Social Security is more than just a government program; for millions of Americans, it’s a foundational pillar of financial security, particularly in retirement. Yet, despite its pervasive influence, a significant degree of misunderstanding often surrounds how much individuals can truly “earn” from it. The phrase “earn with Social Security” itself can be misleading, as benefits are not earnings in the traditional sense, but rather an entitlement built on your lifetime contributions and specific programmatic rules. Understanding the intricacies of how your benefits are calculated, the factors that influence them, and strategies to maximize your payout is crucial for effective retirement planning. This article delves into the mechanisms that determine your Social Security income, offering insights to help you navigate this complex, yet vital, financial landscape.

Understanding the Fundamentals of Social Security Benefits

Before we can discuss how much you can potentially receive, it’s essential to grasp the core principles behind Social Security. It operates on a pay-as-you-go system, where current workers’ contributions fund the benefits of today’s retirees and other beneficiaries. Your future benefits are intrinsically linked to your work history and contributions, making it a system where you effectively “earn” your entitlement over decades.

What is Social Security?

Social Security is a federal insurance program that provides benefits to retirees, the disabled, and survivors of deceased workers. It is funded through payroll taxes, specifically the Federal Insurance Contributions Act (FICA) tax, which is deducted from your wages. These taxes go into trust funds that pay out current benefits. The program’s fundamental goal is to provide a baseline level of income replacement, helping to protect beneficiaries from the financial hardships associated with old age, disability, or the death of a primary wage earner. It’s not designed to be a sole source of retirement income but rather a component of a diversified financial plan.

The Core Calculation: AIME and PIA

The amount you receive from Social Security primarily depends on your lifetime earnings. The Social Security Administration (SSA) calculates your benefit using a formula based on your Average Indexed Monthly Earnings (AIME).

- Indexed Earnings: The SSA takes your earnings from your highest 35 years of work, adjusting (indexing) them to account for changes in the average wage level over time. This indexing ensures that earlier earnings reflect their relative value compared to more recent earnings.

- Average Indexed Monthly Earnings (AIME): These 35 years of indexed earnings are summed up and then divided by 420 (the number of months in 35 years) to arrive at your AIME.

- Primary Insurance Amount (PIA): Your PIA is the basic benefit you would receive if you claim benefits at your Full Retirement Age (FRA). It’s calculated by applying a progressive formula to your AIME using specific “bend points.” These bend points mean that lower earners receive a higher percentage of their average earnings back as benefits compared to higher earners, reflecting the program’s aim to provide a safety net. For example, a certain percentage of your AIME up to the first bend point is included, then a smaller percentage for the AIME between the first and second bend points, and so on.

Understanding your AIME and PIA is critical because these figures form the bedrock of your potential Social Security income. Without a 35-year work history, years with no earnings are counted as zero, which can significantly lower your AIME and, consequently, your PIA.

Key Factors Influencing Your Benefit Amount

While AIME and PIA are central, several other factors can significantly alter the amount you actually receive:

- Lifetime Earnings History: As noted, higher indexed earnings over 35 years lead to a higher AIME and PIA. Consistent work and maximizing your earnings throughout your career are paramount.

- Age You Claim Benefits: This is arguably the most impactful decision you’ll make. You can start receiving retirement benefits as early as age 62, but your monthly benefit will be permanently reduced. Conversely, delaying beyond your FRA (up to age 70) results in an increased monthly benefit.

- Cost-of-Living Adjustments (COLAs): Once you start receiving benefits, they are subject to annual COLAs, which are designed to help your purchasing power keep pace with inflation.

- Spousal and Survivor Benefits: If you are married or divorced, or if a spouse has passed away, you may be eligible for spousal or survivor benefits based on their earnings record, which can sometimes be higher than your own benefit.

- Government Pension Offset (GPO) and Windfall Elimination Provision (WEP): If you receive a pension from a job where you didn’t pay Social Security taxes (e.g., some government jobs), the GPO or WEP might reduce your Social Security benefits.

- Taxes: A portion of your Social Security benefits may be subject to federal income tax, depending on your combined income.

Navigating Earnings Limits While Receiving Benefits

A common misconception revolves around working while receiving Social Security benefits, especially before reaching Full Retirement Age. The Social Security Administration imposes annual earnings limits that can temporarily reduce your benefits if you earn above a certain threshold. This is a critical aspect to understand if you plan to ease into retirement or continue working part-time.

The Annual Earnings Limit Explained

If you are below your Full Retirement Age (FRA) and collecting Social Security benefits, there’s a limit to how much you can earn from working without your benefits being reduced. This earnings limit changes annually.

- Before Year of FRA: For those who will not reach their FRA in the current year, the SSA will deduct $1 from your benefits for every $2 you earn above a specific annual limit. For example, if the limit is $22,320 (as it was in 2024), and you earn $24,320, you’ve exceeded the limit by $2,000. Your benefits would be reduced by $1,000 ($2,000 / 2).

