In an era of economic uncertainty and ever-present financial goals, the question “how much do I save?” transcends mere curiosity; it becomes a fundamental inquiry into one’s financial health and future prosperity. This article delves into the critical aspects of personal saving, offering insights, strategies, and tools to help you understand your current saving habits and cultivate a robust financial future. Saving isn’t just about putting money aside; it’s about building resilience, achieving dreams, and securing peace of mind.

The Imperative of Saving: Why “How Much Do I Save” Matters

Understanding your savings rate and actively engaging in saving practices is foundational to a stable and prosperous financial life. It’s the bedrock upon which all other financial goals are built. The act of saving transforms abstract desires into tangible realities, offering a shield against life’s unpredictability and a clear path toward desired milestones.

Building a Foundation of Financial Security

At its core, saving is about creating a safety net. An emergency fund, typically three to six months’ worth of living expenses, is the first and most critical saving goal for many. This fund acts as a buffer against unforeseen circumstances such as job loss, medical emergencies, or unexpected home repairs, preventing these events from spiraling into financial crises or forcing reliance on high-interest debt. Beyond emergencies, a healthy savings account fosters a general sense of security, knowing you have options and aren’t living paycheck to paycheck. This financial cushion can alleviate stress and empower you to make decisions not out of necessity, but out of choice.

Achieving Short-Term and Long-Term Goals

Whether you dream of a down payment on a house, a child’s education, a relaxing vacation, or a comfortable retirement, saving is the vehicle that drives you there. Short-term goals, like buying a new car or taking a trip, might require a few months to a few years of dedicated saving. Long-term goals, such as retirement planning, demand decades of consistent contributions and strategic investing. By quantifying “how much do I save,” you can allocate funds specifically to these goals, track your progress, and stay motivated. Each deposit is a step closer to turning those aspirations into reality, making the abstract idea of a goal feel concrete and achievable.

Navigating Unexpected Financial Challenges

Life is unpredictable, and financial challenges are an inevitable part of the journey. From a sudden income reduction to an unforeseen medical bill, these events can derail financial plans if you’re not prepared. A robust savings habit not only covers these immediate shocks but also provides the flexibility to absorb larger, less frequent challenges, such as unexpected home repairs or the need for a new appliance. Moreover, consistent saving fosters a discipline that helps you make sound financial decisions even under pressure, reinforcing good habits and preventing impulsive choices that could exacerbate a difficult situation.

Unpacking Your Current Savings Landscape

Before you can optimize your savings, you need a clear picture of where you stand. This involves honest introspection, diligent tracking, and a willingness to confront your financial realities. Understanding your current “how much do I save” metric is the first step toward improvement.

Calculating Your Current Savings Rate

Your savings rate is a powerful metric: it’s the percentage of your gross income that you save after taxes and other deductions. To calculate it, subtract your monthly expenses from your net income, and then divide the remainder by your net income. For example, if your net monthly income is $4,000 and you save $800, your savings rate is 20%. Regularly calculating and tracking this rate provides a tangible measure of your financial progress. It helps you identify whether you are meeting your targets and where adjustments might be needed. This metric is a personal benchmark, often more indicative of financial health than simply the absolute dollar amount saved.

Distinguishing Between Different Types of Savings

Not all savings are created equal, and understanding their purposes is crucial for effective financial planning.

- Emergency Fund: As discussed, this is a readily accessible fund for unexpected financial shocks. It should be kept in a liquid account, like a high-yield savings account.

- Retirement Savings: Funds explicitly designated for your post-working years, typically held in tax-advantaged accounts like 401(k)s, IRAs, or Roth IRAs. These usually involve long-term investments.

- Short-Term Goal Savings: Money earmarked for specific, nearer-term goals (e.g., a vacation, a new gadget, a car down payment).

- Long-Term Goal Savings (Non-Retirement): Funds for larger, distant goals like a home down payment, a child’s college education, or starting a business.

Segmenting your savings into these categories helps prevent “raiding” your retirement fund for a vacation and provides clarity on the purpose of each saved dollar.

The Role of Budgeting in Understanding Your Finances

A budget is not merely a restrictive tool; it’s an illuminating financial map. By meticulously tracking your income and expenditures, a budget reveals exactly where your money goes each month. This clarity is indispensable for answering “how much do I save.” It highlights areas of overspending, identifies opportunities for cutting back, and ensures that your financial resources are aligned with your priorities. Without a budget, you’re essentially flying blind, making it nearly impossible to consistently increase your savings or even understand your current savings capacity. Regular budget reviews allow you to adjust to changing circumstances and maintain control over your financial destiny.

Setting Realistic and Ambitious Saving Benchmarks

Once you understand your current situation, the next step is to set targets. While personal circumstances dictate specific figures, general guidelines and benchmarks can provide a valuable starting point for optimizing your savings.

