Building strong business credit is a critical step for any entrepreneur aiming for sustainable growth and financial independence from their personal credit profile. It’s not merely a luxury but a fundamental necessity for securing favorable lending terms, attracting investors, and ultimately, expanding your operational capacity. Understanding how to systematically establish and nurture this financial pillar can significantly impact your business’s trajectory, opening doors to capital that might otherwise remain inaccessible.

The Indispensable Value of Business Credit

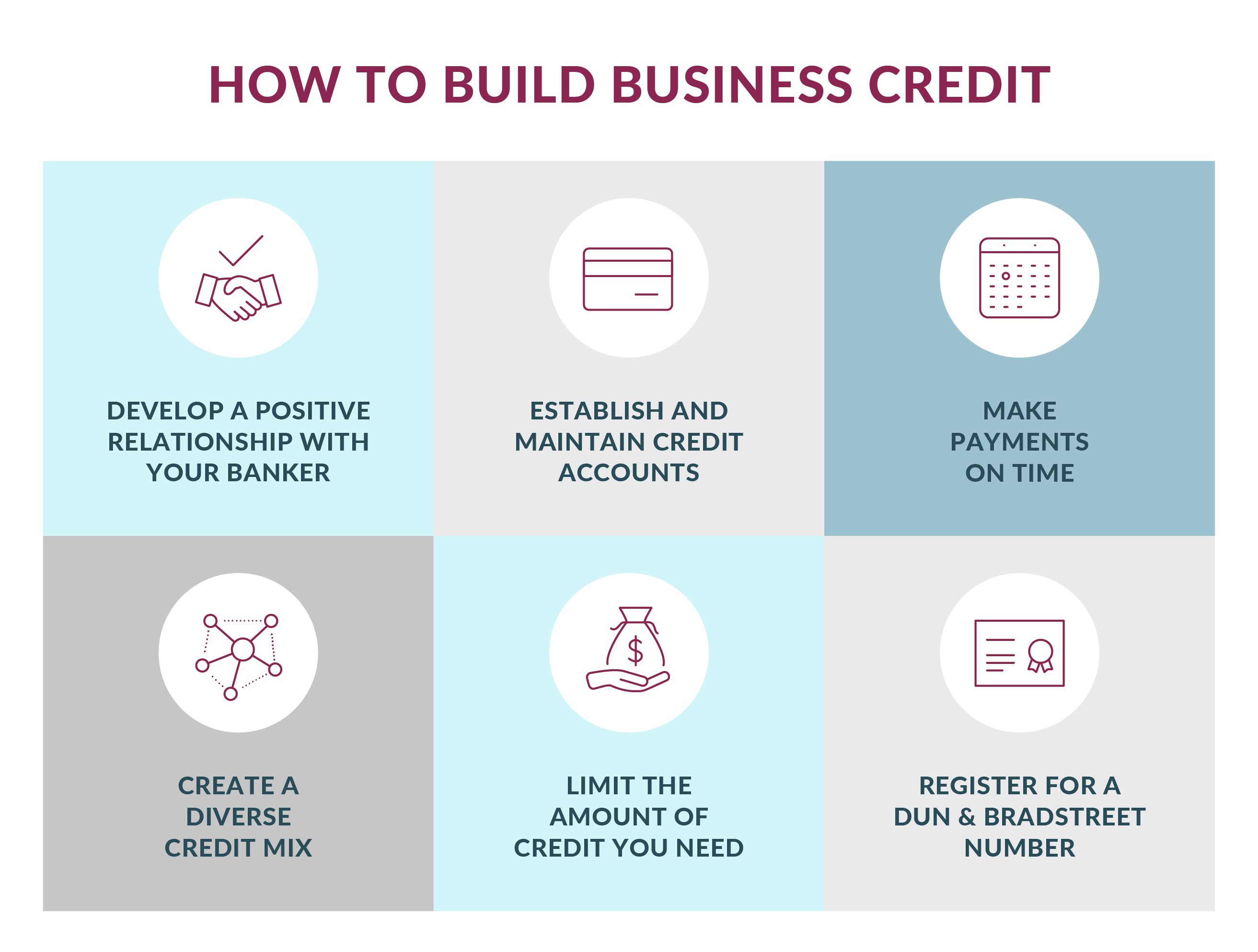

Many entrepreneurs make the mistake of conflating personal credit with business credit, often relying on personal guarantees for early-stage funding. While personal credit can certainly facilitate initial access to capital, it presents significant limitations and risks. A robust business credit profile stands as a testament to your company’s financial health and responsibility, entirely separate from your personal assets and liabilities.

