Navigating the complexities of tax season and managing your financial obligations can often feel like a daunting task. One critical aspect of responsible financial stewardship is understanding your tax standing, specifically knowing if you owe the Internal Revenue Service (IRS) money, and if so, how much. An unexpected tax bill can disrupt even the most meticulously planned budget, underscorring the importance of proactively checking your IRS balance. This article will serve as a comprehensive guide, demystifying the process of checking your IRS balance, understanding what it means, and exploring the official channels available for inquiry and resolution, all within the crucial domain of personal finance.

For many, the IRS is synonymous with stress and obligation. However, the agency provides several accessible tools designed to help taxpayers stay informed and compliant. Whether you’re anticipating a payment, reconciling previous years’ taxes, or simply curious about your current tax account status, knowing how to access this information is a fundamental skill for sound financial health. Let’s delve into the specific methods and strategies for gaining clarity on your IRS balance, ensuring you’re always in control of your financial relationship with the tax authority.

Understanding Your IRS Balance: What It Means and Why It Matters

Before diving into the “how-to,” it’s essential to grasp the fundamental concept of an “IRS balance” and its implications for your personal finance strategy. This isn’t just about a number; it reflects your financial responsibility to the government and can significantly impact your future financial planning.

Defining Your IRS Balance

When we talk about an “IRS balance,” we’re generally referring to a situation where you owe the government money. This could be due to several reasons:

- Unpaid Taxes: You may have underpaid your estimated taxes throughout the year, or your employer might have withheld less than your actual tax liability.

- Penalties: The IRS can assess penalties for various reasons, including failure to file on time, failure to pay on time, or inaccurate tax preparation. These penalties add to your overall balance.

- Interest: Interest is charged on underpayments and unpaid taxes from the original due date of the tax until the date of payment. Interest can compound, significantly increasing your total balance over time.

- Audit Adjustments: If your tax return was audited, and the IRS determined you owed additional tax, this would contribute to your balance due.

Conversely, some individuals might refer to their “IRS balance” in the context of a refund due. While the methods for checking the status are similar, the focus of this guide is primarily on understanding and managing liabilities.

The Importance of Knowing Your Balance

Proactively checking your IRS balance isn’t merely about curiosity; it’s a critical component of responsible financial management.

- Avoiding Further Penalties and Interest: The most immediate benefit is preventing additional financial burdens. Unpaid balances accrue interest daily, and penalties for non-payment can rapidly increase your debt. Knowing your balance allows you to pay it promptly or arrange a payment plan, mitigating these costs.

- Informed Financial Planning: Your tax obligations directly impact your disposable income and savings capacity. Understanding your current or projected balance allows you to adjust your budget, allocate funds, or make informed decisions about investments and major purchases.

- Maintaining Good Standing with the IRS: Ignoring tax liabilities can lead to more severe consequences, including liens, levies, and even wage garnishment. Staying informed and compliant helps you avoid these stressful and financially damaging actions, preserving your financial integrity.

- Peace of Mind: Perhaps less tangible but equally important is the psychological benefit. Knowing where you stand with the IRS eliminates uncertainty and contributes to overall financial peace of mind, allowing you to focus on other financial goals without this looming concern.

Common Reasons for an IRS Balance Due

Understanding why you might owe the IRS can help prevent future surprises.

- Under-withholding: This is a common culprit. If you don’t update your Form W-4 with your employer when life events (marriage, new child, second job) change your tax situation, too little tax might be withheld from your paychecks.

- Estimated Tax Discrepancies: Self-employed individuals, gig workers, and those with significant investment income are often required to pay estimated taxes quarterly. Miscalculating these payments or missing deadlines can lead to a balance due.

- Significant Income Changes: A sudden increase in income without corresponding adjustments to withholding or estimated payments can result in a higher tax liability than anticipated.

- Audit Adjustments or Errors: Sometimes, an error on your tax return, or an audit that uncovers unreported income or disallowed deductions, can result in an unexpected balance due.

Official Methods to Directly Check Your IRS Balance

The IRS provides several secure and official channels for taxpayers to check their balance, review their payment history, and understand their tax account status. These tools are designed to empower you with direct access to your financial information with the agency.

