The year 1929 remains a stark reminder in financial history, etched into the collective memory as the beginning of one of the most severe economic downturns the world has ever witnessed. The stock market crash of 1929, often synonymous with “Black Tuesday,” was not merely a single event but a series of catastrophic declines that signaled the end of the “Roaring Twenties” and ushered in the Great Depression. Understanding the sheer magnitude of this crash requires delving into the specifics of its initial impact, its prolonged effects, and the underlying vulnerabilities that led to such an unprecedented financial collapse. For anyone interested in investing, business finance, or personal finance, the lessons of 1929 are invaluable, illustrating the profound risks of unchecked speculation and the critical importance of sound economic policy and regulation.

The Unprecedented Scale of the 1929 Market Collapse

The stock market crash of 1929 was a cataclysmic event that unfolded over several days, wiping out billions of dollars in wealth and shattering investor confidence. The scale of the collapse was unlike anything seen before, leaving an indelible mark on financial markets and the global economy.

Black Thursday: The Initial Jolt

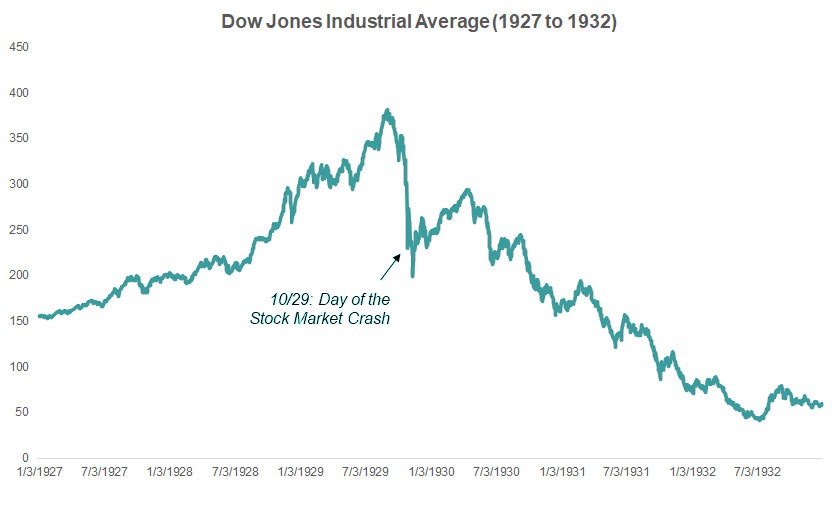

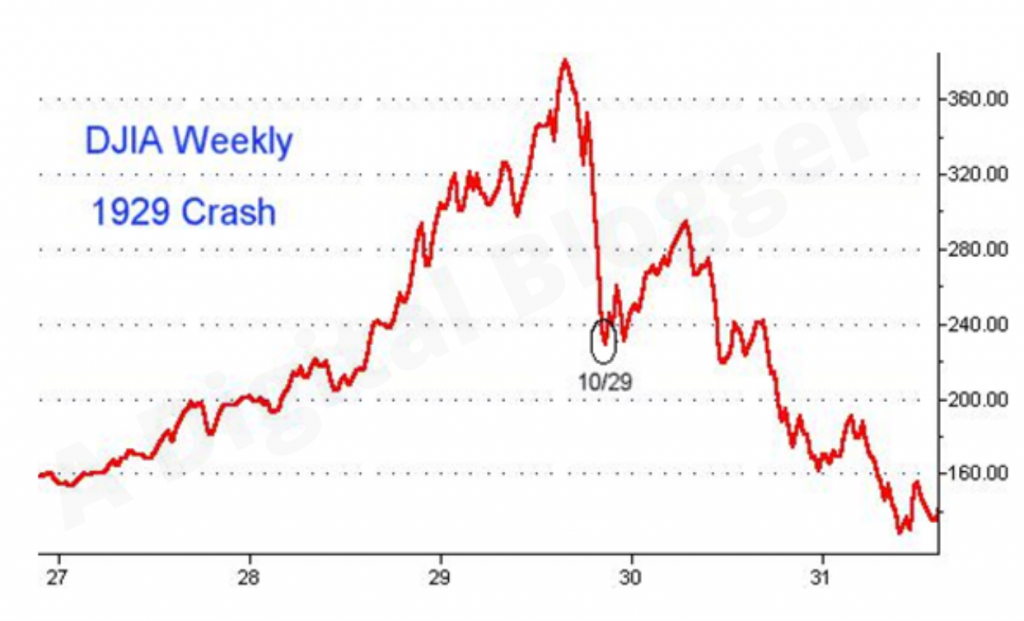

The first major tremor occurred on Thursday, October 24, 1929, a day now infamously known as Black Thursday. Prior to this, the market had been experiencing a period of decline from its September peak, but nothing prepared investors for the panic that ensued. On Black Thursday, the market opened to heavy selling, and by midday, the Dow Jones Industrial Average (DJIA) had plunged by approximately 11% from the previous day’s close. Panic gripped Wall Street as brokers struggled to keep up with the overwhelming volume of sell orders. Rumors spread like wildfire, exacerbating the fear. In an attempt to stem the tide, a group of leading bankers, including J.P. Morgan Jr. and Charles E. Mitchell, pooled their resources to buy up large blocks of shares, notably at prices above the prevailing market rate, to demonstrate confidence and stabilize the market. This intervention did provide a temporary reprieve, and the market managed to recover some losses by the end of the day, closing down a more modest 2.1%. However, the damage to investor psychology was done, and the foundation of confidence had been irrevocably shaken.

Black Monday and Black Tuesday: The Devastating Descent

The brief recovery seen on Friday and Saturday proved to be a false dawn. The true catastrophe unfolded on Monday, October 28, 1929, or Black Monday. With the weekend to reflect, investors returned to the market en masse, determined to sell their holdings before prices plummeted further. This time, there was no coordinated banking intervention strong enough to halt the cascade. The selling pressure was relentless and widespread. On Black Monday, the DJIA fell by an staggering 12.82%, closing at 260.64 points, with trading volume reaching a then-record 9.2 million shares.

