In the complex tapestry of personal finance, few concepts hold as much weight and direct impact as the interest rate. It’s a term we hear constantly, from mortgage advertisements to credit card statements, yet its true meaning and implications for our individual financial health often remain shrouded in ambiguity. Understanding “what is my interest rate” isn’t merely about knowing a number; it’s about grasping the fundamental cost of borrowing money and the potential returns on your savings and investments. This knowledge empowers you to make smarter financial decisions, optimize your debt, and grow your wealth more effectively. This article will demystify interest rates, guiding you through their various forms, the factors that shape them, and practical strategies to ascertain and manage your own rates for a more robust financial future.

The Ubiquity of Interest Rates in Your Financial Life

Interest rates are the silent, yet powerful, force driving the economy and shaping personal financial realities. Whether you’re a borrower, a saver, or an investor, interest rates touch nearly every aspect of your financial existence. They represent the price of money – the cost for someone to borrow it, or the reward for someone to lend or save it.

Defining Interest Rates: The Cost or Reward of Borrowing and Lending

At its core, an interest rate is expressed as a percentage of the principal amount – the initial sum of money borrowed or saved. When you borrow money, the interest rate is the charge you pay to the lender for the privilege of using their capital over a specified period. This charge compensates the lender for the risk of lending and for the opportunity cost of not being able to use that money themselves. Conversely, when you save or invest money, the interest rate represents the return you earn from the financial institution or borrower for letting them use your funds. In this scenario, your money is working for you, generating additional income.

The calculation of interest can vary significantly. Simple interest is calculated only on the principal amount, while compound interest, far more common and impactful, is calculated on the principal and on the accumulated interest from previous periods. Understanding this distinction, especially with investments, is key to appreciating the power of compounding over time, which Albert Einstein reputedly called “the eighth wonder of the world.”

Why Understanding Your Interest Rate is Crucial

Knowing your interest rate is not an academic exercise; it’s a critical component of effective financial management. For borrowers, a higher interest rate means a greater total cost for the same amount borrowed, translating into larger monthly payments and a longer repayment period. Conversely, a lower rate can save you thousands over the life of a loan. For savers and investors, a higher interest rate accelerates wealth accumulation, allowing your money to grow more rapidly.

Beyond the immediate financial implications, understanding interest rates enables strategic financial planning. It helps you prioritize debt repayment, choose the right savings vehicles, and evaluate the profitability of investments. It allows you to identify opportunities for refinancing existing loans, negotiate better terms, and forecast the trajectory of your financial goals. In an economy where interest rates are constantly fluctuating, informed decision-making based on this knowledge is paramount.

Deciphering the Different Types of Interest Rates You Encounter

Interest rates are not monolithic; they manifest in various forms, each with distinct characteristics and implications for your finances. Recognizing these different types is fundamental to navigating the financial landscape effectively.

Borrowing Rates: Loans, Credit Cards, and Mortgages

When you borrow money, whether for a house, a car, or daily expenses, you encounter borrowing rates. These are the rates lenders charge you for the use of their funds.

