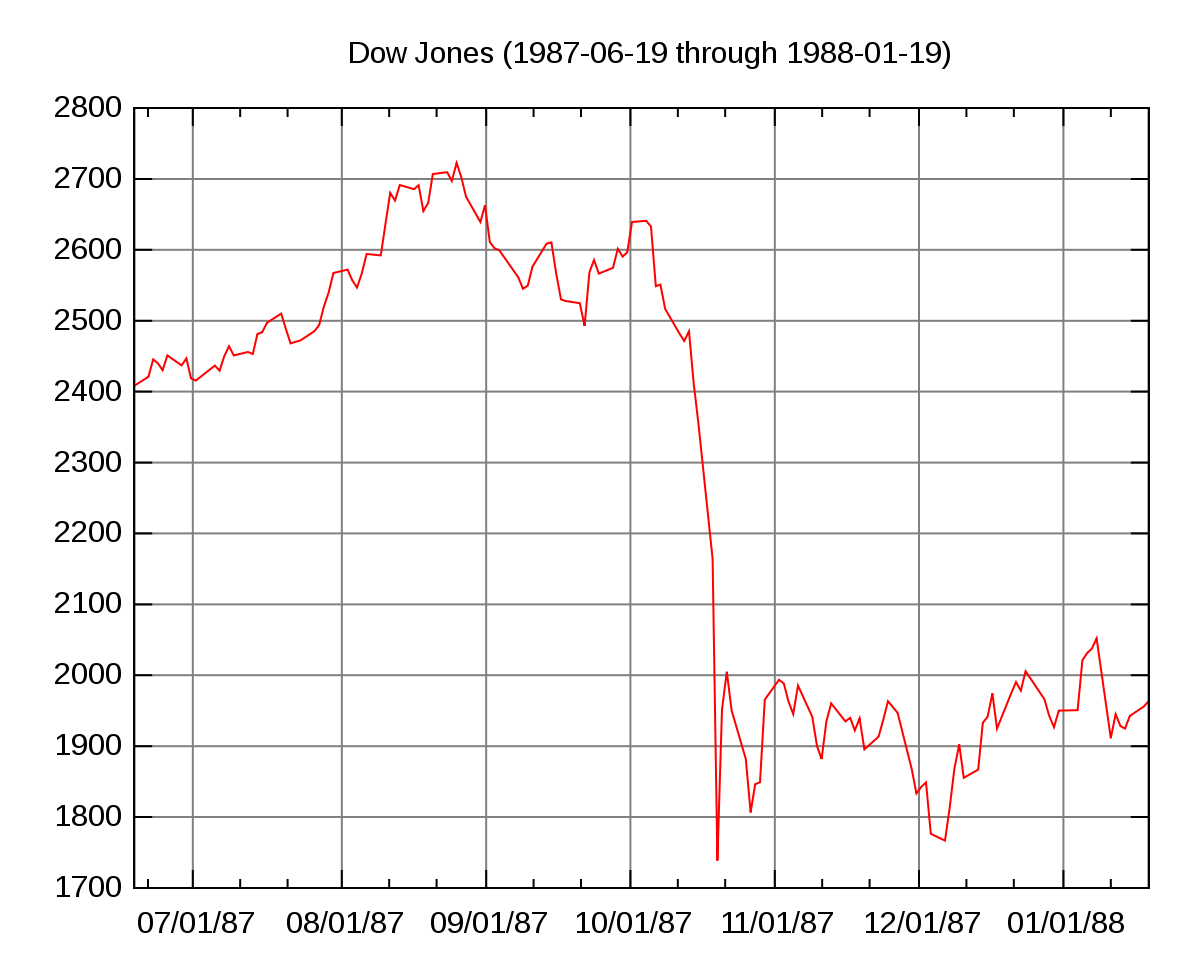

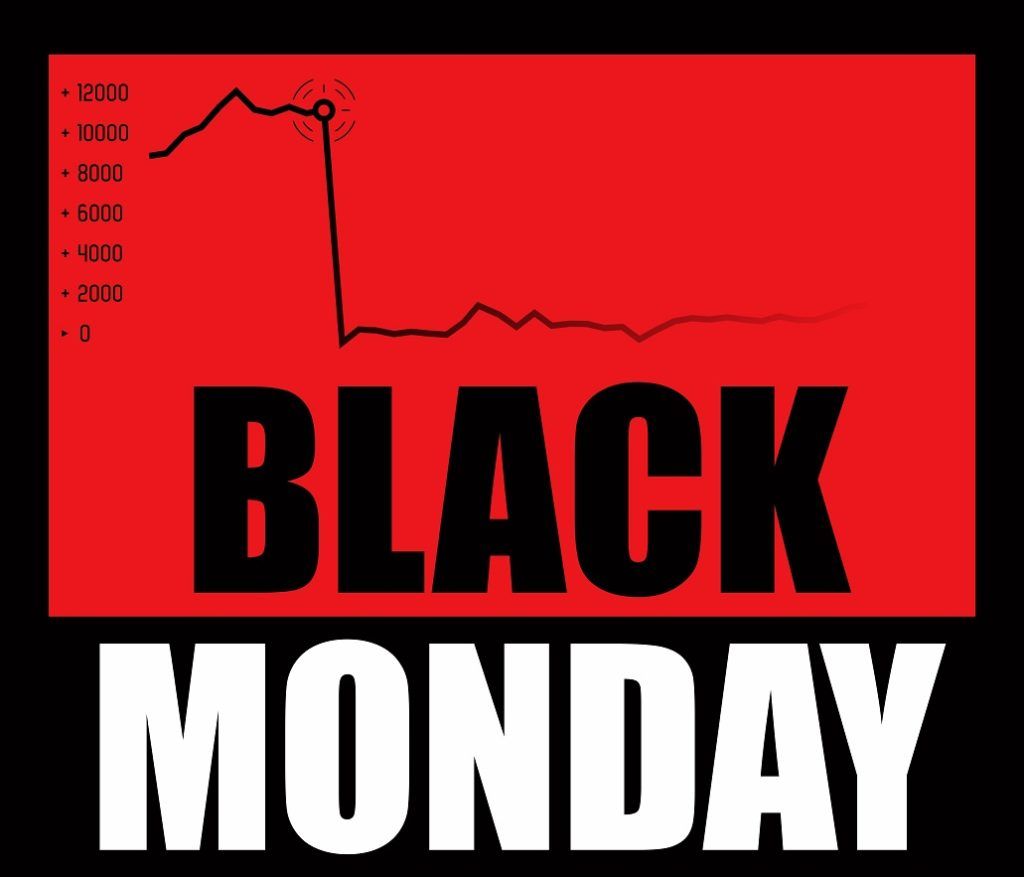

Black Monday, October 19, 1987, stands as one of the most abrupt and severe stock market crashes in modern financial history. On this harrowing day, the Dow Jones Industrial Average (DJIA) plummeted an astounding 508 points, translating to a staggering 22.6% loss in a single trading session. This unprecedented drop wiped out approximately $500 billion in market value from U.S. equities alone, sending shockwaves across global financial markets and leaving investors, policymakers, and economists grappling with the speed and scale of the catastrophe. Unlike previous market downturns that often unfolded over days or weeks, Black Monday delivered its devastating blow in a mere few hours, testing the resilience of the financial system and prompting a profound reassessment of market mechanisms, regulatory frameworks, and investor psychology. It was a pivotal event that reshaped how markets operate, leaving an indelible mark on the landscape of global finance.

The Unprecedented Crash of October 1987

The events of Black Monday did not occur in a vacuum, yet their immediate intensity caught virtually everyone by surprise. The preceding week had already seen significant market volatility, but nothing prepared the world for the freefall that began shortly after the opening bell on Monday, October 19.

A Day of Reckoning on Wall Street

The day began with a palpable sense of unease. Futures markets had opened significantly lower, signaling trouble ahead, and indeed, the stock market followed suit. What ensued was a chaotic cascade of selling orders, overwhelming market makers and brokerage firms. The sheer volume of transactions, combined with the technology of the time, led to severe operational bottlenecks. Trading systems struggled to keep up, order books became backlogged, and liquidity evaporated. Brokers found themselves unable to execute trades at quoted prices, or even at all, exacerbating the panic. Investors, witnessing their portfolios evaporate in real-time, rushed to sell, creating a vicious cycle of falling prices and increased selling pressure. The ticker tape, which usually provided real-time updates, lagged by hours, leaving participants in the dark and fueling uncertainty. By the close of trading, the devastation was clear: a quarter of the market’s value had vanished, marking the largest single-day percentage decline in the DJIA’s history. The magnitude of the loss surpassed even the darkest days of the 1929 crash, which had unfolded over a longer period.

