Understanding how interest accrues on a daily basis is a cornerstone of financial literacy. Whether you’re a saver watching your money grow, a borrower managing debt, or a business owner optimizing cash flow, daily interest calculations play a critical role in determining your financial outcomes. It’s not just an abstract financial concept; it’s a tangible factor that impacts your savings, the cost of your loans, and the efficiency of your investments. Many people are familiar with annual interest rates, but the power and peril often lie in how that interest is compounded and applied on a day-to-day schedule. Mastering this calculation empowers you to make smarter financial decisions, avoid unnecessary costs, and accelerate your wealth accumulation. This comprehensive guide will demystify daily interest, providing you with the formulas, practical examples, and insights needed to navigate the financial landscape with confidence.

Understanding the Fundamentals of Interest Calculation

Before diving into the specifics of daily interest, it’s crucial to establish a solid foundation in the core principles of how interest works. This will provide the necessary context for understanding why daily calculations are so impactful.

What is Daily Interest?

Daily interest refers to the amount of interest charged or earned on a principal sum over a single day. Instead of interest being calculated annually or monthly, it is determined each day based on the outstanding balance. This method is prevalent in various financial products, including savings accounts, money market accounts, credit cards, and certain types of loans. The key distinction is the frequency of calculation and application, which, as we’ll see, can significantly alter the total interest paid or received over time. For savers, daily interest means your earnings start compounding sooner. For borrowers, it means interest charges can escalate more rapidly if balances are not managed.

Simple vs. Compound Interest: A Crucial Distinction

The world of interest fundamentally divides into two main types: simple and compound.

- Simple Interest is calculated only on the initial principal amount. It remains constant throughout the loan or investment period, assuming the principal doesn’t change. For example, if you borrow $1,000 at 5% simple annual interest, you’ll pay $50 in interest each year, regardless of how long you’ve had the loan. Simple daily interest would be a fraction of that annual amount applied daily.

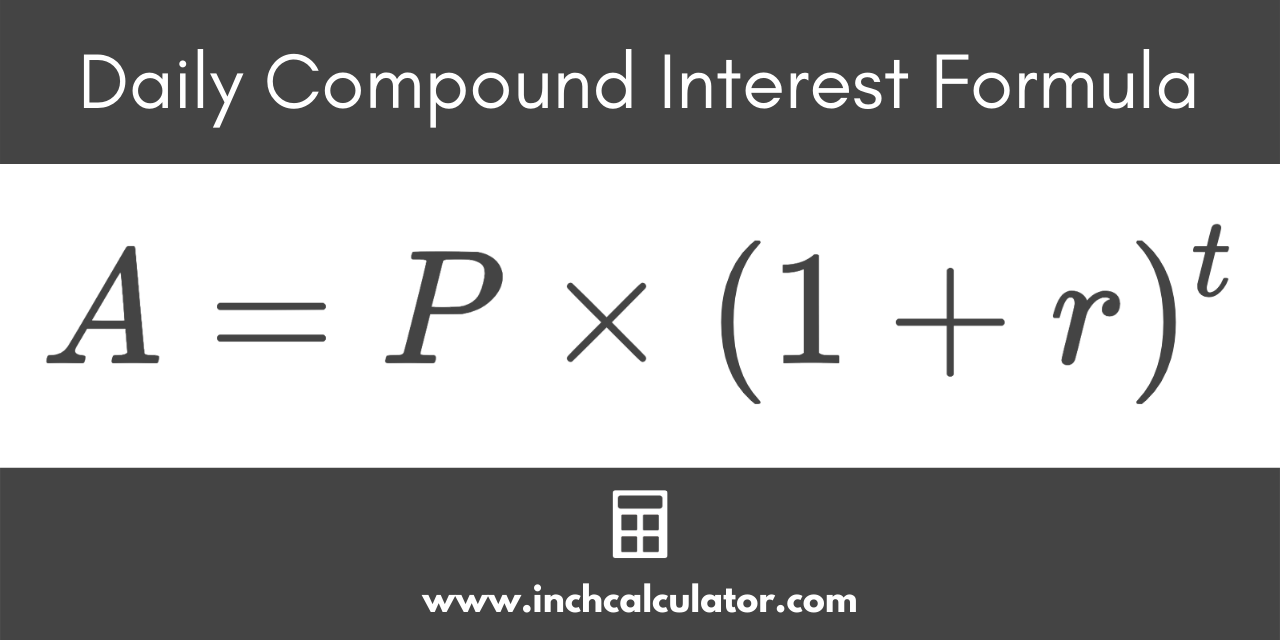

- Compound Interest is calculated on the principal amount and on the accumulated interest from previous periods. This is often referred to as “interest on interest” and is the engine behind exponential growth (or debt). When interest is compounded daily, the interest earned or charged one day is added to the principal, and the next day’s interest is calculated on this new, slightly larger principal. This frequent compounding is why even small differences in rates or balances can lead to substantial long-term variations.

