The American Bankers Association (ABA) routing number, often simply called a routing number, serves as a crucial identifier in the vast and intricate world of electronic funds transfers. For account holders at major financial institutions like Chase Bank, understanding this nine-digit code is fundamental to navigating various personal and business financial transactions. It acts as a digital address, ensuring that money transferred electronically finds its way to the correct bank and, subsequently, the correct account. Without this precise identifier, the seamless flow of modern finance would grind to a halt, leading to misdirected funds, delays, and significant financial frustration.

Deciphering the ABA Routing Number: A Core Financial Identifier

At its heart, the ABA routing number is a nine-digit code used to identify a specific financial institution in the United States. Its origins trace back to 1910 when the American Bankers Association introduced it to facilitate the sorting and delivery of paper checks. While checks remain a part of the financial landscape, the routing number’s role has evolved dramatically, becoming indispensable for the vast majority of electronic transactions that define contemporary banking. Each digit in the nine-digit sequence holds significance, collectively identifying the bank, its location, and the specific clearinghouse through which transactions will be processed. It is distinct from an individual’s account number, which identifies a specific account within a particular financial institution.

The Fundamental Role in Electronic Transactions

The primary function of an ABA routing number in today’s digital age is to direct electronic payments. When you send money to another person or institution, or when you receive funds, the routing number tells the sending bank exactly which receiving bank to route the funds to. This precision is paramount for a wide array of financial activities that individuals and businesses rely on daily. From the convenience of direct deposit paychecks to the necessity of paying utility bills online, the routing number ensures that funds are accurately and efficiently transferred. It underpins the entire ecosystem of automated financial exchanges, transforming what was once a laborious manual process into an instantaneous digital one. The absence or inaccuracy of this number can disrupt these critical financial flows, causing significant inconvenience and potential financial penalties.

Distinguishing Between ACH, Wire Transfers, and Check Routing

It’s a common misconception that a bank will only have one routing number. In reality, large national banks like Chase often utilize multiple routing numbers depending on the type of transaction and sometimes even the geographic location where the account was opened. This distinction is critical for financial accuracy.

ACH (Automated Clearing House) Transfers: These are common electronic funds transfers processed through the ACH network. They include direct deposits (paychecks, government benefits), automatic bill payments, and person-to-person transfers. ACH transactions are generally less expensive, but they also take longer to process, typically 1-3 business days. The routing number used for ACH transactions is designed to route funds efficiently through this specific network.

Wire Transfers: These are typically faster, irrevocable, and more expensive than ACH transfers. Wire transfers are often used for large sums of money, time-sensitive payments, or international transactions (though international wires usually involve SWIFT/BIC codes in addition to or instead of ABA numbers for the foreign bank). Due to their immediacy and finality, domestic wire transfers often use a specific routing number to ensure they are directed through the appropriate, expedited channels within the banking system.

Check Routing: The routing number printed on the bottom of a physical check is primarily for processing paper checks. While checks are less common than in previous decades, this number still facilitates their clearance. When a check is deposited, the routing number guides it to the correct financial institution for payment. Even when a physical check is converted into an electronic image (a process known as Check 21), this routing number remains crucial for the electronic processing of the funds. It’s important to note that the check routing number is often the most generally applicable routing number for ACH transactions, but it’s always best to verify with Chase directly for specific electronic transfer types.

Navigating Chase Bank’s Routing Numbers

Chase Bank, as one of the largest financial institutions in the United States, manages a vast network of accounts and transactions daily. Consequently, it employs several routing numbers to streamline its operations and ensure the accurate processing of diverse financial activities. Understanding which number applies to which situation is key to avoiding transaction failures and delays.

Geographic and Transactional Specificity

While some smaller, regional banks might have a single routing number, major national banks like Chase often have several. These variations are typically driven by two main factors:

- Geographic Location: Historically, banks assigned routing numbers based on the state or region where an account was opened. While less common for accounts opened today directly with Chase online, older accounts or those opened at specific branches might still be associated with a routing number tied to that original geographic location. For current online accounts, Chase often assigns a routing number that is widely applicable, frequently one of their primary routing numbers.