Global Domino Effect

The interconnectedness of global financial markets, though not as digitally advanced as today, was already significant in 1987. The crash in New York immediately triggered similar steep declines across international exchanges. Asian markets, having already closed for the day before the full extent of the U.S. crash was known, were hit hard when they reopened the following day. European markets, which were still open when Wall Street began its descent, experienced rapid and severe downturns. London’s FTSE 100 fell by 10.8% on Black Monday, and by an additional 12.2% the following day. Markets in Hong Kong, Sydney, and Tokyo experienced unprecedented drops, with Hong Kong suspending trading for four days. The synchronized nature of these global declines highlighted the emerging reality of a truly global financial system, where a crisis in one major market could instantly ripple across continents, emphasizing the need for coordinated international responses in times of crisis.

Underlying Causes and Contributing Factors

While the speed of Black Monday was shocking, financial analysts and economists quickly identified several underlying factors that had created a fragile market environment ripe for a severe correction.

Overvaluation and Economic Imbalances

Leading up to October 1987, the U.S. stock market had experienced a robust bull run, with the DJIA nearly tripling in value since 1982. This rapid ascent had led to concerns about market overvaluation, with many stock prices appearing disconnected from fundamental economic indicators. Corporate earnings growth, while solid, was not keeping pace with the exponential rise in stock prices, leading to stretched price-to-earnings ratios. Furthermore, there were growing anxieties about macroeconomic imbalances. The U.S. was grappling with significant trade and budget deficits, often referred to as the “twin deficits.” Concerns about a weakening dollar and rising inflation were also prevalent, prompting the Federal Reserve to raise interest rates in the preceding months. These factors created a general sense of unease among investors, making the market susceptible to negative news and sharp corrections.

The Rise of Program Trading and Portfolio Insurance

A critical, and often controversial, factor cited in the acceleration of the crash was the widespread adoption of new automated trading strategies, particularly “portfolio insurance.” This strategy, designed to protect institutional investors from significant market downturns, involved selling stock index futures when prices fell, effectively hedging against portfolio losses. The theory was that by selling futures, investors could lock in a floor for their portfolio’s value. However, the sheer number of institutions employing this strategy meant that as the market began to fall, their automated programs simultaneously triggered massive sell orders in the futures market.

This had a devastating amplifying effect. Selling in the futures market drove down futures prices, creating a discount relative to the underlying stocks. Arbitrageurs, seeking to profit from this discrepancy, would then sell the underlying stocks and buy futures. This mechanical selling of actual stocks further depressed equity prices, triggering more portfolio insurance sell orders, creating a dangerous feedback loop. The automated, pre-programmed nature of these trades meant that human judgment and discretion were removed from the selling process, accelerating the market’s descent far beyond what might have occurred under traditional, human-driven trading.

Technical Triggers and Market Fragility

Beyond the fundamental and systemic issues, several technical triggers contributed to the immediate panic. A failed bond auction in the days preceding Black Monday highlighted concerns about rising interest rates and inflation, unnerving institutional investors. Geopolitical tensions were also simmering, adding to global uncertainty. The market’s infrastructure itself proved fragile under stress. Outdated communication systems and a lack of standardized trading protocols across different exchanges meant that information flow was slow and fragmented. The Specialist system on the NYSE, responsible for maintaining orderly markets, was overwhelmed. Specialists, who are obligated to buy when there are no other buyers, simply could not absorb the massive selling pressure, leading to wide bid-ask spreads and effectively non-existent markets for many stocks. This lack of liquidity and transparency further fueled investor fear and compounded the selling frenzy.

The Immediate Aftermath and Regulatory Response

The immediate aftermath of Black Monday was characterized by intense fear, widespread uncertainty, and urgent action from central banks and regulators determined to prevent a systemic collapse.

