In the intricate world of personal and business finance, understanding interest rates is paramount. For many, a loan represents a significant financial commitment, a gateway to a new home, a crucial business investment, or a lifeline in an unexpected emergency. At the heart of every loan agreement lies the interest rate—the cost of borrowing money. But what exactly constitutes a “good” loan interest rate? The answer, unfortunately, is rarely a simple number. Instead, it’s a dynamic interplay of market conditions, lender policies, your individual financial health, and the specific type of loan you’re seeking. Defining “good” requires a nuanced understanding of these factors, empowering you to make informed decisions that align with your financial goals.

Understanding the Fundamentals of Loan Interest Rates

Before we can even begin to define what makes an interest rate “good,” it’s crucial to grasp the foundational concepts that underpin how these rates are determined and what they represent. This understanding forms the bedrock of savvy borrowing.

What is an Interest Rate?

At its simplest, an interest rate is the percentage charged by a lender to a borrower for the use of assets, typically expressed as an annual percentage of the loan principal. This is the cost you pay for the privilege of borrowing money. When discussing loans, two primary types of interest rates are often mentioned: the nominal interest rate and the Annual Percentage Rate (APR).

The nominal interest rate is the stated rate on the loan, not accounting for any fees or compounding. The Annual Percentage Rate (APR), on the other hand, is a more comprehensive measure of the cost of borrowing. It includes the nominal interest rate plus any additional fees or charges imposed by the lender, such as origination fees, closing costs, or discount points. For consumers, the APR is often the more useful figure for comparing loan offers, as it provides a clearer picture of the total annual cost of the loan. While a lower nominal rate might look appealing, a higher APR due to hidden fees can make it a more expensive option in the long run.

Factors Influencing Interest Rates

Interest rates don’t just appear out of thin air; they are the result of a complex calculation involving numerous variables. Understanding these influences can help you anticipate rates and improve your position as a borrower.

- Credit Score and History: This is arguably the most significant individual factor. A higher credit score (typically above 700-750) signals to lenders that you are a responsible borrower with a strong history of repaying debts. Lenders perceive lower risk with high credit scores, leading them to offer lower interest rates. Conversely, a low credit score indicates higher risk, resulting in higher interest rates to compensate the lender for that perceived risk.