- Transaction Type: As discussed, the most significant differentiator for Chase routing numbers is the type of transaction. A routing number designated for ACH transfers will differ from one specifically for domestic wire transfers. This specialization ensures that funds are routed through the correct processing network, optimizing speed and efficiency for each type of transaction. It’s crucial not to interchange these numbers, as doing so will almost certainly result in a failed transfer and potentially incur fees.

Essential Scenarios Requiring a Chase Routing Number

Account holders will frequently encounter situations demanding the correct Chase routing number. These include:

- Setting Up Direct Deposit: For receiving paychecks, government benefits (like Social Security or tax refunds), or other regular disbursements directly into a Chase account, the correct ACH routing number is essential. This streamlines income reception and improves financial planning.

- Initiating or Receiving Domestic Wire Transfers: If you need to send or receive a large sum of money quickly within the U.S., a domestic wire transfer is often the chosen method. This requires a specific Chase routing number designated for wires, distinct from the ACH number.

- Paying Bills Electronically via ACH: Many utility companies, landlords, and service providers offer the option to pay bills directly from your bank account using ACH. This process mandates the correct Chase ACH routing number to ensure payments are processed successfully.

- Linking External Accounts: When connecting your Chase account to an external service like an investment platform, a budgeting app, or another bank account for transfers, the correct routing number is almost always required to establish the link.

- Receiving Tax Refunds or Other Electronic Disbursements: Government agencies, insurance companies, and other entities often disburse funds electronically, necessitating the correct routing information for your Chase account.

Practical Methods for Locating Your Chase ABA Number

Accuracy in obtaining your Chase routing number is paramount. Fortunately, Chase provides several reliable and accessible methods for finding this critical piece of financial information. Relying on official sources is key to ensuring you have the correct number for your specific account and transaction needs.