Central Banks Intervene

As the U.S. stock market closed on Black Monday, there was genuine concern that the crisis could spill over into the banking system, potentially triggering a wider economic recession or even depression. Many brokerage firms and banks were facing massive margin calls and liquidity shortfalls. In a swift and decisive move, the Federal Reserve, under Chairman Alan Greenspan, issued a succinct yet powerful statement the morning after Black Monday: “The Federal Reserve, in its capacity as the central bank of the United States, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.” This statement, coupled with immediate actions to inject liquidity into the banking system, was crucial. The Fed encouraged banks to lend freely to brokerage houses and other financial institutions, assuring them that the central bank would provide any necessary funding. Other central banks around the world followed suit, providing liquidity to their respective financial systems. This coordinated and rapid response was instrumental in restoring confidence and preventing a complete meltdown of the financial system.

Reassessing Market Mechanisms

The sheer speed and scale of Black Monday necessitated a comprehensive review of market operations and regulatory frameworks. The Brady Commission, formally known as the Presidential Task Force on Market Mechanisms, was established to investigate the causes of the crash and recommend reforms. Its findings highlighted the interconnectedness of equity and futures markets, the amplifying role of portfolio insurance, and the strains on market infrastructure.

Key recommendations from the Brady Commission and subsequent actions included:

- Implementation of “Circuit Breakers”: These mechanisms are designed to temporarily halt trading across all markets (stocks, options, futures) if prices fall by a certain percentage. The idea is to provide a “cooling-off” period, allowing investors to reassess the situation, process information, and prevent panic selling from spiraling out of control. These circuit breakers have been refined over the years and are now standard practice in global exchanges.

- Enhanced Information Sharing and Coordination: Regulators recognized the need for better communication and coordination between different exchanges (e.g., stock and futures markets) and across international borders.

- Review of Margins and Clearing Procedures: Rules for futures trading margins and the processes for clearing trades were scrutinized and strengthened to ensure that clearinghouses could withstand extreme volatility.

These regulatory changes aimed to build greater resilience into the financial system, mitigating the risk of a similar catastrophic freefall driven by automated trading and panic.

Enduring Lessons and Legacy

Black Monday, while a traumatic event, ultimately served as a profound learning experience for the financial world, shaping risk management practices, regulatory policies, and investor behavior for decades to come.

The Birth of Circuit Breakers

Perhaps the most visible and lasting legacy of Black Monday is the widespread adoption of market-wide circuit breakers. These pre-defined thresholds for market declines are now an integral part of exchanges globally, including the NYSE. For example, the NYSE has different levels of circuit breakers that trigger a trading halt of varying durations, depending on the severity of the market drop. While rarely invoked to their fullest extent, their very existence provides a psychological safety net, assuring investors that there are limits to how far and fast a market can fall in a single day. This innovation fundamentally changed the mechanism of market operations during periods of extreme stress, providing a critical buffer against unbridled panic.

The Human Element in Market Crashes

Black Monday also provided a stark reminder of the enduring power of human psychology in financial markets. Despite the rise of automated trading, the crash underscored how fear, herd mentality, and a lack of confidence can override rational decision-making, leading to irrational selling sprees. The event highlighted the importance of behavioral economics in understanding market phenomena and the need for investors to maintain a long-term perspective, rather than succumbing to short-term panic. It reinforced the idea that while technology can amplify market movements, the underlying drivers often remain rooted in human emotion and perception of value and risk.

Preparing for Future Volatility

In the years following Black Monday, there has been a continuous evolution in risk management practices, particularly for institutional investors. Greater emphasis is now placed on stress testing portfolios against extreme market scenarios, diversifying assets more effectively, and having robust liquidity management plans. Regulatory bodies have also matured, developing more sophisticated surveillance tools and international cooperation agreements to monitor and respond to potential systemic risks. While no market is entirely immune to corrections or even crashes, the lessons of Black Monday have led to a more robust, albeit still imperfect, global financial architecture better equipped to handle periods of extreme volatility. It serves as a perennial reminder that while financial innovation can bring efficiency, it also necessitates careful oversight and a deep understanding of potential unintended consequences. The continuous balancing act between fostering innovation and safeguarding market stability remains a central challenge for financial policymakers, echoing the profound insights gleaned from that fateful Monday in October 1987.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.