Annual Percentage Rate (APR) vs. Annual Equivalent Rate (AER/APY)

When discussing interest, you’ll often encounter APR and AER (or APY in the U.S.), and understanding their relationship to daily interest is vital:

- APR (Annual Percentage Rate) represents the annual cost of borrowing or earning, expressed as a percentage. It typically reflects the simple interest rate over a year. However, it often doesn’t account for compounding frequency. A loan with a 10% APR might have interest calculated daily, which means the effective rate you pay might be slightly higher due to compounding.

- AER (Annual Equivalent Rate) or APY (Annual Percentage Yield) is a more accurate measure, especially for savings and investments. It reflects the effective annual rate of return, taking into account the effects of compounding over a year. If an account offers interest compounded daily, its AER/APY will typically be slightly higher than its simple annual rate because it includes the benefit of interest earning interest throughout the year. For borrowers, understanding the AER/APY helps compare the true cost of loans where interest compounds differently.

The Core Formula for Daily Interest

At the heart of daily interest calculation lies a straightforward mathematical formula that allows you to determine precisely how much interest accrues each day.

The Basic Daily Interest Formula

The most fundamental formula to calculate daily interest is:

Daily Interest = (Principal Amount × Annual Interest Rate) / Number of Days in the Year

Let’s break down each component:

- Principal Amount: This is the initial sum of money borrowed or invested, or the outstanding balance on which interest is calculated.

- Annual Interest Rate: This is the nominal interest rate, expressed as a decimal. For example, if the annual rate is 5%, you would use 0.05 in the calculation. It’s crucial to use the annual rate before dividing it by the number of days.

- Number of Days in the Year: This is typically 365 days (or 366 in a leap year). For simplicity and consistency, many financial institutions use 365 days even in a leap year, but always confirm the specific methodology.

Step-by-Step Calculation Guide

Let’s illustrate with an example:

Suppose you have a savings account with a principal balance of $10,000 and an annual interest rate of 3%. We’ll assume 365 days in the year.

-

Convert the Annual Interest Rate to a Decimal:

3% = 0.03 -

Apply the Formula:

Daily Interest = ($10,000 × 0.03) / 365 -

Calculate the Annual Interest Amount First:

$10,000 × 0.03 = $300 (This is the annual simple interest) -

Divide by the Number of Days:

$300 / 365 ≈ $0.8219

So, in this scenario, your account would earn approximately $0.82 in interest each day.

Adjusting for Compounding

The basic formula calculates the simple daily interest. However, most financial products operate on a compound interest basis, especially when daily interest is involved. When interest is compounded daily, the interest earned on day 1 is added to the principal, and day 2’s interest is calculated on this new, slightly higher principal.

To reflect daily compounding over multiple days, you’d calculate the daily interest, add it to the principal, and then use that new total as the principal for the next day’s calculation. This iterative process is best managed using a spreadsheet or financial software.

For example, using the above $10,000 at 3% annual rate, earning $0.8219 on day 1:

- End of Day 1 Principal: $10,000 + $0.8219 = $10,000.8219

- Daily Interest for Day 2: ($10,000.8219 × 0.03) / 365 ≈ $0.8220

As you can see, the daily interest subtly increases each day due to the compounding effect. Over a year, this small daily difference accumulates into a noticeable total, reflected in the AER/APY being higher than the simple annual rate.

Practical Applications: Where Daily Interest Matters Most

Daily interest calculations are not just theoretical; they have profound implications across various financial products and situations. Understanding these applications can significantly impact your financial planning and outcomes.

Savings Accounts and Investments

For savings accounts, money market accounts, and certain investment vehicles, daily interest compounding is your ally. The earlier interest is calculated and added to your principal, the faster your money grows. A bank advertising a 2% APY on a savings account with daily compounding means you’re continuously earning interest on your initial deposit and the interest already earned. This “interest on interest” effect, magnified daily, is the core of wealth accumulation over the long term, making daily compounding accounts highly attractive for savers.

Loans and Mortgages

On the borrowing side, daily interest can be a double-edged sword. While some loans, like simple interest personal loans, accrue interest daily but only apply it monthly, others, like certain lines of credit or even some mortgages, can see interest truly compounding daily on the outstanding balance. For loans, understanding daily interest helps you grasp the true cost. Paying down your principal even slightly earlier can reduce the daily interest accrual, leading to significant savings over the life of the loan. This is particularly relevant for variable-rate loans where the principal balance can fluctuate, directly impacting the daily interest charged.

