Understanding precisely how much money you earn each month is not merely a bureaucratic exercise; it is the bedrock of sound personal finance. Without a clear and accurate picture of your monthly income, effective budgeting, strategic saving, wise investing, and informed financial planning become virtually impossible. In an increasingly complex economic landscape, where income streams can vary from fixed salaries to dynamic freelance earnings and passive investments, mastering this calculation is more critical than ever. It empowers you to make informed decisions, identify financial vulnerabilities, and set achievable monetary goals. This comprehensive guide will walk you through the nuances of calculating your monthly income, ensuring you have the clarity needed to navigate your financial journey with confidence.

The Foundational Importance of Understanding Your Income

Before delving into the mechanics of calculation, it’s crucial to grasp why this particular financial metric holds such significant weight. Your monthly income isn’t just a number; it’s a reflection of your earning power and the primary fuel for your financial aspirations.

Why Accurate Income Calculation Matters

At its core, accurate income calculation serves several vital functions. Firstly, it forms the basis of budgeting. A well-structured budget dictates where your money goes, ensuring expenses don’t outpace earnings. Without a precise income figure, any budget you create will be built on shaky ground, potentially leading to overspending, debt accumulation, or missed financial opportunities. Secondly, it is indispensable for financial planning and goal setting. Whether you’re saving for a down payment on a house, planning for retirement, funding a child’s education, or aiming for financial independence, knowing your monthly income allows you to set realistic savings targets and project how long it will take to achieve your goals.

Furthermore, understanding your income helps in debt management. When assessing your capacity to take on new debt or pay down existing liabilities, lenders and financial advisors heavily rely on your income figures. Internally, a clear income picture helps you gauge your debt-to-income ratio, a key indicator of financial health. Lastly, it offers peace of mind and financial control. The clarity that comes with knowing your exact monthly earnings alleviates financial anxiety and puts you firmly in the driver’s seat of your financial life.

Gross vs. Net: A Crucial Distinction

One of the most common pitfalls in income calculation is confusing gross income with net income. The distinction between these two figures is paramount for accurate financial management.

Gross Monthly Income refers to the total amount of money you earn before any deductions are taken out. This includes your base salary, hourly wages multiplied by hours worked, commissions, bonuses, freelance payments, rental income, and any other earnings from all sources. It’s the “headline” number you might see on your employment contract or a project invoice.

Net Monthly Income, often referred to as “take-home pay,” is the amount of money you actually receive after all mandatory and voluntary deductions have been subtracted from your gross income. These deductions can include federal, state, and local taxes, Social Security contributions, Medicare contributions, health insurance premiums, retirement plan contributions (e.g., 401(k), IRA), and other voluntary deductions like life insurance or union dues. It is your net income that you actually have available to spend, save, and invest. For effective budgeting and daily financial planning, your net monthly income is the figure you should primarily focus on.

Deconstructing Your Income Streams

The first step in calculating your monthly income is to identify and itemize all your sources of income. Most people have multiple streams, and understanding how each one contributes to your total is essential.