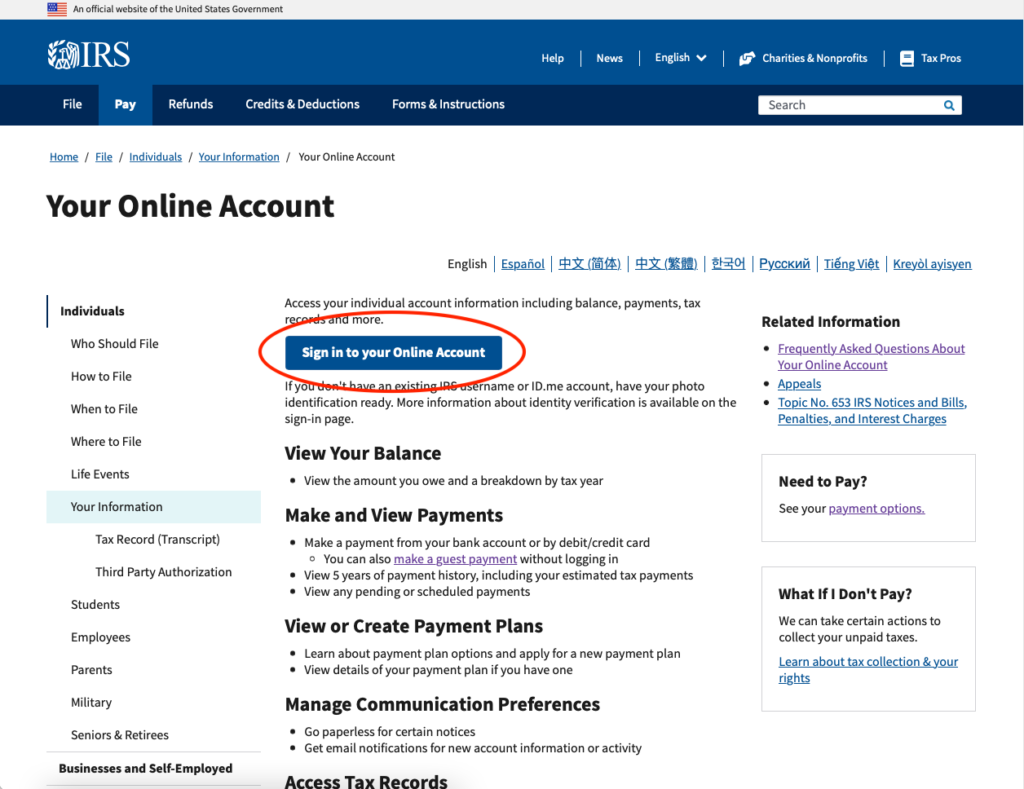

IRS Online Account

The IRS Online Account is arguably the most comprehensive and convenient tool for checking your balance and managing your tax affairs. It’s a secure portal that offers a wealth of information at your fingertips.

- Features: Through your IRS Online Account, you can:

- View your tax balance, including tax, penalties, and interest.

- See your payment history and any scheduled or pending payments.

- Access key tax records, including your adjusted gross income (AGI) for previous years.

- View tax transcripts (e.g., account transcript, tax return transcript).

- Set up a payment plan (installment agreement) if you owe money.

- View digital copies of certain IRS notices.

- Registration Process: To access your IRS Online Account, you’ll need to create an account and verify your identity through a multi-step process, which may involve providing personal information, financial account details, and potentially receiving a verification code via mail. This robust verification ensures the security of your sensitive tax data.

- Information Available: Once logged in, you can see your current tax liability for each tax year, broken down by tax due, penalties, and interest. This level of detail is invaluable for precise financial planning and resolution.

Checking Via Phone

For those who prefer direct human interaction or cannot access the online services, contacting the IRS by phone is another official method.

- IRS Customer Service Numbers: The general number for individual taxpayer inquiries is 1-800-829-1040. Be aware that specific issues (e.g., business taxes, payment plans) may have dedicated lines. The best times to call are typically early in the morning (8 a.m. to 10 a.m. local time) or later in the afternoon (3 p.m. to 5 p.m. local time), and mid-week (Tuesday to Thursday) to avoid peak call volumes.

- Information to Have Ready: When you call, the IRS representative will need to verify your identity. Be prepared to provide your Social Security number (SSN), date of birth, filing status, and the address from your last filed tax return. It’s also helpful to have a copy of your most recent tax return handy.