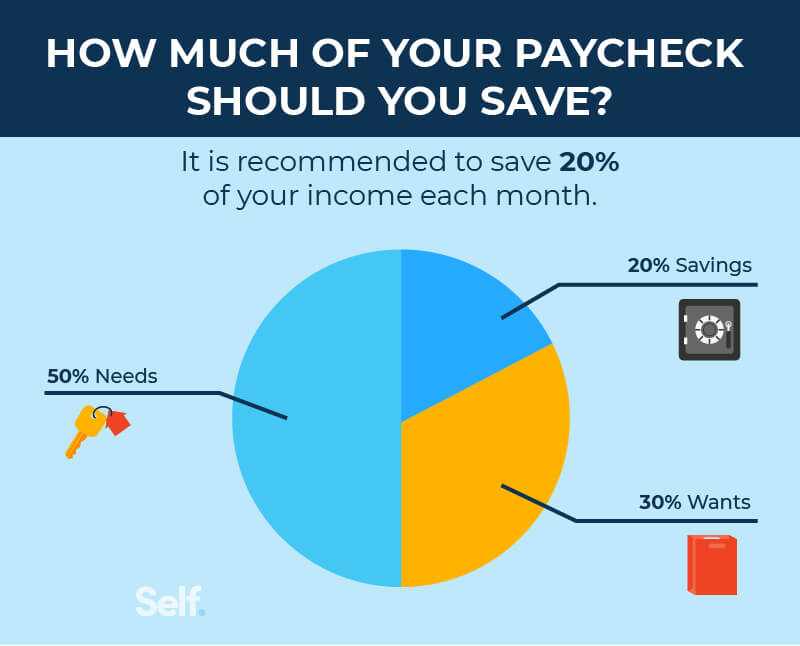

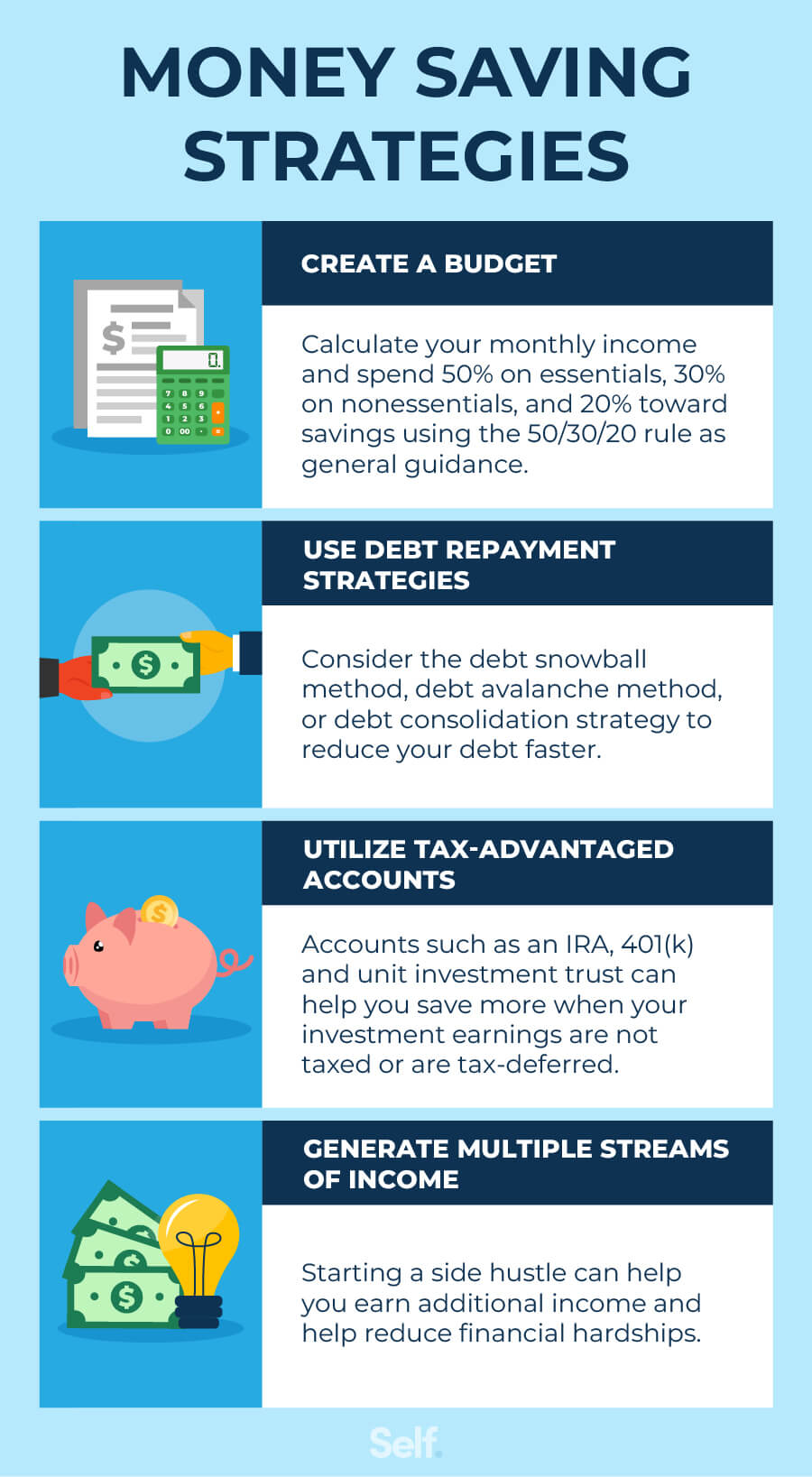

The 50/30/20 Rule and Other Guiding Principles

One popular guideline is the 50/30/20 Rule:

- 50% of your after-tax income goes towards Needs (housing, utilities, groceries, transportation, insurance).

- 30% goes towards Wants (dining out, entertainment, hobbies, travel, shopping).

- 20% goes towards Savings and Debt Repayment (emergency fund, retirement, investments, extra payments on high-interest debt).

This rule provides a straightforward framework for allocating your income. While not universally applicable to everyone, it serves as an excellent starting point for assessing if your spending aligns with healthy saving habits. Other principles suggest saving at least 10-15% of every paycheck, or specific amounts by certain ages (e.g., one times your salary by age 30, three times by age 40).

Tailoring Savings Goals to Life Stages

Your saving capacity and priorities will naturally evolve throughout your life:

- Early Career: Focus on building an emergency fund and starting retirement contributions early to leverage compound interest.

- Mid-Career/Family Building: Saving for a home, children’s education, and increasing retirement contributions become paramount.

- Late Career: Maximize retirement contributions, potentially paying off your mortgage, and planning for healthcare costs in retirement.