Fixed Salary and Hourly Wages: The Straightforward Approach

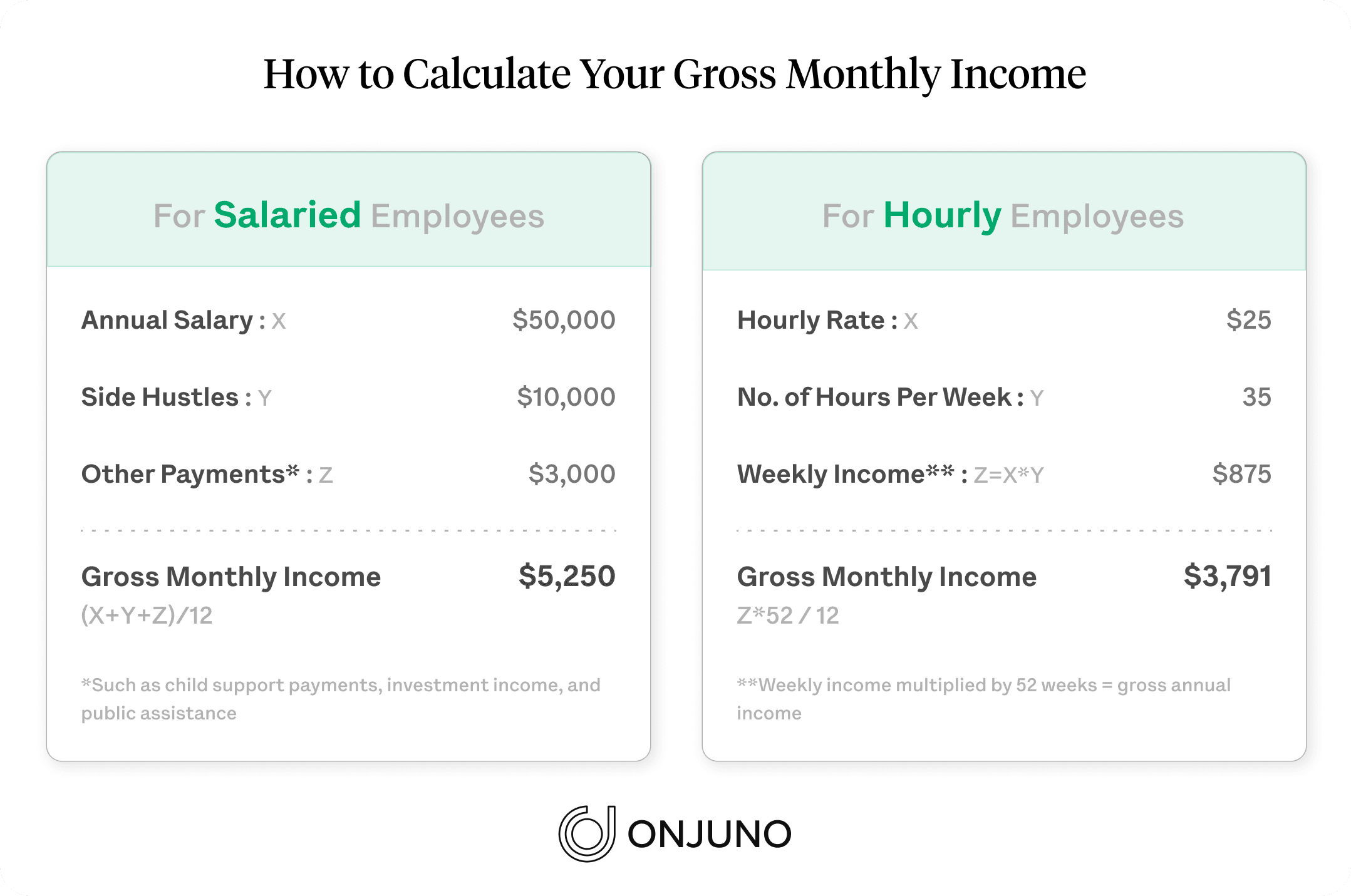

For individuals on a fixed annual salary, calculating monthly gross income is relatively straightforward. Simply divide your annual salary by 12. For example, if your annual salary is $60,000, your gross monthly income from this source is $5,000.

For those earning hourly wages, the calculation requires multiplying your hourly rate by the number of hours you typically work in a month. This can be slightly trickier if your hours vary.

- Consistent Hours: If you consistently work 40 hours a week, multiply 40 hours/week by your hourly rate, then multiply that weekly total by 4 (for an average month) or 4.33 (for a more precise annual average divided by 12).

- Example: $25/hour x 40 hours/week = $1,000/week. $1,000/week x 4.33 weeks/month = $4,330 gross monthly.

- Variable Hours: If your hours fluctuate, it’s best to look at your pay stubs for the last few months to calculate an average. Sum your gross income from hourly wages over a three-month period and divide by three to get a more realistic monthly average.

Navigating Variable Income: Freelance, Commissions, and Gig Work

Income from freelance work, commissions, sales, tips, or gig economy platforms presents a unique challenge due to its inherent variability. Relying on the best month’s earnings can lead to overestimation, while only considering the worst month can lead to unnecessary belt-tightening.

