Purchasing a car is a significant financial decision for most individuals and families. Beyond the excitement of choosing a make and model, understanding the financial mechanics of a car loan is paramount to making an informed and responsible investment. A car loan isn’t just a monthly payment; it’s a complex financial product influenced by several variables that collectively determine its true cost over time. Properly computing a car loan empowers you to compare offers, negotiate effectively, and ensure your new vehicle fits comfortably within your budget without compromising other financial goals.

This guide will demystify the process of computing a car loan. We’ll delve into the core components that shape your loan, explore both manual calculation methods and the power of digital tools, and look beyond the monthly payment to understand the total cost implications. By the end, you’ll possess the knowledge and confidence to approach car financing with clarity, ensuring you secure a deal that’s not only affordable but also strategically sound.

Understanding the Fundamentals of a Car Loan

Before diving into computations, it’s crucial to grasp the foundational elements that constitute any car loan. These variables interact to dictate your monthly payments and the total amount you will ultimately pay back to the lender. A solid understanding of these terms is your first step towards financial literacy in vehicle acquisition.

Key Components of a Car Loan

Every car loan is built upon a few critical pillars:

- Principal Amount: This is the initial sum of money you borrow to purchase the car. It’s typically the car’s price minus any down payment, trade-in value, or rebates. A lower principal amount directly translates to lower monthly payments and less interest paid over the life of the loan.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage of the principal. It’s more than just the interest rate; it often includes other fees charged by the lender, giving a more complete picture of the loan’s annual cost. A lower APR significantly reduces the total amount you’ll pay. Factors like your credit score, the loan term, and market conditions heavily influence the APR you’re offered.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A shorter loan term means higher monthly payments but less interest paid overall, as you’re paying off the principal more quickly. Conversely, a longer loan term reduces monthly payments but increases the total interest paid because the principal remains outstanding for a longer period.

Fixed vs. Variable Interest Rates

While less common for standard car loans, it’s worth understanding the distinction:

- Fixed Interest Rate: The interest rate remains constant throughout the life of the loan. This provides predictability, as your monthly payment for the principal and interest component will not change. Most conventional car loans are fixed-rate.

- Variable Interest Rate: The interest rate can fluctuate over the loan term, usually tied to a benchmark interest rate (like the prime rate). This means your monthly payments could increase or decrease. While potentially offering lower initial payments, it introduces uncertainty and risk.

The Impact of Down Payment and Trade-in

Your down payment—the upfront cash you pay towards the car’s purchase price—and any trade-in value from your old vehicle directly reduce the principal amount you need to borrow. A larger down payment or a valuable trade-in not only lowers your monthly payments but also reduces the total interest you’ll pay over the loan’s duration, as the loan principal is smaller from the outset. This also helps reduce your loan-to-value ratio, potentially making you a less risky borrower in the eyes of lenders and leading to better interest rates.

Manual Calculation Methods for Your Car Loan

While digital tools have simplified the process, understanding the underlying mathematical formulas can provide deeper insights into how your car loan is structured. This knowledge is particularly useful for verifying figures or performing quick estimates.

Simple Interest Calculation: The Basics

Many people mistakenly believe car loan interest is calculated using simple interest on the initial principal over the entire loan term. While some short-term or specific types of loans might use this, most car loans use compound interest on the remaining principal balance.

However, understanding simple interest is a good starting point for grasping the concept of interest accrual. The basic formula for simple interest is:

Interest = Principal × Rate × Time

Where:

- Principal is the initial amount borrowed.

- Rate is the annual interest rate (expressed as a decimal, e.g., 5% is 0.05).

- Time is the loan term in years.

Example: If you borrow $20,000 at 5% simple interest for 5 years, the total simple interest would be $20,000 × 0.05 × 5 = $5,000. However, this doesn’t account for payments reducing the principal over time, which is how car loans actually work.

