For many entrepreneurs, freelancers, gig economy workers, and individuals with significant investment income, the quarterly obligation of paying federal estimated taxes is a critical component of their financial discipline. Unlike traditional employees who have taxes withheld from each paycheck, these individuals are responsible for proactively remitting taxes throughout the year to cover their income, self-employment, and certain other taxes. Failing to do so can result in unwelcome underpayment penalties come tax season.

Fortunately, the digital age has revolutionized how taxpayers meet this obligation. Paying federal estimated tax online is not only a matter of convenience but also a strategic move towards more efficient financial management, enhanced security, and reliable record-keeping. This comprehensive guide will walk you through the necessities of estimated taxes, the various online payment methods available, and best practices to ensure a smooth, penalty-free tax year.

Understanding Federal Estimated Taxes

Before diving into the mechanics of online payments, it’s crucial to grasp the fundamental principles of federal estimated taxes: who needs to pay them, why they’re essential, and how they are calculated. This foundational knowledge empowers you to approach your tax obligations with confidence and clarity.

Who Needs to Pay Estimated Taxes?

The requirement to pay estimated taxes primarily falls on individuals whose income is not subject to sufficient tax withholding. This typically includes:

- Self-Employed Individuals: Sole proprietors, partners in a partnership, and S-corporation shareholders who anticipate owing at least $1,000 in tax.

- Freelancers and Independent Contractors: Those who receive income through 1099 forms rather than W-2s.

- Individuals with Significant Investment Income: Income from stocks, bonds, mutual funds, or real estate that generates substantial capital gains, interest, or dividends.

- Retirees with Unwithheld Income: Those receiving pensions, annuities, or Social Security benefits without sufficient tax withheld.

- Recipients of Alimony: For divorce agreements executed before January 1, 2019, alimony payments are taxable to the recipient.

- Anyone with Insufficient Withholding: Even if you’re traditionally employed, if you have significant side income or have not adjusted your W-4 correctly, you might need to pay estimated taxes to cover any shortfall.

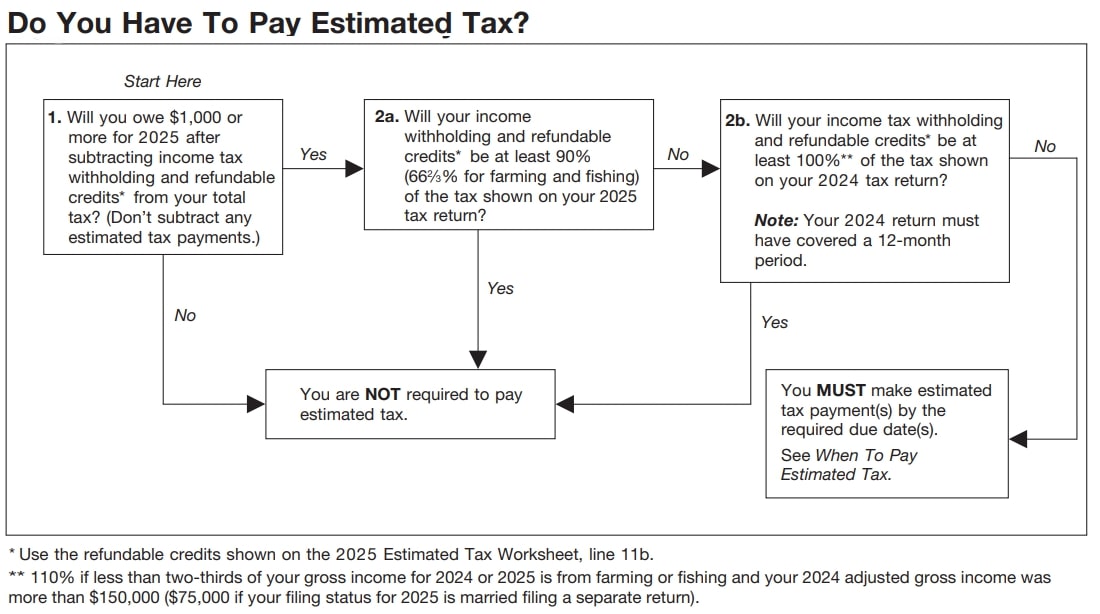

Generally, you must pay estimated tax if you expect to owe at least $1,000 in tax for the current year, and your withholding and refundable credits are expected to be less than the smaller of:

- 90% of the tax to be shown on your current year’s return.

- 100% of the tax shown on your previous year’s return (110% if your adjusted gross income was over $150,000).

Why Estimated Taxes Are Necessary

The U.S. tax system operates on a “pay-as-you-go” principle. This means that taxes should be paid throughout the year as income is earned, rather than in one lump sum at year-end. For wage earners, this is handled through payroll withholding. For those whose income streams don’t have withholding, estimated taxes fulfill this requirement.

