3: Tipping

For a restaurant bill of $75, if you wish to leave a 15% tip:

Tip Amount = 15% of $75 = 0.15 × $75 = $11.25

Total Payment = Bill + Tip = $75 + $11.25 = $86.25

Understanding Interest Rates (Simple vs. Compound)

Interest rates, expressed as percentages, dictate the cost of borrowing money and the return on savings or investments.

- Simple Interest: Calculated only on the principal amount.

Example 4: Simple Interest

You borrow $1,000 at a simple interest rate of 5% per year for 2 years.

Annual Interest = 5% of $1,000 = 0.05 × $1,000 = $50

Total Interest (2 years) = $50 × 2 = $100 - Compound Interest: Calculated on the initial principal and on the accumulated interest from previous periods. This is why it’s often called “interest on interest” and is crucial for understanding long-term savings growth.

Example 5: Compound Interest

You invest $1,000 at an annual compound interest rate of 5%.

Year 1 Interest = 0.05 × $1,000 = $50. New Principal = $1,050.

Year 2 Interest = 0.05 × $1,050 = $52.50. New Principal = $1,102.50.

The total interest is $50 + $52.50 = $102.50, more than simple interest for the same period.

Budgeting and Expense Tracking

Effective budgeting relies heavily on understanding percentages.

Example 6: Budgeting Rules

The “50/30/20 rule” suggests allocating 50% of income to needs, 30% to wants, and 20% to savings/debt repayment. For a $5,000 monthly income:

Needs = 50% of $5,000 = $2,500

Wants = 30% of $5,000 = $1,500

Savings/Debt = 20% of $5,000 = $1,000

This framework uses percentages to simplify financial planning and ensure a balanced approach to spending and saving.

Percentages in Business Finance & Investing: Strategic Insights

Beyond personal finance, percentages are critical analytical tools for businesses and investors to gauge performance, growth, and profitability.

Gross and Net Profit Margins

Profitability metrics are almost always expressed as percentages.

- Gross Profit Margin: Measures the percentage of revenue left after deducting the cost of goods sold (COGS).

Formula: (Gross Profit / Revenue) × 100

Example 7: Gross Profit Margin

If a company has $1,000,000 in revenue and COGS of $600,000:

Gross Profit = $1,000,000 – $600,000 = $400,000

Gross Profit Margin = ($400,000 / $1,000,000) × 100 = 40% - Net Profit Margin: Measures the percentage of revenue remaining after all expenses, including COGS, operating expenses, interest, and taxes, have been deducted.

Formula: (Net Profit / Revenue) × 100

This percentage indicates how much profit a company makes for every dollar of sales.

Return on Investment (ROI)

ROI is a widely used metric to evaluate the efficiency of an investment or to compare the efficiency of several different investments.

Formula: ((Net Return on Investment – Cost of Investment) / Cost of Investment) × 100

Example 8: ROI Calculation

You invest $10,000 in a stock, and it grows to $12,000.

Net Return = $12,000 – $10,000 = $2,000

ROI = ($2,000 / $10,000) × 100 = 20%

A positive ROI indicates a gain, while a negative ROI signifies a loss.

Analyzing Market Share and Growth

Businesses use percentages to understand their position in the market and track expansion.

Example 9: Market Share

If the total market for a product is $10 million, and Company A sells $2 million worth of that product:

Market Share = ($2,000,000 / $10,000,000) × 100 = 20%

Example 10: Revenue Growth Rate

If a company’s revenue increased from $500,000 last year to $600,000 this year:

Growth (Absolute) = $600,000 – $500,000 = $100,000

Growth Rate = ($100,000 / $500,000) × 100 = 20%

Investment Portfolio Performance

Investors frequently track their portfolio’s performance using percentages to easily compare returns across different assets or over different timeframes.

Example 11: Portfolio Return

If your investment portfolio started the year at $100,000 and ended at $108,000 (after all contributions and withdrawals are accounted for, or by calculating the percentage change in value only):

Portfolio Return = (($108,000 – $100,000) / $100,000) × 100 = 8%

Advanced Scenarios & Common Pitfalls

While basic percentage calculations are straightforward, certain scenarios demand careful attention to avoid misinterpretation.

