In the intricate world of personal finance and investment, few factors hold as much sway over our economic well-being as “today’s rates.” These seemingly simple numbers – whether referring to interest rates, exchange rates, or investment returns – are the lifeblood of economic activity, influencing everything from the cost of our daily coffee to the long-term viability of our retirement plans. For the savvy individual, understanding and actively tracking these rates isn’t just a matter of curiosity; it’s a fundamental pillar of informed financial decision-making.

The financial landscape is dynamic, shaped by a confluence of global economic trends, central bank policies, geopolitical events, and market sentiment. What constitutes “today’s rates” is a constantly evolving picture, demanding regular attention to ensure one’s financial strategies remain optimized and resilient. This article delves into the various facets of financial rates that impact our lives, offering insights into their mechanisms, implications, and how to effectively leverage this critical information.

The Ever-Shifting Landscape of Interest Rates

Interest rates are arguably the most pervasive and impactful category of “rates” in our daily financial lives. They dictate the cost of borrowing and the return on savings, serving as a primary tool for central banks to manage economic growth and inflation. Understanding their movement is crucial for both consumers and investors.

Central Bank Policies and Their Ripple Effect

At the core of the interest rate ecosystem are the central banks, such as the Federal Reserve in the United States, the European Central Bank, or the Bank of England. Their primary policy rate – the Federal Funds Rate in the U.S., for instance – is the benchmark that influences all other interest rates in the economy. When a central bank raises its policy rate, it typically aims to cool down an overheating economy and curb inflation. Conversely, rate cuts are often implemented to stimulate economic activity during downturns.

The ripple effect is immediate and widespread. Banks borrow from each other and the central bank at rates influenced by this benchmark, which then translates into the rates they offer to their customers. A hike in the Federal Funds Rate, for example, signals to commercial banks that their cost of borrowing has increased, prompting them to raise their prime lending rates, which in turn affects a vast array of consumer and business loans. This interconnectedness means that a single announcement from a central bank can send tremors through global markets and impact the monthly budgets of millions.

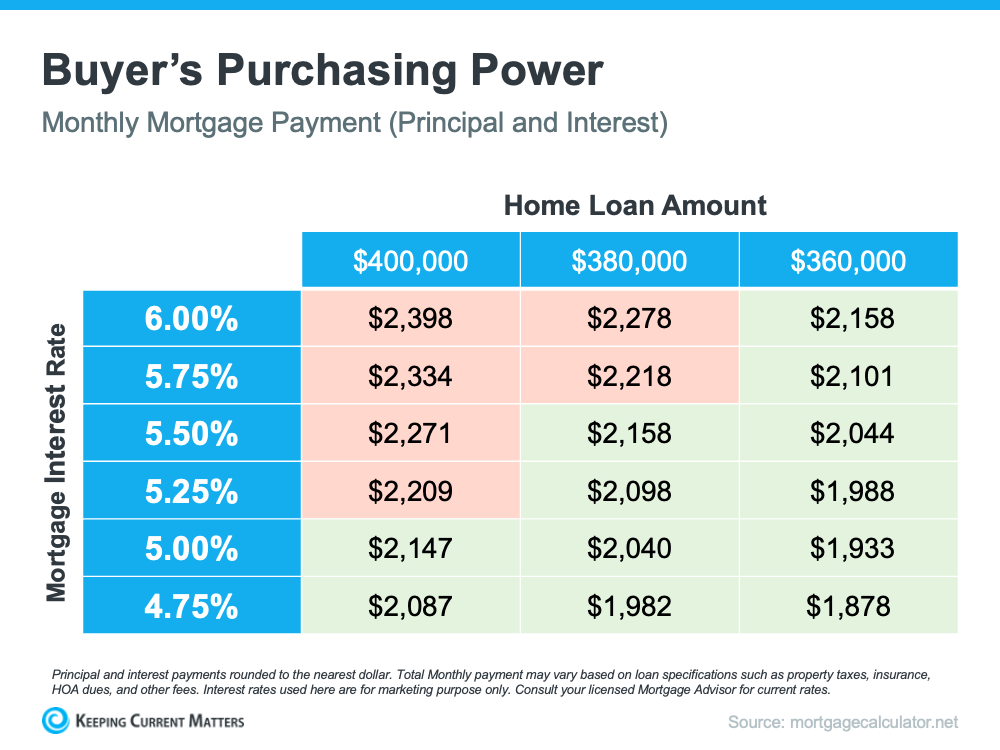

Mortgage Rates: The Cost of Homeownership

For many, mortgage rates represent the single largest financial commitment and cost. These rates determine the monthly payments for one of life’s most significant assets – a home. Mortgage rates are not directly set by central bank policy rates but are heavily influenced by them, along with bond market yields (specifically the 10-year Treasury bond in the U.S.), inflation expectations, and economic forecasts.