The most accurate method for variable income is to calculate an average over a significant period, typically the last 6 to 12 months.

- Gather Records: Compile all invoices, payment confirmations, bank statements, or platform reports showing your gross earnings from these sources over the chosen period.

- Sum Total Earnings: Add up all gross income from these variable sources for the entire period.

- Calculate Monthly Average: Divide the total earnings by the number of months in your chosen period.

- Example: If you earned $30,000 from freelance work over the past 12 months, your average gross monthly income from freelance is $2,500.

When dealing with highly unpredictable variable income, it’s often prudent to adopt a conservative estimate. You might budget based on 80% of your historical average or use the average of your lower-earning months to ensure you always have enough to cover your expenses, using any surplus as a bonus for savings or discretionary spending.

Unlocking Passive and Investment Income

Don’t forget to include income generated from passive sources and investments. These can significantly bolster your overall monthly income picture.

- Rental Income: If you own property and rent it out, subtract any direct monthly expenses (mortgage interest, property taxes, insurance, maintenance reserves) from your gross rental receipts to arrive at a net rental income.

- Dividends and Interest: If you receive regular dividends from stocks or interest from savings accounts, bonds, or other investments, factor these into your monthly calculation. Some dividends might be quarterly, so divide the quarterly amount by three.

- Royalties: For authors, musicians, or creators, royalties can be a sporadic but important income stream. Average these over a longer period, similar to variable income.

- Business Income (for owners): If you own a small business, calculate your personal draw or profit distribution. This requires a clear understanding of your business’s net profit after all business expenses.

Essential Deductions and Adjustments

Once you have a handle on your gross income from all sources, the next critical step is to account for all deductions to arrive at your true net monthly income. This is where most people get confused, but understanding these deductions is fundamental.

Mandatory Deductions: Taxes, Social Security, and Medicare

These are non-negotiable deductions that are typically withheld from your pay by your employer.

- Federal Income Tax: The amount withheld depends on your income, filing status, and the information provided on your W-4 form. It’s progressive, meaning higher earners pay a higher percentage.

- State and Local Income Tax: Many states and some cities also levy income taxes. The rates vary significantly by location.

- Social Security (FICA): A fixed percentage (currently 6.2% for employees) of your earnings up to an annual limit. Employers match this amount.

- Medicare (FICA): A fixed percentage (currently 1.45% for employees) of all your earnings, with no income limit. Employers also match this amount.

For self-employed individuals, these taxes are paid directly as self-employment tax and are typically higher (covering both the employee and employer portions of Social Security and Medicare) and paid quarterly. You must set aside a significant portion of your gross income for these taxes.

Voluntary Deductions: Retirement, Health Benefits, and More

Beyond mandatory taxes, employers often offer benefits that come with voluntary deductions from your paycheck.

- Retirement Contributions: Contributions to a 401(k), 403(b), or other employer-sponsored retirement plans are often deducted pre-tax, reducing your taxable income.

- Health Insurance Premiums: Your share of health, dental, and vision insurance premiums is typically deducted.

- Life and Disability Insurance: Premiums for employer-provided or optional life and disability insurance.

- Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): Contributions to these accounts, often pre-tax, used for healthcare or dependent care expenses.

- Loan Repayments: Some companies offer payroll deductions for company loans or charitable contributions.

Collect all your pay stubs and benefit statements to accurately identify and sum these deductions.

Accounting for Pre-Tax vs. Post-Tax Contributions

It’s important to understand the difference between pre-tax and post-tax deductions, as they impact your taxable income differently.

- Pre-Tax Deductions (e.g., traditional 401(k) contributions, health insurance premiums, FSA contributions) are subtracted from your gross income before federal and state income taxes are calculated. This reduces your taxable income, leading to a lower tax bill.

- Post-Tax Deductions (e.g., Roth 401(k) contributions, some life insurance premiums) are subtracted after taxes have been calculated. They don’t reduce your current taxable income but still lower your net take-home pay.

Be meticulous in identifying which deductions fall into each category, as this precision is vital for accurately determining your true net income.

Practical Methods and Tools for Calculation

Calculating your monthly income doesn’t have to be daunting. Several practical methods and tools can streamline the process and enhance accuracy.