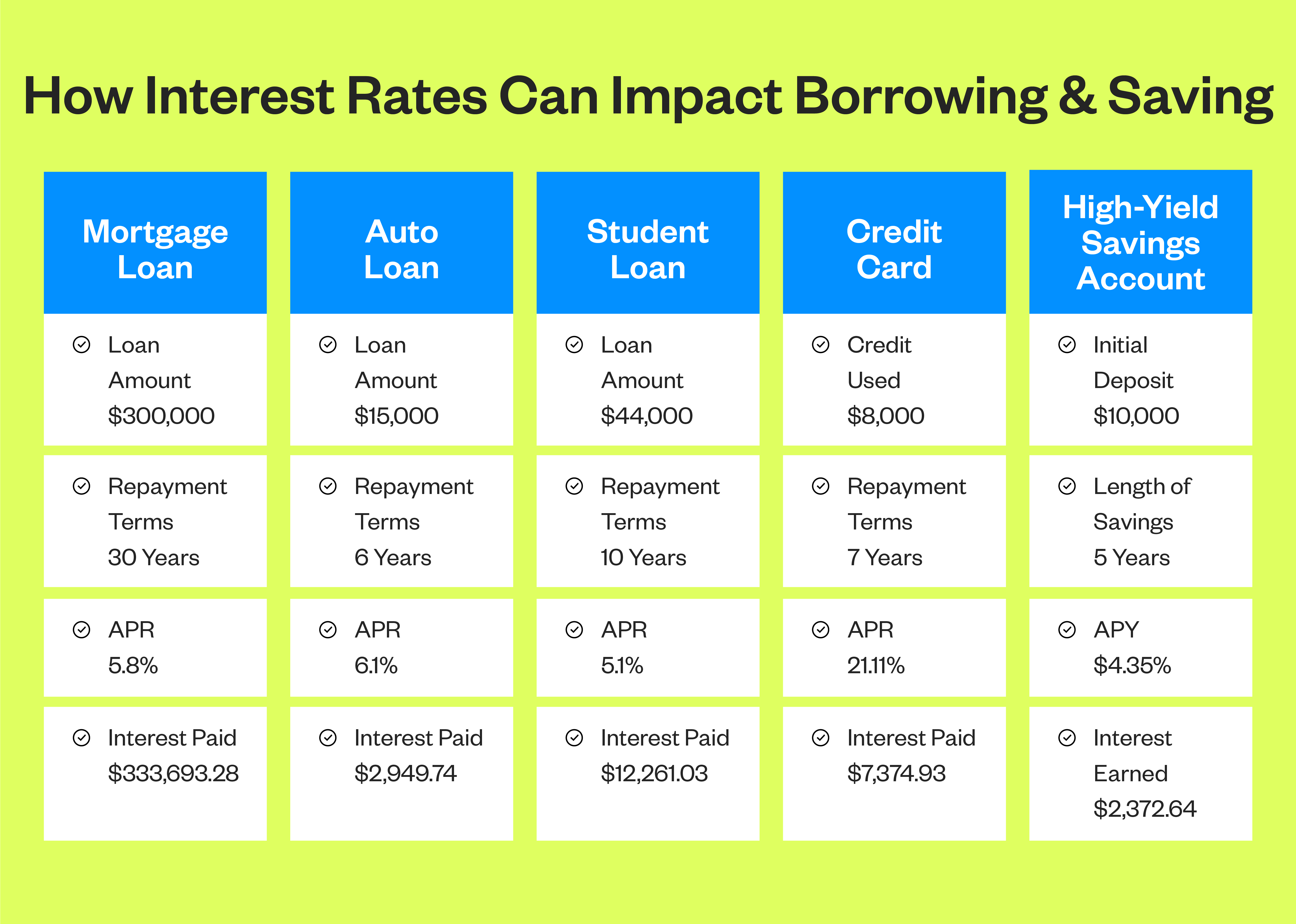

- Loan Type: Different loan products inherently carry different risk profiles and, consequently, different rate structures. Mortgages, secured by real estate, generally have lower rates than unsecured personal loans or credit cards. Auto loans fall somewhere in between, secured by the vehicle itself.

- Market Rates and Economic Conditions: Broader economic factors play a huge role. The federal funds rate set by central banks (like the Federal Reserve in the U.S.) influences the prime rate, which in turn impacts consumer loan rates. During periods of economic growth and low inflation, rates might be higher as demand for money increases. During recessions, central banks often lower rates to stimulate borrowing and economic activity. Inflation expectations also directly impact interest rates; lenders will demand higher rates to protect the purchasing power of their returns.

- Lender’s Risk Assessment: Beyond your credit score, lenders assess other risks. This includes your debt-to-income ratio (DTI), employment stability, and even the loan-to-value (LTV) ratio for secured loans. A higher DTI or less stable employment can lead to a higher rate.

- Loan Term: Generally, shorter loan terms carry lower interest rates because the lender’s risk is contained over a shorter period. Longer loan terms, while offering lower monthly payments, typically come with higher interest rates and result in more interest paid over the life of the loan.

Fixed vs. Variable Rates

Another critical distinction is between fixed-rate and variable-rate loans.

- Fixed-Rate Loans: The interest rate remains constant for the entire duration of the loan. This provides predictability and stability in your monthly payments, making budgeting easier. It’s an excellent choice if you believe interest rates might rise in the future or if you value payment consistency. Mortgages and most personal loans are commonly fixed-rate.

