Embarking on the journey to homeownership is a significant financial milestone, often representing the largest investment most individuals will make in their lifetime. At the heart of this journey lies the mortgage – a loan specifically designed to help you purchase real estate. But with a multitude of financial institutions vying for your business, the fundamental question often arises: “Where do you get a mortgage?” Navigating the diverse landscape of mortgage providers requires understanding their distinct offerings, processes, and the unique advantages each brings to the table. This comprehensive guide will demystify the options, empowering you to make an informed decision that aligns with your financial goals and homeownership aspirations.

Traditional Lenders: The Cornerstones of Mortgage Finance

For decades, conventional financial institutions have served as the bedrock of the mortgage industry. These entities are characterized by their physical presence, established reputations, and a broad range of financial products beyond just home loans. While their processes may sometimes feel more formal, they offer stability, personalized service, and a comprehensive suite of banking services that can be appealing to many borrowers.

Banks: Retail Giants with Diverse Offerings

Commercial banks are arguably the most recognizable source for mortgages. From large national chains to regional and local community banks, they offer a wide array of mortgage products, including conventional fixed-rate and adjustable-rate mortgages (ARMs), jumbo loans for high-value properties, and sometimes even proprietary portfolio loans.

Advantages: Banks often provide competitive interest rates, especially for existing customers who have checking or savings accounts with them. They offer the convenience of in-person consultations, allowing borrowers to sit down with a loan officer to discuss their options face-to-face. Furthermore, banks can streamline the process for customers who already have established banking relationships, sometimes offering preferred rates or quicker approvals. Their extensive branch networks also provide accessibility for document submission and inquiries.

Considerations: While banks offer many benefits, their approval processes can sometimes be more stringent, adhering closely to traditional underwriting guidelines. Their large size might also mean less flexibility for borrowers with unique financial situations that fall outside standard parameters. It’s crucial to compare rates and terms across different banks, as they can vary significantly.

Credit Unions: Member-Focused Alternatives

Credit unions are non-profit financial cooperatives owned by their members. This ownership structure often translates to a member-centric approach, where profits are returned to members in the form of lower fees, higher savings rates, and often, more competitive loan rates.

Advantages: Credit unions are renowned for their personalized customer service and a community-focused ethos. They often offer very competitive interest rates on mortgages, which can be particularly attractive for those looking to minimize borrowing costs. Because they are member-owned, they may also be more flexible with borrowers who have less-than-perfect credit scores or unique financial circumstances, provided they meet membership criteria. Many also provide educational resources to help members navigate the home-buying process.

Considerations: Membership is typically required to obtain a loan from a credit union, which might involve meeting specific eligibility criteria (e.g., living in a certain area, working for a particular employer, or belonging to an affiliated organization). While some credit unions have expanded their reach, their branch networks might be smaller than large commercial banks, potentially limiting physical access for some borrowers.

Mortgage Lenders: Specialized Expertise

Unlike banks and credit unions, mortgage lenders specialize exclusively in home loans. These companies focus solely on originating, processing, and closing mortgages. Some prominent examples include Quicken Loans (Rocket Mortgage), Wells Fargo Home Mortgage, and Guaranteed Rate.

Advantages: As specialists, mortgage lenders often possess deep expertise in the intricacies of various loan products and the underwriting process. They can offer a wider variety of niche mortgage products designed for specific situations (e.g., construction loans, doctor loans, or loans for self-employed individuals). Their focused business model often allows for more efficient processing and faster closing times compared to general banks. Many also have robust online platforms for application and tracking.

Considerations: While competitive, their rates and fees might not always be the absolute lowest, so comparison shopping is still essential. They typically do not offer other banking services like checking or savings accounts, meaning you’ll need to maintain separate relationships for those needs. The customer service experience can vary significantly between different mortgage lenders, so researching reviews and reputation is vital.

Modern Avenues: Navigating the Digital Mortgage Landscape

The digital revolution has profoundly impacted the mortgage industry, introducing new players and streamlined processes. Online platforms and independent advisors have emerged as powerful alternatives, offering convenience, competitive pricing, and sometimes, a more personalized touch through dedicated human assistance.

