In the intricate world of personal finance, understanding the fundamental tools at your disposal is paramount. Among the most crucial pieces of information for managing your money are your bank account and routing numbers. These seemingly simple strings of digits are the bedrock upon which most financial transactions are built, facilitating everything from direct deposits and automated bill payments to wire transfers and online purchases. Yet, despite their importance, many individuals find themselves momentarily stumped when asked to provide them. This comprehensive guide aims to demystify these essential numbers, explaining what they are, why they matter, and, most importantly, precisely how and where you can locate them with ease and confidence.

Understanding the Fundamentals: Account and Routing Numbers Explained

Before delving into the “how-to,” it’s vital to grasp the distinct roles of these two critical identifiers. While often requested in tandem, they serve different, albeit complementary, functions in the banking ecosystem.

What is a Routing Number?

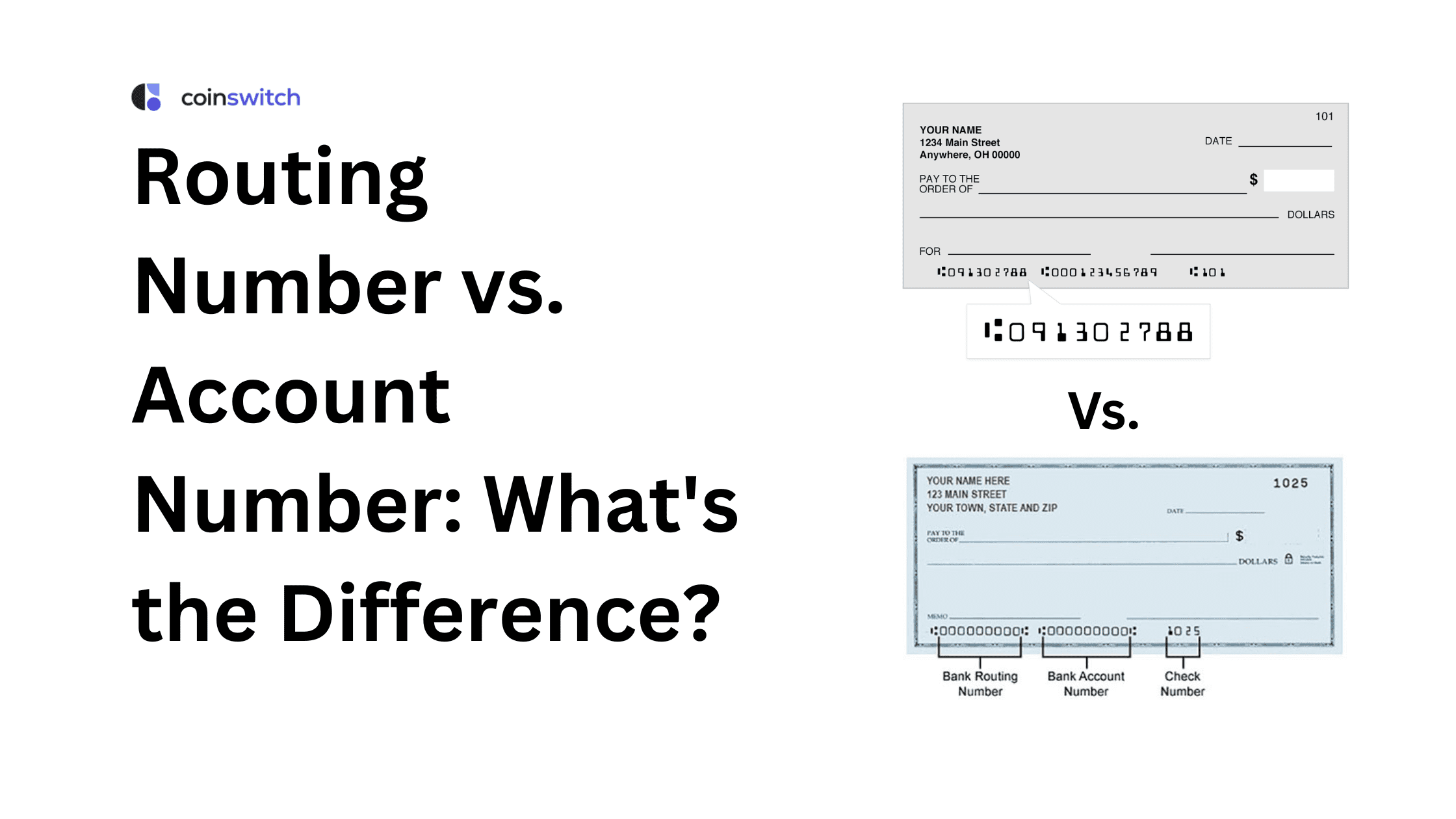

A routing number, also known as an ABA (American Bankers Association) routing transit number, is a nine-digit code that identifies your financial institution in the United States. It’s like a postal code for your bank, ensuring that money transfers are directed to the correct bank or credit union. Issued by the American Bankers Association, these numbers are unique to each financial institution and can sometimes vary based on the type of transaction (e.g., wire transfer vs. ACH transfer) or even the specific region or branch where your account was opened, especially with larger banks. Their primary purpose is to facilitate the electronic transfer of funds between financial institutions, most notably through the Automated Clearing House (ACH) network for direct deposits and bill payments, and for wire transfers.

