For many, owning a home represents the quintessential American dream, a cornerstone of financial stability and personal fulfillment. Yet, achieving this dream often necessitates navigating one of the most significant financial commitments of a lifetime: the house mortgage. Far from being a simple loan, a mortgage is a complex financial instrument that underpins the vast majority of real estate transactions, allowing individuals to purchase property without paying the full price upfront. Understanding the intricacies of a mortgage is not just an academic exercise; it is an essential step towards making informed decisions that will impact your financial future for decades.

This comprehensive guide aims to demystify the house mortgage, breaking down its core components, exploring the various types available, walking through the application process, and shedding light on the strategic considerations that every homeowner and prospective buyer should understand. By delving into the world of mortgages, you can equip yourself with the knowledge needed to secure the best terms, manage your financial obligations effectively, and ultimately transform the dream of homeownership into a tangible reality.

Understanding the Fundamentals of a House Mortgage

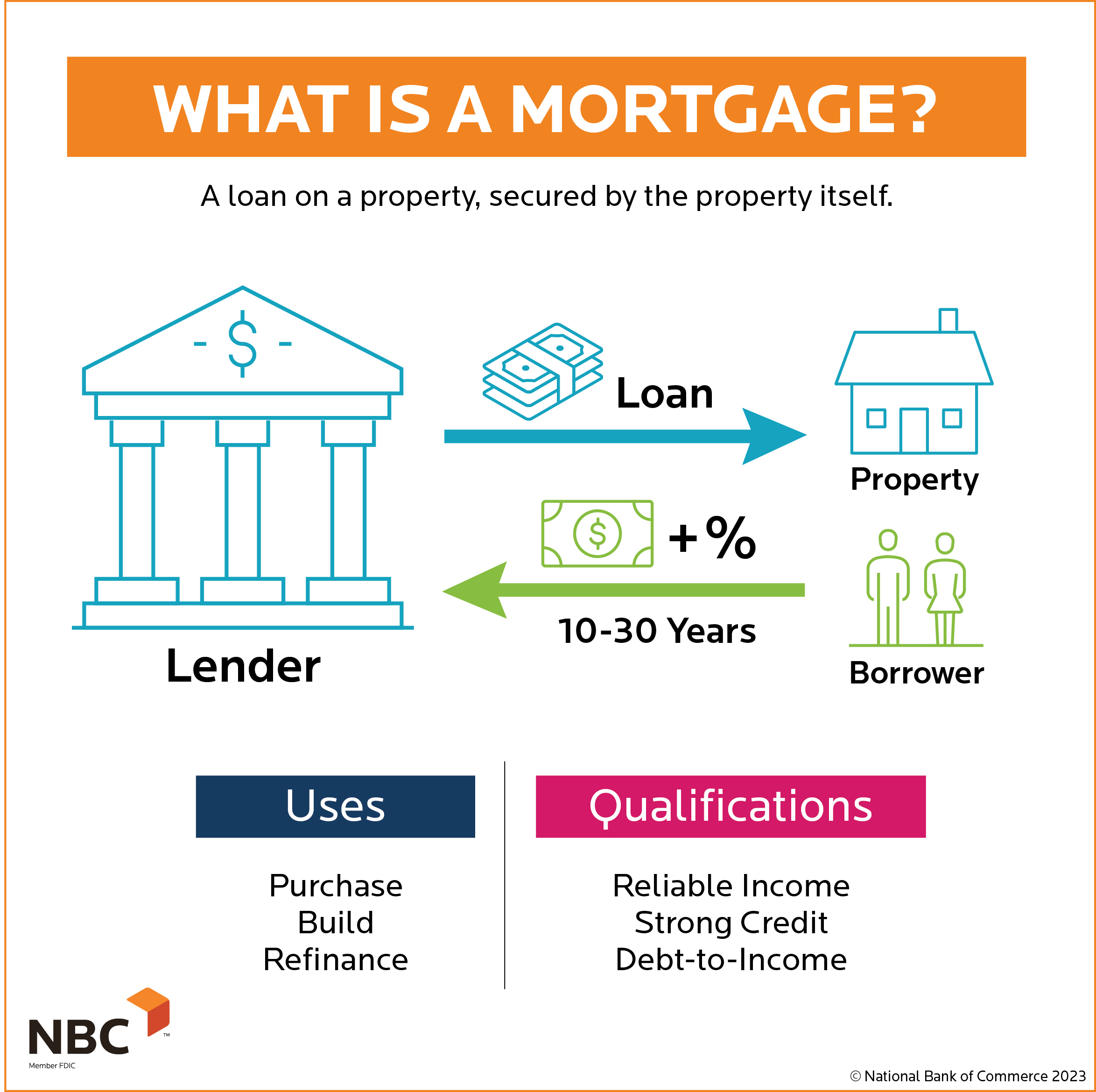

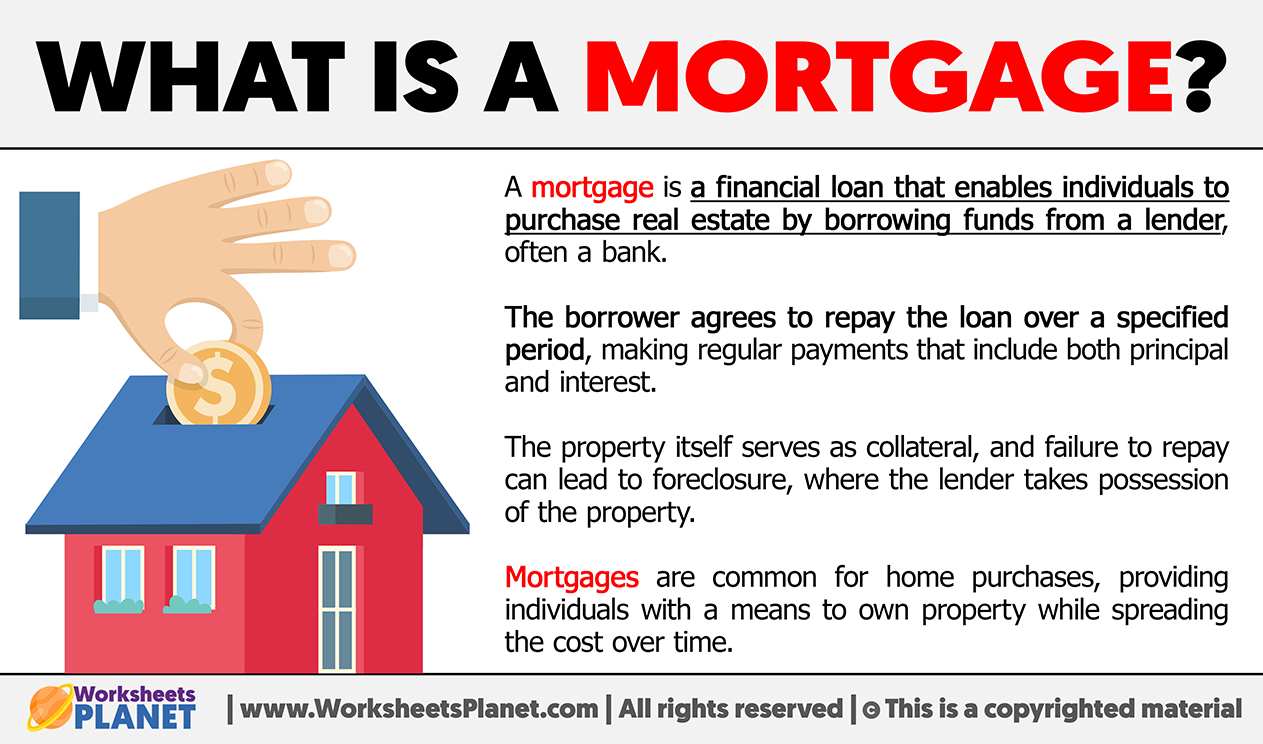

At its heart, a house mortgage is a loan specifically for buying real estate. It’s a contract between you (the borrower) and a financial institution (the lender) where the lender provides funds to purchase a property, and in return, you agree to repay the loan over a set period, typically with interest. The property itself serves as collateral for the loan, meaning if you fail to make your payments, the lender has the right to repossess the property through a process known as foreclosure.

The Core Definition and Purpose

A mortgage is essentially a secured loan. Unlike an unsecured personal loan, which relies solely on your creditworthiness, a mortgage is “secured” by the asset it’s used to purchase – your home. This security is what allows lenders to offer larger sums of money at more favorable interest rates compared to other types of loans. The primary purpose of a mortgage is to make homeownership accessible by distributing the substantial cost of a home over many years, usually 15 to 30. This allows individuals and families to acquire an appreciating asset without needing to save the entire purchase price upfront.

Key Components: Principal, Interest, Escrow, and Term

To truly understand a mortgage, it’s crucial to grasp its fundamental components:

- Principal: This is the actual amount of money borrowed to purchase the home. Every payment you make chipping away at this principal balance builds equity in your home.

- Interest: This is the cost of borrowing the principal amount. It’s expressed as a percentage rate and is a significant portion of your monthly payment, especially in the early years of the loan. The total interest paid over the life of a loan can often exceed the original principal amount.

- Escrow: An escrow account is a special account managed by your lender to pay property taxes and homeowner’s insurance premiums on your behalf. A portion of your monthly mortgage payment goes into this account. It simplifies these payments for you and ensures these crucial expenses are covered, protecting the lender’s interest in the property.