The nightmare continued on Tuesday, October 29, 1929, forever etched in history as Black Tuesday. The panic reached its zenith. Small investors, alongside large institutions, frantically tried to liquidate their positions. The ticker tape ran hours behind, creating an atmosphere of utter chaos as investors had no real-time understanding of their losses. On Black Tuesday, the market dropped another 11.73%, with an unprecedented 16.4 million shares traded—a record that would not be broken for nearly 40 years. In just two days, the market lost over 23% of its value. By the close of trading, an estimated $14 billion of market value had evaporated on Black Tuesday alone, contributing to a total loss of approximately $30 billion over the four major days of the crash (October 24, 28, 29). This figure was more than the entire cost of World War I to the United States.

The Lingering Aftermath: A Prolonged Downturn

While Black Thursday, Black Monday, and Black Tuesday mark the most dramatic initial plunges, the stock market’s decline was far from over. The crash was not a single event but the beginning of a prolonged bear market that would last for years. After the initial shock, the market continued to slide, albeit at a less frenzied pace, throughout the remainder of 1929 and into the early 1930s.

The DJIA’s peak before the crash was 381.17 on September 3, 1929. By its lowest point in the bear market, on July 8, 1932, the Dow had fallen to a mere 41.22 points. This represented a staggering 89% decline from its pre-crash peak. It took more than two decades, until November 1954, for the Dow Jones Industrial Average to finally recover to its pre-crash levels of September 1929. This prolonged and devastating decline underscores that the 1929 crash was not just a blip but a fundamental revaluation of assets and a deep, systemic shock to the financial world.

Unpacking the Causes: Why the Market Imploded

The sudden and severe collapse of the stock market in 1929 was not due to a single factor but rather a confluence of economic vulnerabilities, speculative excesses, and a lack of regulatory oversight that had built up over the preceding decade.

Speculative Mania and Margin Buying

The “Roaring Twenties” were characterized by an unprecedented period of economic growth and widespread optimism, fueling a speculative frenzy in the stock market. Many Americans, enticed by the prospect of quick wealth, poured their savings into stocks. The most dangerous aspect of this speculation was the widespread practice of margin buying. Investors could purchase stocks by paying only a small percentage (often as little as 10-20%) of the stock’s value upfront, borrowing the rest from their brokers. As long as stock prices rose, this strategy magnified returns. However, it also magnified losses. When prices began to fall, brokers issued “margin calls,” demanding that investors deposit more funds to cover their loans. Unable to do so, many investors were forced to sell their shares, irrespective of price, to repay their debts, thus accelerating the market’s downward spiral.