What is an Account Number?

Your account number is a unique identifier assigned by your financial institution to your specific bank account. Unlike the routing number, which identifies the bank, the account number specifies your individual account within that bank. Ranging typically from 10 to 12 digits (though variations exist), this number ensures that once funds arrive at the correct bank (identified by the routing number), they are then deposited into or withdrawn from the exact account belonging to you. Every checking, savings, and even loan account you hold will have its own distinct account number, making it the personal identifier for your financial relationship with the bank.

Why Are These Numbers Crucial for Your Finances?

These two numbers are the fundamental coordinates for your financial life, enabling a wide array of essential transactions that underpin modern money management. Their importance cannot be overstated:

- Direct Deposit: For receiving your salary, tax refunds, government benefits, or other regular payments directly into your account, both numbers are indispensable.

- Automated Bill Payments: Setting up recurring payments for utilities, loans, rent, or subscriptions often requires these details to ensure seamless, on-time payments.

- Online and Mobile Banking Transfers: While internal transfers within the same bank might not always require them, initiating transfers to accounts at other financial institutions certainly does.

- Wire Transfers: For expedited, often international, money transfers, both your bank’s routing number and your specific account number are critical for the funds to reach the intended recipient swiftly and securely.

- Setting Up Payment Services: Many third-party payment apps and services require these details to link your bank account for deposits or withdrawals.

- Check Writing: When you write a personal check, both your routing and account numbers are pre-printed, authorizing the payee to withdraw funds from your account.

Without accurate routing and account numbers, many common financial activities would be impossible, leading to delays, fees, or even misdirected funds.

Primary Methods for Locating Your Banking Information

Fortunately, finding your account and routing numbers isn’t a treasure hunt. Financial institutions make them readily accessible through several common and secure channels.

On Your Personal Checks

Perhaps the most common and often the quickest way to find these numbers is by looking at a personal check from your checking account. On the bottom of a standard check, you’ll typically find three sets of numbers printed in magnetic ink (MICR line), usually from left to right:

- Routing Number: This is the first set of nine digits on the far left.

- Account Number: This is the middle set of numbers, which can vary in length.

- Check Number: The final set of numbers on the right, which matches the check number in the top right corner of the check.

It’s important to note that the routing number on your checks is specifically for your checking account and might differ from the routing number used for wire transfers or your savings account. Always double-check with your bank if you’re unsure.

Through Your Bank Statements

Whether you receive paper statements in the mail or access them digitally through your bank’s website, your bank statement is another reliable source for your account and routing numbers.

- Paper Statements: Your full account number is almost always printed prominently near the top of your statement, often alongside your name and address. The routing number might also be listed in a section dedicated to “Bank Information” or “Important Numbers,” though it’s sometimes omitted if the statement pertains only to a single account type (e.g., checking) and the routing number is widely known for that bank.

- Online Statements: Accessing your statements through your bank’s online portal or mobile app provides the same information. Navigate to the “Statements” section, select the most recent statement, and view the PDF. The information will be structured similarly to a paper statement. This method offers a secure way to retrieve details without needing a physical checkbook.

Utilizing Online Banking and Mobile Apps

In today’s digital age, your bank’s online banking platform and mobile app are arguably the most convenient and frequently used resources for managing your accounts and finding key information.

- Online Banking Portal: Log in to your bank’s website. Once logged in, navigate to the specific account you need information for (checking, savings, etc.). Banks typically display your full account number directly on the account summary page or within an “Account Details,” “Account Information,” or “View Details” section. The routing number is often found in a separate section labeled “Bank Info,” “Direct Deposit Info,” or “Routing Numbers,” as it applies to the institution as a whole rather than a single account.

- Mobile Banking App: Similar to the online portal, most modern banking apps provide easy access to this information. After logging in, select the desired account. Look for options like “Account Details,” “Show Account Numbers,” or a similar phrasing. Due to security protocols, some apps might require an additional verification step (like a PIN or biometric scan) to display sensitive numbers. This method is exceptionally useful when you’re on the go and need quick access to your financial details.

Alternative and Direct Approaches

While checks, statements, and online banking cover the vast majority of needs, there are other situations or methods you might need to employ.

