For many, purchasing a home represents the most significant financial decision of their lives. It’s not just about finding the right property; it’s equally, if not more, about securing the right financing. A mortgage, essentially a loan used to buy real estate, will likely be a commitment spanning decades, influencing your monthly budget, long-term financial health, and overall wealth accumulation. Approaching this process without due diligence is akin to walking into a high-stakes negotiation unprepared. Smart mortgage shopping can save you tens of thousands of dollars over the life of the loan, making it imperative to understand the landscape, prepare thoroughly, strategize your search, and navigate the closing process with confidence. This guide will demystify the journey, empowering you to secure a mortgage that aligns perfectly with your financial goals.

Understanding the Mortgage Landscape

Before you even begin to compare offers, it’s crucial to grasp the fundamental types of mortgages available and the terminology used by lenders. This foundational knowledge will equip you to make informed decisions and ask pertinent questions throughout your shopping process.

Types of Mortgages

The mortgage market offers a variety of products, each designed to suit different financial situations and risk tolerances. Understanding these distinctions is your first step.

- Fixed-Rate Mortgages (FRMs): As the name suggests, the interest rate on an FRM remains constant for the entire life of the loan, typically 15, 20, or 30 years. This offers predictable monthly principal and interest payments, providing stability and protection against rising interest rates. This predictability is ideal for those who value consistent budgeting and plan to stay in their home for the long term.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an interest rate that is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a chosen market index. The initial fixed rate is often lower than that of a comparable FRM, making ARMs attractive for borrowers who anticipate selling or refinancing before the fixed period ends, or those who expect their income to rise significantly. However, they carry the risk of higher payments if rates increase after the adjustment period.

- FHA Loans: Insured by the Federal Housing Administration (FHA), these loans are popular among first-time homebuyers and those with less-than-perfect credit. FHA loans typically require a lower minimum down payment (as low as 3.5%) and more flexible credit requirements than conventional loans. However, they mandate mortgage insurance premiums (MIP) for the life of the loan in many cases, which adds to the monthly cost.