- Variable-Rate Loans (or Adjustable-Rate Loans – ARMs): The interest rate can fluctuate over the loan term, usually tied to an underlying index (like the prime rate or LIBOR/SOFR). While variable rates often start lower than fixed rates, they carry the risk of increasing, leading to higher monthly payments. These can be attractive if you expect rates to fall or if you plan to pay off the loan quickly before rates have a chance to rise significantly. However, they introduce an element of uncertainty into your financial planning.

Defining ‘Good’ in Context: Different Loan Types

The definition of a “good” interest rate is highly contextual. A rate considered excellent for a credit card would be abysmal for a mortgage. Let’s break down what constitutes a competitive rate across various common loan types.

Personal Loans

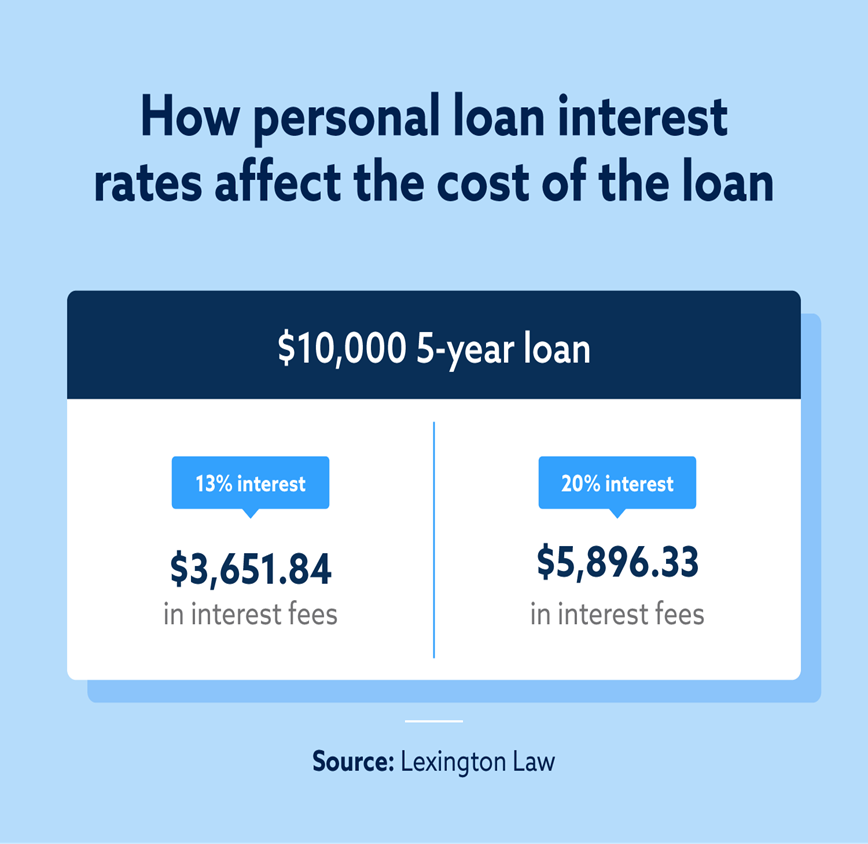

Personal loans are typically unsecured, meaning they aren’t backed by collateral. This inherently makes them riskier for lenders, resulting in higher interest rates compared to secured loans. A “good” personal loan interest rate usually falls between 6% and 15% APR for borrowers with excellent credit (740+). For those with good credit (670-739), rates might range from 10% to 20% APR. If your credit is fair or poor, you could see rates exceeding 25% or even 30% APR. Given the higher average rates, anything below 10% is generally considered excellent, while anything above 20% warrants careful consideration due to the substantial cost over the loan term.