Leveraging Pay Stubs and Bank Statements

Your pay stubs are your most direct and accurate source of information for employed income. They clearly itemize your gross pay, all deductions (mandatory and voluntary), and ultimately your net pay for each pay period.

- Bi-weekly Pay: If you are paid bi-weekly (26 times a year), multiply your net pay per period by 26 and then divide by 12 to get your average net monthly income.

- Semi-monthly Pay: If you are paid semi-monthly (twice a month, 24 times a year), multiply your net pay per period by 24 and then divide by 12, or simply multiply by 2.

- Weekly Pay: If you are paid weekly (52 times a year), multiply your net pay per period by 52 and then divide by 12.

For variable income, bank statements and platform transaction histories are invaluable. They provide a clear record of all deposits received. Remember to differentiate between gross deposits and any platform fees or taxes already deducted. For self-employed individuals, a well-maintained income and expense ledger is essential.

The Power of Spreadsheets and Budgeting Apps

For a more robust and organized approach, spreadsheets (like Microsoft Excel or Google Sheets) are highly effective. You can create a simple template to list all income sources, gross amounts, and deductions, allowing you to automatically calculate your total gross and net monthly income.

- Create columns for “Income Source,” “Gross Amount,” “Pre-Tax Deductions,” “Post-Tax Deductions,” “Net Amount.”

- Use formulas to sum up totals and perform calculations.

- This approach is particularly useful for tracking variable income, as you can continuously update it.

Budgeting apps (e.g., Mint, YNAB, Personal Capital, Simplifi) offer an automated solution. Many of these apps can link directly to your bank accounts, credit cards, and investment accounts, automatically categorizing transactions and providing an overview of your income and expenses. While convenient, always double-check their categorization, especially for less common income sources, to ensure accuracy. These tools can also help you track your net worth and progress towards financial goals.

Seeking Professional Guidance

If your financial situation is particularly complex—perhaps you have multiple businesses, intricate investments, or unique tax considerations—it might be beneficial to consult with a financial advisor or an accountant. They can help you accurately calculate your income, understand tax implications, and develop strategies for optimizing your financial health. Their expertise can provide invaluable insights and ensure you’re not missing any crucial details.

Beyond the Numbers: Maximizing and Managing Your Income

Calculating your monthly income is not the final step; it’s the starting point for effective financial management and strategic growth.

Regular Review and Adaptation

Your income and expenses are not static. Life changes, promotions happen, new side hustles emerge, and expenses fluctuate. Therefore, it’s crucial to review your income calculations regularly, at least once a quarter or whenever there’s a significant life event (e.g., a new job, marriage, birth of a child, major purchase). This ensures your budget remains relevant and accurate, allowing you to adapt your financial strategies as needed.

Strategies for Stabilizing Variable Income

For those with highly variable income, maintaining financial stability can be challenging.

- Build an Emergency Fund: A robust emergency fund (3-6 months of living expenses) is even more critical for variable income earners, providing a buffer during lean periods.

- “Pay Yourself a Salary”: Consider transferring a consistent “salary” amount from your business or main income account to your personal checking account each month, saving the surplus from higher-earning months.

- Conservative Budgeting: Always budget based on your lower average income months to avoid overspending and build a cushion.

The Link Between Income Calculation and Financial Goals

Ultimately, a precise understanding of your monthly income is the engine that drives your financial aspirations. It allows you to:

- Set Realistic Goals: Knowing what you earn helps you determine how much you can realistically save or invest towards a down payment, retirement, or debt repayment.

- Track Progress: You can monitor your income growth over time and see how it impacts your ability to reach financial milestones faster.

- Identify Opportunities: A clear picture might reveal that you have more disposable income than you thought, opening up opportunities for additional investments or accelerated debt payoff. Conversely, it might highlight a need to explore additional income streams.

Calculating your monthly income might seem like a simple task, but its accuracy underpins every other aspect of your personal financial health. By diligently tracking all income sources, meticulously accounting for deductions, and regularly reviewing your figures, you gain the clarity and control necessary to build a secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.