- Typical Wait Times: Due to high call volumes, especially during tax season, wait times can be substantial. The IRS website often provides estimates for current wait times, which can help you plan your call.

Requesting a Transcript

Tax transcripts provide a summary of your tax return information and are often used by lenders or for verification purposes. An “account transcript” specifically can help you understand your balance.

- Types of Transcripts:

- Account Transcript: Shows most line items from a tax return, but it may also display changes made by the taxpayer or the IRS after the original return was filed. It provides information about your tax account, including payments made, penalties assessed, and current balance.

- Tax Return Transcript: Shows most line items from your original tax return (Form 1040, 1040A, or 1040EZ) as you filed it, including any accompanying forms and schedules. It doesn’t include changes made after the return was filed.

- How to Request:

- Online: Use the “Get Transcript Online” tool on the IRS website. You’ll need to verify your identity using a secure process.

- By Mail: Use “Get Transcript by Mail.” You’ll receive your transcript at the address on file with the IRS within 5 to 10 calendar days.

- By Fax or Mail (Form 4506-T/4506T-EZ): For more complex requests or if online options aren’t suitable, you can fill out Form 4506-T (Request for Transcript of Tax Return) or Form 4506T-EZ (Short Form Request for Individual Tax Return Transcript) and fax or mail it to the IRS.

Mail Correspondence

The IRS often communicates balances due through official notices sent via mail. These notices are direct indicators of your tax liability and should never be ignored.

- Official Notices: Examples include:

- CP14: Notice of Balance Due, often for unpaid taxes.

- CP504: Notice of Intent to Levy, a more serious notice indicating the IRS may seize property or assets if the balance is not paid.

- LT11: Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

- Responding to Notices: It’s crucial to read these notices carefully, understand the balance due, and follow the instructions provided. Often, they will detail the amount owed, the reason for the balance, and payment options or avenues for appealing the decision. If you disagree, there are procedures for responding and potentially disputing the balance.

Managing and Resolving Your IRS Balance

Discovering you owe the IRS can be unsettling, but proactive management and understanding your options are key to resolving the situation effectively. The IRS provides several pathways for taxpayers to fulfill their obligations, even when facing financial hardship.

Understanding Penalties and Interest

One of the primary motivations for promptly addressing an IRS balance is to minimize additional costs.

- How They Accrue: Penalties are assessed for specific non-compliance issues, such as failure to file or failure to pay on time. Interest, on the other hand, is charged on the unpaid balance, including any penalties, from the due date of the tax until the full payment is received. Both accumulate daily, meaning the longer you wait, the more expensive your liability becomes.

- Why Prompt Action is Crucial: Acting quickly can significantly reduce the total amount you eventually have to pay. If you know you’ll owe, it’s generally better to pay as much as you can, even if not the full amount, to reduce the principal on which interest and penalties are calculated.

Payment Options Available

Once you know your balance, the next step is to make a payment. The IRS offers a variety of convenient methods:

- Direct Pay (Bank Account): The most popular and often recommended method. IRS Direct Pay allows you to pay your taxes directly from your checking or savings account with no fees. You can schedule payments up to 365 days in advance.

- Debit Card, Credit Card, or Digital Wallet: You can pay using a third-party payment processor via debit card, credit card, or digital wallet (e.g., PayPal). Be aware that these processors charge a fee, which varies depending on the service and the card type.

- Electronic Federal Tax Payment System (EFTPS): This free service is primarily for business taxpayers but can also be used by individuals. It requires enrollment and allows you to make federal tax payments online or by phone.

- Check or Money Order: You can mail a check or money order directly to the IRS. Ensure you include the correct payment voucher (Form 1040-V) and write your SSN, the tax year, and the form number on your payment.

- Cash: The IRS has partnered with various retail stores that offer a secure way to pay federal taxes with cash. This option usually requires an appointment and processing fees.

What If You Can’t Pay? Exploring Payment Plans

If you cannot pay your full tax balance immediately, the IRS offers several options to help you manage your debt. It’s crucial to contact the IRS as soon as possible to discuss these options rather than ignoring the problem.

- Short-Term Payment Plan: You may be granted up to 180 additional days to pay your tax liability in full, although interest and penalties still apply. This is an informal agreement and doesn’t require a formal installment agreement application.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. An OIC is typically granted when a taxpayer’s financial situation prevents them from paying the full amount and will not be able to pay it in the foreseeable future. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating an OIC.

