In an increasingly interconnected world, the need to transfer funds to others, whether across the street or across continents, is a common financial necessity. From splitting a dinner bill with a friend to sending emergency funds to a family member abroad, the options for moving money have proliferated beyond traditional banking, offering a spectrum of speed, cost, and convenience. Understanding the various methods available is crucial for making informed financial decisions, ensuring your money reaches its destination securely and efficiently, without unnecessary fees or complications. This guide will navigate the landscape of money transfer options, from the ubiquitous digital platforms to time-honored traditional banking services, emphasizing the financial implications and security considerations of each.

Understanding Your Options: A Spectrum of Payment Methods

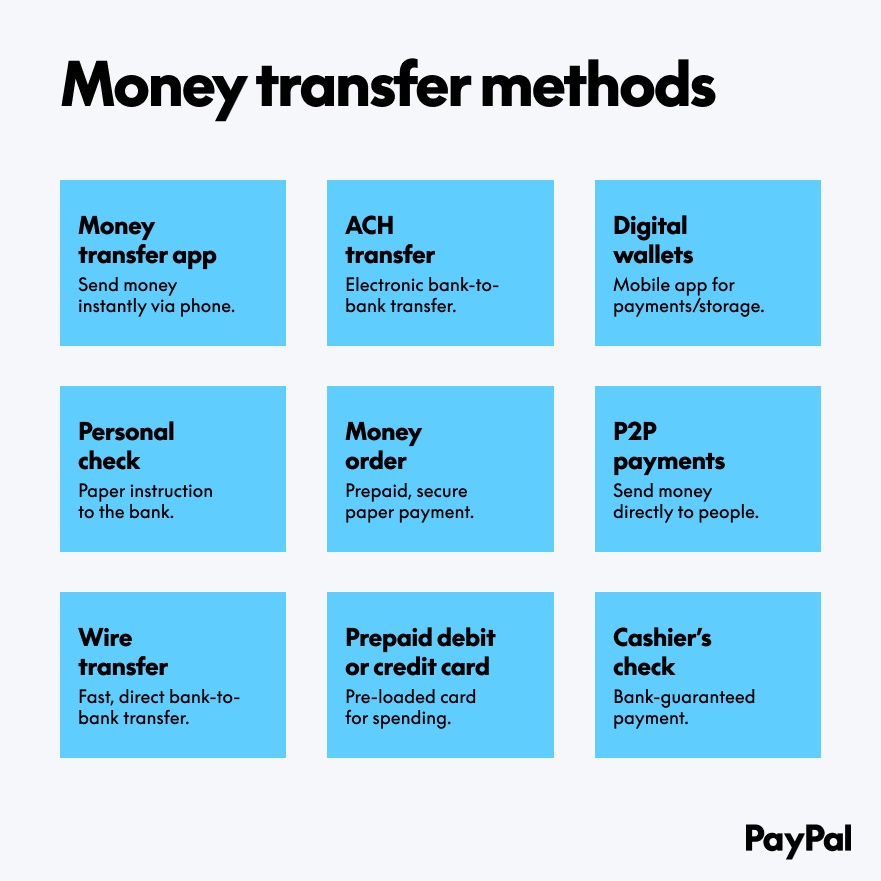

The ability to send money to someone has evolved dramatically over the past few decades. What once primarily involved physical cash, checks, or slow bank transfers now encompasses a vast ecosystem of digital applications and specialized services designed for speed and convenience. The “best” method isn’t universal; it hinges on several key factors: the urgency of the transfer, the amount being sent, the recipient’s location and access to financial tools, and your tolerance for fees and potential security risks.

Modern financial tools have democratized money movement, making it possible for individuals to perform transactions that once required a bank teller. However, this convenience also introduces a layer of complexity regarding choices. You might need to send a small sum instantly to a friend, or a significant amount securely to a business partner, or regularly remit funds to family overseas. Each scenario demands a different approach, balancing the desire for immediacy with the imperative for security and cost-effectiveness. By exploring the various avenues, you can tailor your approach to the specific requirements of each transaction, optimizing for both peace of mind and financial prudence.

Digital Payment Platforms: Speed, Convenience, and Considerations

Digital payment platforms have revolutionized how we interact with money, offering unparalleled speed and convenience for a wide array of transactions. These platforms leverage technology to facilitate near-instantaneous transfers, often with minimal fees for domestic transactions, making them a cornerstone of modern personal finance.