- Term: This refers to the duration over which you agree to repay the loan, typically 15, 20, or 30 years. A shorter term usually means higher monthly payments but less interest paid over the life of the loan, while a longer term offers lower monthly payments but more interest over time.

The Role of Lenders and Borrowers

In a mortgage transaction, the lender (e.g., bank, credit union, mortgage company) provides the capital, assesses risk, and sets the terms of the loan. Their goal is to ensure the loan is repaid and to generate profit through interest. The borrower, on the other hand, is the individual or entity receiving the funds. Their role is to adhere to the terms of the mortgage agreement, making timely payments and maintaining the property as stipulated. A healthy relationship built on transparency and mutual understanding is critical for a smooth homeownership journey.

Navigating the Different Types of Mortgages

The mortgage landscape is diverse, offering various products designed to fit different financial situations and borrower profiles. Choosing the right type of mortgage is a critical decision that can significantly impact your monthly payments, the total cost of your home, and your financial flexibility.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

- Fixed-Rate Mortgages (FRMs): As the name suggests, the interest rate on a fixed-rate mortgage remains constant for the entire life of the loan. This provides predictability and stability in your monthly payments, making budgeting easier and protecting you from potential interest rate increases. The most common terms are 15-year and 30-year fixed-rate mortgages.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an interest rate that changes periodically after an initial fixed period (e.g., 3/1, 5/1, 7/1 ARMs). For the initial period, the rate is fixed and often lower than a comparable fixed-rate mortgage. After this period, the rate adjusts up or down based on a specified market index, plus a margin. ARMs can offer lower initial payments but come with the risk of future payment increases, which can be challenging if not properly anticipated.

Government-Insured Loans: FHA, VA, and USDA

These mortgage types are backed by various government agencies, making homeownership more accessible to specific groups:

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers and those with lower credit scores or smaller down payments (as low as 3.5%). They require mortgage insurance premiums, both upfront and annually.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, VA loans are available to eligible service members, veterans, and surviving spouses. They offer significant benefits, including no down payment requirements and no private mortgage insurance (PMI).

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income individuals purchasing homes in eligible rural areas. They also typically require no down payment.

Conventional Mortgages and Jumbo Loans

- Conventional Mortgages: These are loans that are not insured or guaranteed by a government agency. They often require higher credit scores and down payments (typically 5% to 20%). If your down payment is less than 20%, you’ll generally be required to pay private mortgage insurance (PMI), which protects the lender in case you default.

- Jumbo Loans: When a conventional loan exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA), it’s considered a jumbo loan. These are used for higher-value properties and typically come with stricter qualification requirements, including higher credit scores and larger down payments.

Understanding Niche Mortgage Products

Beyond the main categories, there are other specialized mortgage products. Interest-only mortgages, for example, allow borrowers to pay only the interest for a set period, resulting in lower initial payments but without building equity during that time. Reverse mortgages allow homeowners (usually seniors) to convert a portion of their home equity into cash without having to sell the home or make monthly mortgage payments. These niche products cater to very specific financial situations and carry unique risks and benefits that require careful consideration.

The Mortgage Application Process: A Step-by-Step Guide

The journey from dreaming about a home to holding the keys involves a structured application process. While it can seem daunting, breaking it down into manageable steps makes it less intimidating.

Pre-Qualification vs. Pre-Approval

The first step is typically to gauge what you can afford:

- Pre-Qualification: This is an informal assessment based on basic financial information you provide to a lender (income, debt, assets). It gives you a rough estimate of what you might be able to borrow.

- Pre-Approval: This is a more rigorous process. You submit actual financial documents (pay stubs, bank statements, tax returns), and the lender conducts a credit check. A pre-approval letter is a conditional commitment from the lender to loan you a specific amount, making your offer more competitive to sellers.

Gathering Essential Documentation

Once you’re ready for pre-approval or to formally apply, you’ll need to compile a comprehensive dossier of your financial life. This typically includes:

- Proof of income (W-2s, pay stubs, tax returns for the past two years)

- Bank statements and investment account statements

- Identification (driver’s license, social security card)

- Information on existing debts (car loans, student loans, credit cards)

- Rental history (if applicable)

Underwriting: What Lenders Look For

After submitting your application and documentation, your file moves to underwriting. This is where the lender thoroughly assesses your financial health and risk profile. They will scrutinize:

- Credit History: Your credit score and history of responsible debt repayment are crucial.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders typically look for a DTI below 43% for most conventional loans.

- Employment History: Lenders prefer a stable work history, usually two years in the same field or with the same employer.

- Assets: They’ll verify you have sufficient funds for the down payment, closing costs, and a reserve cushion.

The underwriter’s job is to ensure you meet all lending criteria and that the loan represents an acceptable risk for the institution.