Online Mortgage Lenders: Convenience and Competitive Rates

The rise of online mortgage lenders has transformed how many people shop for and secure a home loan. These lenders operate primarily, or exclusively, online, reducing overhead costs and often passing those savings on to borrowers in the form of lower rates.

Advantages: Online lenders are celebrated for their unparalleled convenience. You can research, apply, upload documents, and track your loan progress from the comfort of your home, at any time of day. Their cost structure often allows them to offer highly competitive interest rates and lower fees compared to some traditional brick-and-mortar institutions. Many online platforms use advanced technology to simplify the application process, providing quick pre-approvals and clear progress updates. They also make it easy to compare different loan products and terms side-by-side.

Considerations: While convenient, the lack of a physical branch might be a drawback for those who prefer face-to-face interaction or assistance with complex questions. The entirely digital process might require borrowers to be comfortable with technology and uploading sensitive financial documents online. Customer service quality can vary widely, so it’s important to choose a reputable online lender with strong reviews and responsive support channels.

Mortgage Brokers: Your Independent Guide

A mortgage broker acts as an intermediary between you (the borrower) and multiple lenders. Unlike a direct lender, a broker doesn’t fund the loan themselves but instead helps you find the best mortgage product and rate from their network of banks, credit unions, and wholesale lenders.

Advantages: Brokers are invaluable for borrowers seeking expert guidance and access to a broad market of loan products. They do the legwork of shopping around for you, comparing rates, fees, and terms from numerous lenders to find the most suitable option for your specific situation. This can save you significant time and potentially secure a better deal than you might find on your own. Brokers can be particularly beneficial for first-time homebuyers or those with unique financial profiles, as they can navigate complex scenarios and identify niche products. They are often paid by the lender, though some may charge a borrower fee, so clarity on compensation is important.

Considerations: While brokers offer convenience, ensure that they are transparent about their fees and the lenders they work with. A broker might not have access to every lender in the market, so it’s wise to still do some independent research. The quality of service heavily depends on the individual broker’s expertise, ethics, and responsiveness.

Fintech Platforms: Streamlining the Application Process

Financial technology (Fintech) companies are increasingly disrupting the mortgage space by leveraging technology to enhance efficiency, transparency, and the overall customer experience. These platforms often combine elements of online lenders with innovative digital tools.

Advantages: Fintech platforms excel at digitizing and automating much of the mortgage application and underwriting process. This can lead to faster approvals, reduced paperwork, and a more seamless user experience. Many utilize AI and machine learning to analyze financial data quickly, provide personalized recommendations, and even offer predictive analytics regarding interest rate trends. They often emphasize user-friendly interfaces and robust digital security measures. Some platforms also integrate with other financial tools, offering a more holistic view of a borrower’s financial health.

Considerations: While highly efficient, some advanced fintech solutions might still be evolving, and their human support systems might not be as extensive as traditional lenders. Borrowers need to be comfortable with sharing their financial data digitally and trusting the algorithms that drive these platforms. As with any newer technology, it’s crucial to verify their regulatory compliance and track record.

Beyond the Mainstream: Exploring Niche and Government-Backed Options

While banks, credit unions, and online lenders cover the majority of mortgage seekers, certain situations call for specialized financing. Government-backed programs and niche lenders cater to specific demographics or unique property types, providing crucial access to homeownership for many who might not qualify for conventional loans.

Government-Insured Loans (FHA, VA, USDA): Tailored Support

These loans are not originated by the government directly but are insured by government agencies, making them less risky for lenders and thus more accessible to a wider range of borrowers.

FHA Loans: Insured by the Federal Housing Administration, these loans are popular among first-time homebuyers and those with lower credit scores. They typically require a lower down payment (as low as 3.5%) and have more lenient credit requirements than conventional loans. However, they come with mandatory mortgage insurance premiums (MIP) for the life of the loan or a significant portion of it.

VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are an invaluable benefit for eligible active-duty service members, veterans, and surviving spouses. They often require no down payment, no private mortgage insurance (PMI), and offer competitive interest rates. VA loans are one of the most powerful tools for military families to achieve homeownership.

USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed to promote homeownership in eligible rural and suburban areas. They often require no down payment and offer favorable terms to low- and moderate-income borrowers, provided the property is in a designated rural area and the borrower meets income limits.