- Retirement: Shifting from saving to smart withdrawal strategies and managing your existing nest egg.

Recognizing these life stages helps you adjust your “how much do I save” targets and ensures your financial planning remains relevant and effective.

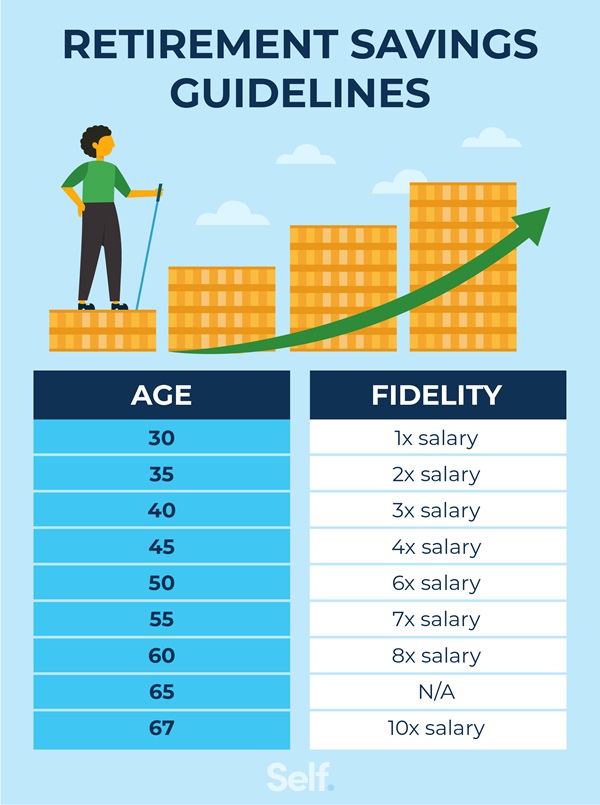

Benchmarking Against Financial Milestones (Emergency Fund, Retirement)

Specific financial milestones provide concrete benchmarks:

- Emergency Fund: Aim for 3-6 months of living expenses. Some experts recommend up to 12 months for higher job insecurity.

- Retirement: General advice suggests having specific multiples of your salary saved by certain ages (e.g., 1x salary by age 30, 3x by age 40, 6x by age 50, 8x by age 60, 10x by retirement). These are aggressive targets but provide a good aspirational framework.

- Down Payment: For a home, 20% of the purchase price is often recommended to avoid private mortgage insurance (PMI).

These milestones offer clear, measurable goals that can guide your saving efforts and provide a sense of accomplishment as you reach each one.

Practical Strategies to Boost Your Savings Potential

Knowing how much you should save is one thing; consistently saving that amount is another. Implementing practical strategies can transform your intentions into tangible results, significantly improving your “how much do I save” answer.