When interest rates are low, borrowing for a home becomes more affordable, spurring housing market activity. Conversely, rising rates can cool down a hot housing market by making homeownership more expensive. Tracking “today’s mortgage rates” is essential for prospective homebuyers, those considering refinancing, and even current homeowners who might be looking to assess their equity or future housing plans. Factors like credit score, down payment size, and loan term (e.g., 15-year vs. 30-year fixed) also play a significant role in the specific rate an individual qualifies for. Small percentage point differences can translate into tens of thousands of dollars over the life of a loan, underscoring the importance of vigilance and comparison shopping.

Savings and Loan Rates: Your Money’s Growth and Borrowing Costs

Beyond mortgages, interest rates dictate the return on your savings and the cost of various other forms of credit.

- Savings Accounts and Certificates of Deposit (CDs): These rates determine how much interest your deposited money earns. In a rising rate environment, savings rates typically increase, offering a better return on your idle cash. CDs, which lock in a rate for a specific term, can be particularly attractive when rates are expected to decline.

- Personal Loans and Auto Loans: Similar to mortgages, these rates are influenced by the broader interest rate environment and the borrower’s creditworthiness. Lower rates mean cheaper borrowing, which can make financing a car or consolidating debt more manageable.

- Credit Card APRs: Annual Percentage Rates (APRs) on credit cards are often variable and tied to a benchmark rate, such as the prime rate. When the prime rate rises, so too do credit card APRs, making carrying a balance significantly more expensive. Monitoring these rates is crucial for managing consumer debt effectively and avoiding spiraling interest payments.

Unpacking Exchange Rates: Global Commerce and Travel

For anyone engaged in international trade, travel, or investment, exchange rates are a daily consideration. An exchange rate defines how much one currency is worth in terms of another, constantly fluctuating based on a multitude of economic and political factors.

Understanding Currency Volatility

Currency markets are among the most liquid and volatile in the world. The value of a currency against another is influenced by interest rate differentials between countries (higher rates can attract foreign investment, increasing demand for that currency), economic performance (strong growth often strengthens a currency), political stability, trade balances, and even speculative trading. These factors create a dynamic environment where exchange rates can shift significantly within hours, let alone days.

For instance, a country with robust economic growth and higher interest rates might see its currency appreciate as investors seek better returns, while political instability can cause a currency to depreciate rapidly. Central banks also intervene in currency markets to stabilize their economies, further adding to the complexity.

Impact on International Trade and Personal Travel

The implications of exchange rates are profound:

- International Trade: For businesses, favorable exchange rates can make exports more competitive or imports cheaper. A strong domestic currency makes imports less expensive but exports more costly for foreign buyers, potentially impacting a country’s trade balance. Businesses engaged in international transactions must constantly monitor exchange rates to manage costs and revenues effectively. Hedging strategies are often employed to mitigate the risks associated with currency fluctuations.

- Personal Travel: For individuals planning an international trip, knowing “today’s exchange rates” is essential for budgeting. A stronger domestic currency means your money will go further abroad, allowing for more spending on accommodation, food, and activities. Conversely, a weaker currency means your travel budget will stretch less. Travelers often use currency converters and track rates to determine the optimal time to exchange money or make purchases in foreign currencies.

- International Investing: Investors holding foreign stocks or bonds are also exposed to exchange rate risk. A gain in a foreign asset can be offset or even turned into a loss if the foreign currency depreciates against the investor’s home currency.

Investment Rates and Market Performance

Beyond traditional interest rates, the world of investing presents its own set of “rates” that inform decisions about wealth creation and preservation. These rates reflect the expected or actual returns on various investment vehicles.

Bond Yields: A Glimpse into Fixed-Income Returns

Bonds are essentially loans made to governments or corporations, and their “rate” is referred to as a yield. Bond yields are inversely related to bond prices: as interest rates rise, existing bond prices typically fall, and their yields (return relative to price) increase to remain competitive. The yield curve, which plots the yields of bonds with different maturities, is a key economic indicator, often signaling market expectations about future interest rates and economic growth.

- Treasury Yields: Government bond yields, particularly the 10-year Treasury yield in the U.S., are closely watched as benchmarks for long-term interest rates and as indicators of economic sentiment. They influence mortgage rates and the cost of corporate borrowing.

- Corporate Bond Yields: These offer investors a return for lending money to companies, with yields varying based on the company’s creditworthiness. Higher yields typically compensate for higher risk.

- Municipal Bond Yields: Issued by state and local governments, these often offer tax-exempt interest, making their effective yield attractive to high-income earners.

Understanding bond yields is critical for fixed-income investors seeking stable returns and for anyone assessing the broader interest rate environment.

Equity Markets: Daily Pulse of Corporate Value

While stocks don’t have a fixed “rate” in the same way bonds do, their performance is measured by rates of return – capital appreciation and dividends. “Today’s rates” in the equity market refer to the daily performance of stock indices (e.g., S&P 500, Dow Jones Industrial Average, NASDAQ) and individual stocks, expressed as percentage changes.