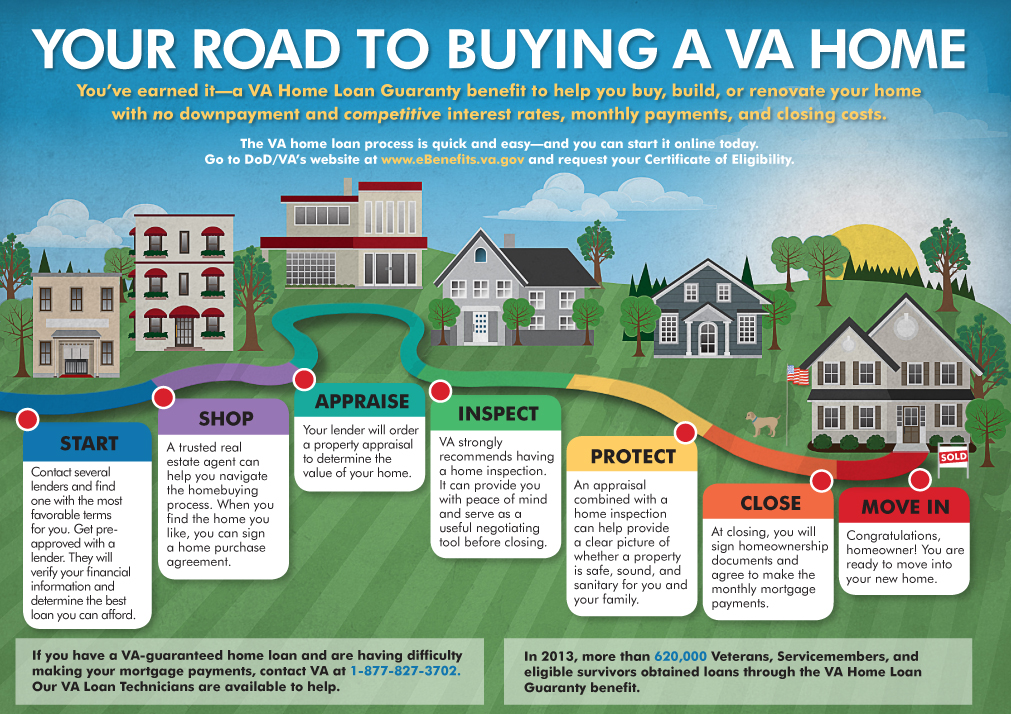

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs (VA), these loans are an invaluable benefit for eligible service members, veterans, and surviving spouses. VA loans often require no down payment, offer competitive interest rates, and do not require private mortgage insurance (PMI). They do, however, involve a funding fee, which can be financed into the loan.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans aim to help low-to-moderate-income individuals purchase homes in eligible rural and suburban areas. USDA loans often require no down payment and offer favorable terms, making them an excellent option for qualifying borrowers in designated regions.

Key Mortgage Terms to Know

Navigating mortgage discussions requires familiarity with a specific lexicon. These terms are fundamental to understanding your loan agreement and comparing offers.

- Interest Rate: This is the cost of borrowing the principal amount, expressed as a percentage. A lower interest rate translates to lower monthly payments and less money paid over the life of the loan.

- APR (Annual Percentage Rate): While the interest rate reflects the cost of borrowing the principal, the APR provides a broader measure of the total cost of the loan. It includes the interest rate plus certain upfront fees and charges, such as origination fees, discount points, and some closing costs. Comparing APRs across different lenders can give you a more accurate picture of the true cost of each loan.

- Down Payment: This is the portion of the home’s purchase price that you pay upfront in cash. A larger down payment can reduce your loan amount, lower your monthly payments, decrease interest paid over time, and potentially eliminate the need for private mortgage insurance (PMI).

- Closing Costs: These are fees charged by lenders and third parties for processing the loan and closing the transaction. They typically range from 2% to 5% of the loan amount and can include origination fees, appraisal fees, title insurance, recording fees, and attorney fees.

- Escrow: An escrow account is often set up by your lender to collect and hold funds for property taxes and homeowners insurance premiums. A portion of your monthly mortgage payment is deposited into this account, and the lender pays these bills on your behalf when they are due. This ensures these important payments are made on time, protecting the lender’s collateral.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI as a key indicator of your ability to manage monthly payments and repay debt. A lower DTI ratio (typically below 43%) generally signals to lenders that you are a less risky borrower.

Preparing for the Mortgage Application Process

Before you even speak to a lender, investing time in preparing your financial profile will significantly strengthen your position and streamline the application process. Lenders assess risk, and a well-organized, financially stable applicant is always more attractive.

Assessing Your Financial Health

A thorough review of your finances is the bedrock of a successful mortgage application. This involves more than just knowing your bank balance.

- Credit Score: Your credit score is a numerical representation of your creditworthiness and is a primary factor lenders use to determine your eligibility and interest rate. A higher score (generally 740 and above) can qualify you for the best rates. Obtain copies of your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) well in advance, review them for errors, and dispute any inaccuracies. Pay down high-interest debt, avoid opening new credit lines, and make all payments on time to boost your score.

- Income and Employment Stability: Lenders want assurance that you have a stable and reliable income stream to make your monthly mortgage payments. They will typically look for at least two years of consistent employment in the same field or with the same employer. Be prepared to provide pay stubs, W-2s, and tax returns to verify your income. For self-employed individuals, this often means providing two or more years of detailed tax returns and profit-and-loss statements.

- Savings for Down Payment and Closing Costs: Having sufficient funds for your down payment is critical. While some loans offer low or no down payment options, a larger down payment generally results in a lower interest rate, smaller monthly payments, and potentially avoids private mortgage insurance (PMI). Additionally, you’ll need funds for closing costs, which can range from 2% to 5% of the loan amount. Start saving early and keep these funds in an easily accessible account.