Separating Personal from Business Finances

The primary benefit of establishing business credit is the clear demarcation it creates between your personal and business finances. Without this separation, your personal credit score becomes the de facto credit score for your business, meaning personal financial setbacks could directly impact your business’s ability to secure loans, and conversely, business debts could threaten your personal assets if you’ve provided a personal guarantee. Building business credit protects your personal assets, allowing you to secure funding based on your business’s own performance and history, not just your personal financial standing. This separation is also crucial for legal liability protection, especially if your business is structured as an LLC or corporation.

Unlocking Capital and Favorable Terms

A strong business credit score acts as a golden key to a wider array of financing options, often with more attractive interest rates and repayment terms. Lenders, suppliers, and even potential business partners assess your company’s creditworthiness to gauge risk. A high score signals reliability and lower risk, making lenders more willing to offer unsecured loans, lines of credit, or trade credit without requiring personal guarantees or extensive collateral. This access to diverse capital is vital for managing cash flow, investing in growth opportunities, purchasing inventory, or even navigating unexpected economic shifts without straining your personal finances. It allows your business to stand on its own financial feet, leveraging its established credit to fuel its own expansion.

Laying a Robust Foundation for Creditability

Before you can begin to build business credit, it’s essential to establish a solid legal and financial infrastructure that clearly identifies your business as a separate, credible entity. Skipping these foundational steps can hinder your ability to open accounts or secure loans in your business’s name.

Formalizing Your Business Structure

The first critical step is to legally register your business. Operating as a sole proprietorship or a general partnership often means your business is legally intertwined with your personal identity. To build separate business credit, you typically need to formalize your structure as a Limited Liability Company (LLC), S-Corporation, or C-Corporation. These structures not only offer liability protection but also provide the legal framework necessary for your business to exist as its own entity, capable of entering into contracts and securing credit. Register your business with your state’s Secretary of State or equivalent agency, obtaining all necessary licenses and permits for your industry and locality.

Obtaining Your Employer Identification Number (EIN)

An Employer Identification Number (EIN) is a unique nine-digit tax ID assigned by the IRS to businesses, analogous to a Social Security Number for an individual. Even if you’re a sole proprietor without employees, obtaining an EIN is highly recommended. It’s often required to open a business bank account, apply for business licenses, and file taxes. Critically, it allows you to separate your business’s financial activities from your personal Social Security Number, which is a cornerstone of building distinct business credit. You can apply for an EIN for free directly through the IRS website.

Establishing Dedicated Business Finances

Once you have your formal business structure and EIN, the next non-negotiable step is to open a dedicated business checking account and, eventually, a business savings account. Co-mingling personal and business funds is detrimental to both your accounting practices and your ability to build business credit. Lenders and credit bureaus need to see a clear transactional history belonging solely to your business. This account will be used for all business income, expenses, and payroll. Additionally, consider setting up a dedicated business phone number and physical mailing address (not a P.O. Box if possible, as some lenders prefer a street address) that are distinct from your personal contact information. This professional presence further solidifies your business’s independent identity.

Professionalizing Your Business Presence

Beyond bank accounts and EINs, ensuring your business has a professional and consistent presence across all touchpoints is crucial. This includes registering a business domain name, setting up a professional email address (e.g., info@yourbusiness.com), and creating a basic but professional website. Lenders and credit providers often perform due diligence, and a verifiable, professional online presence adds credibility and signals that your business is legitimate and established, even if it’s new.

Initiating Your Business Credit Profile

With the foundational elements in place, you can now proactively begin to establish a credit history that credit bureaus can track and score. This involves securing accounts that report payment activity to commercial credit agencies.

Leveraging Vendor and Supplier Credit

One of the most effective ways to start building business credit is by establishing trade lines with vendors and suppliers. These are typically “net-30” accounts, meaning you have 30 days to pay for goods or services after invoicing. Examples include office supply companies, shipping services, or industry-specific suppliers. When applying, ask if they report payment activity to business credit bureaus like Dun & Bradstreet, Experian Business, or Equifax Business. Consistent, on-time payments to these vendors will begin to populate your business credit reports, demonstrating your reliability as a payer. Aim for at least three to five such accounts reporting positively.