Contacting Your Financial Institution Directly

If you’re unable to find your numbers through the above methods, or if you require specific routing numbers for particular transaction types (e.g., an international wire transfer routing number, which can differ from the standard ACH routing number), contacting your bank directly is a foolproof solution.

- Customer Service Line: Call the customer service number listed on your bank’s website, statement, or the back of your debit card. Be prepared to verify your identity thoroughly (account number, social security number, mother’s maiden name, security questions, etc.) to ensure your financial information is protected.

- Visiting a Branch: For those who prefer in-person assistance, a visit to your local bank branch can resolve the issue quickly. A bank teller or customer service representative can provide you with your account and routing numbers after verifying your identity with a valid photo ID. This method can also be helpful for more complex inquiries, such as setting up specific types of transfers.

Other Physical Documents: Deposit Slips and Debit Cards (Caveats)

While less common or less reliable for all information, some other documents can occasionally provide clues:

- Deposit Slips: Pre-printed deposit slips for your checking account will also contain your routing and account numbers, similar to personal checks. However, these are less commonly used by individuals today.

- Debit Cards: Your debit card does not contain your account number or routing number. It has a 16-digit card number, an expiration date, and a CVV code, which are used for purchases, not for direct bank account transactions like direct deposit or ACH payments. Do not confuse your debit card number with your bank account number.

Safeguarding Your Financial Identity: Security Best Practices

Your account and routing numbers are sensitive pieces of information. While not as high-risk as your social security number, they can be exploited if they fall into the wrong hands. Protecting them is an integral part of responsible financial management.

When and How to Share Your Numbers Safely

Only share your account and routing numbers with trusted entities and for legitimate financial purposes. This includes:

- Employers: For direct deposit of your paycheck.

- Government Agencies: For tax refunds or benefits.

- Reputable Billers: For automated payments of utilities, loans, etc.

- Investment Firms or Payment Processors: To link your bank account for transfers.

Always ensure you are using secure channels (e.g., a secure online portal with encryption, or a verified paper form). Be wary of sharing this information over unsecured email or public Wi-Fi networks.

Recognizing and Avoiding Scams

Scammers often try to phish for banking information. Be suspicious of:

- Unsolicited requests: Never provide your bank details in response to unexpected emails, texts, or calls, especially if they threaten to close your account or demand immediate action.

- Too-good-to-be-true offers: Be skeptical of requests for your banking info to receive prize money, lottery winnings, or inheritances.

- Suspicious websites: Always ensure you are on your bank’s official website (check the URL and look for “https”).

Legitimate institutions will rarely ask for your full account number via email or text. If in doubt, always contact your bank directly using a verified phone number or website.

Regular Monitoring of Your Accounts

Even with the best security practices, vigilance is key. Regularly review your bank statements and transaction history through online banking or your mobile app. Look for any unauthorized transactions, no matter how small. Promptly report any suspicious activity to your bank to mitigate potential fraud. Setting up transaction alerts can also provide an early warning system for any unusual account activity.

Common Scenarios and Troubleshooting Tips

Navigating banking information can sometimes present specific challenges. Being prepared for these can save time and frustration.

Distinguishing Between Checking and Savings Account Numbers

It’s a common misconception that checking and savings accounts within the same bank share the same account number, or even the same routing number. This is almost never the case. While they might share the same bank’s routing number (for ACH transfers), each individual account (checking, savings, money market) will have its own distinct account number. When setting up a direct deposit or payment, always ensure you are providing the correct account number for the specific account you intend to use. Double-check in your online banking platform or on your respective statements.

Handling Multiple Accounts and Institutions

If you hold accounts at multiple banks or have several accounts (e.g., two checking accounts, one savings) with the same institution, it’s crucial to keep track of which routing and account numbers belong to which. Creating a secure, encrypted document or using a reputable password manager to store this information (alongside other sensitive data) can be a helpful organizational strategy. When initiating transactions, always pause to confirm you’ve selected the correct set of numbers for the intended account.

What to Do If You Can’t Find Them

If, after trying all the suggested methods, you still cannot locate your account and routing numbers, don’t panic. The definitive solution is always to contact your financial institution directly.

- Call Customer Service: This is the most efficient route. Be ready to verify your identity.

- Visit a Branch: For in-person assistance and peace of mind.

Avoid guessing or using old, unverified information, as incorrect numbers can lead to returned payments, delays, and additional fees. Your bank’s representatives are equipped to provide accurate information and guide you through any specific requirements.

In conclusion, your account and routing numbers are the essential coordinates that govern the movement of your money. By understanding what they are, where to find them, and how to protect them, you empower yourself to manage your finances effectively and securely in an increasingly digital world. Make it a habit to know where these numbers reside, and you’ll be well-prepared for any financial transaction life throws your way.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.