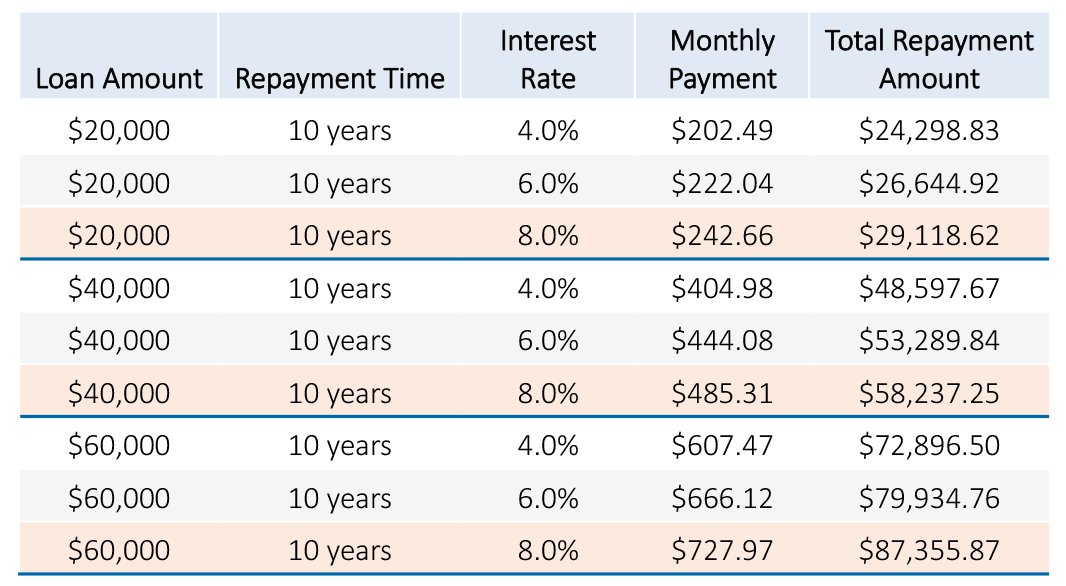

- Mortgage Rates: These are the interest rates applied to home loans. They can be fixed (staying the same for the entire loan term) or adjustable/variable (fluctuating periodically based on a benchmark index). Mortgage rates are heavily influenced by the broader economic environment, central bank policies, and the borrower’s creditworthiness. Even a small difference in a mortgage rate can mean tens of thousands of dollars over a 15- or 30-year term.

- Credit Card APRs (Annual Percentage Rates): Credit card interest rates are typically much higher than other forms of borrowing due to their unsecured nature and convenience. The APR is the annual rate charged for borrowing, and it often varies based on your credit score, the type of card, and promotional offers. Many credit cards have variable APRs, meaning they can change with market conditions.

- Personal Loan and Auto Loan Rates: These are installment loans with fixed repayment schedules. Their interest rates fall somewhere between mortgages and credit cards, depending on the lender, loan term, and borrower’s credit profile. These rates can be fixed or variable, though fixed rates are more common for personal and auto loans.

- Student Loan Rates: These rates can be fixed or variable and are typically set by the government (for federal loans) or private lenders. They are often tied to specific indices and can vary based on the type of loan (e.g., subsidized vs. unsubsidized).

Savings and Investment Rates: The Return on Your Capital

On the flip side, when you save or invest, you are typically earning interest or a return. These are the rates paid to you for lending your money to a financial institution or for investing it.

- Savings Account Rates: These are the interest rates paid on deposits held in savings accounts. They are generally low, reflecting the liquidity and safety of these accounts. High-yield savings accounts typically offer better rates than traditional brick-and-mortar bank accounts.

- Certificate of Deposit (CD) Rates: CDs offer higher interest rates than regular savings accounts in exchange for locking up your money for a fixed period (e.g., 6 months, 1 year, 5 years). The longer the term, generally the higher the interest rate.

- Money Market Account Rates: These accounts offer a blend of savings account liquidity and slightly higher interest rates, often tied to short-term market rates. They may also come with limited check-writing privileges.

- Bond Yields: When you invest in bonds, the “interest rate” is often referred to as the yield. This is the return an investor receives on a bond over a specific period. Bond yields are influenced by economic conditions, inflation expectations, and the creditworthiness of the bond issuer.

Fixed vs. Variable Rates: Understanding the Implications

A critical distinction across all types of interest rates is whether they are fixed or variable.

- Fixed Rates: A fixed interest rate remains constant for the entire duration of the loan or investment. This provides predictability and stability, as your payments or earnings won’t change even if market rates fluctuate. Fixed-rate mortgages are a prime example, offering homeowners consistent monthly payments for decades.

- Variable (or Adjustable) Rates: A variable interest rate can change periodically based on a predetermined benchmark index (e.g., the Prime Rate, SOFR, or Treasury yields) plus a fixed margin. While variable rates can start lower than fixed rates, they introduce uncertainty, as your payments or earnings can increase or decrease over time. Adjustable-rate mortgages (ARMs) and many credit cards feature variable rates.

The choice between fixed and variable rates depends on your risk tolerance, market outlook, and financial goals. Fixed rates offer peace of mind, while variable rates can offer savings if rates fall, but pose a risk if they rise.

Key Factors That Influence Your Personal Interest Rate

While global economic forces play a significant role in setting the general direction of interest rates, several specific factors determine the individual rate you are offered. Understanding these influences is crucial for improving your borrowing power and maximizing your returns.

Your Credit Score: The Cornerstone of Borrowing Rates

Without a doubt, your credit score is the single most important factor influencing the interest rates you receive on loans and credit cards. A credit score is a three-digit number that summarizes your creditworthiness, reflecting your history of managing debt.

- High Credit Scores (e.g., 720+): Individuals with excellent credit scores are considered low-risk borrowers. Lenders view them as highly likely to repay their debts on time. Consequently, they are offered the most favorable, lowest interest rates available. This translates to significant savings over the life of a loan.

- Average Credit Scores (e.g., 620-719): Borrowers with average credit scores will still qualify for credit, but they will likely be offered higher interest rates than those with excellent credit. Lenders perceive a slightly higher risk and price that into the rate.