Advantages: These programs significantly expand access to homeownership for specific populations by offering more flexible eligibility criteria, lower down payment requirements, and sometimes better rates than conventional loans.

Considerations: Each program has specific eligibility requirements for borrowers and properties. They may also come with unique fees (e.g., FHA’s MIP, VA funding fee) and potentially more extensive appraisal processes to ensure property standards are met.

Portfolio Lenders: Flexibility for Unique Situations

Portfolio lenders are financial institutions that originate and hold loans on their own books rather than selling them on the secondary market. This gives them greater flexibility in setting their own underwriting guidelines.

Advantages: Portfolio lenders can be a lifeline for borrowers who fall outside the strict parameters of conventional or government-backed loans. This includes individuals with complex income structures (e.g., self-employed with variable income), unique property types (e.g., non-conforming homes, rural properties), or those with recent credit events that might disqualify them from traditional lenders. Their ability to make exceptions and consider the “whole picture” of a borrower’s financial situation is a significant benefit.

Considerations: Because these loans are held by the lender, they might come with slightly higher interest rates or fees to compensate for the increased risk the lender is taking. The application process might also be more involved, requiring more detailed documentation and explanation of unique circumstances. These lenders are often smaller banks or credit unions, so finding them might require more targeted research.

Private Lenders: Alternative Financing Sources

Private lenders, including individuals, investment groups, or hard money lenders, offer alternative financing solutions, typically for specific, short-term needs or properties that traditional lenders won’t finance.

Advantages: Private lending can be an option for quick closings, loans on properties in disrepair (where traditional financing is difficult), or for borrowers with very poor credit who have a clear repayment strategy. They are often less concerned with traditional credit scores and more focused on the collateral and repayment potential.

Considerations: This option is typically a last resort due to significantly higher interest rates, substantial origination fees, and often shorter repayment terms. It’s crucial to approach private lending with extreme caution, ensure all terms are transparent, and only use it when conventional options are completely exhausted and a clear, profitable exit strategy is in place. It’s generally not suitable for long-term home financing for primary residences.

Key Factors Influencing Your Lender Choice

The decision of where to get a mortgage is multifaceted, extending beyond just the interest rate. A holistic approach considering various financial and service-oriented factors will lead to the most favorable outcome for your specific circumstances.

Interest Rates and Fees: The Cost of Borrowing

The interest rate is arguably the most impactful factor on the total cost of your mortgage over its lifetime. Even a small difference in percentage points can translate into thousands of dollars saved or spent.

H3: Understanding APR vs. Interest Rate: It’s critical to distinguish between the nominal interest rate and the Annual Percentage Rate (APR). The interest rate is solely the cost of borrowing the principal amount. The APR, however, represents the total cost of the loan, including the interest rate, origination fees, discount points, mortgage insurance, and other charges. Comparing APRs provides a more accurate picture of the true cost when evaluating different lenders.

H3: Discount Points and Origination Fees: Many lenders offer the option to “buy down” your interest rate by paying discount points upfront (each point is typically 1% of the loan amount). While this lowers your monthly payment, it increases your closing costs. Origination fees, usually 0.5% to 1% of the loan amount, cover the administrative costs of processing the loan. Carefully weigh whether paying points is financially beneficial over the expected life of your mortgage.

H3: Loan Estimates and Comparison: The Consumer Financial Protection Bureau (CFPB) mandates that lenders provide a standardized Loan Estimate (LE) form within three business days of application. This document details the estimated interest rate, monthly payment, and closing costs. Always request and compare LEs from multiple lenders to ensure you’re getting the best possible deal.

Loan Products and Eligibility: Finding the Right Fit

The type of mortgage product you choose and your eligibility for it are crucial considerations. Not all lenders offer the same range of loans, and not all borrowers will qualify for every product.

H3: Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs): Fixed-rate mortgages offer predictable monthly payments for the life of the loan, providing stability. ARMs, on the other hand, have an interest rate that adjusts periodically after an initial fixed period, which can lead to lower initial payments but introduces interest rate risk. Your risk tolerance and long-term financial plans should guide this choice.

H3: Conventional vs. Government-Backed Loans: As discussed, conventional loans have stricter credit and down payment requirements, while FHA, VA, and USDA loans offer more flexibility for eligible borrowers. Understanding your credit score, down payment availability, and eligibility for specific programs will narrow down your options.