Mortgages

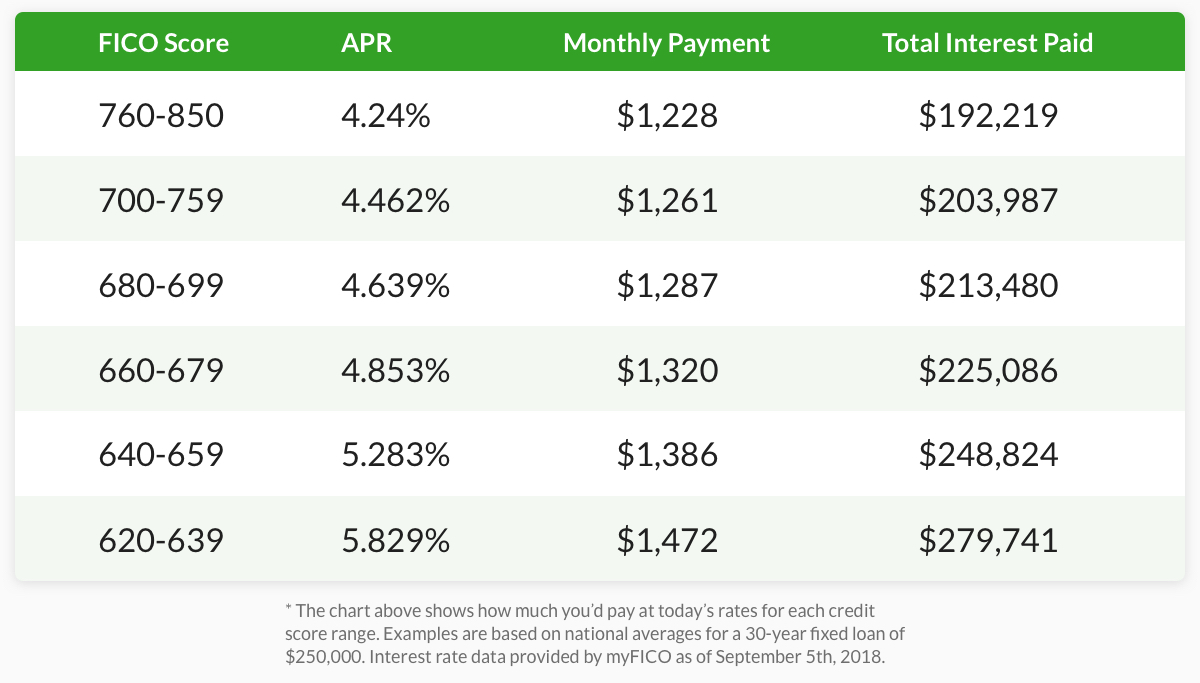

Mortgages, being secured by real estate, generally boast some of the lowest interest rates available. Historical averages fluctuate, but in stable economic periods, a “good” mortgage rate for a 30-year fixed-rate loan is typically anything below the prevailing market average, which can range from 3% to 7% APR depending on the economic climate. For borrowers with excellent credit (760+ FICO), rates can be at the lower end of this spectrum or even slightly below the market average. A “good” rate also depends on the type of mortgage (e.g., FHA, VA, conventional) and the loan term (15-year mortgages often have lower rates than 30-year ones). Even a quarter-point difference can save tens of thousands of dollars over the life of a large mortgage.

Auto Loans

Auto loans are secured by the vehicle you purchase. Rates vary based on whether the car is new or used, the loan term, and your creditworthiness. For a new car, borrowers with excellent credit might secure rates as low as 0% to 3% APR (often promotional offers from manufacturers) or more commonly 3% to 6% APR. For used cars, rates are typically higher, ranging from 5% to 10% APR for good credit, as used vehicles are considered higher risk and depreciate faster. Anything below 5% for a new car and below 7% for a used car is generally considered a strong rate.

Student Loans

Student loans can be federal or private. Federal student loans offer generally consistent, fixed interest rates determined by Congress, regardless of the borrower’s credit score (though eligibility for certain loan types depends on financial need). These rates are often among the lowest available and include benefits like income-driven repayment and deferment options. For the 2023-2024 academic year, undergraduate federal loan rates were around 5.50% APR, and graduate loans around 7.05% APR. Private student loans, conversely, are credit-based and can have fixed or variable rates. A “good” private student loan rate would be anything comparable to or below federal rates, generally in the 4% to 8% APR range for well-qualified borrowers. High-interest private loans can easily exceed 10-12% APR, making them a less desirable option.