Automating Your Savings for Consistency

One of the most effective strategies is to automate your savings. Set up an automatic transfer from your checking account to your savings or investment accounts immediately after payday. This “pay yourself first” approach ensures that saving happens before you have a chance to spend the money. Automation removes the need for willpower or remembering to save, making it a consistent and reliable habit. Even small, regular transfers accumulate significantly over time thanks to the power of compounding.

Identifying and Reducing Unnecessary Expenses

A detailed budget often reveals “money leaks”—small, recurring expenses that add up without much perceived value. This could include unused subscriptions, daily coffee purchases, excessive dining out, or impulse buys. Conduct a “spending audit” to identify these areas. Challenging your habits and making conscious choices to reduce or eliminate unnecessary spending can free up significant funds for saving. Even minor adjustments, like packing lunch instead of buying it, can lead to substantial savings over a year.

Exploring Avenues for Income Growth

While cutting expenses is vital, increasing your income offers another powerful lever for boosting savings. Consider:

- Negotiating a raise: Research industry benchmarks and make a compelling case to your employer.

- Starting a side hustle: Monetize a skill or hobby, such as freelancing, tutoring, or selling handmade goods.

- Investing in your skills: Acquire new qualifications or certifications that can lead to higher-paying roles.

- Leveraging passive income streams: Explore options like rental properties, dividend stocks, or high-yield savings accounts (though often modest).

Any additional income, even if small, can be directed entirely towards savings, accelerating your progress towards financial goals.

Optimizing Debt Management to Free Up Cash Flow

High-interest debt, such as credit card balances, can severely impede your ability to save. The interest payments consume a significant portion of your income, leaving less for savings. Prioritizing debt repayment, particularly high-interest debt, is a crucial step in optimizing your cash flow. Strategies like the “debt snowball” or “debt avalanche” can help you systematically eliminate debt. Once high-interest debts are paid off, the money previously allocated to interest payments can then be redirected towards savings and investments, dramatically increasing your “how much do I save” capacity.

Leveraging Financial Tools and Mindset for Sustained Saving

In today’s digital age, a plethora of tools and a robust financial mindset can empower you to not only track but also enhance your saving efforts, making the journey towards financial freedom more manageable and effective.

Digital Tools and Apps for Tracking Progress

Technology has revolutionized personal finance, offering powerful tools to simplify budgeting and saving:

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), or Personal Capital connect to your bank accounts, categorize transactions, and provide visual summaries of your spending and saving. They can help you identify trends, set goals, and stick to your budget.

- Investment Apps: Platforms like Acorns, Betterment, or Fidelity allow you to easily set up automated investments, even with small amounts, and track the growth of your retirement or long-term savings.

- High-Yield Savings Accounts: Online banks often offer significantly higher interest rates than traditional brick-and-mortar banks, allowing your emergency fund or short-term savings to grow faster.

These tools provide convenience, insights, and motivation, making it easier to monitor your “how much do I save” metric and stay on track.

Cultivating a Savings-Oriented Mindset

Saving isn’t just about numbers; it’s also about psychology. Cultivating a positive, proactive savings mindset is crucial for long-term success. This involves:

- Delayed Gratification: Resisting immediate temptations for greater future rewards.

- Mindful Spending: Making conscious decisions about every purchase, aligning it with your values and goals.

- Financial Literacy: Continuously educating yourself about personal finance, investing, and economic principles.

- Goal Visualization: Regularly reminding yourself of your financial goals to stay motivated.

A strong savings mindset transforms saving from a chore into an empowering habit, leading to sustained financial growth.

Seeking Professional Guidance When Needed

While self-management is commendable, there are times when professional guidance can be invaluable. A certified financial planner (CFP) can help you:

- Create a personalized financial plan: Tailored to your specific goals, risk tolerance, and life stage.

- Optimize investment strategies: Guide you through complex investment vehicles and diversification.

- Plan for major life events: Such as retirement, college funding, or estate planning.

- Navigate complex tax situations: Maximize tax efficiency in your saving and investment strategies.

For those with significant assets, complex financial situations, or simply a desire for expert reassurance, a financial advisor can provide clarity and accelerate your journey toward answering “how much do I save” with confidence and strategic insight. They can help you see the bigger picture and make informed decisions that align with your long-term aspirations.

Conclusion

The question “how much do I save” is far more than a simple query about a number; it’s an invitation to take control of your financial destiny. By understanding the importance of saving, meticulously analyzing your current financial landscape, setting realistic yet ambitious benchmarks, implementing practical strategies, and leveraging both technological tools and a robust financial mindset, you can transform your saving habits. Consistent saving builds a foundation of security, enables the achievement of diverse goals, and provides the freedom to navigate life’s challenges with resilience. Embrace the journey of saving, and watch as your financial future becomes clearer, more secure, and ultimately, more prosperous.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.