Peer-to-Peer (P2P) Apps

P2P payment apps like Zelle, Venmo, PayPal, and Cash App have become household names, primarily for their ease of use in splitting bills, paying friends, or making small purchases. They link directly to your bank account or debit card, allowing for quick transfers using just a recipient’s phone number, email address, or username.

- Zelle: Often integrated directly into banking apps, Zelle allows for fast transfers between bank accounts of participating financial institutions, typically within minutes. It’s ideal for sending money to trusted individuals, as transactions are generally irreversible and often free.

- Venmo: Popular for its social features, Venmo is widely used for casual money sharing among friends. While standard transfers to a bank account are free (but can take 1-3 business days), instant transfers incur a small fee. Funding with a credit card also typically carries a percentage-based fee.

- PayPal: A veteran in online payments, PayPal offers broad functionality, including P2P payments, online shopping, and international transfers through its Xoom service. It provides robust buyer and seller protection for goods and services but may charge fees for certain types of transactions or international transfers.

- Cash App: Similar to Venmo, Cash App enables quick P2P transfers, direct deposits, and even investing in stocks and Bitcoin. It charges fees for instant transfers from the app to a bank account and for credit card funding.

While incredibly convenient, P2P apps come with limitations. Transaction limits vary by service and verification level, and the irrevocability of payments means careful verification of recipient details is paramount to avoid sending money to the wrong person. Fraud protection often differs from traditional banking, placing a greater onus on the user.

Online Banking Transfers (ACH)

Most banks offer online platforms that allow you to transfer money directly from your account to another person’s account, often through the Automated Clearing House (ACH) network. These transfers are generally secure and reliable, suitable for both recurring payments and one-off transactions.

- Benefits: ACH transfers are typically free for domestic transactions, especially within the same bank or between linked accounts. They are ideal for paying bills, rent, or transferring larger sums between your own accounts or to trusted individuals.

- Considerations: ACH transfers are not instant; they usually take 1-3 business days to clear. You’ll need the recipient’s bank account number and routing number, which requires a higher level of trust and data sharing than P2P apps.

International Remittance Services

When sending money across borders, specialized international remittance services offer more competitive exchange rates and lower fees compared to traditional banks’ wire transfers. Companies like Wise (formerly TransferWise), Remitly, and Xoom (a PayPal service) specialize in cross-border payments.

- Benefits: These services often provide transparent fee structures, better exchange rates, and various delivery options, including direct bank deposits, cash pickup, or mobile wallet transfers. They are particularly advantageous for regular remittances or larger international transfers.

- Considerations: Exchange rates fluctuate, and fees can vary based on the amount, destination country, and transfer method. Verification processes can be rigorous due to international regulations, and delivery times may still vary.

Traditional Methods: When Analog Still Makes Sense

Despite the rise of digital options, traditional money transfer methods continue to hold relevance in specific scenarios, offering reliability, a physical record, or a broad reach to individuals who may not have access to digital financial tools.

Checks and Money Orders

These methods offer tangible proof of payment and can be useful for non-urgent transactions or when a digital footprint is not desired.

- Personal Checks: Still a common way to pay for goods or services or send money to individuals, checks provide a physical record and are often free from your bank’s perspective. However, they are slow (requiring mailing and several days to clear), can be lost or stolen, and carry the risk of bouncing if funds are insufficient. They are best for non-urgent payments to trusted recipients.

- Money Orders: A prepaid guarantee of funds, money orders are similar to cashier’s checks but for smaller amounts, typically purchasable at post offices, convenience stores, or grocery stores for a small fee. They are a good option for sending money to someone without a bank account or when you need guaranteed funds without using a personal check. They offer security in that they are prepaid, but can still be lost or stolen, requiring a receipt for potential replacement.

Bank Wire Transfers

A bank wire transfer is an electronic transfer of funds directly from one bank account to another, through a network managed by central banks or payment systems.

- Benefits: Wires are one of the fastest ways to send money, often arriving on the same business day for domestic transfers, and generally within a few days for international transfers. They are highly secure when handled through legitimate banking channels and are suitable for large sums of money.

- Considerations: Wire transfers are typically the most expensive option, with fees ranging from $25-$50 for domestic transfers and more for international ones. More critically, they are almost always irreversible once sent. This irreversibility makes them a prime target for fraudsters. Extreme caution is advised; always verify the recipient’s bank details meticulously, especially for international transfers, and never send a wire to someone you don’t know or trust for unsolicited offers, prizes, or emergency requests you haven’t independently verified.

Security and Fees: Protecting Your Funds and Your Wallet

Regardless of the method chosen, understanding the associated costs and prioritizing security are paramount to responsible money management. Sending money always carries some level of financial risk, and being aware of potential pitfalls can save you from significant losses.