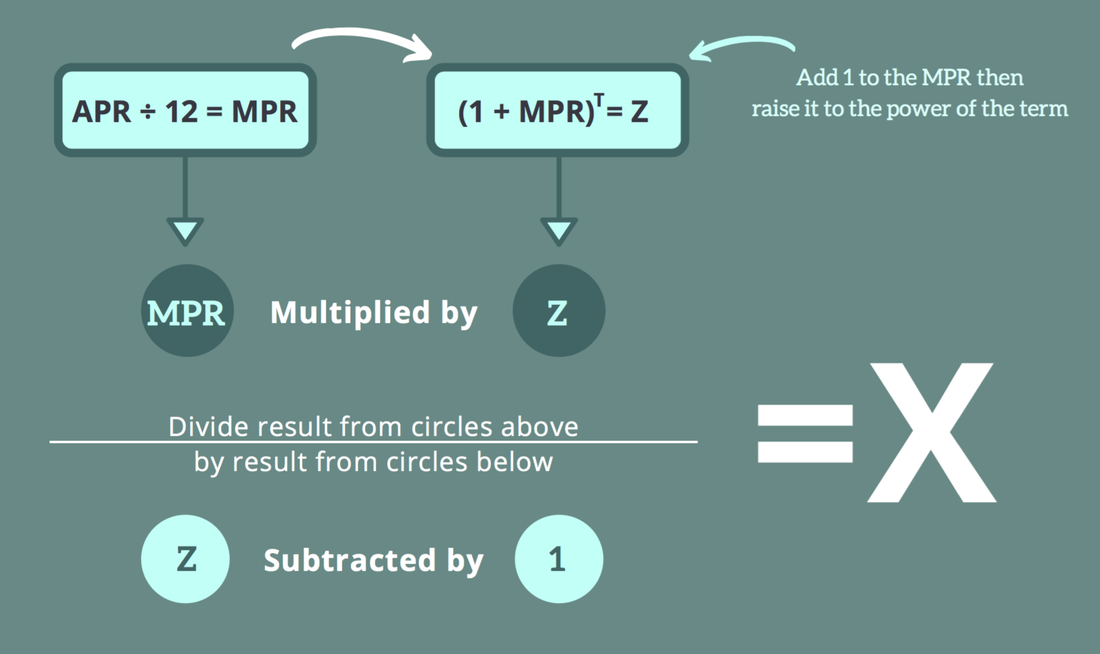

Amortization Formula: The Comprehensive Approach

The most accurate way to calculate car loan payments, which uses compound interest and an amortization schedule, involves a more complex formula. This formula determines the fixed monthly payment required to fully pay off the loan (principal and interest) over its term.

The monthly payment (P) formula is:

P = [L * c * (1 + c)^n] / [(1 + c)^n – 1]

Where:

- P = Monthly payment

- L = Loan principal amount (the amount you’re borrowing)

- c = Monthly interest rate (annual rate divided by 12, expressed as a decimal)

- n = Total number of payments (loan term in years multiplied by 12)

Let’s break it down with an example:

- Loan Amount (L): $25,000

- Annual Interest Rate: 6% (or 0.06 as a decimal)

- Loan Term: 5 years (60 months)

- Calculate Monthly Interest Rate (c): 0.06 / 12 = 0.005

- Calculate Total Number of Payments (n): 5 years * 12 months/year = 60

- Plug values into the formula:

P = [25000 * 0.005 * (1 + 0.005)^60] / [(1 + 0.005)^60 – 1]

P = [125 * (1.005)^60] / [(1.005)^60 – 1]

P = [125 * 1.34885] / [1.34885 – 1]

P = 168.60625 / 0.34885

P ≈ $483.33

So, your estimated monthly payment would be approximately $483.33.

Challenges of Manual Calculation

While understanding the amortization formula is enlightening, performing these calculations manually for every scenario (different loan amounts, rates, terms) is tedious and prone to errors. Furthermore, this formula typically doesn’t account for potential loan fees that might be rolled into the principal or charged separately, which can affect the true APR. This is where digital tools become invaluable.

Leveraging Digital Tools and Calculators

In today’s digital age, relying solely on manual calculations for complex financial products like car loans is inefficient. A plethora of digital tools can provide instant, accurate, and customizable computations, making the process much simpler and more insightful.

Online Car Loan Calculators: Ease and Accuracy

Online car loan calculators are perhaps the most accessible and user-friendly tools available. A quick search will reveal numerous options from financial institutions, automotive websites, and independent financial planning sites.