The Conventional Checkbook Method

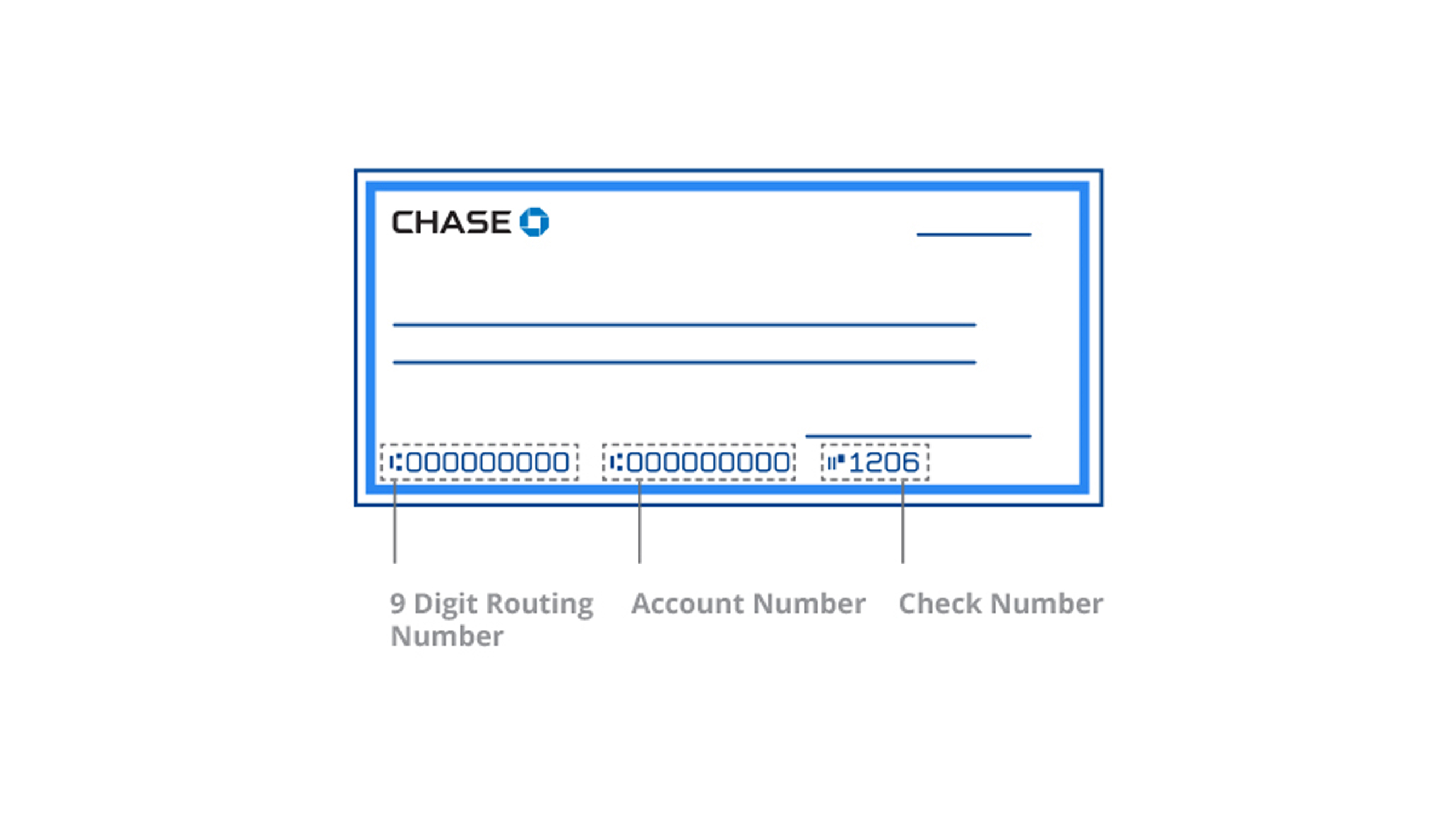

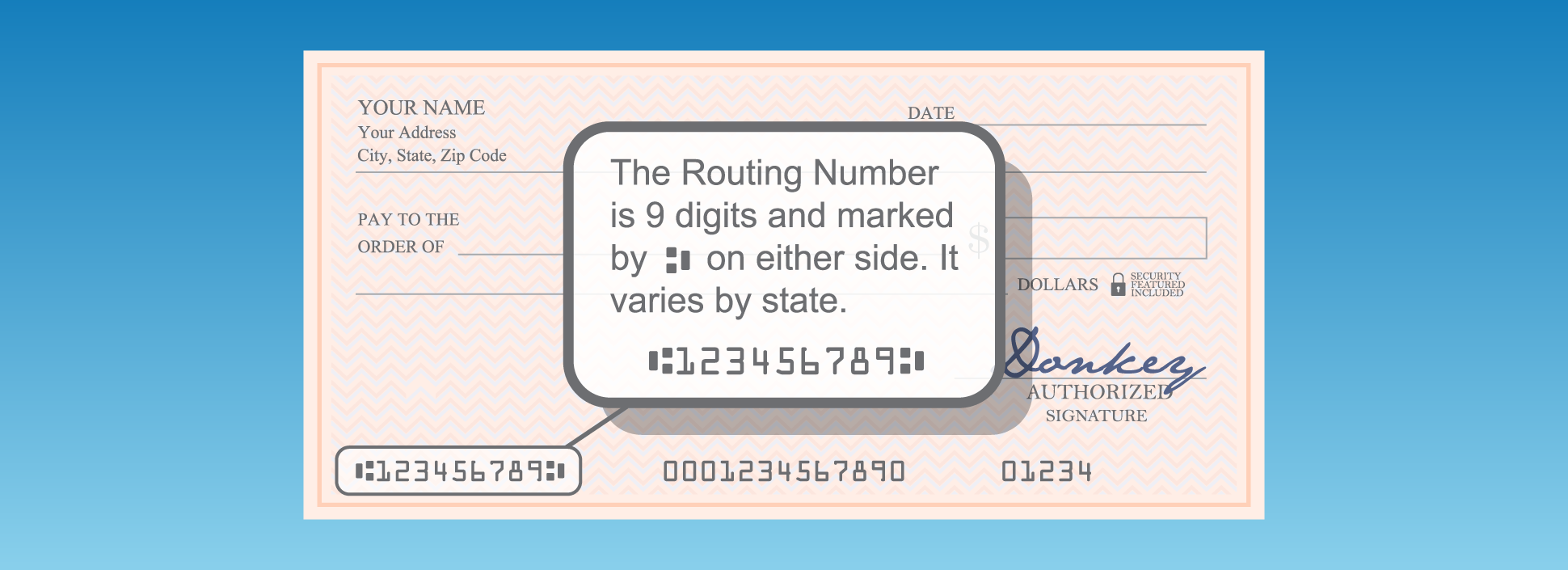

For many, the quickest way to find a routing number is on a personal check. For Chase accounts, the routing number is typically the first nine-digit number printed at the bottom left of your checks. It sits to the left of your account number and the check number. This method is generally reliable for standard ACH transactions and paper check processing. However, as noted, specific wire transfers might require a different number, so always cross-reference if the transaction is time-sensitive or involves a significant sum.

Leveraging Chase Online Banking and Mobile App

Chase’s digital platforms offer the most secure and up-to-date methods for finding your routing number.

- Chase Online Banking: After logging into your Chase online account, you can typically navigate to your account details. The routing number for your specific account will often be displayed prominently here. Some sections might be labeled “Account details,” “Statements,” or “Routing & Account numbers.” You may also be able to view a sample check image with the numbers highlighted.

- Chase Mobile App: Similarly, the Chase mobile application allows users to access their account information. By selecting a specific account, users can often find details like the account number and the relevant routing number. Some apps even have a dedicated “Routing Number” section within their menu or help resources. This method is particularly convenient for on-the-go verification.

Direct Communication with Chase Customer Service