- Debt Management: Lenders scrutinize your existing debt-to-income (DTI) ratio. High credit card balances, car loans, student loans, and other forms of debt can limit your borrowing capacity or lead to a higher interest rate. Prioritize paying down consumer debt, especially those with high interest rates, before applying for a mortgage. This will improve your DTI and make you a more attractive borrower.

Gathering Necessary Documentation

Once your finances are in order, gather all the essential documents you’ll need for the application. Having these ready will prevent delays and demonstrate your preparedness to potential lenders.

- Proof of Income: This typically includes your last two years of W-2 forms, your most recent two to three pay stubs, and potentially the last two years of federal tax returns if you have self-employment income or complex tax situations.

- Bank and Asset Statements: Provide statements from all checking, savings, retirement (401k, IRA), and investment accounts for the past two to three months. These demonstrate your available funds for the down payment and closing costs, as well as your ability to maintain reserves.

- Identification: A valid government-issued photo ID (like a driver’s license or passport) and your Social Security card are standard requirements.

- Rental History (if applicable): If you’ve been renting, some lenders may ask for proof of timely rent payments, typically in the form of cancelled checks or a letter from your landlord.

- Other Financial Documents: Depending on your situation, you might need divorce decrees, bankruptcy discharge papers, or gift letters if a portion of your down payment is coming from a relative.

The Strategic Art of Mortgage Shopping

Once your financial house is in order, the real shopping begins. This phase is critical for comparing options, understanding the nuances of different offers, and ultimately securing the best possible terms for your specific situation.

Get Pre-Approved, Not Just Pre-Qualified

Understanding the difference between pre-qualification and pre-approval is vital, and only one truly matters in a competitive housing market.

- Pre-qualification is an informal estimate of how much you might be able to borrow. It’s based on a brief review of your stated income and debts and does not involve a deep dive into your credit report or verification of your financial documents. It’s useful for getting a rough idea of your budget.

- Pre-approval, on the other hand, is a conditional commitment from a lender to loan you a specific amount of money, up to a certain price range, at an estimated interest rate. It involves a thorough review of your credit history, income, assets, and employment. The lender verifies your financial information and performs a hard credit inquiry. A pre-approval letter demonstrates to sellers that you are a serious and qualified buyer, giving you a significant advantage in negotiations. Aim to get pre-approved before you start seriously looking at homes.

Comparing Lenders and Offers

Never settle for the first offer you receive. Diligent comparison shopping is where you can realize significant savings.

- Shop Around Broadly: Engage with multiple types of lenders. This includes traditional banks (large national banks and smaller regional ones), credit unions (often known for competitive rates and personalized service), mortgage brokers (who work with various lenders to find you the best deal), and online lenders (which can offer convenience and competitive rates due to lower overhead). Each has pros and cons, and exploring multiple avenues increases your chances of finding the ideal fit.

- Focus Beyond the Interest Rate: While the interest rate is a critical factor, it’s not the only component of your loan’s cost. Pay close attention to the APR, which provides a more holistic view of the loan’s total cost, including fees. Also, consider origination fees, discount points, appraisal fees, and other closing costs. A slightly higher interest rate with significantly lower fees might result in a better overall deal. Don’t overlook customer service and lender responsiveness – a smooth process can be just as valuable as a few basis points on the interest rate.

- Utilizing Loan Estimates: Once you apply for a loan, lenders are legally required to provide you with a Loan Estimate within three business days. This standardized form details the loan terms, projected payments, and estimated closing costs. This is your most powerful tool for comparison. Get Loan Estimates from at least three to five different lenders. Carefully compare Section A (Origination Charges), Section B (Services You Cannot Shop For), and Section C (Services You Can Shop For) across all estimates. Look for discrepancies, negotiate fees, and understand exactly what you’re paying for.

Negotiating Your Mortgage Terms

Even after receiving multiple Loan Estimates, there’s often room for negotiation. Lenders are competing for your business.

