Discovering you might owe money to the IRS can evoke a range of emotions, from anxiety to outright panic. However, facing this uncertainty head-on is the first crucial step toward financial clarity and peace of mind. Proactively understanding your tax obligations not only helps you avoid mounting penalties and interest but also empowers you to strategize effectively for payment and future tax management. This guide will walk you through the definitive methods available to ascertain your current tax liability with the IRS, offering practical advice and leveraging official resources to help you gain a firm grasp on your financial standing.

Navigating the IRS: Your Primary Digital Resources

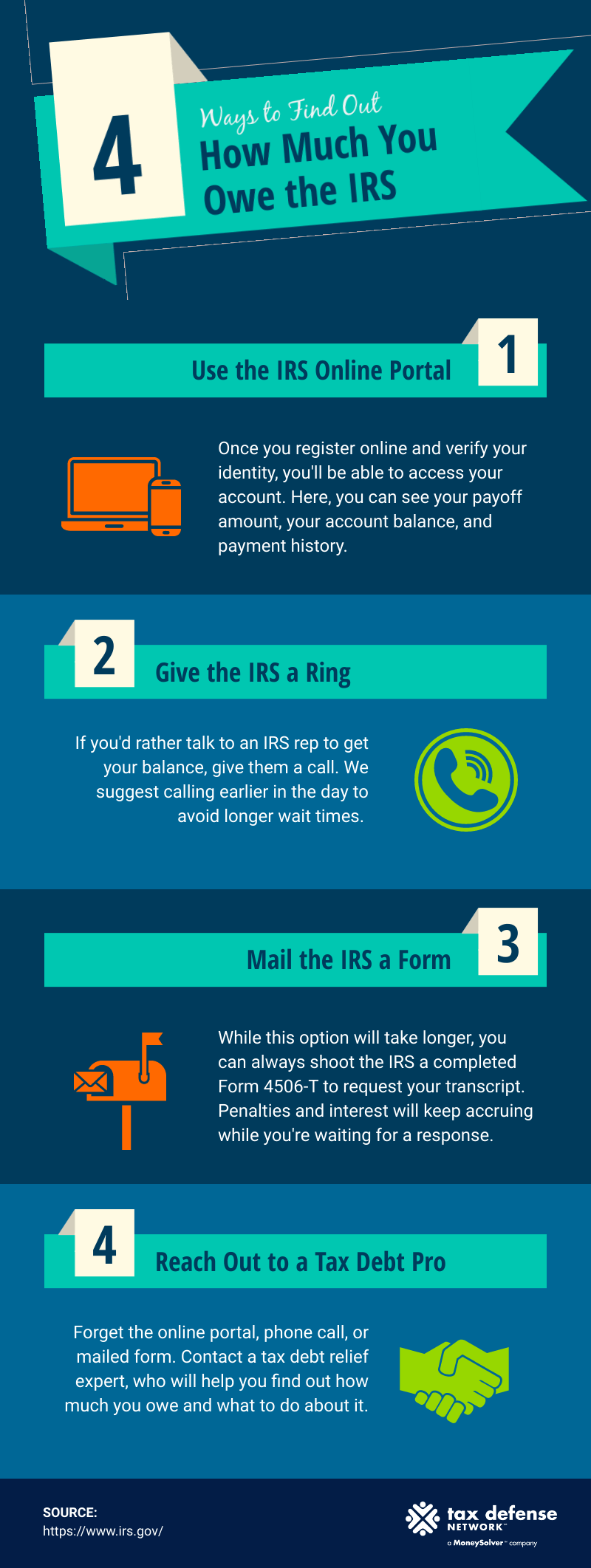

In an increasingly digital world, the IRS has significantly enhanced its online platforms to provide taxpayers with convenient and secure access to their tax information. These digital tools are often the fastest and most efficient ways to determine what you owe.

IRS Online Account: Your Personal Tax Dashboard

The IRS Online Account is arguably the most powerful tool at your disposal for managing your tax affairs. It functions as a personalized digital dashboard, offering a comprehensive overview of your federal tax obligations and history.

To access your IRS Online Account, you’ll need to go through a secure identity verification process, typically facilitated by ID.me. This multi-factor authentication ensures that your sensitive financial information remains protected. Once verified and logged in, you can view a wealth of information, including:

- Balance Due: Instantly see your current outstanding balance, including any penalties and interest that have accrued.

- Payment History: Review past payments you’ve made, whether through direct debit, estimated tax payments, or prior year refunds applied to future tax.

- Tax Transcripts: Request and view various tax transcripts, which provide detailed line-by-line information from your filed returns, your tax account status, and wage and income data reported by employers and financial institutions.

- Tax Notices: Access digital copies of certain IRS notices and communications.

- Estimated Tax Payments: See a summary of any estimated tax payments you’ve made for the current tax year.

- Payment Plans: View details of existing payment plans (like installment agreements) and make payments.