- Market Indices: These aggregate rates of return provide a snapshot of overall market sentiment and economic health. A positive “rate” on the indices signifies growth, while a negative one indicates a downturn.

- Dividend Yields: For income-focused investors, the dividend yield (annual dividend payment divided by the stock price) is a crucial “rate” to track. It represents the return on investment through profit distribution rather than capital gains.

- Earnings Growth Rates: While not a market rate, the rate of earnings growth for companies is a fundamental driver of stock prices and long-term investment returns.

Staying abreast of equity market rates helps investors assess the value of their portfolios, identify investment opportunities, and understand the general direction of corporate profitability and economic confidence.

Other Investment Vehicles: CDs, Money Market Accounts

For those seeking lower-risk, more liquid options, Certificates of Deposit (CDs) and Money Market Accounts offer fixed or variable interest rates. “Today’s rates” for these products reflect the current short-term interest rate environment and are often influenced by central bank policy. They are critical for managing short-term cash flows and conservative savings goals.

Beyond the Obvious: Inflation and Other Crucial Metrics

While interest, exchange, and investment rates are prominent, other critical “rates” silently impact our financial well-being, demanding attention for a holistic financial perspective.

The Erosion of Purchasing Power: Inflation

The inflation rate measures the pace at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. A 3% inflation rate means that what cost $100 last year now costs $103. This rate is arguably one of the most important metrics, as it directly impacts the real return on savings and investments and the actual cost of living.

Central banks target specific inflation rates to maintain economic stability. When inflation is high, the real return on savings accounts with low interest rates can become negative, meaning your money is losing purchasing power. Understanding “today’s inflation rate” is vital for long-term financial planning, ensuring that investment returns outpace inflation to grow real wealth.

Credit Card APRs and Personal Loan Rates

As briefly touched upon, the Annual Percentage Rate (APR) on credit cards and personal loans is a daily rate that directly impacts consumer debt. These rates are often variable and can change with the prime rate, leading to fluctuations in the cost of borrowing. A high APR can make it incredibly difficult to pay down debt, as a significant portion of monthly payments goes towards interest. Monitoring these rates allows individuals to make informed decisions about debt consolidation, balance transfers, or accelerating repayment to minimize interest charges.

Staying Informed and Making Rate-Savvy Decisions

In a world where financial rates are in constant flux, the ability to access real-time information and interpret its implications is invaluable. Proactive monitoring empowers individuals to make strategic adjustments to their financial plans, optimize returns, and mitigate risks.

Essential Resources for Real-Time Data

Fortunately, a wealth of resources exists to help you track “today’s rates”:

- Financial News Outlets: Reputable financial media (e.g., The Wall Street Journal, Bloomberg, Reuters) provide daily updates, analysis, and forecasts on all types of rates.

- Central Bank Websites: The Federal Reserve, ECB, BoE, etc., publish their policy rate decisions and economic outlooks.

- Online Aggregators and Comparison Sites: For specific rates like mortgages, savings accounts, or CDs, websites specialize in comparing offers from multiple lenders and institutions.

- Investment Platforms: Brokerage accounts and investment apps often provide real-time market data, including bond yields and stock performance.

- Government Statistics Agencies: Bodies like the Bureau of Labor Statistics (BLS) provide official inflation figures.

By regularly consulting these sources, individuals can gain a comprehensive understanding of the current financial environment and anticipate future rate movements.

Leveraging Rate Information for Personal Finance Goals

Armed with knowledge of “today’s rates,” you can make smarter financial decisions:

- Savings and Investments: During periods of rising interest rates, consider moving cash from low-yield checking accounts into high-yield savings accounts or short-term CDs to maximize returns. When bond yields are attractive, consider fixed-income investments.

- Borrowing: If you anticipate rates to rise, consider locking in a fixed-rate mortgage or consolidating variable-rate debt. Conversely, if rates are falling, it might be an opportune time to refinance existing loans. Always shop around for the best rates on loans and credit cards, as even small differences can save you significant money over time.

- Budgeting and Debt Management: Factor in current and projected interest rates when planning your budget, especially if you carry credit card debt or have variable-rate loans. Prioritize paying down high-interest debt, particularly when rates are high.

- International Planning: For travelers or those sending money abroad, monitor exchange rates to find the most favorable time to convert currency. For businesses, active monitoring can inform hedging strategies and pricing decisions.

In conclusion, “today’s rates” are far more than mere numbers; they are powerful indicators that reflect the health and direction of the economy, shaping our financial realities. By embracing a proactive approach to understanding and monitoring these rates – from the minutiae of a savings account yield to the macro-trends of inflation – individuals can position themselves to navigate the financial landscape with greater confidence, make informed choices, and ultimately achieve their long-term money goals. Financial literacy, in this context, is not just about knowing the numbers, but understanding the story they tell and how to write your own successful financial narrative within it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.