- In the Year You Reach FRA: A higher earnings limit applies in the year you reach your FRA, and the reduction rate is different. The SSA will deduct $1 from your benefits for every $3 you earn above a higher annual limit (e.g., $59,520 in 2024), but only up to the month you reach your FRA. Once you hit your FRA, the earnings limit no longer applies.

How Earnings Limits Impact Your Checks

It’s important to understand that any benefits withheld due to exceeding the earnings limit are not lost forever. Once you reach your FRA, the SSA recalculates your benefit amount to account for the months your benefits were withheld. This means your future monthly payments will be slightly higher to compensate for the reduction. This adjustment effectively “gives back” the withheld benefits over your remaining lifespan. However, the immediate impact is a reduced or temporarily suspended monthly payment, which can significantly affect your cash flow if not anticipated.

Exceptions and Full Retirement Age Considerations

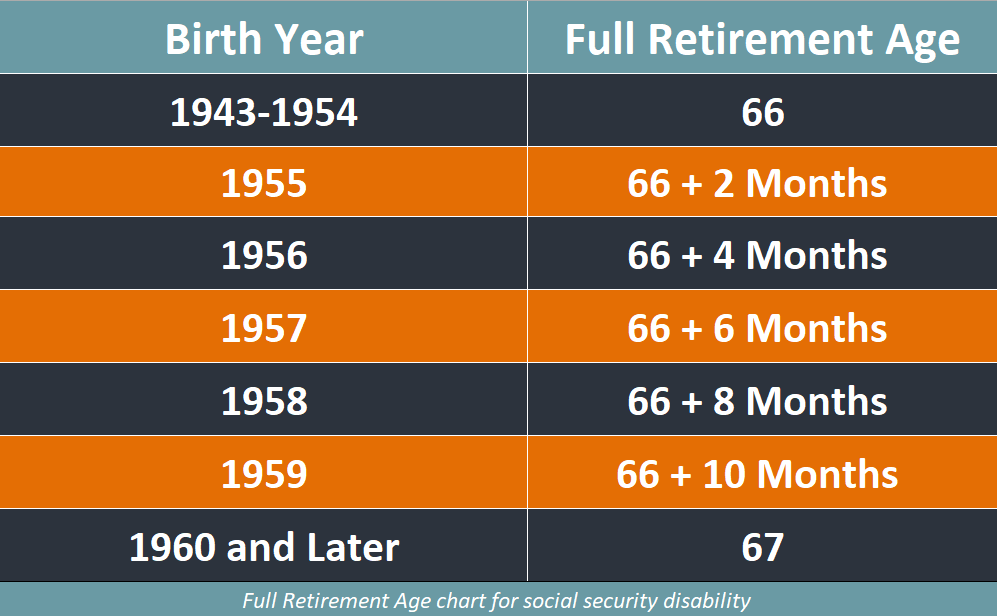

The most significant exception to earnings limits is reaching your Full Retirement Age (FRA). Once you attain your FRA, you can earn any amount of money from work without it affecting your Social Security benefits. This is a crucial point for retirement planning, as it provides financial flexibility for those who wish to continue working without penalty. Your FRA depends on your birth year, generally ranging from 66 for those born between 1943 and 1954, gradually increasing to 67 for those born in 1960 or later. Knowing your specific FRA is fundamental to making informed decisions about when to claim benefits and whether to continue working.

Strategies to Maximize Your Social Security Income

While Social Security isn’t meant to be your sole source of retirement income, maximizing your benefits is a smart financial move. Strategic decisions made over your working life and at the point of claiming can significantly increase the total amount you receive over your lifetime.

The Critical Role of Claiming Age

The decision of when to claim Social Security benefits is perhaps the single most impactful choice you’ll make regarding your payout.

- Claiming Early (Age 62-FRA): You can start receiving benefits as early as age 62, but your monthly payment will be permanently reduced. The reduction is about 6.7% per year for the first three years before your FRA, and then about 5% per year for any additional years. For example, claiming at age 62 when your FRA is 67 can result in a permanent reduction of up to 30%. While you get more payments overall, each payment is smaller. This strategy might be suitable for those with health issues, a shorter life expectancy, or an immediate need for funds.

- Claiming at Full Retirement Age (FRA): This is the age at which you receive 100% of your Primary Insurance Amount (PIA). For most people, this is a balanced approach, providing a substantial benefit without waiting too long.

- Delaying Benefits (FRA-Age 70): For every year you delay claiming benefits past your FRA, up to age 70, you earn Delayed Retirement Credits (DRCs). These credits increase your monthly benefit by 8% per year. This means delaying from an FRA of 67 to age 70 can result in a 24% permanent increase in your monthly benefit (8% x 3 years). This strategy is often recommended for those with good health, a longer life expectancy, or who don’t need the income immediately, as it guarantees a higher inflation-adjusted income stream for life.