- Low Credit Scores (e.g., below 620): Individuals with poor credit scores are considered high-risk borrowers. Lenders are more hesitant to extend credit and, if they do, will charge very high interest rates to compensate for the increased risk of default. Sometimes, they may not qualify for conventional loans at all.

Your credit report, which forms the basis of your credit score, details your payment history, amounts owed, length of credit history, types of credit used, and new credit. Regularly monitoring and working to improve your credit score is paramount to securing better interest rates.

Economic Indicators: Central Bank Policies and Inflation

Beyond individual creditworthiness, macroeconomic conditions exert a powerful influence on interest rates across the board.

- Central Bank Monetary Policy: In the United States, the Federal Reserve’s Federal Open Market Committee (FOMC) sets the federal funds rate, a target rate for interbank lending. While not an interest rate you directly pay, changes to the federal funds rate ripple through the entire financial system, influencing the Prime Rate (a benchmark for many variable loans), mortgage rates, and savings account yields. When the Fed raises rates to combat inflation, borrowing costs generally increase. When they lower rates to stimulate economic growth, borrowing becomes cheaper.

- Inflation: Inflation is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. Lenders factor inflation into their interest rates to ensure that the money they are repaid in the future has similar purchasing power to the money they lent today. If inflation is expected to rise, interest rates tend to increase to compensate lenders for the eroding value of future repayments.

- Economic Growth and Stability: A strong, growing economy generally leads to higher demand for credit, which can put upward pressure on interest rates. Conversely, during economic downturns, central banks may lower rates to encourage borrowing and investment.

Loan Specifics and Lender Policies

Finally, the characteristics of the loan product itself and the specific lender’s policies also play a role.

- Loan Type: Different loan products inherently carry different risk profiles, leading to varied interest rates. For instance, secured loans (like mortgages or auto loans, backed by collateral) generally have lower interest rates than unsecured loans (like personal loans or credit cards).

- Loan Term: The length of the loan can influence the rate. Shorter-term loans often have lower rates than longer-term loans because the risk of economic changes over a shorter period is less. However, longer terms usually mean lower monthly payments, which can be attractive despite the higher total interest paid.

- Down Payment/Equity: For secured loans like mortgages, a larger down payment or more equity in the property reduces the lender’s risk, often resulting in a lower interest rate.

- Lender-Specific Policies: Each financial institution has its own lending criteria, risk assessment models, and profit margins. This is why shopping around with different banks, credit unions, and online lenders can result in finding varying interest rates for the same loan product. Some lenders specialize in certain types of borrowers or loans, leading to competitive offers in specific niches.

Practical Steps to Discover Your Current Interest Rates

Knowing your interest rates is the first step toward managing them effectively. Fortunately, finding this information is relatively straightforward, although it may require reviewing a few different sources.

Reviewing Loan Statements and Account Agreements

The most direct way to find your current interest rates is by examining your official financial documents.

- Monthly Statements: For credit cards, mortgages, personal loans, and auto loans, your monthly statement is a treasure trove of information. Look for sections detailing your interest rate (often listed as APR for credit cards), the interest charged in the current billing cycle, and sometimes the overall effective rate.

- Original Loan Documents: When you first took out a loan, you signed an agreement. This document (e.g., mortgage note, credit card agreement, loan disclosure) explicitly states the initial interest rate, whether it’s fixed or variable, and the terms for any rate adjustments. Keep these documents in a safe place for future reference.

- Savings Account Statements: For savings, money market accounts, and CDs, your periodic statements will show the interest rate (or Annual Percentage Yield, APY) you are currently earning, along with the interest credited to your account.

Utilizing Online Banking Portals and Financial Apps

In today’s digital age, accessing your financial information is often just a few clicks or taps away.

- Online Banking Platforms: Log in to your bank or credit union’s online portal. Most platforms provide a clear overview of your accounts, including current balances, interest rates, and recent transactions. Navigate to the specific account (e.g., credit card, mortgage, savings) to find its detailed information.

- Mobile Banking Apps: Similar to online banking, mobile apps offer convenient access to your account details. Look for an “Account Details,” “Summary,” or “Loan Info” section within each account’s page.

- Third-Party Financial Aggregator Apps: Apps like Mint, Personal Capital, or YNAB (You Need a Budget) can consolidate all your financial accounts in one place. Once linked, they often display your current interest rates for various loans and savings vehicles, providing a holistic view of your financial landscape. Be sure to use reputable apps with strong security protocols.