H3: Jumbo Loans and Niche Products: If you’re purchasing a high-value property that exceeds the conforming loan limits set by Fannie Mae and Freddie Mac, you’ll need a jumbo loan. Similarly, some lenders offer niche products for specific professions (e.g., doctors, lawyers) or unique property types. Ensure your chosen lender can accommodate your specific needs.

Customer Service and Reputation: A Smooth Experience

The mortgage process can be complex and sometimes stressful. A lender’s customer service and reputation can significantly impact your experience.

H3: Responsiveness and Communication: Effective communication from your loan officer and support team is paramount. You want a lender who is responsive to your questions, proactive in providing updates, and clear in their explanations. Delays in communication can cause significant stress, especially during time-sensitive transactions.

H3: Online Reviews and Ratings: Before committing, research potential lenders through online review platforms (e.g., Google Reviews, Yelp, Better Business Bureau) and consumer advocacy sites. Pay attention to common themes regarding responsiveness, transparency, and problem resolution. While not every review tells the whole story, patterns of complaints can be red flags.

H3: Local Expertise vs. National Reach: Some borrowers prefer a local lender with deep knowledge of the regional real estate market, while others prioritize the vast resources and potentially lower rates of a national lender. Consider whether localized expertise is important for your specific home purchase.

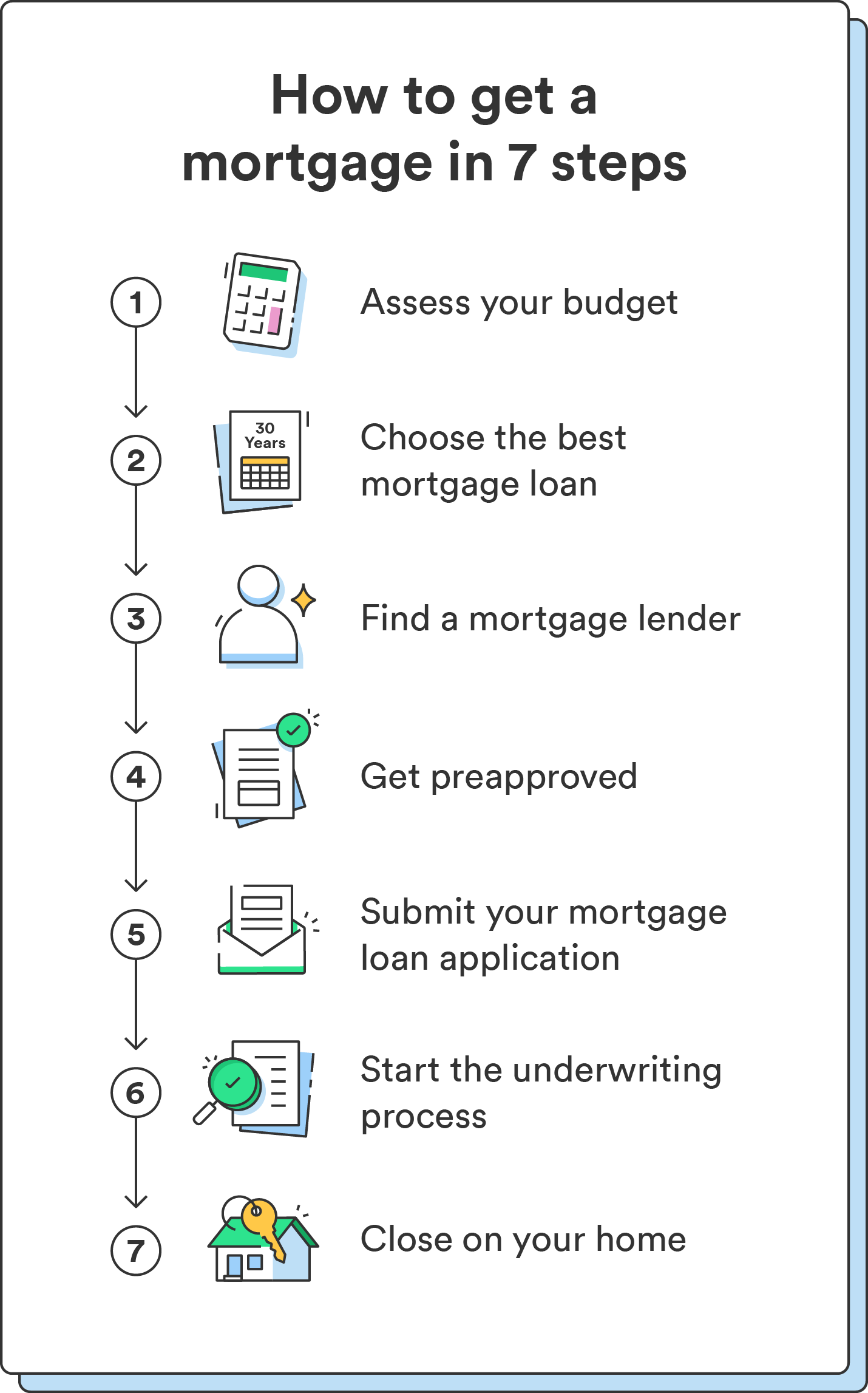

The Mortgage Application Journey: Steps to Success

Once you’ve identified potential lenders, understanding the typical mortgage application journey will help you prepare and navigate the process with confidence, bringing you closer to securing your dream home.

Pre-Approval: Understanding Your Buying Power

The first crucial step is getting pre-approved for a mortgage. This is a formal statement from a lender indicating how much money you are qualified to borrow.

H3: What is Pre-Approval? Unlike a pre-qualification (which is a rough estimate), a pre-approval involves a more thorough review of your financial situation, including a credit check, income verification, and an assessment of your debts. It demonstrates to sellers that you are a serious and qualified buyer, giving you a competitive edge in a hot housing market.

H3: Documentation Required: To get pre-approved, you’ll typically need to provide pay stubs, W-2s, tax returns, bank statements, and information about your debts and assets. Having these documents ready will expedite the process.