If you’re unsure or need to verify a specific routing number for a complex transaction, especially an international wire, contacting Chase customer service directly is a reliable option. You can call their dedicated support lines or send a secure message through your online banking portal. When speaking with a representative, be prepared to verify your identity and clearly state the type of transaction for which you need the routing number (e.g., “I need the routing number for a domestic wire transfer to my checking account”). They can provide the precise number required.

Utilizing Official Chase Resources

Chase’s official website often provides a dedicated section for finding routing numbers. This might be under their “Help” or “FAQ” sections, or directly searchable. These online tools are designed to provide the correct numbers based on account type and transaction needs. It’s crucial to ensure you are on Chase’s official website (e.g., chase.com) to avoid phishing scams or misinformation from unofficial sources.

The Financial Ramifications of Incorrect Routing Information

The integrity of financial transactions hinges on the accuracy of banking information, none more so than the routing number. Providing an incorrect ABA number for your Chase account can have a cascading series of negative financial consequences, impacting both individuals and businesses. Understanding these risks underscores the importance of diligent verification.

Transaction Delays and Reversals

The most immediate consequence of using a wrong routing number is a transaction failure. Funds intended for direct deposit may not reach your account, causing delays in receiving your salary or benefits. Bill payments might bounce, leading to late fees from service providers and potential service interruptions. Wire transfers could be misdirected to an incorrect bank or returned to the sender, often taking several days or even weeks to resolve, during which time the funds are inaccessible. These delays can create significant liquidity issues, especially for businesses dependent on timely payments or payroll processing.