The benefits of utilizing your IRS Online Account are manifold: 24/7 access from anywhere, immediate access to up-to-date information, and a centralized hub for all your federal tax interactions. It’s an essential tool for proactive financial management.

Requesting Tax Transcripts: A Detailed Look at Your History

Beyond the summary information available in your online account, tax transcripts offer a granular view of your financial interactions with the IRS. These documents are often required for loan applications, student aid, and in-depth financial planning, and they are invaluable for understanding how your tax liability was calculated or why you might owe a balance.

There are several types of transcripts, each serving a specific purpose:

- Tax Return Transcript: Shows most line items from your original tax return (Form 1040, 1040-SR, 1040-NR) as you filed it, without any changes made by the IRS. It does not show changes made after you filed the original return.

- Tax Account Transcript: Provides basic data such as marital status, type of return filed, adjusted gross income, and payment information. It also shows changes made by you or the IRS after the original return was filed. This transcript is particularly useful for understanding the current status of your tax account and any adjustments that have led to a balance due.

- Record of Account Transcript: Combines the information from the Tax Return Transcript and the Tax Account Transcript into one comprehensive document. This is often the most complete picture of your tax filing and account activity.

- Wage and Income Transcript: Displays information reported to the IRS by employers and other third parties, such as Forms W-2, 1099, 1098, and 5498. This is crucial for verifying all sources of income and potential withholding.

- Verification of Non-filing Letter: Confirms that the IRS has no record of a filed Form 1040, 1040-SR, or 1040-NR for the year requested.

You can request these transcripts online through the “Get Transcript Online” service (which requires identity verification), by mail using Form 4506-T or Form 4506T-EZ, or by phone. While online requests are typically instant, mail requests can take 5 to 10 calendar days. Using transcripts can help you reconcile your records with what the IRS has on file, uncover discrepancies, and understand the basis of any outstanding debt.

Direct Communication Channels with the IRS

While digital tools offer convenience, certain situations or preferences may necessitate direct communication with the IRS. These traditional channels remain vital for resolving complex issues, seeking clarification, or for those who prefer human interaction.

Contacting the IRS by Phone: When You Need to Speak to Someone

For specific questions, complex account issues, or when online resources don’t provide the answers you need, speaking directly with an IRS representative can be invaluable. The IRS offers various phone lines tailored to different inquiries, though wait times can often be substantial, especially during peak tax season.

When preparing to call, have the following information readily available to expedite the process:

- Your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Your date of birth.

- Your address as shown on your last filed tax return.

- Your prior tax return(s).

- Any IRS notices you’ve received.

Be prepared to navigate automated systems and potentially long hold times. Calling early in the morning, late in the afternoon, or on weekdays during the middle of the week tends to yield shorter wait times. While agents can provide account information and explain notices, they generally cannot provide tax advice or interpret tax law for your specific situation.

Mail Correspondence and Notices: Understanding Official Communications

The IRS frequently communicates with taxpayers via mail, sending a variety of notices and letters. These documents are critical and should never be ignored, as they often contain important information about your tax account, proposed changes, or demands for payment.

Common types of IRS notices include:

- CP14 (Balance Due): Notifies you of an unpaid balance due for a specific tax year.

- CP2000 (Underreported Income): Informs you that income reported by third parties (like employers or financial institutions) does not match what you reported on your tax return, potentially leading to an increase in your tax liability.

- Notices about penalties and interest: These letters explain why you’ve been assessed penalties (e.g., for failure to file, failure to pay, accuracy-related) and how interest is calculated on overdue balances.

It’s crucial to read these notices carefully, understand the proposed action, and adhere to any stated deadlines for response. If you disagree with the notice or need more time, prompt communication with the IRS is essential. Keep copies of all correspondence you send to and receive from the IRS for your records. Ignoring official mail can lead to further penalties, interest, and even enforced collection actions.

In-Person Assistance: When a Face-to-Face Meeting is Necessary

For taxpayers who prefer or require in-person assistance, Taxpayer Assistance Centers (TACs) offer direct support. These centers are staffed by IRS employees who can help with a range of services, including:

- Answering questions about an IRS notice.

- Making payments.

- Providing tax forms.

- Assisting with basic tax law questions.

- Helping with account inquiries (like finding out what you owe).

TACs primarily operate by appointment only. You can find your nearest TAC and schedule an appointment through the IRS website. In-person visits can be particularly beneficial for resolving complex issues, verifying identity, or when digital and phone channels have proven insufficient. It’s advisable to bring all relevant documentation, including photo identification, your SSN/ITIN, and any pertinent tax notices or records.

Understanding Your Tax Debt and Payment Options

Once you’ve determined what you owe, the next step is to understand the components of your tax debt and explore the various payment options available through the IRS.

Interpreting Your Balance Due: Principal, Penalties, and Interest

Your total balance due to the IRS often comprises more than just the original tax liability. It can include:

- Principal amount: The core amount of tax you originally owed.