- Installment Agreement: This allows you to make monthly payments for up to 72 months. You can apply online, by phone, or by mail. Setting up an installment agreement incurs a one-time fee, and interest and penalties continue to accrue, albeit at a reduced rate for certain penalties.

- Currently Not Collectible (CNC) Status: If the IRS determines that you cannot pay any of your tax debt due to financial hardship, it may place your account in currently not collectible status. While in this status, the IRS will temporarily stop collection efforts, but interest and penalties continue to accrue. This is usually a temporary status, and the IRS may review your financial situation periodically.

Seeking Professional Assistance

For complex tax situations, significant balances, or when navigating payment plans and appeals, consulting a qualified tax professional is often advisable.

- When to Consult a Professional: Consider hiring an Enrolled Agent (EA), Certified Public Accountant (CPA), or tax attorney if you:

- Owe a substantial amount and are unsure of your best payment or resolution strategy.

- Are considering an Offer in Compromise.

- Are facing an audit or have received an aggressive collection notice (e.g., levy or lien).

- Need assistance negotiating with the IRS.

- Have complex financial situations impacting your ability to pay.

A professional can provide expert guidance, represent you before the IRS, and help ensure you choose the most favorable resolution strategy for your specific circumstances.

Proactive Strategies to Avoid Future IRS Balances

The best way to manage an IRS balance is to avoid having one in the first place. Integrating proactive tax planning into your overall personal finance strategy can save you stress, time, and money in the long run.

Adjusting Withholding (W-4 Form)

For most employed individuals, ensuring the correct amount of tax is withheld from your paycheck is the simplest and most effective way to prevent an unexpected tax bill.

- How to Use Form W-4: Review and update your Form W-4 (Employee’s Withholding Certificate) whenever there are significant changes in your life, such as marriage, divorce, birth or adoption of a child, purchase of a home, or a second job. The IRS Tax Withholding Estimator tool on their website is an excellent resource for calculating the appropriate withholding. Adjusting your W-4 can either reduce your refund (allowing you to have more money in each paycheck) or increase your withholding to cover potential liabilities, avoiding a balance due.

Making Estimated Tax Payments

If you earn income not subject to withholding (e.g., self-employment income, rental income, interest, dividends), you are likely required to pay estimated taxes quarterly.

- Who Needs to Pay: Individuals who expect to owe at least $1,000 in tax (or corporations expecting to owe $500 or more) from income not subject to withholding typically need to pay estimated taxes.

- Calculating and Paying: Use Form 1040-ES (Estimated Tax for Individuals) to calculate your estimated tax. You can pay estimated taxes online via IRS Direct Pay, EFTPS, or by mail. Missing these payments or underpaying can result in penalties, so regular review of your income and adjustments to your estimated payments are crucial.

Keeping Meticulous Records

Good record-keeping is the bedrock of accurate tax preparation and financial compliance.

- Importance of Documentation: Maintain organized records of all income sources, expenses, charitable contributions, medical expenses, and any other relevant financial transactions. This includes W-2s, 1099s, bank statements, receipts, and mileage logs.

- Benefits: Meticulous records not only simplify tax preparation but also provide undeniable proof of your income and deductions in case of an IRS inquiry or audit, helping to prevent discrepancies that could lead to a balance due.

Regular Financial Reviews

Tax planning shouldn’t be a once-a-year event. Integrating it into your ongoing financial management can lead to better outcomes.

- Integrating Tax Planning: Periodically (e.g., quarterly or semi-annually), review your income, expenses, and any major life changes to assess their potential tax impact.

- Professional Consultation: Consider a year-end tax planning session with a financial advisor or tax professional. They can help identify potential deductions, credits, and strategies to optimize your tax situation and prevent surprises at tax time. This proactive approach ensures you’re always ahead of your tax obligations.

Staying informed about your IRS balance is a non-negotiable aspect of sound personal finance. By understanding the various official methods to check your balance, recognizing what those numbers mean, and proactively implementing strategies to manage and avoid future liabilities, you empower yourself to navigate the world of taxes with confidence and clarity. The tools and resources provided by the IRS, combined with diligent personal financial management, are your strongest allies in maintaining a healthy and compliant tax standing. Don’t let uncertainty be a source of stress; take charge of your tax information today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.