Understanding Transaction Fees

Fees can erode the value of your transfer. They manifest in several forms:

- Flat Fees: A fixed amount charged per transaction (common for wire transfers, money orders, or instant P2P app transfers).

- Percentage Fees: A percentage of the transfer amount (often seen when funding P2P apps with a credit card or for certain international transfers).

- Exchange Rate Markups: For international transfers, some services or banks embed a markup into the exchange rate, meaning you get a less favorable rate than the mid-market rate, effectively increasing the cost. Always compare the total cost, including fees and the effective exchange rate, when sending money internationally.

Always scrutinize the fee structure before initiating a transfer. Many services offer free domestic transfers if certain conditions are met (e.g., using a bank account via ACH for P2P apps, or standard transfer speeds). Opting for speed or convenience often comes with an extra charge.

Prioritizing Security Measures

Protecting your financial information and funds is critical.

- Enable Two-Factor Authentication (2FA): For all digital payment apps and online banking, 2FA adds an essential layer of security by requiring a second verification method (like a code from your phone) in addition to your password.

- Strong, Unique Passwords: Use complex, unique passwords for each financial account. A password manager can help manage these.

- Verify Recipient Details: This is perhaps the most critical step. Double-check email addresses, phone numbers, and bank account details before confirming any transfer, especially for irreversible methods like Zelle or wire transfers. A single digit error can send your money to the wrong person, often with no recourse.

- Use Secure Networks: Avoid making financial transactions over public Wi-Fi networks, which can be vulnerable to eavesdropping. Use a secure, private network or a VPN.

- Monitor Account Activity: Regularly review your bank statements and transaction history for any unauthorized activity.

- Understand Fraud Protection: Be aware that P2P apps typically offer less fraud protection for unauthorized transactions compared to credit cards or even traditional bank transfers. If you send money to a scammer via a P2P app, it’s often difficult to recover.

Fraud Prevention Tips

The landscape of financial scams is constantly evolving. Staying vigilant is your best defense.

- Be Skeptical of Unsolicited Requests: Never send money to someone you don’t know personally for a “prize,” a “loan,” an “inheritance,” or an “emergency” you haven’t independently verified. Scammers frequently pressure victims to send money quickly via irreversible methods like wire transfers or gift cards.

- Beware of Impersonation Scams: Government agencies (IRS, police), banks, or utility companies will never demand immediate payment via unusual methods or threaten arrest if you don’t comply. Verify any suspicious contact directly with the organization using official contact information, not the details provided by the caller/emailer.

- Don’t Fall for Online Purchase Scams: For online purchases from unfamiliar sellers, use payment methods that offer buyer protection (e.g., credit cards, PayPal for goods and services). Avoid using P2P apps for purchasing from strangers, as these transactions typically lack protection.

- Protect Personal Information: Never share your passwords, PINs, or sensitive banking information with anyone.

Choosing the Right Method for Your Needs

Selecting the optimal way to send money requires a thoughtful assessment of your specific situation. There is no one-size-fits-all solution; instead, the best method is the one that aligns most effectively with your priorities for speed, cost, security, and the recipient’s ability to receive funds.

- For Instant, Small Transfers to Friends/Family: P2P apps like Zelle, Venmo, or Cash App are usually the best choice, especially if the recipient uses the same app or if it’s bank-integrated like Zelle. Ensure you have the correct recipient details.

- For Domestic Bank-to-Bank Transfers (non-urgent): Online banking transfers via ACH are reliable, secure, and typically free. They are ideal for paying rent, utilities, or transferring funds between your own accounts.

- For International Transfers: Specialized remittance services such as Wise, Remitly, or Xoom generally offer better exchange rates and lower fees than traditional bank wires. Compare options for the best value and choose based on payout methods convenient for the recipient.

- For Large, Urgent Transfers (High Cost/Risk): Bank wire transfers are the fastest way to move significant sums, domestically or internationally. However, due to high fees and irreversibility, they should be reserved for highly trusted transactions where speed is critical and security can be absolutely assured through meticulous verification.

- For Recipients Without Bank Accounts or When Physical Payment is Needed: Money orders offer a guaranteed form of payment for smaller sums, while checks are suitable for non-urgent payments to trusted parties with bank accounts.

Always prioritize verifying recipient information, understanding the fees, and assessing the level of fraud protection offered by each method. By carefully weighing these factors, you can navigate the diverse landscape of money transfer options confidently, ensuring your funds reach their intended destination safely and efficiently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.