How they work: You simply input the principal loan amount, the interest rate (APR), and the loan term. With a click, the calculator instantly provides:

- Your estimated monthly payment.

- The total amount of interest you will pay over the loan term.

- The total cost of the loan (principal + interest).

Benefits:

- Speed: Get results in seconds.

- Accuracy: Most calculators use the precise amortization formula.

- Scenario Planning: Easily adjust variables (down payment, trade-in, loan term) to see how they impact your payments, allowing you to compare different financing options on the fly.

- Accessibility: Available 24/7 from any device with internet access.

Spreadsheet Applications: Customization and Scenario Planning

For those who prefer a more hands-on approach or need to build detailed financial models, spreadsheet applications like Microsoft Excel or Google Sheets are powerful tools. You can create your own amortization schedule, which breaks down each payment into its principal and interest components over the entire loan term.

Using Excel/Google Sheets for loan amortization schedules:

- Set up columns: You’ll typically need columns for: Payment Number, Starting Balance, Interest Paid, Principal Paid, and Ending Balance.

- Input loan details: Enter your loan principal, annual interest rate, and loan term in dedicated cells.

- Use financial functions: Excel/Sheets have built-in functions like

PMT(to calculate monthly payment),IPMT(to calculate interest payment for a specific period), andPPMT(to calculate principal payment for a specific period).=PMT(rate, nper, pv, [fv], [type])rate: Monthly interest rate (e.g.,B2/12where B2 is annual rate).nper: Total number of payments (e.g.,B3*12where B3 is loan term in years).pv: Present value or principal amount (e.g.,B1).

- Populate the schedule: Use these functions and simple arithmetic to fill out your amortization table. This allows you to see how your principal reduces with each payment and how the proportion of interest vs. principal paid changes over time.

Advantages: Full control, detailed breakdown, ability to integrate with other budget planning sheets, and complex scenario analysis (e.g., impact of extra payments).

Lender-Specific Calculators and Features

Many banks, credit unions, and automotive manufacturers offer their own proprietary loan calculators on their websites. These can sometimes incorporate specific promotional rates, fees, or financing programs unique to their offerings. It’s always a good idea to use these calculators when comparing offers from different lenders, as they may reflect additional terms or conditions that generic calculators cannot. Some may even allow pre-qualification checks without impacting your credit score.

Beyond the Monthly Payment: Total Cost and Financial Implications

Focusing solely on the monthly payment can be misleading. While a low monthly payment might seem attractive, it often comes at the cost of a longer loan term and significantly more interest paid over time. A holistic view requires understanding the total cost of the loan and its broader financial implications.

The True Cost of Your Car Loan

The true cost of your car loan extends beyond just the principal amount. It encompasses several factors:

- Total Interest Paid: This is often the most overlooked cost. Using our earlier example ($25,000 loan at 6% for 60 months with a monthly payment of $483.33), the total payments would be $483.33 * 60 = $28,999.80. Subtracting the principal, the total interest paid is $28,999.80 – $25,000 = $3,999.80. A seemingly small interest rate can still accumulate to a substantial sum over several years.

- Additional Fees: Car loans can come with various fees that may or may not be rolled into the principal. These can include:

- Origination Fees: Charged by the lender for processing the loan.

- Documentation Fees: Charged by the dealership for preparing paperwork.

- Registration and Licensing Fees: Government-mandated fees for owning and operating a vehicle.

- Prepayment Penalties: Though less common with car loans, some lenders might charge a fee if you pay off your loan early. Always check for this in the loan agreement.

These fees can add hundreds or even thousands of dollars to the overall cost, so always inquire about them.

Strategies to Reduce Total Loan Cost

Proactive strategies can significantly cut down the total amount you pay for your car:

- Larger Down Payment: As discussed, this reduces the principal, leading to less interest accrued.

- Shorter Loan Term: While increasing monthly payments, a shorter term drastically reduces the total interest paid because you pay off the principal faster.

- Improving Credit Score: A higher credit score signals lower risk to lenders, allowing you to qualify for lower interest rates (APR), which is the most impactful way to save on interest.

- Refinancing Options: If your credit score improves after taking out a loan, or if interest rates drop, refinancing your car loan for a better rate or shorter term can save you money. Be mindful of any refinancing fees.