Economic Fragilities and Uneven Distribution of Wealth

Beneath the glittering surface of the Roaring Twenties lay significant economic weaknesses. Key sectors, such as agriculture, had been struggling for years due to overproduction and falling prices, diminishing the purchasing power of a large segment of the population. Furthermore, the decade saw a growing uneven distribution of wealth. While some prospered immensely, a large portion of the population did not share equally in the economic boom. This meant that consumer demand, the engine of economic growth, was not robust enough to sustain the inflated production levels, leading to an oversupply of goods and services that consumers couldn’t afford to buy. Factories began to cut production, and unemployment started to tick up even before the crash.

Lack of Regulation and Oversight

The financial markets of the 1920s operated with remarkably little government oversight. There were no robust regulatory bodies like today’s Securities and Exchange Commission (SEC) to monitor trading practices, ensure transparency, or protect investors. Manipulative practices, such as “pools” of wealthy investors artificially inflating stock prices before dumping them, were common. There were also no strict rules against insider trading or requirements for companies to disclose accurate financial information. This lack of regulation created an environment ripe for fraud, misinformation, and excessive risk-taking, making the market vulnerable to sharp corrections.

International Economic Instability

The global economic landscape also played a role. Post-World War I, many European nations struggled with war debts and reparations, particularly Germany. The United States, having emerged as a global creditor, lent heavily to these countries. This intricate web of international debt and trade imbalances made the global economy fragile. When the U.S. stock market crashed and American banks began to call in foreign loans, it triggered a chain reaction, exacerbating economic woes across Europe and contributing to a worldwide depression.

The Rippling Economic Consequences and the Great Depression

The stock market crash of 1929 was not merely a financial event; it was the catalyst that triggered a devastating cascade of economic consequences, ushering in the Great Depression, a period of profound economic hardship that affected millions globally.

Bank Failures and Credit Crunch

One of the most immediate and crippling effects of the crash was on the banking system. Many banks had invested heavily in the stock market themselves or had lent large sums of money to investors for margin buying. When the market crashed, these loans became worthless, and the value of their stock holdings plummeted. This led to widespread bank insolvencies. As public confidence eroded, a wave of bank runs began, with depositors frantically withdrawing their savings, fearing their banks would fail. Lacking federal deposit insurance (which didn’t exist until 1933), many banks simply ran out of cash and were forced to close, wiping out the life savings of millions of Americans. The ensuing credit crunch meant that businesses could not obtain loans to expand or even maintain operations, further stifling economic activity.

Mass Unemployment and Deflation

As businesses faced dwindling demand and could not secure credit, they were forced to cut production, reduce wages, and, most devastatingly, lay off workers. Unemployment skyrocketed from a pre-crash low of 3.2% in 1929 to an agonizing high of nearly 25% by 1933. Millions of Americans lost their jobs, their homes, and their livelihoods. This mass unemployment led to a dramatic decrease in consumer spending, creating a vicious cycle. With less money circulating, prices for goods and services plummeted, a phenomenon known as deflation. While lower prices might seem beneficial, deflation actually made the situation worse, as it increased the real value of debts, making it harder for individuals and businesses to repay loans, and discouraged investment, as businesses waited for prices to fall further.

Global Repercussions

The economic crisis quickly spread beyond the borders of the United States. Given the interconnectedness of the global economy, especially the web of war debts and reparations, the U.S. crash reverberated worldwide. As American banks called in their loans, European economies, already fragile, spiraled into their own depressions. International trade collapsed as countries imposed tariffs to protect domestic industries, further shrinking global markets. The severe economic contraction in the U.S. and Europe directly contributed to political instability in many nations, laying the groundwork for future global conflicts.

Enduring Lessons for Investors and Regulators

The traumatic experience of the 1929 crash and the subsequent Great Depression served as a harsh, but ultimately transformative, lesson for policymakers, financial institutions, and individual investors. The fallout spurred fundamental changes in how financial markets are regulated and how economic crises are managed.