The primary reason for paying estimated taxes is to avoid underpayment penalties. The IRS can impose penalties if you don’t pay enough tax throughout the year, either through withholding or estimated payments, by certain deadlines. These penalties are designed to compensate the government for the time value of money that was not collected when it was due. Proactive quarterly payments ensure you meet your obligations and prevent financial surprises during tax season.

Calculating Your Estimated Tax

Calculating your estimated tax requires a forward-looking assessment of your income, deductions, credits, and potential tax liability for the entire year. The IRS Form 1040-ES, “Estimated Tax for Individuals,” is your primary tool for this. Key steps include:

- Estimate Your Gross Income: Project all sources of income for the year, including self-employment earnings, investment income, rental income, and any other taxable income not subject to withholding.

- Estimate Your Deductions and Credits: Account for anticipated itemized or standard deductions, and any tax credits you expect to qualify for (e.g., child tax credit, education credits, self-employment tax deductions).

- Compute Your Expected Tax: Use your estimated income, deductions, and credits to calculate your total tax liability for the year. The IRS tax tables or tax software can help with this.

- Subtract Withholding and Credits: Deduct any federal income tax you expect to have withheld from wages (if applicable) and any refundable credits.

- Divide by Four: The remaining amount is your estimated tax liability for the year. Divide this total by four to determine your quarterly payment amount.

It’s important to remember that this is an estimate. If your income or deductions change significantly during the year, you may need to recalculate and adjust your remaining estimated tax payments.

Navigating Online Payment Options

The IRS provides several secure and convenient online methods for paying federal estimated taxes. Each option has its own features, benefits, and requirements, allowing you to choose the one that best fits your financial preferences and technical comfort.

IRS Direct Pay

IRS Direct Pay is a free, secure web service that allows individuals to pay their federal taxes directly from their checking or savings account. It’s often the simplest method for a one-time payment without prior registration.

- Pros: It’s free, highly secure, and does not require pre-registration. You receive immediate confirmation once the payment is submitted.

- Cons: Limited to bank account payments (checking or savings). You can schedule payments up to 365 days in advance, but you can only make two payments within a 24-hour period.

- Steps:

- Visit the official IRS.gov website and navigate to the Direct Pay section.

- Select “Make a Payment.”

- Choose your reason for payment (e.g., “Estimated Tax”), apply payment to (e.g., “1040ES”), and select the tax period.

- Verify your identity using information from a previous tax return (e.g., filing status, SSN, date of birth, address).

- Enter your bank routing and account numbers.

- Review and submit your payment. You’ll receive a confirmation number via email if you provide one.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is a robust, free service offered by the U.S. Treasury Department that allows businesses and individuals to make all federal tax payments electronically. It’s ideal for those who make frequent or scheduled tax payments.

- Pros: Extremely secure, allows for scheduling payments up to 365 days in advance, supports all federal tax payments (not just estimated), and provides a comprehensive payment history. It’s also available 24/7.

- Cons: Requires an enrollment process that can take 5-7 business days to complete as a PIN is mailed to your address. This makes it less suitable for last-minute payments if you’re not already enrolled.

- Steps:

- Enroll online at EFTPS.gov. You’ll provide your taxpayer identification number (SSN or EIN), bank account information, and an email address.

- Wait to receive your mailed Personal Identification Number (PIN) – typically within a week.

- Once enrolled and with your PIN, log in using your Tax ID, PIN, and password.

- Select “Make a Payment,” choose the tax type (e.g., “Form 1040 Estimated Tax”), and enter the payment amount and effective date.

- Confirm your payment. You’ll receive an immediate confirmation number.

Payment Processors (Third-Party Services)

For those who prefer to pay their estimated taxes using a credit card, debit card, or digital wallet, the IRS partners with several third-party payment processors. These services offer flexibility but come with associated convenience fees.

- Pros: Offers alternative payment methods like credit cards (earning rewards points), debit cards, and digital wallets (e.g., PayPal, Venmo, Click to Pay). Provides immediate payment confirmation.

- Cons: These services charge a separate convenience fee, which varies by processor and payment method (typically 1.87% – 2.0% for credit cards, flat fee for debit cards).

- Examples: PayUSAtax, Official Payments, ACI Payments Inc. (check their websites for the most current fees).

- Steps:

- Visit the IRS website to find approved payment processors.

- Choose a processor and click through to their website.

- Select “Federal Estimated Tax” (Form 1040-ES) as the payment type.

- Enter your payment details, including your SSN, name, address, payment amount, and chosen payment method.

- Review the convenience fee and authorize the payment.

- Receive a confirmation number from the processor.

Tax Software Providers

Many popular tax preparation software programs (e.g., TurboTax, H&R Block, TaxAct) offer an integrated option to pay your estimated taxes directly through their platform after you’ve calculated your liability.

- Pros: Seamless integration with your tax preparation process, reducing manual entry and potential errors. Can often automate the calculation and scheduling of payments.

- Cons: Typically part of a paid software package. May use one of the third-party payment processors, incurring fees if paying by credit/debit card.