Securing Your First Business Credit Cards

Once you have a few reporting vendor accounts, you can start applying for entry-level business credit cards. Many financial institutions offer secured business credit cards, which require a cash deposit as collateral, making them easier to obtain for new businesses or those with limited credit history. Use these cards for everyday business expenses and ensure you pay the balances in full and on time every month. Over time, you can graduate to unsecured business credit cards. Be mindful of credit utilization, keeping balances low relative to your credit limits, ideally below 30%, to reflect responsible credit management.

The Role of Business Credit Bureaus

Unlike personal credit, which primarily uses FICO and VantageScore, business credit relies on scores and reports from specialized agencies.

- Dun & Bradstreet (D&B): Known for its PAYDEX score (0-100), which indicates how promptly your business pays its bills. You’ll need a D-U-N-S Number to be listed.

- Experian Business: Provides a business credit score (0-100) and risk assessments.

- Equifax Business: Offers a business credit risk score and a business failure score.

It’s crucial to understand how these bureaus operate and what information they collect. Regularly check your reports with each bureau to ensure accuracy and to monitor your progress. Some vendors only report to one bureau, so diversifying your credit sources is beneficial.

Strategic Utilization and Timely Payments

The cornerstone of any good credit score, personal or business, is timely payments. Every late payment can significantly harm your score and remain on your report for years. Automate payments where possible or set up strict internal reminders. Beyond timeliness, strategic utilization is key. For business credit cards, try to keep your credit utilization ratio (the amount of credit you’re using compared to your total available credit) as low as possible. A low utilization rate signals that your business isn’t over-reliant on credit and has ample financial breathing room.

Advanced Strategies for Elevating Your Credit Score

Once you’ve established a basic credit profile, the focus shifts to strategic management and continuous improvement to achieve a high business credit score, which will unlock greater financial opportunities.

Monitoring Your Business Credit Reports

Just as you monitor your personal credit, regular scrutiny of your business credit reports is paramount. Access your reports from Dun & Bradstreet, Experian Business, and Equifax Business. Each bureau may have different information and scoring, so reviewing all three provides a comprehensive view. Look for any inaccuracies, such as incorrect company information, mistaken late payments, or accounts that don’t belong to your business. Promptly dispute any errors to ensure your credit profile accurately reflects your payment behavior and financial health. Regular monitoring also helps you track your progress and understand which actions are impacting your score most effectively.

Managing Credit Utilization Effectively

Credit utilization remains a significant factor in business credit scoring. Lenders view a high utilization ratio as a sign of potential financial distress or over-reliance on credit, even if you pay your bills on time. Aim to keep your total credit utilization across all business credit lines below 30%, and ideally even lower, closer to 10-20%. This doesn’t mean you shouldn’t use your credit; rather, it means using it judiciously and paying down balances frequently. If you have multiple business credit cards, spreading your spending across them can sometimes help maintain lower utilization on individual cards, provided you manage all payments responsibly.

Diversifying Your Credit Portfolio

A healthy credit profile typically includes a mix of credit types, such as trade lines, credit cards, and installment loans. As your business grows and your credit score improves, consider applying for small business loans or lines of credit from traditional banks or alternative lenders. Successfully managing and repaying these larger financial commitments will further diversify your credit portfolio and demonstrate your ability to handle different types of debt responsibly. However, only take on debt that your business can comfortably service. Each new credit account adds to your overall credit history, assuming it’s managed well, and signals stability and growth potential to future lenders.

Cultivating Long-Term Lender Relationships

Building strong relationships with your lenders can be incredibly valuable. Consistently paying on time, communicating proactively about any potential challenges, and engaging with your banking partners can lead to more favorable terms, easier access to capital, and tailored financial advice as your business evolves. A long-standing, positive relationship with a bank can be a significant asset, especially when seeking larger loans or more complex financial products. This relationship, built on trust and consistent financial responsibility, often provides a competitive edge over businesses that are constantly seeking new lenders.

Building business credit is a marathon, not a sprint. It requires discipline, strategic financial management, and consistent attention to detail. By systematically implementing these steps, you will establish a solid financial foundation that empowers your business to secure the capital needed for growth, stability, and long-term success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.