Credit Cards

Credit cards typically carry the highest interest rates among all loan types due to their unsecured nature and revolving credit lines. A “good” credit card interest rate is usually an oxymoron; the objective is often to avoid paying interest altogether by paying your balance in full each month. However, if carrying a balance is unavoidable, a “good” rate would be anything significantly below the national average, which often hovers around 20-25% APR. Cards with introductory 0% APR periods can be “good” for temporary borrowing, provided you pay off the balance before the promotional period ends. Any rate below 15% for a standard credit card is extremely rare and generally indicative of specific promotional offers or highly specialized cards.

How Your Credit Score Impacts Your Rate

The single most influential factor in determining the interest rate you’re offered across nearly all loan types is your credit score. A strong credit score is your golden ticket to lower borrowing costs, while a poor one can significantly inflate them.

The Role of Credit Scores (FICO/VantageScore)

Credit scores, like FICO Score and VantageScore, are three-digit numbers that summarize your creditworthiness based on your credit history. They are essentially a predictive measure of how likely you are to repay your debts. Lenders use these scores to quickly assess risk:

- Excellent (800-850 FICO): You’re considered a prime borrower, eligible for the very best rates and terms.

- Very Good (740-799 FICO): Highly desirable borrower, excellent rates still within reach.

- Good (670-739 FICO): A solid borrower, will qualify for competitive rates, though not always the absolute lowest.

- Fair (580-669 FICO): Subprime borrower, will likely face higher interest rates and fewer loan options.

- Poor (300-579 FICO): High-risk borrower, will have difficulty securing loans and will be charged very high interest rates if approved.

Each point on your credit score can translate into tangible savings. For a mortgage, a difference of just 20-30 points can impact your interest rate by a quarter-percent, leading to thousands of dollars in savings over the loan’s lifetime.

Strategies to Improve Your Credit Score

If your credit score isn’t where you want it to be, there are concrete steps you can take to improve it and qualify for better rates in the future:

- Pay Your Bills on Time, Every Time: Payment history is the most significant factor (35% of FICO score). Late payments severely damage your score. Set up autopay or reminders.

- Keep Credit Utilization Low: This refers to the amount of credit you’re using compared to your total available credit (30% of FICO score). Aim to keep your utilization below 30% across all accounts, ideally even lower (under 10%).

- Maintain a Long Credit History: The length of your credit history (15% of FICO score) shows stability. Avoid closing old, unused credit accounts, as this can shorten your average account age.

- Diversify Your Credit Mix: Having a mix of different types of credit (e.g., credit cards, installment loans like mortgages or auto loans) can be beneficial (10% of FICO score), demonstrating you can responsibly manage various credit products.

- Limit New Credit Applications: Each hard inquiry (when a lender checks your credit for a loan application) can temporarily ding your score. Only apply for credit when genuinely needed.

Strategies for Securing a Better Interest Rate

Even with a strong credit score, proactive strategies can further enhance your chances of locking in the most favorable interest rate possible.

Shop Around and Compare Lenders

This is perhaps the most fundamental and effective strategy. Don’t simply accept the first offer you receive. Different lenders—banks, credit unions, online lenders, and even peer-to-peer lending platforms—have varying risk appetites, overhead costs, and target markets. Consequently, they offer different rates. Get quotes from at least three to five different sources. Utilize online comparison tools, but always verify directly with the lender for personalized rates. For major loans like mortgages, pre-approval letters from multiple lenders can be invaluable negotiation tools.

Negotiate with Lenders

While not always possible, particularly for standardized products like credit cards, negotiation can be effective for larger loans like mortgages, auto loans, or personal loans. If you have an excellent credit score and multiple offers, you can leverage one lender’s offer to get a better deal from another. Be polite but firm in asking if there’s any flexibility in the rate or fees. Sometimes, even a small reduction can save you a significant amount over the loan’s life.