- Leverage Competing Offers: Use the best Loan Estimate you’ve received from one lender to negotiate with another. Tell your preferred lender about a better offer you’ve received and ask if they can match or beat it. Be specific about the interest rate, APR, and any particular fees.

- Ask for Fee Reductions or Credits: Some fees, especially origination fees or processing fees, may be negotiable. Don’t hesitate to ask your lender to waive or reduce certain costs or provide a lender credit to offset a portion of your closing costs in exchange for a slightly higher interest rate.

- Locking In Your Interest Rate: Once you find a rate you’re happy with, ask your lender about locking it in. An interest rate lock guarantees the specified interest rate for a set period (typically 30 to 60 days) while your loan is being processed. This protects you if market rates rise before your closing date. Understand the terms of the lock, including its duration and any potential fees for extending it.

Navigating the Closing Process and Beyond

Securing pre-approval and comparing offers are significant milestones, but the journey isn’t over. The underwriting and closing phases require continued attention, and your responsibilities extend long after you get the keys.

The Underwriting Stage

After you submit a full application, your loan moves into underwriting. This is where the lender thoroughly verifies all the information you’ve provided.

- What it Entails: Underwriters will meticulously review your credit history, income, assets, and employment stability. They will also assess the property itself through an appraisal to ensure its value supports the loan amount. They are looking for any inconsistencies or red flags that might indicate a higher risk.

- Be Responsive to Requests: The underwriter may ask for additional documentation or clarification on certain items. Respond promptly and completely to avoid delays. Any new debts, large purchases, or significant changes in employment during this period can jeopardize your loan approval, so maintain your financial stability.

Final Walk-Through and Closing Day

The culmination of your mortgage shopping journey is the closing table, but there are vital steps right before you sign on the dotted line.

- Reviewing the Closing Disclosure: By law, you must receive a Closing Disclosure (CD) at least three business days before your scheduled closing. This document is the final version of your Loan Estimate, detailing all the final loan terms, projected payments, and closing costs. Compare it meticulously with your last Loan Estimate. Look for any significant changes to the interest rate, loan terms, or fees. If you find discrepancies, ask your lender for an explanation and resolution before closing.

- Final Walk-Through: Conduct a final walk-through of the property the day before or the morning of closing. Ensure all agreed-upon repairs have been made, and that the property is in the condition you expect.

- What to Expect at the Closing Table: Closing is typically held at a title company or attorney’s office. You will sign numerous documents, including the promissory note (your promise to repay the loan), the mortgage or deed of trust (the lien on the property), and various disclosures. Be prepared to bring certified funds for your down payment and closing costs. Don’t be afraid to ask questions about any document you don’t fully understand before signing.

Post-Closing Responsibilities

Getting the keys is the end of the buying process, but the beginning of your responsibilities as a homeowner and mortgage holder.

- Making Timely Payments: Your primary responsibility is to make your monthly mortgage payments on time, every time. Missing payments can severely damage your credit score and potentially lead to foreclosure. Set up automatic payments to ensure consistency.

- Understanding Escrow Accounts and Property Taxes: If you have an escrow account, a portion of your monthly payment goes towards property taxes and homeowners insurance. Your lender will manage these payments. However, it’s wise to periodically review your escrow statements to ensure accuracy and understand any adjustments. Property values and tax rates can change, potentially impacting your monthly escrow payment.

- Refinancing Considerations Down the Road: Over the years, interest rates may fluctuate, or your financial situation might change. Keep an eye on market conditions. If interest rates drop significantly or if you wish to change your loan term, refinancing your mortgage might be a viable option to lower your payments or save money over the long term.

Shopping for a mortgage is a comprehensive financial undertaking that demands careful attention to detail, diligent research, and strategic comparison. By understanding the types of loans available, preparing your financial profile, comparing offers meticulously, and navigating the closing process with awareness, you can secure a mortgage that not only fits your budget but also supports your long-term financial prosperity. This isn’t just about getting a loan; it’s about making one of the smartest financial decisions of your life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.