- Penalties: Assessed for various reasons, such as failure to file on time, failure to pay on time, or accuracy-related issues (e.g., substantial understatement of tax). Penalties can significantly increase your debt.

- Interest: The IRS charges interest on underpayments, unpaid balances, and certain penalties. Interest compounds daily, meaning it is charged on the unpaid balance plus any accumulated interest and penalties.

Understanding these components is vital because some penalties can be abated (removed) under certain circumstances, such as reasonable cause, while interest charges are generally mandatory on underpayments. Knowing the breakdown allows for more informed discussions with the IRS or a tax professional.

IRS Payment Solutions: Flexible Options for Repayment

The IRS offers several options for taxpayers who cannot pay their tax debt in full immediately. It’s always best to pay as much as you can as soon as you can to minimize penalties and interest.

- Payment in Full: The simplest and most cost-effective way to resolve your debt, stopping all penalties and interest from accruing.

- Short-Term Payment Plan: If you can pay your balance within 180 days, you might qualify for a short-term payment plan, though penalties and interest will continue to accrue.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to settle their tax liability with the IRS for a lower amount than what they originally owe. This option is typically available when taxpayers are experiencing significant financial difficulty, and the IRS believes it is unlikely to collect the full amount owed. Qualification for an OIC is stringent, often based on your ability to pay, income, expenses, and asset equity.

- Installment Agreement: If you can’t pay in full immediately and don’t qualify for an OIC, an installment agreement allows you to make monthly payments over an extended period (up to 72 months). This option is generally available to taxpayers who owe a combined total of $50,000 or less in tax, penalties, and interest (for individuals) or $25,000 or less (for businesses). While interest and penalties still apply, setting up an installment agreement prevents further collection actions.

- Currently Not Collectible (CNC) Status: In extreme cases of financial hardship, the IRS may determine that you are unable to pay your tax debt and place your account in “Currently Not Collectible” status. This is a temporary status, and the IRS can review your financial situation periodically.

Professional Assistance for Tax Debt: Expert Guidance

Navigating tax debt can be complex and emotionally draining. Consulting a qualified tax professional—such as a Certified Public Accountant (CPA), an Enrolled Agent (EA), or a tax attorney—can be immensely beneficial. These professionals can:

- Help you accurately determine your tax liability.

- Explain the various IRS notices and collection processes.

- Advise you on the best payment options for your specific financial situation.

- Represent you in communications with the IRS, negotiating payment plans or Offers in Compromise on your behalf.

- Help prepare and submit necessary documentation.

Their expertise can not only alleviate stress but also potentially save you money by identifying eligible penalty abatements or securing more favorable payment terms.

Proactive Strategies for Future Tax Management

Understanding what you owe is a reactive step. Moving forward, adopting proactive strategies is key to avoiding future tax surprises and maintaining good financial health.

Accurate Record Keeping: The Foundation of Good Tax Practice

Diligent record keeping is the bedrock of sound financial management and tax compliance. Maintaining accurate and organized records helps you:

- Support all income, deductions, and credits claimed on your tax return.

- Easily verify information against IRS records.

- Prepare for potential audits with confidence.

- Track past payments and communications with the IRS.

Keep records such as income statements (W-2s, 1099s), receipts for deductible expenses, bank and credit card statements, investment records, and any correspondence related to your taxes. Both physical and digital storage methods are acceptable, as long as they are secure and easily accessible.

Estimating and Adjusting Withholding: Avoiding Future Surprises

A common reason for owing the IRS is insufficient tax withholding throughout the year. For employees, this means your employer isn’t holding back enough from your paycheck. For self-employed individuals, it means not making adequate estimated tax payments.

The IRS Tax Withholding Estimator tool is an excellent resource to help you determine the correct amount of tax to have withheld from your pay. If you’re an employee, you can then adjust your Form W-4 with your employer. If you’re self-employed or have other income not subject to withholding, you may need to make quarterly estimated tax payments using Form 1040-ES. Regularly reviewing and adjusting your withholding or estimated payments helps ensure you don’t end up with a large balance due or, conversely, a massive refund that could have been in your pocket sooner.

![]()

Regular Financial Review: Staying Ahead of the Curve

Make it a habit to regularly review your financial situation and tax obligations. This includes:

- Periodically checking your IRS Online Account: Even outside of tax season, a quick check can alert you to any unexpected issues or updates from the IRS.

- Reviewing pay stubs and financial statements: Ensure that your income and withholding are on track.

- Staying informed about tax law changes: Tax laws can change frequently, impacting your deductions, credits, or income. Subscribing to financial newsletters or following reputable tax news sources can help you stay current.

By integrating these practices into your financial routine, you can prevent future tax debts from accumulating and maintain greater control over your financial well-being.

Ultimately, figuring out what you owe the IRS is a manageable process when armed with the right knowledge and tools. By leveraging the IRS’s digital platforms, understanding official communications, exploring payment options, and adopting proactive financial habits, you can confidently navigate your tax obligations and achieve financial peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.