- Steps:

- Use your tax software to calculate your annual income and estimated tax liability.

- Within the software’s estimated tax section, select the option to make a payment.

- Follow the prompts to enter your bank account or credit card information. The software will usually connect to an IRS-approved payment method.

- Confirm the payment.

Best Practices for Online Estimated Tax Payments

While paying online simplifies the process, adopting certain best practices can further enhance efficiency, accuracy, and security in your financial operations.

Timing Your Payments

Federal estimated tax payments are due quarterly. The standard deadlines are:

- April 15: For income earned January 1 to March 31.

- June 15: For income earned April 1 to May 31.

- September 15: For income earned June 1 to August 31.

- January 15 of next year: For income earned September 1 to December 31.

If any of these dates fall on a weekend or holiday, the deadline shifts to the next business day. It’s wise to make payments a few days before the deadline to account for any unforeseen technical issues or bank processing times. Scheduling payments in advance, especially with EFTPS, can help you avoid missing deadlines.

Keeping Meticulous Records

Digital payments generate digital records, which are invaluable for financial management. Always save or print:

- Confirmation Numbers: Crucial proof of payment from the IRS Direct Pay, EFTPS, or third-party processor.

- Transaction Dates and Amounts: Ensure these match your records and bank statements.

- Screenshots: If you’re particularly cautious, take screenshots of the final confirmation pages.

- Bank Statements: Regularly reconcile your bank statements with your tax payment records to confirm transactions cleared correctly.

These records are essential for tax preparation, audit defense, and general financial oversight.

Security Considerations

When paying taxes online, security is paramount.

- Only Use Official IRS Channels: Always access IRS Direct Pay or EFTPS through the official IRS.gov or EFTPS.gov websites. Be wary of emails or links claiming to be from the IRS.

- Strong Passwords: Use unique, strong passwords for any accounts (like EFTPS) and consider multi-factor authentication where available.

- Public Wi-Fi: Avoid making sensitive financial transactions, including tax payments, over unsecured public Wi-Fi networks.

- Phishing Awareness: The IRS will never initiate contact with you via email, text message, or social media to request personal or financial information. Report suspicious communications.

What to Do if You Make a Mistake

If you discover an error after making an estimated tax payment online:

- Incorrect Amount: For IRS Direct Pay, you can modify or cancel a payment up to two days before the scheduled payment date. EFTPS allows cancellation or modification up to two calendar days before the payment date. If the payment has already processed, you cannot directly reverse it through the IRS. You’ll need to adjust future estimated payments or claim an overpayment on your annual tax return.

- Incorrect Tax Year/Type: This is more challenging. Contact the IRS directly (via phone or written correspondence) to explain the error and request a reapplication of the funds to the correct tax period or type. Keep all documentation of your original payment and your communication with the IRS.

- Payment Failure: If a payment is rejected (e.g., due to incorrect bank info or insufficient funds), you will likely be notified. You’ll need to submit a new payment and potentially incur penalties if the original due date was missed.

The Benefits of Going Digital with Estimated Taxes

Embracing online payment methods for federal estimated taxes offers a multitude of advantages that extend beyond mere convenience, impacting your financial planning and overall peace of mind.

Convenience and Accessibility

The ability to pay your taxes 24/7, from anywhere with an internet connection, is a significant benefit. This eliminates the need for paper checks, envelopes, stamps, and trips to the post office. Whether you’re at home, in the office, or traveling, managing your tax obligations is always within reach, fitting seamlessly into your busy schedule.

Accuracy and Reduced Errors

Online payment systems often incorporate validation checks, reducing the likelihood of common errors such as incorrect Social Security numbers, tax year designations, or payment amounts. The digital transfer of funds directly to the IRS minimizes the risk of mail loss or processing delays, ensuring your payment is accurately attributed and received on time.

Improved Financial Planning

Online payment platforms, particularly EFTPS, allow you to schedule payments in advance. This capability is a powerful tool for financial planning, enabling you to budget more effectively and manage your cash flow throughout the year. By setting up recurring payments, you can automate your tax obligations, reducing mental load and the stress of remembering quarterly deadlines. It helps you integrate tax responsibilities into your broader financial strategy rather than treating them as isolated, stressful events.

Environmental Impact

Opting for online payments contributes to a paperless environment. Reducing paper consumption for checks, payment vouchers, and postal receipts aligns with environmentally conscious practices, offering a small but meaningful contribution to sustainability.

Conclusion

Paying federal estimated tax online is no longer just an option; for many, it’s the preferred and most efficient method for fulfilling their tax obligations. By understanding who needs to pay, how to calculate your liability, and by leveraging the secure online tools provided by the IRS and its partners, you can navigate the complexities of estimated taxes with ease and confidence. Adhering to best practices for timing, record-keeping, and security will ensure a smooth, penalty-free experience, allowing you to focus on what you do best while maintaining sound financial health. Embrace the digital convenience and empower your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.