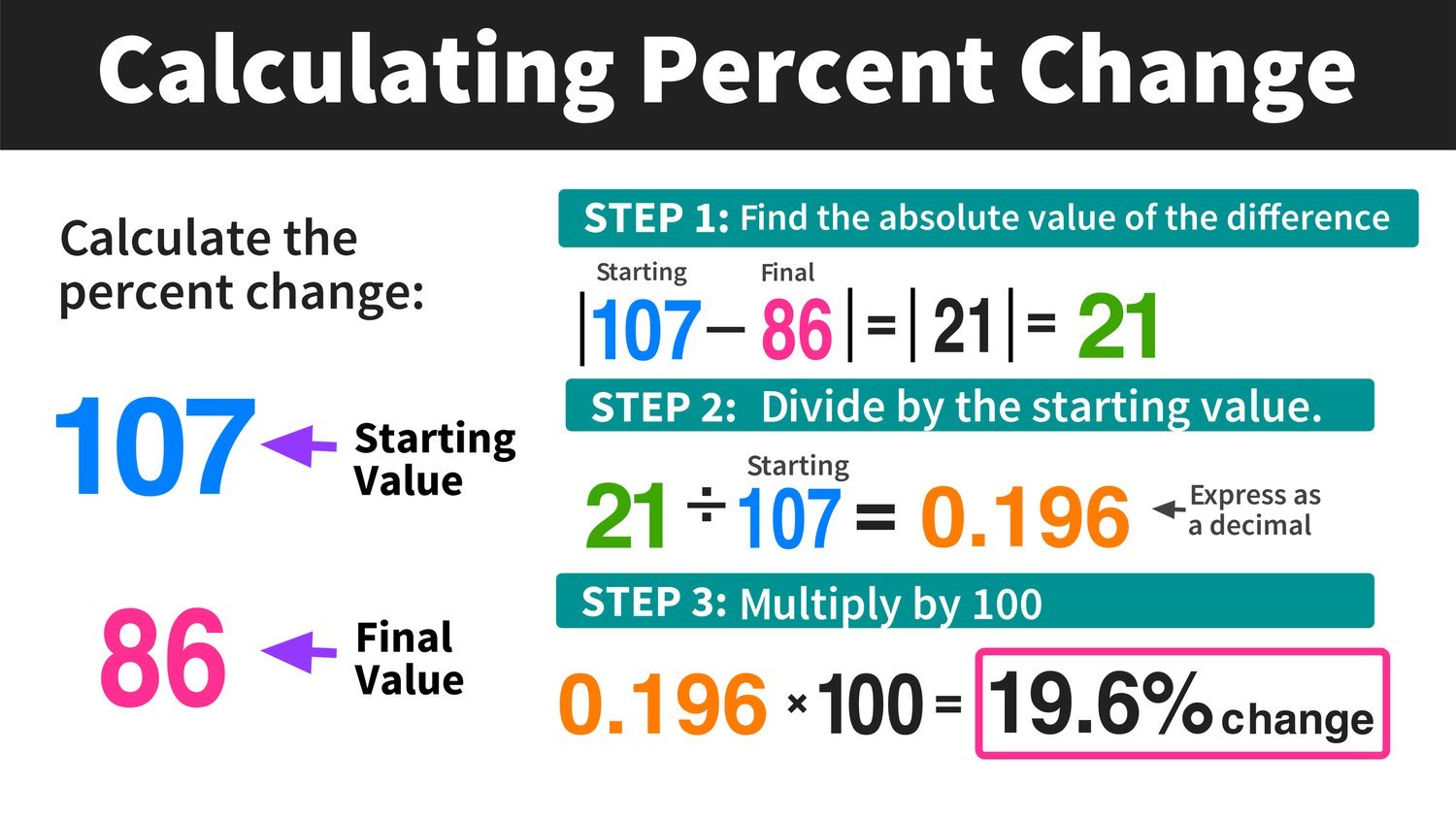

Percentage Increase and Decrease

Calculating the percentage change between two values is common in finance.

- Percentage Increase: ((New Value – Original Value) / Original Value) × 100

Example 12: Stock Price Increase

A stock’s price went from $50 to $60.

Percentage Increase = (($60 – $50) / $50) × 100 = ($10 / $50) × 100 = 0.20 × 100 = 20% - Percentage Decrease: ((Original Value – New Value) / Original Value) × 100

Example 13: Stock Price Decrease

A stock’s price went from $60 to $50.

Percentage Decrease = (($60 – $50) / $60) × 100 = ($10 / $60) × 100 ≈ 0.1667 × 100 = 16.67%

Notice that a $10 increase from $50 is a 20% rise, but a $10 decrease from $60 is a 16.67% drop. The base value matters significantly.

The Importance of the Base Value

A common error is confusing the “whole” or “original value” when calculating percentages. Always be clear about what constitutes the 100% reference point.

Example 14: Confusing the Base

If an item’s price is increased by 20% and then decreased by 20%, it does not return to its original price.

Original Price: $100

Increase by 20%: $100 + (0.20 × $100) = $120

Decrease by 20% (of new price): $120 – (0.20 × $120) = $120 – $24 = $96

The final price is $96, not $100, because the 20% decrease was applied to a higher base ($120) than the 20% increase ($100).

Understanding Basis Points

In financial markets, especially for interest rates, bond yields, and fee structures, basis points (bps) are often used to express percentage changes that are less than one percent. One basis point is equal to 0.01% or 0.0001.

Example 15: Basis Points

If an interest rate increases by 25 basis points:

25 bps = 25 × 0.01% = 0.25%

If the rate was 3.50%, it would become 3.50% + 0.25% = 3.75%.

Using basis points avoids ambiguity when discussing small percentage shifts.

Tools and Strategies for Accuracy

While mental math is useful for quick estimates, leveraging technology ensures precision, especially with complex financial calculations.

Spreadsheet Formulas (Excel, Google Sheets)

Spreadsheets are invaluable for financial modeling and analysis.

- To calculate a percentage: If you have “Part” in cell A1 and “Whole” in cell B1, the formula

= (A1/B1)*100will give you the percentage. - To find a part given a percentage and a whole: If you have a percentage (as a decimal) in C1 and “Whole” in B1,

= C1*B1gives you the part. - To calculate percentage change:

=( (New_Value - Old_Value) / Old_Value ) * 100

Financial Calculators and Online Tools

Dedicated financial calculators (physical or app-based) often have specific functions for percentages, interest, and loans. Many online percentage calculators also exist for quick checks. While convenient, always understand the underlying formula to ensure the tool is being used correctly for your specific financial question.

Double-Checking Your Work

For critical financial decisions, always double-check your calculations. A small error in a percentage can lead to significant discrepancies in budgeting, investment returns, or loan repayments over time. Use multiple methods or tools to verify results, especially when dealing with large sums or long-term projections.

A thorough understanding of how to calculate and interpret percentages is more than just a math skill; it’s a cornerstone of financial literacy that empowers you to manage your money, evaluate opportunities, and make sound financial decisions in a world driven by numbers.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.