Potential Fees and Associated Costs

Financial institutions typically charge fees for failed transactions, returned items, or investigations stemming from incorrect routing information. If a direct deposit is returned due to a wrong routing number, your employer might charge a fee for reprocessing the payroll. Similarly, if an automated bill payment fails, your bank might impose an “insufficient funds” or “returned item” fee, even if your account had sufficient balance, simply because the routing information was incorrect. The recipient of a misdirected wire transfer might also incur fees if their bank has to process a return. These charges can quickly accumulate, adding an unexpected financial burden.

Security and Fraud Prevention

While an incorrect routing number primarily leads to transaction errors, it’s also important to consider the broader security implications. Fraudsters sometimes attempt to trick individuals into providing incorrect routing and account numbers to divert funds. This highlights the importance of only sharing your routing information through secure, verified channels and always double-checking any numbers you are given. If you suspect you’ve provided incorrect information or fallen victim to a scam, immediately contact Chase to report the issue and mitigate potential losses. Safeguarding your financial identifiers is a critical component of personal and business financial security.

Best Practices for Financial Accuracy

To avoid these pitfalls, always:

- Double-Check: Before initiating any transfer or setting up direct deposit, verify the routing number at least twice, preferably from a secure source like your online banking portal or a physical check.

- Use Specific Numbers: Understand whether the transaction requires an ACH, wire, or general check routing number.

- Consult Official Sources: Rely on Chase’s official website, mobile app, or customer service for the most accurate and up-to-date information.

- Confirm with Recipient/Sender: If you are receiving funds, confirm the required routing number with the sender. If sending, confirm with the recipient’s bank.

Integrating Routing Numbers into Your Financial Ecosystem

The correct ABA routing number for your Chase account is more than just a sequence of digits; it’s a foundational element that enables the vast majority of your financial interactions. Its accurate use is critical for both personal and business financial health, allowing for the seamless execution of transactions that define modern economic activity.

Streamlining Personal Finance Management

For individuals, accurate routing numbers are indispensable for efficient personal finance management. They enable automated savings plans, where funds are regularly transferred from a checking to a savings account. They facilitate seamless investment contributions by linking bank accounts to brokerage platforms. Budgeting apps and financial aggregators often require routing numbers to connect and monitor accounts, providing a holistic view of one’s financial standing. Without the correct routing number, these essential tools and strategies for building wealth and managing expenses would be cumbersome, inefficient, or entirely impossible.

Business Finance and Payroll Efficiency

In the realm of business finance, the correct Chase routing number is a non-negotiable requirement. Businesses rely on it for:

- Payroll Processing: Employers use routing numbers to ensure that employee paychecks are directly deposited into the correct bank accounts on time, a critical component of employee satisfaction and regulatory compliance.

- Vendor Payments: Paying suppliers and vendors electronically via ACH or wire transfers necessitates accurate routing information to maintain good business relationships and avoid late payment penalties.

- Receiving Customer Funds: Businesses that accept electronic payments from customers (e.g., subscription services, e-commerce, B2B invoices) depend on accurate routing numbers to ensure these funds are correctly deposited into their operating accounts, directly impacting cash flow and revenue recognition.

- Treasury Management: For larger corporations, precise routing information is vital for sophisticated treasury management operations, including inter-account transfers, liquidity management, and international fund movements.

Any error in routing numbers can lead to significant disruptions in cash flow, reconciliation nightmares, and potentially damage business reputation.

Regulatory Compliance and Data Integrity

The widespread use of ABA routing numbers is also deeply integrated with financial regulatory compliance and the broader principle of data integrity within the banking sector. Regulatory bodies require financial institutions to process transactions accurately to prevent fraud, facilitate anti-money laundering (AML) efforts, and ensure consumer protection. Accurate routing numbers contribute to the audit trails necessary for compliance and provide the data integrity required for reliable financial reporting and system operations. As such, the seemingly simple act of using the correct routing number is a small but vital cog in the vast, regulated machinery of the global financial system.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.