Directly Contacting Your Financial Institutions

If you cannot locate the information through statements or online portals, or if you have specific questions about how your rate is calculated or if it can be adjusted, don’t hesitate to reach out to your financial institution.

- Customer Service Hotline: Call the customer service number provided on your statements or the institution’s website. Be prepared to verify your identity. A representative can provide your current interest rates and answer any related questions.

- In-Person Visit: For more complex inquiries or if you prefer face-to-face interaction, visiting a local branch can be beneficial. A loan officer or personal banker can review your accounts with you.

- Secure Message System: Many online banking platforms offer a secure messaging system, allowing you to send inquiries directly to your bank or credit union in writing. This can be a good option for non-urgent questions and provides a written record of your communication.

When contacting your institution, specify the account you’re asking about and clarify whether you need the current rate, historical rates, or information on how your variable rate is calculated.

Strategies for Managing and Optimizing Your Interest Rates

Once you know your interest rates, the next logical step is to manage and optimize them to your financial advantage. This proactive approach can lead to substantial savings and accelerated wealth growth.

Improving Your Credit Profile

Since your credit score is paramount in determining borrowing rates, investing in its improvement is one of the most effective strategies.

- Pay Bills on Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Utilization: Keep your credit card balances low relative to your credit limits (ideally below 30%). High utilization can signal financial distress to lenders.

- Monitor Your Credit Report: Regularly check your credit report from all three major bureaus (Equifax, Experian, TransUnion) for errors or fraudulent activity. You can get a free report annually from AnnualCreditReport.com. Dispute any inaccuracies promptly.

- Avoid Opening Too Many New Accounts: Each new credit application can temporarily ding your score. Only apply for credit when genuinely needed.

- Maintain a Long Credit History: The longer your credit accounts have been open and in good standing, the better for your score. Avoid closing old, unused credit cards if they don’t have annual fees, as this can shorten your average credit age.

Refinancing and Rate Shopping

For existing loans, exploring refinancing options or simply shopping around can yield significant savings.

- Refinancing Existing Debt: If interest rates have dropped since you took out a loan, or if your credit score has significantly improved, refinancing could allow you to secure a lower interest rate. This is common for mortgages, auto loans, and student loans. Be sure to weigh the savings against any refinancing fees or closing costs.

- Balance Transfers for Credit Cards: If you have high-interest credit card debt, consider a balance transfer to a new card offering a 0% introductory APR. This gives you a window to pay down debt without accruing additional interest, though balance transfer fees often apply. Plan to pay off the balance before the promotional period ends.

- Shop Around for New Loans: Before taking out any new loan, compare offers from multiple lenders – banks, credit unions, and online lenders. Each institution has different lending criteria and pricing models. Don’t just accept the first offer; a few percentage points difference can save you thousands over the loan term.

Accelerating Debt Repayment

Reducing the principal amount of your debt directly reduces the total interest you pay, regardless of the rate.

- Make Extra Payments: If your budget allows, make more than the minimum payment on high-interest debts. Even small additional payments can shave years off a loan and save you considerable interest.

- Debt Snowball or Avalanche Method:

- Snowball: Pay off your smallest debt first to build momentum, then apply that payment to the next smallest, and so on.

- Avalanche: Prioritize paying off debts with the highest interest rates first, which mathematically saves you the most money. Choose the method that best motivates you.

- Bi-Weekly Payments: For mortgages, making bi-weekly payments (half your monthly payment every two weeks) results in one extra full payment per year, significantly reducing the loan term and total interest paid.

Maximizing Returns on Savings

While focusing on debt is crucial, don’t neglect the earning potential of your savings.

- High-Yield Savings Accounts: Move your emergency fund and short-term savings from traditional savings accounts to high-yield savings accounts, often offered by online banks. These typically offer significantly higher interest rates with similar liquidity.

- Certificates of Deposit (CDs): For money you won’t need for a specific period, CDs offer higher guaranteed returns than standard savings accounts. Consider a “CD ladder” strategy to maintain liquidity while earning better rates.

- Explore Investment Options: For long-term goals, consider investments like bonds, which offer yields (their form of interest), or even dividend-paying stocks and mutual funds, which can provide capital appreciation alongside income. Always understand the risks associated with investments.

Understanding “what is my interest rate” is the starting point for a journey toward financial mastery. By consistently monitoring your rates, diligently managing your credit, and strategically applying the insights gleaned from this article, you can transform interest rates from a silent burden into a powerful tool for achieving your financial aspirations. The effort put into optimizing these critical numbers will pay dividends, quite literally, throughout your financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.