The Closing Process

If your loan is approved by underwriting, you’re on the home stretch. The closing is the final stage where all parties (buyer, seller, lenders, real estate agents, attorneys/title company) gather to sign numerous documents. At closing, you’ll pay your down payment and closing costs, and ownership of the property legally transfers to you. Key documents include the promissory note (your promise to repay the loan) and the mortgage (the legal document that pledges the property as collateral).

Beyond Approval: Managing Your Mortgage and Its Financial Implications

Securing a mortgage is a significant achievement, but the financial journey continues long after you get the keys. Effectively managing your mortgage means understanding your ongoing financial obligations and how your payments contribute to your long-term wealth.

Decoding Your Monthly Mortgage Payment

Your monthly mortgage payment is usually composed of four main elements, often referred to as PITI:

- Principal: The portion that reduces your loan balance.

- Interest: The cost of borrowing money.

- Taxes: Property taxes collected by your lender and held in escrow.

- Insurance: Homeowner’s insurance premiums (and potentially private mortgage insurance) also held in escrow.

Understanding how these components are allocated is key to financial planning. Early in the loan term, a larger portion of your payment goes towards interest, while later, more goes towards principal.

Understanding Amortization Schedules

An amortization schedule details every payment you’ll make over the life of your loan, showing how much goes towards principal and how much towards interest. Reviewing this schedule highlights the front-loaded nature of interest payments. Observing how your principal balance slowly decreases initially can be a powerful motivator for making extra payments.

The Impact of Interest Rates and Loan Terms

Even a small difference in your interest rate can translate to tens of thousands of dollars over the life of a 30-year mortgage. Similarly, choosing a shorter loan term (e.g., 15 years instead of 30) dramatically reduces the total interest paid, despite higher monthly payments. These are critical factors to weigh during the initial decision-making process, as they define your long-term financial commitment.

Escrow Accounts and Property Taxes/Insurance

As mentioned, your lender typically manages an escrow account for property taxes and homeowner’s insurance. While convenient, it’s important to understand that your escrow payment can fluctuate. Increases in property values (leading to higher taxes) or insurance premiums can cause your monthly mortgage payment to rise, even if your principal and interest remain fixed. Lenders usually conduct an annual escrow analysis to adjust your payments accordingly.

Strategic Considerations for Mortgage Holders

A mortgage isn’t a static financial product; it’s a dynamic tool that can be strategically managed to optimize your financial position over time. Understanding when and how to leverage options like refinancing or early repayment can significantly impact your net worth.

Refinancing: When and Why?

Refinancing involves replacing your existing mortgage with a new one, often to secure a lower interest rate, change the loan term, or convert an ARM to a fixed-rate loan. It can be a smart move when:

- Interest rates have dropped significantly since you originated your current loan.

- Your credit score has improved, qualifying you for better terms.

- You want to switch from an ARM to a stable fixed-rate mortgage.

- You need to pull cash out of your home equity for other financial goals (cash-out refinance).

However, refinancing involves closing costs, so it’s essential to calculate if the savings outweigh the expenses.

Accelerating Your Mortgage Repayment

Paying off your mortgage early can save you a substantial amount in interest and free up your monthly budget sooner. Strategies include:

- Making extra principal payments: Even small, consistent additional payments can shave years off your loan.

- Bi-weekly payments: Paying half your monthly payment every two weeks results in 13 full payments per year instead of 12.

- Using windfalls: Applying bonuses, tax refunds, or other unexpected income directly to your principal.

The Decision to Sell or Stay

Life circumstances change, and sometimes the decision arises whether to sell your home or remain in it. Your mortgage plays a crucial role here. If you sell, you’ll need to pay off the remaining mortgage balance. If you stay but need to adapt the property (e.g., for retirement or a growing family), understanding your remaining mortgage obligation and potential home equity can inform decisions about renovations or reverse mortgages.

Leveraging Your Home Equity Wisely

As you pay down your mortgage and your home’s value potentially appreciates, you build home equity. This equity can be a valuable financial asset. It can be leveraged through:

- Home Equity Loans (HELs): A lump sum loan against your equity, repaid with a fixed interest rate over a set term.

- Home Equity Lines of Credit (HELOCs): A revolving line of credit that you can draw from as needed, similar to a credit card but secured by your home.

These tools can finance major expenses like home renovations, education, or debt consolidation, but they must be used cautiously, as your home serves as collateral.

Conclusion

A house mortgage is much more than a financial product; it is the gateway to homeownership for millions, offering both profound benefits and significant responsibilities. By thoroughly understanding its definition, exploring the various types available, meticulously navigating the application process, and strategically managing its long-term financial implications, aspiring and current homeowners can approach this critical commitment with confidence and foresight. The journey of a mortgage is a marathon, not a sprint, and with the right knowledge, it can be a powerful tool for building wealth and securing a stable future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.