H3: Shop Around with Pre-Approvals: Obtain pre-approvals from 2-3 different lenders. This not only gives you options but also helps you compare initial offers and potentially leverage them to negotiate better terms with your preferred lender. Multiple inquiries for mortgage pre-approvals within a short period (typically 14-45 days) are usually counted as a single hard inquiry on your credit report, minimizing the impact on your score.

Gathering Documentation: Preparing for Scrutiny

After pre-approval and once you’ve found a property and made an offer, the full underwriting process begins, requiring extensive documentation.

H3: Essential Financial Records: Expect to provide updated pay stubs, bank statements, investment account statements, and potentially proof of any large deposits. Lenders will want to see a consistent income stream and sufficient funds for your down payment and closing costs.

H3: Tax Returns and Employment Verification: Lenders will typically request two years of tax returns to verify your income history, especially for self-employed individuals. They will also verify your employment directly with your employer to confirm your job status and income.

H3: Property-Specific Documents: Once an offer is accepted, you’ll need to provide the purchase agreement, details about the property, and potentially an appraisal and inspection reports requested by the lender.

Underwriting and Approval: The Final Review

The underwriting phase is where the lender meticulously scrutinizes all your financial information and the property details to assess the risk of lending to you.

H3: Risk Assessment: Underwriters evaluate your creditworthiness (credit score, payment history), capacity (income vs. debt), capital (assets, down payment), and collateral (the property itself). They ensure that the loan meets both the lender’s internal guidelines and any external regulatory requirements.

H3: Conditions and Clear-to-Close: It’s common for underwriters to request additional documents or explanations – these are called “conditions.” Promptly addressing these conditions is vital to avoid delays. Once all conditions are met and approved, the loan receives a “clear-to-close” status.

H3: The Appraisal and Inspection: The lender will order an appraisal to ensure the property’s value supports the loan amount. While not always required by the lender, a home inspection is highly recommended for your protection to identify any potential issues with the property.