Consider a Co-signer

If your credit score is fair or poor, or if you have limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially agrees to be responsible for the debt if you default, reducing the lender’s risk. However, this is a serious commitment for the co-signer, as the loan will appear on their credit report and impact their own borrowing capacity.

Make a Larger Down Payment

For secured loans like mortgages and auto loans, making a larger down payment reduces the amount you need to borrow and, more importantly, reduces the lender’s risk. A lower loan-to-value (LTV) ratio often translates into a more attractive interest rate. For mortgages, a down payment of 20% or more can also help you avoid private mortgage insurance (PMI), which adds to your monthly cost.

Shorten Your Loan Term

Opting for a shorter loan term (e.g., a 15-year mortgage instead of 30, or a 3-year auto loan instead of 5) generally results in a lower interest rate. Lenders perceive less risk over a shorter period. While this will lead to higher monthly payments, you’ll pay significantly less interest over the life of the loan. Ensure your budget can comfortably accommodate the higher payments before committing to a shorter term.

Understand and Avoid Hidden Fees

Always scrutinize the loan agreement for any hidden fees, such as origination fees, application fees, or prepayment penalties. These fees can inflate the true cost of the loan, even if the nominal interest rate appears low. Focus on the APR, which incorporates most of these costs, to get a clearer picture of the loan’s overall expense.

When is a Higher Rate Acceptable? (The Trade-Offs)

While the pursuit of the lowest possible interest rate is often a sound financial strategy, there are specific circumstances where a slightly higher rate might be acceptable, or even necessary. Financial decisions are rarely black and white, and sometimes trade-offs are warranted.

Emergency Needs

In an absolute emergency, access to funds quickly might take precedence over securing the absolute lowest interest rate. If you need money urgently for a critical medical expense, car repair that prevents you from working, or an unexpected home repair, a personal loan with a slightly higher rate might be a better option than, say, a payday loan or going without the necessary funds. The cost of inaction or the higher cost of alternative borrowing (like high-interest credit cards) could outweigh the premium paid for a slightly higher but still reasonable personal loan rate.

Building Credit

For individuals with thin credit files or those actively working to rebuild their credit, securing a loan—even with a higher-than-average interest rate—can be a strategic move. A responsible repayment history on a personal loan or a secured credit card can significantly improve your credit score over time. This improved score then unlocks access to much lower rates on future, larger loans like mortgages or auto loans. In this scenario, the higher interest is an investment in your financial future, paving the way for substantial long-term savings.

Long-Term Financial Goals

Sometimes, taking on a loan with a moderate interest rate can free up capital for other investments that promise a higher return. For example, if you can secure a personal loan at 8% APR, but you have a high-yield investment opportunity that consistently returns 12% or more, using the loan to fund that investment could be a smart financial play (assuming you’ve thoroughly assessed the risks of the investment). This is a more advanced strategy and requires a clear understanding of risk tolerance and investment returns, but it illustrates that a “good” rate isn’t always about the absolute lowest number, but rather its role within your broader financial ecosystem.

Conclusion

Ultimately, defining “what is a good loan interest rate” is a highly personalized endeavor. It hinges on your unique financial profile, the specific type of loan you need, and the prevailing economic winds. A truly “good” rate is one that is competitive within the current market for your credit tier and loan type, and one that you can comfortably afford to repay without straining your financial health.

To secure the best possible rates, focus on maintaining a stellar credit score, diligently comparing offers from multiple lenders, and understanding all the terms and conditions, especially the APR. While the allure of the lowest rate is strong, also consider the trade-offs, such as a shorter loan term for lower overall interest paid, or the strategic use of a loan to address emergencies or build credit. By approaching borrowing with knowledge, diligence, and a clear understanding of your financial landscape, you can navigate the loan market effectively and make choices that contribute positively to your long-term financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.