Credit Cards and Revolving Debt

Perhaps nowhere is the impact of daily interest more acutely felt than with credit cards. Credit card companies typically calculate interest on your average daily balance. This means that every day, your outstanding balance is multiplied by your daily periodic rate (the APR divided by 365 or 360). If you carry a balance, especially a high one, the daily interest charges can quickly accumulate, making it difficult to pay off the principal. Even a small purchase can start accruing interest immediately if you don’t pay your full statement balance each month. Understanding this mechanism highlights the importance of paying your credit card bill in full and on time to avoid the compounding trap.

Business Finance

For businesses, particularly those managing working capital and short-term financing, daily interest calculations are critical. Lines of credit, merchant cash advances, and short-term business loans often accrue interest daily. Accurate daily interest calculation helps businesses forecast cash flow, understand the true cost of borrowing, and make informed decisions about liquidity management. Optimizing daily cash balances to minimize interest paid on borrowings or maximize interest earned on idle funds can directly impact a company’s profitability.

Tools and Tips for Accurate Daily Interest Calculation

While the formula is straightforward, real-world financial products can introduce complexities. Fortunately, various tools and tips can help ensure your daily interest calculations are accurate.

Using Online Calculators and Spreadsheets

For most people, manually calculating daily compounded interest for an extended period is tedious and prone to error.

- Online Interest Calculators: Numerous free online calculators are available specifically for daily compound interest. You simply input the principal, annual rate, and number of days, and the calculator provides the total interest earned or paid.

- Spreadsheets (e.g., Excel, Google Sheets): Spreadsheets are incredibly powerful for daily interest calculations, especially for modeling compounding over time. You can set up columns for date, beginning balance, daily interest, and ending balance, using formulas to automatically calculate interest and update the balance for each subsequent day. Functions like

FV(Future Value) or building custom formulas based on the daily periodic rate can provide detailed insights into growth or accrual.

Understanding Bank Statements and Loan Amortization Schedules

Financial institutions provide statements that detail interest charges or earnings.

- Bank Statements: For savings, review your statements to see how interest is calculated and applied. Look for “interest earned” sections and compare them to your own calculations or expectations.

- Loan Amortization Schedules: For loans, an amortization schedule breaks down each payment into principal and interest. While these are often monthly, they provide a clear picture of how much of your payment goes towards interest, which is directly influenced by the daily accrual. Requesting a daily breakdown or understanding the lender’s exact daily calculation method is crucial for complex loans.

Key Factors Affecting Your Daily Interest

Several factors can influence the actual daily interest you pay or earn:

- Balance Fluctuations: Any changes to your principal balance (deposits, withdrawals, payments, purchases) immediately alter the base on which daily interest is calculated.

- Interest Rate Changes: Variable-rate accounts or loans can see their annual interest rate adjusted, directly impacting the daily calculation.

- Payment Timing (for loans/credit cards): Making payments earlier in your billing cycle can reduce your average daily balance, thereby lowering the total interest charged. Conversely, late payments can lead to higher average daily balances and additional fees.

- Days in the Month/Year: While often standardized to 365, some institutions might use 360 days for certain calculations, subtly affecting the daily rate. Always confirm the denominator used.

Leveraging Daily Interest Knowledge for Better Financial Health

The ability to calculate and understand daily interest is more than just an academic exercise; it’s a practical skill that underpins sound financial planning and decision-making.

Maximizing Your Savings and Investments

By understanding daily compounding, you can actively seek out savings accounts or investment vehicles that offer favorable daily interest calculation methods and higher AER/APYs. The difference between an account that compounds monthly and one that compounds daily, even with the same nominal annual rate, can be significant over years. Regularly contributing to these accounts, even small amounts, leverages the power of daily compounding to accelerate your wealth growth.

Minimizing Your Debt Burden

For debt, knowledge of daily interest empowers you to strategically tackle it. Prioritize paying off high-interest, daily-compounding debts like credit cards. Making extra payments or even just paying a few days before the due date can reduce your average daily balance and, consequently, the total interest you owe. This proactive approach can save you hundreds or even thousands of dollars over time, freeing up capital for other financial goals.

Informed Financial Decision-Making

Ultimately, understanding daily interest allows you to evaluate financial products more critically. When comparing loans, don’t just look at the APR; consider how frequently interest is compounded and how that translates to the effective annual cost. For savings, focus on the AER/APY rather than just the stated annual rate. This nuanced understanding enables you to choose products that align with your financial goals, whether that’s minimizing borrowing costs or maximizing investment returns. It transforms you from a passive consumer of financial services into an active, informed participant in your own financial journey.

In conclusion, daily interest is a powerful force in finance, capable of both building wealth and accumulating debt rapidly. By mastering its calculation and understanding its implications, you gain a significant advantage in managing your money effectively, ensuring that you’re always making the most informed and beneficial financial decisions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.