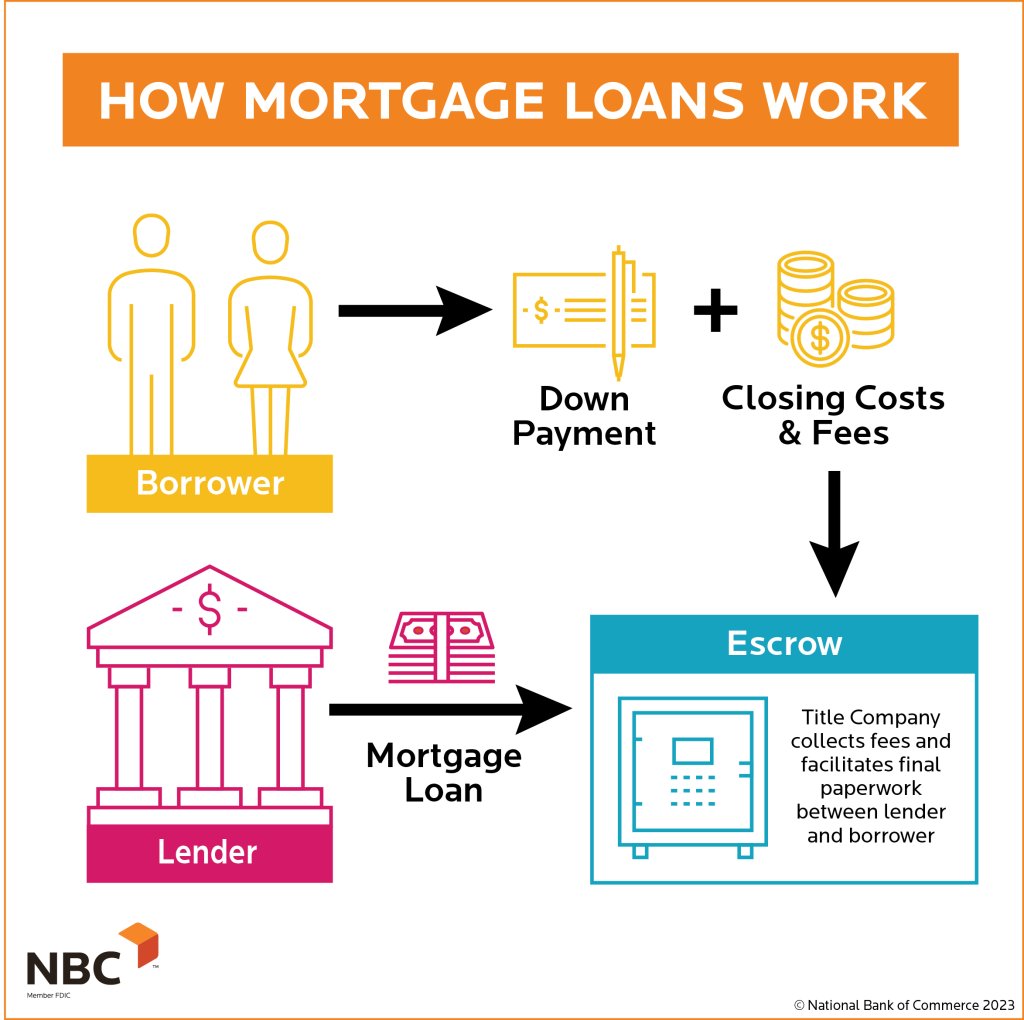

Closing: Securing Your Home

The closing is the final step where all parties sign the necessary paperwork, transfer funds, and the property officially changes hands.

H3: Reviewing the Closing Disclosure: At least three business days before closing, you’ll receive a Closing Disclosure (CD). This document provides a final breakdown of all closing costs, loan terms, and the total amount you need to bring to closing. Compare it carefully with your initial Loan Estimate to ensure there are no unexpected charges.

H3: What Happens at Closing: At the closing appointment, you’ll sign numerous documents, including the promissory note (your promise to repay the loan) and the mortgage or deed of trust (giving the lender a lien on the property). You’ll also provide the funds for your down payment and closing costs, typically via a cashier’s check or wire transfer.

H3: Keys in Hand: Once all documents are signed, funds are disbursed, and the deed is recorded, you officially become the homeowner. The keys are yours, marking the successful completion of your mortgage journey.

Choosing where to get a mortgage is a foundational decision in your homeownership journey. By understanding the diverse landscape of lenders, carefully evaluating your financial situation, and diligently navigating the application process, you can secure a mortgage that aligns with your financial well-being and helps you realize the dream of owning a home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.