The Birth of Modern Financial Regulation

Perhaps the most significant long-term consequence was the creation of a robust regulatory framework designed to prevent a similar catastrophe. In the aftermath of the crash, the U.S. government enacted landmark legislation aimed at restoring confidence and ensuring market integrity. The Securities Act of 1933 mandated transparency in securities offerings, requiring companies to provide investors with comprehensive financial information. The Securities Exchange Act of 1934 created the Securities and Exchange Commission (SEC), a federal agency tasked with regulating the stock market, overseeing exchanges, and protecting investors from fraud and manipulation. Furthermore, the Glass-Steagall Act of 1933 separated commercial banking from investment banking, aimed at reducing speculative risks in the banking sector (though largely repealed in 1999, aspects of its intent have resurfaced in modern discussions). The establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 provided government insurance for bank deposits, ending bank runs and restoring public trust in the banking system. These measures fundamentally reshaped the financial landscape and are cornerstones of modern financial stability.

Diversification and Risk Management

For individual investors, the 1929 crash underscored the critical importance of diversification and prudent risk management. The collapse demonstrated the perils of putting all investment eggs in one basket, particularly in highly speculative assets. Investors learned that chasing quick gains without understanding underlying risks could lead to catastrophic losses. The event highlighted the need for a balanced portfolio that includes various asset classes, industries, and geographies to mitigate risk. It also emphasized the danger of excessive leverage (margin buying) and the importance of investing within one’s means, without relying on borrowed funds for speculative ventures. The principle of “don’t put all your money in one stock” became a foundational tenet of sound investing.

The Dangers of Unchecked Speculation

The 1929 crash stands as a historical testament to the destructive power of unchecked speculation and herd mentality in financial markets. The period leading up to the crash was characterized by irrational exuberance, where stock prices became detached from the underlying economic fundamentals. The lesson is that while markets can experience periods of significant growth, they are also prone to irrational bubbles, fueled by greed and overconfidence. Regulators, central banks, and investors must remain vigilant against the signs of asset bubbles, understanding that “this time is different” is often the most dangerous phrase in finance.

Comparing 1929 to Modern Market Crises

While the 1929 crash was unique in its scale and impact, subsequent financial crises have occurred, prompting comparisons and highlighting both enduring patterns and critical differences in the financial landscape.

Similarities in Market Psychology

Despite technological advancements and regulatory changes, human psychology remains a constant in financial markets. The 1929 crash, much like the dot-com bubble burst of 2000 or the 2008 financial crisis, was characterized by periods of irrational exuberance followed by widespread panic and fear. Herd mentality, where investors follow the actions of the majority rather than rational analysis, played a significant role in both the run-up and the collapse in 1929. Similarly, the rapid spread of fear and the rush to liquidate assets are common features across different crises. The cycle of greed and fear, speculation and deleveraging, continues to be a driving force in market dynamics.

Key Differences: Regulation and Economic Structure

The most significant differences between 1929 and modern crises lie in the regulatory framework and the structure of the global economy. As discussed, the post-1929 era gave birth to robust financial regulations, central bank interventions, and social safety nets that did not exist before. Today, institutions like the SEC, FDIC, and the Federal Reserve have broad powers to stabilize markets, protect investors, and inject liquidity during crises.

Modern economies also have more diverse structures, with greater emphasis on services and technology, compared to the industrial and agricultural focus of the 1920s. Furthermore, the understanding of macroeconomics and the tools available to governments and central banks (e.g., fiscal stimulus, monetary policy) are far more sophisticated. This means that while market corrections and recessions are inevitable, the systemic collapse and prolonged depression seen after 1929 are less likely, largely due to these learned lessons and implemented safeguards.

The Evolving Landscape of Financial Crises

While the specific triggers and mechanisms of financial crises evolve (e.g., subprime mortgages in 2008, tech bubbles in 2000), the underlying principles of risk management, valuation, and market psychology remain relevant. Each crisis offers new lessons, particularly concerning the interconnectedness of global finance and the emergence of new asset classes and financial instruments. The 1929 crash serves as a foundational case study, reminding us that continuous vigilance, adaptive regulation, and a deep understanding of market history are essential for fostering a resilient financial system capable of weathering future storms. For investors, the enduring takeaway is the importance of long-term perspective, disciplined investing, and a healthy respect for the market’s capacity for both immense growth and significant downturns.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.