Budgeting for Car Ownership (Insurance, Maintenance, Fuel)

The car loan payment is just one piece of the puzzle. A truly responsible financial plan for car ownership must include other recurring expenses:

- Car Insurance: Mandatory and often a significant monthly cost, varying based on vehicle type, driver history, and coverage.

- Fuel: A variable cost depending on mileage and gas prices.

- Maintenance and Repairs: Regular servicing, oil changes, tire rotations, and unexpected repairs are inevitable. It’s wise to budget a contingency fund for these.

- Registration and Inspection: Annual or biennial fees.

- Depreciation: While not a direct cash outlay, depreciation is the loss in value of your car over time, which impacts your asset’s worth.

Ignoring these costs can lead to financial strain, even if your loan payment seems affordable.

What to Consider Before Committing to a Car Loan

A well-computed loan is only part of the equation. Before signing on the dotted line, it’s essential to conduct a thorough evaluation of your personal finances and explore all available options. This due diligence ensures you secure the best possible terms and avoid future financial pitfalls.

Assessing Your Financial Health and Affordability

Before even looking at cars, honestly assess your current financial situation:

- Monthly Income vs. Expenses: Do you have a consistent surplus each month that can comfortably cover a new car payment and all associated ownership costs (insurance, fuel, maintenance)?

- Debt-to-Income Ratio: Lenders look at this. If your existing debt payments (mortgage, student loans, credit cards) consume a large portion of your income, taking on a new car loan might make you overleveraged.

- Emergency Fund: Do you have at least 3-6 months of living expenses saved? Don’t deplete your emergency fund for a down payment if it leaves you vulnerable to unexpected financial shocks.

Ensure the car loan payment, combined with all other car-related expenses, doesn’t exceed a comfortable percentage of your disposable income (e.g., no more than 10-15%).

The Importance of Your Credit Score

Your credit score is perhaps the single most influential factor in determining the interest rate you qualify for. Lenders use it to assess your creditworthiness.

- Higher Score = Lower Risk = Lower Interest Rate: A strong credit score (typically 700+) can unlock the most competitive APRs, saving you thousands over the life of the loan.

- Lower Score = Higher Risk = Higher Interest Rate: If your score is low, lenders perceive you as a higher risk, and you’ll likely be offered a higher interest rate or less favorable terms.

- Check Your Score Regularly: Before applying for a car loan, obtain your credit report and score from the major credit bureaus (Experian, Equifax, TransUnion). Correct any errors and take steps to improve your score if necessary.

Shopping Around for the Best Loan Terms

Never settle for the first loan offer you receive, especially from the dealership. While convenient, dealership financing isn’t always the most competitive.

- Pre-Approval from Multiple Lenders: Apply for pre-approval from banks, credit unions, and online lenders before visiting the dealership. This provides you with concrete offers based on your creditworthiness.

- Compare APRs, Not Just Monthly Payments: Focus on the Annual Percentage Rate (APR) to compare the true cost of borrowing across different lenders. A lower APR is almost always better.

- Negotiate: With pre-approvals in hand, you can negotiate with the dealership’s finance department. They may be able to beat outside offers to close the sale.

Understanding the Loan Agreement and Fine Print

Before signing, meticulously read and understand every clause in the loan agreement. Don’t be afraid to ask questions.

- Verify all figures: Ensure the loan amount, interest rate, term, and monthly payment match what you agreed upon.

- Look for hidden fees: Confirm there are no unexpected charges.

- Prepayment Penalties: Double-check if there are any penalties for paying off the loan early.

- GAP Insurance: The dealership might offer GAP (Guaranteed Asset Protection) insurance. Understand what it covers and if you truly need it (it covers the difference between what you owe on your car and its actual cash value if it’s totaled or stolen). You can often get it cheaper from your own auto insurer.

- Extended Warranties: Be wary of high-pressure sales for extended warranties. Evaluate if the cost and coverage are truly beneficial to you.

Computing a car loan is a fundamental step in responsible vehicle ownership. By understanding the core components, utilizing smart calculation tools, looking beyond just the monthly payment, and conducting thorough research, you can navigate the financing landscape with confidence. This approach ensures that your new car not only meets your transportation needs but also aligns perfectly with your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.