Working Longer: Boosting Your AIME

Your highest 35 years of indexed earnings are used to calculate your AIME. If you have fewer than 35 years of earnings, zero-earning years will be included in the calculation, reducing your overall average. Conversely, if you work more than 35 years, the SSA will automatically drop your lowest-earning years and replace them with higher-earning years from your later career. Since most people’s earnings peak later in their careers, working longer, especially into your 50s and 60s, can replace lower-earning early career years with higher ones, thereby increasing your AIME and ultimately your PIA. Even a few extra years of high earnings can make a noticeable difference in your monthly benefit.

Spousal and Survivor Benefits: Unlocking Additional Value

Social Security is not just for individual workers; it also provides benefits for families.

- Spousal Benefits: If you are married, you may be eligible to claim a spousal benefit based on your spouse’s work record. This benefit can be up to 50% of your spouse’s PIA. You can typically claim a spousal benefit if it’s higher than your own benefit. There are strategies, such as “file and suspend” (now restricted) or “restricted application” (for those born before January 2, 1954), that allowed for maximizing combined household benefits. Consulting with the SSA or a financial advisor is crucial to understand current rules.

- Survivor Benefits: If your spouse passes away, you may be eligible for survivor benefits, which can be up to 100% of the deceased spouse’s benefit. This is a critical safety net for many families. Divorced spouses may also be eligible for benefits if the marriage lasted at least 10 years and other conditions are met.

Understanding Cost-of-Living Adjustments (COLAs)

Once you begin receiving Social Security benefits, they are automatically adjusted annually to account for inflation. These Cost-of-Living Adjustments (COLAs) are designed to help your purchasing power keep pace with rising prices. COLAs are determined by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While COLAs can vary from year to year (and sometimes be zero in periods of low inflation), they provide an invaluable safeguard against the erosion of your fixed income over a long retirement, a feature that many private pensions lack.

Taxation and the Broader Retirement Landscape

While Social Security provides a vital income stream, it’s crucial to understand how it fits into your broader financial picture, including its tax implications and how it integrates with other retirement savings.

When Social Security Benefits Become Taxable

A common surprise for many retirees is that their Social Security benefits may be subject to federal income tax. The extent to which they are taxed depends on your “combined income,” which includes your adjusted gross income (AGI), any tax-exempt interest (like from municipal bonds), and half of your Social Security benefits.

- Individual Filers: If your combined income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If your combined income is above $34,000, up to 85% of your benefits may be taxable.

- Joint Filers: If your combined income is between $32,000 and $44,000, up to 50% of your benefits may be taxable. If your combined income is above $44,000, up to 85% of your benefits may be taxable.

Some states also tax Social Security benefits, though many states have eliminated or significantly reduced these taxes. Understanding these thresholds is important for managing your overall tax liability in retirement and can influence decisions about drawing from other retirement accounts (e.g., Roth vs. traditional IRAs).

Integrating Social Security into Your Comprehensive Retirement Plan

Social Security was never intended to be your sole source of retirement income. For most individuals, it replaces only about 40% of pre-retirement earnings, a figure that is lower for high earners. Therefore, it’s crucial to view Social Security as one component of a diversified retirement plan, alongside:

- Personal Savings: 401(k)s, IRAs (traditional and Roth), and other investment accounts.

- Pensions: If you are fortunate enough to have one.

- Other Investments: Real estate, taxable brokerage accounts, etc.

- Continued Work: Part-time employment or consulting.

Strategic planning involves understanding how your claiming age for Social Security interacts with your withdrawal strategies from these other accounts. For instance, delaying Social Security benefits might mean drawing more heavily from your investment portfolio in your early retirement years, or vice-versa. A holistic approach ensures you maximize all available resources.

The Future Outlook: Challenges and Adaptations

Social Security faces ongoing financial challenges due to demographic shifts, including an aging population and lower birth rates, meaning fewer workers are supporting more retirees. Without legislative action, the trust funds are projected to be unable to pay 100% of scheduled benefits at some point in the future (e.g., around the mid-2030s). While this does not mean the program will run out of money entirely (as ongoing payroll taxes will continue to fund a significant portion of benefits), it does suggest potential future adjustments. These could include:

- Increases in the full retirement age.

- Changes to the benefit calculation formula.

- Increases in the payroll tax rate or the earnings subject to taxation.

- Means-testing of benefits.

Staying informed about these discussions and factoring potential changes into your long-term financial planning is a prudent approach. While the exact nature of future reforms remains uncertain, Social Security is a fundamental and enduring program that will likely continue to evolve to meet its obligations.

In conclusion, “earning” with Social Security is a multifaceted concept that hinges on a lifetime of contributions, strategic claiming decisions, and an understanding of the program’s intricate rules. By maximizing your earnings history, choosing an optimal claiming age, leveraging spousal benefits, and understanding the tax implications, you can significantly enhance your financial security in retirement. However, it remains a piece of the puzzle, reinforcing the need for comprehensive personal savings and astute financial planning to secure a comfortable retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.